High Voltage Transmission Bottlenecks, 266 GW Canceled Projects, $2.5 T Upgrade Need, and FERC Order No. 1920 (2021 to 2026)

Transmission Project Cancellations, 266 GW Dropped Amid 15-Year Delays

The U.S. transmission development crisis has shifted from a theoretical risk to a primary cause of project failure, with systemic permitting and interconnection delays directly leading to the cancellation of 266 GW of power projects in 2025. This structural paralysis, defined by a 15-year development cycle for critical lines, is now the single greatest barrier to accommodating new electricity demand and achieving clean energy objectives.

- Between 2021 and 2024, the primary industry concern was the growing length of interconnection queues, as new renewable projects far outpaced the grid’s ability to connect them, creating a backlog that signaled future constraints.

- The issue became acute in 2025, when nearly 1, 900 power projects were canceled, representing approximately $400 billion in unrealized investment due to economic and policy uncertainty that was severely exacerbated by intractable grid delays.

- Data center demand, particularly from AI, has intensified the problem since early 2025. Utilities like Georgia Power reported a 3.7 GW increase in committed industrial load that the existing grid cannot support without massive, and currently unplanned, upgrades.

- This is not a problem of project availability but a structural inability to build. The average approval timeline for a new transmission line now extends from 12 to 17 years, a timeframe that is fundamentally incompatible with the rapid pace of technological and economic change.

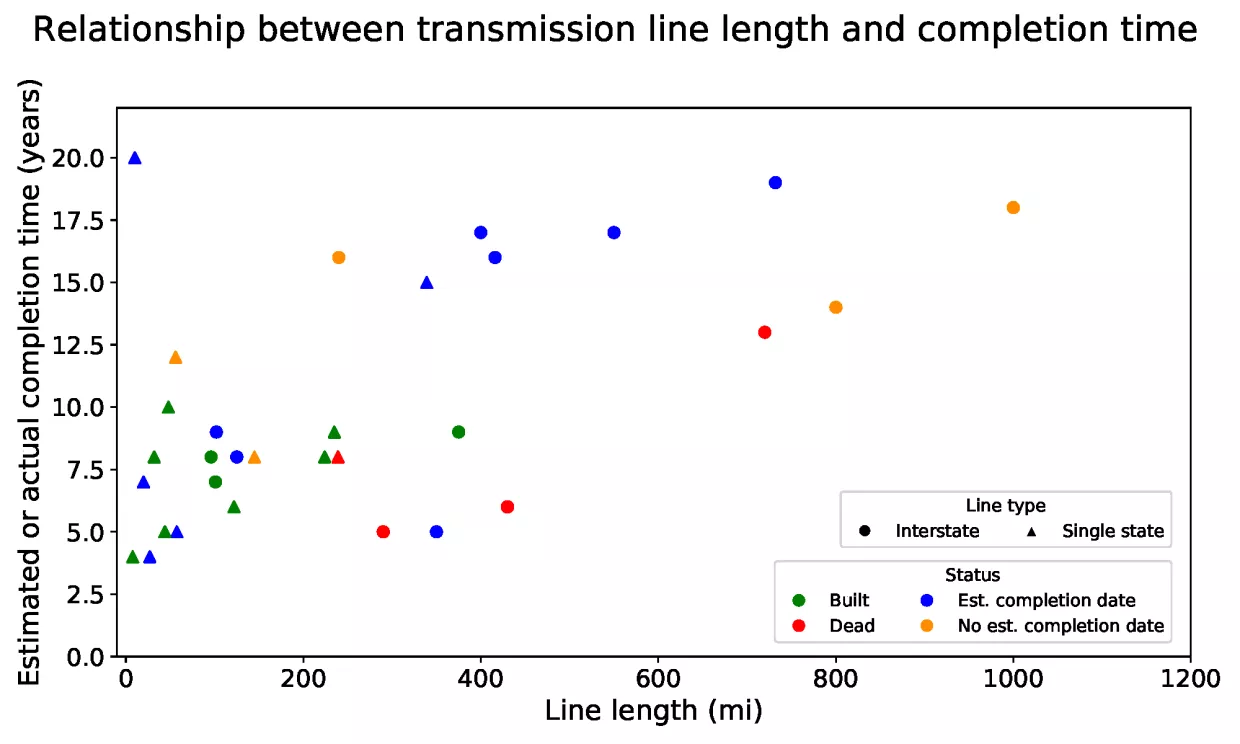

Transmission Project Delays Can Exceed 15 Years

The chart directly visualizes the ’15-year delays’ mentioned in the section heading, breaking down the typical timeline for transmission project development.

(Source: Belfer Center)

$2.5 Trillion Grid Deficit, U.S. Investment Fails to Match Demand Growth

A widening chasm exists between the estimated $2.5 trillion needed for U.S. grid modernization and the available capital, leading to a high rate of project cancellations driven by cost uncertainty and inadequate funding mechanisms. While private capital is available, the extreme financial risks associated with decade-long permitting cycles are a powerful deterrent to investment.

- Prior to 2025, utility capital expenditure plans were increasing steadily but were not calibrated for the exponential surge in demand from data centers and electrification that has since materialized.

- Since 2025, the financial reality has become stark, with a reported $22 billion in clean energy projects canceled in just the first half of the year due to a combination of rising costs, high interest rates, and the prohibitive expense of grid interconnection.

- Federal funding initiatives, such as the DOE’s $1.9 billion opportunity announced in March 2026, represent less than 0.1% of the total estimated need. This highlights the critical reliance on private capital, which is being held back by regulatory risk.

- Cost volatility remains a primary investment deterrent. For example, a proposed mid-Atlantic transmission line saw its projected capital cost more than double in early 2026, making it nearly impossible for developers to secure financing for projects with such unpredictable, long-term development cycles.

Planned Data Center Capacity Skyrockets Past 70 GW

This chart illustrates the scale of the ‘Demand Growth’ that investment is failing to match, pointing to skyrocketing data center capacity as a primary cause of the grid deficit.

(Source: LinkedIn)

Table: Quantified Impact of U.S. Grid Development Bottlenecks

| Metric | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Canceled Capacity | 2025 | Nearly 1, 900 power projects totaling 266 GW were canceled, representing approximately $400 billion in unrealized investment due to economic and policy uncertainty. This demonstrates the direct financial impact of grid-related delays. | Etica Group |

| Canceled Investment | H 1 2025 | $22 Billion in clean energy projects were canceled or delayed, signaling that investment is actively being withdrawn from the sector as developers face insurmountable grid access and cost hurdles. | E 2 |

| Canceled Investment | YTD May 2025 | $14 Billion in clean energy investments were canceled or delayed by May, showing the accelerating pace of project abandonment within the first half of 2025. | Finance & Commerce |

| Average Approval Time | 2026 | Permitting for new transmission lines takes an average of 12 to 17 years, a core metric defining the ’15-year problem’ and the primary bottleneck for new infrastructure. | Silverline Communications |

U.S. Regional Grid Strain, Data Centers Drive Demand in Georgia and Texas

While the transmission crisis is a national issue, its impacts are most acute in specific high-growth regions like the Southeast and Texas, where surging data center and industrial demand is overwhelming local grid capacity. This regional concentration of demand is creating localized reliability risks and forcing urgent, large-scale investment decisions.

- From 2021-2024, grid constraints were broadly distributed, often linked to integrating large-scale renewable energy projects in the windy plains of the Midwest and the sunny deserts of the West.

- Since 2025, a clear geographic pattern has emerged, with states like Georgia seeing unprecedented industrial load growth, primarily from data centers, forcing utilities to fundamentally reconsider their long-term integrated resource plans.

- In Texas, the Public Utility Commission and ERCOT have authorized $33 billion in new long-distance transmission lines to manage the state’s own explosive growth, demonstrating the scale of regional investment required to maintain grid stability.

- FERC’s Order No. 1920, issued in 2024, aims to address this by mandating long-term regional planning. However, its effectiveness is limited because it does not grant federal authority to override the state and local siting opposition that remains the primary bottleneck in these high-demand zones.

Electricity Demand to Surge in Texas, Mid-Atlantic

The chart substantiates the claim of ‘Regional Grid Strain’ by providing a forecast of surging electricity demand in key regions, including ‘Texas’ which is named in the heading.

(Source: Energy Central)

Advanced Conductors Offer 50% Capacity Boost Amid Transformer Supply Chain Issues

The technology to expand and optimize the grid, including mature High-Voltage Direct Current (HVDC) systems and advanced conductors, is readily available. However, its deployment is critically hamstrung by severe supply chain shortages for key components and a regulatory system that fails to incentivize the rapid adoption of these efficiency-boosting solutions.

- Between 2021 and 2024, the industry focus was on proving the value of Grid-Enhancing Technologies (GETs) and advanced conductors through various pilot projects.

- By 2025-2026, the efficacy of these technologies is no longer in question. Studies confirm that reconductoring with advanced materials can double the capacity of existing lines for less than half the cost of a new build, yet widespread deployment remains stalled.

- The primary technological barrier has shifted from innovation to manufacturing. Lead times for essential components like high-voltage transformers have stretched to several years, creating a physical bottleneck that delays even fully permitted and funded projects.

- The supply chain for high-voltage cables and equipment is dominated by a few global players like Prysmian Group, Nexans SA, and Siemens Energy AG. A lack of domestic manufacturing capacity makes the U.S. vulnerable to global supply constraints, prompting large energy consumers like Microsoft to explore on-site power solutions like Small Modular Reactors (SMRs) to bypass grid-related delays entirely.

SWOT Analysis, Transmission Grid Strengths and Execution Risks

The U.S. transmission sector’s primary strength lies in its access to mature technology and available private capital, but this is completely undermined by the critical weakness of a fragmented and painfully slow regulatory system. This internal conflict creates an existential threat where market opportunities from electrification and AI are lost due to project cancellations and constrained economic growth.

- The analysis reveals a core conflict: Strengths like a robust supply chain and market-ready technologies are nullified by the critical Weakness of a broken permitting process.

- Opportunities for massive growth driven by electrification and AI are rapidly turning into Threats of grid instability and canceled investments because the system cannot execute projects fast enough.

- The key change since 2024 is that the “Threat” of mass project cancellations has now become a realized and quantified reality, moving from a hypothetical risk to a primary market signal that is actively deterring new investment.

Solar and Storage Projects Overwhelm Grid Queues

This chart exemplifies a major ‘Execution Risk’ for the SWOT analysis, showing how the grid’s interconnection queues are overwhelmed by solar and storage, a key weakness.

(Source: Cato Institute)

Table: SWOT Analysis for U.S. Transmission Grid Expansion

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Mature HVDC, GETs, and advanced conductor technologies. A deep pool of private capital seeking infrastructure investments. Established global supply chain for key components. | Technologies validated for doubling capacity (advanced conductors). Federal policy support (IRA, IIJA) providing some financial incentives. Key suppliers like Prysmian Group and Siemens have strong order books. | The technology’s value is confirmed, but its impact is limited by non-technical barriers. The problem is execution, not innovation. |

| Weaknesses | Fragmented federal/state permitting. Lengthy NEPA reviews. Lack of clear cost allocation for interregional lines. Nascent awareness of impending demand surge. | A 12 to 17-year permitting timeline is now the accepted baseline. FERC Order No. 1920 attempts reform but lacks federal siting authority. Transformer lead times exceed 2-4 years. | The weakness of the permitting and regulatory system has been validated as the single largest constraint on grid growth, superseding financial or technological issues. |

| Opportunities | Connecting abundant, low-cost renewable energy. Grid modernization for reliability. Supporting the early stages of the EV transition. | Explosive demand growth from AI and data centers (up to 1, 000 TWh by 2030). Industrial onshoring. Broad electrification of transport and buildings. | The scale of the opportunity has grown exponentially, which has in turn made the cost of the system’s failures (i.e., its inability to capture this opportunity) much higher. |

| Threats | NIMBYism and local opposition to new lines. Risk of project delays and cost overruns. Policy uncertainty related to tax credits. | Mass project cancellations (266 GW in 2025). Constrained economic growth as industrial customers cannot secure power. Grid instability and reliability decline. A shift to distributed, balkanized energy systems by large consumers. | The theoretical threat of project failure has become the dominant market reality. The new threat is that major industries will bypass the grid altogether, undermining the entire model for grid investment. |

Scenario Modelling, FERC Order No. 1920 and Federal Permitting Reform

The critical factor for U.S. grid development in the next 18 months is not new technology, but the effective implementation of FERC Order No. 1920 and the success or failure of federal permitting reform. Failure on this front will accelerate the balkanization of the grid as large consumers abandon grid expansion plans in favor of on-site generation to ensure their own energy security.

- If regional planning bodies successfully adopt and implement the long-term planning and cost allocation mandates of Order No. 1920 by late 2026, watch for a potential acceleration of interregional project proposals in 2027-2028, providing the first signal that the logjam could be broken.

- If permitting reform at the federal level fails or is significantly watered down, watch for an increase in project cancellations and a decisive pivot by large energy users like data centers toward dedicated generation, potentially from sources like advanced SMRs from firms like Oklo or on-site gas turbines from providers like Baker Hughes.

- If the supply chain for transformers and high-voltage cables does not see significant domestic investment to shorten lead times, watch for the creation of a “phantom queue” of projects that are fully permitted and funded but simply cannot be built, adding another layer of delay.

Share of Delayed Solar Projects Hovers Around 20%

This chart quantifies a persistent problem—the high share of delayed solar projects—that serves as a critical input and baseline for ‘Scenario Modelling’ the impact of reforms like FERC Order No. 1920.

(Source: Energy Central)

The questions your competitors are already asking

This report covers one angle of the U.S. transmission development crisis. The questions that matter most depend on your work.

- What is the outlook for new high-voltage transmission deployment in the U.S. by 2040, considering the current 15-year development cycle?

- What is the status of FERC Order No. 1920’s implementation? Is it succeeding in accelerating regional transmission planning and cost allocation?

- U.S. transmission investments and funding. Are federal and private capital flows on track to close the $2.5 trillion deficit?

- What are the opportunities for Grid-Enhancing Technologies (GETs) to alleviate near-term bottlenecks while large-scale transmission projects are stalled?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.