Equinor CCUS Infrastructure Strategy, $714 M Northern Lights FID with Shell, 5 Mtpa Capacity, and 3 Major Partnerships (2025)

Equinor Shifts from DAC R&D to Commercial CCS Infrastructure Projects

Equinor’s strategy in 2025 has decisively pivoted from speculative Direct Air Capture (DAC) development towards building and operating large-scale, commercial Carbon Capture and Storage (CCS) infrastructure, positioning itself as a foundational service provider for industrial decarbonization.

- Between 2021 and 2024, Equinor’s focus was on advancing its point-source CCS capabilities, primarily through the Northern Lights project, while acknowledging the high cost of DAC, estimated between $200 and $900 per ton.

- The major shift in 2025 is the concrete financial commitment to this infrastructure-first model, highlighted by the $714 million Final Investment Decision (FID) in March 2025 for Phase 2 of Northern Lights, which triples capacity to 5 million tonnes per year.

- This contrasts with competitors like Occidental Petroleum, which is directly developing large-scale DAC plants like Stratos, demonstrating Equinor’s more conservative, infrastructure-focused approach to the carbon removal market.

- While Equinor maintains a conceptual DAC cost target below $200 per tonne and secured UK government support for a DAC project, its commercial activities and capital are overwhelmingly directed at CO₂ transport and storage, not capture technology itself.

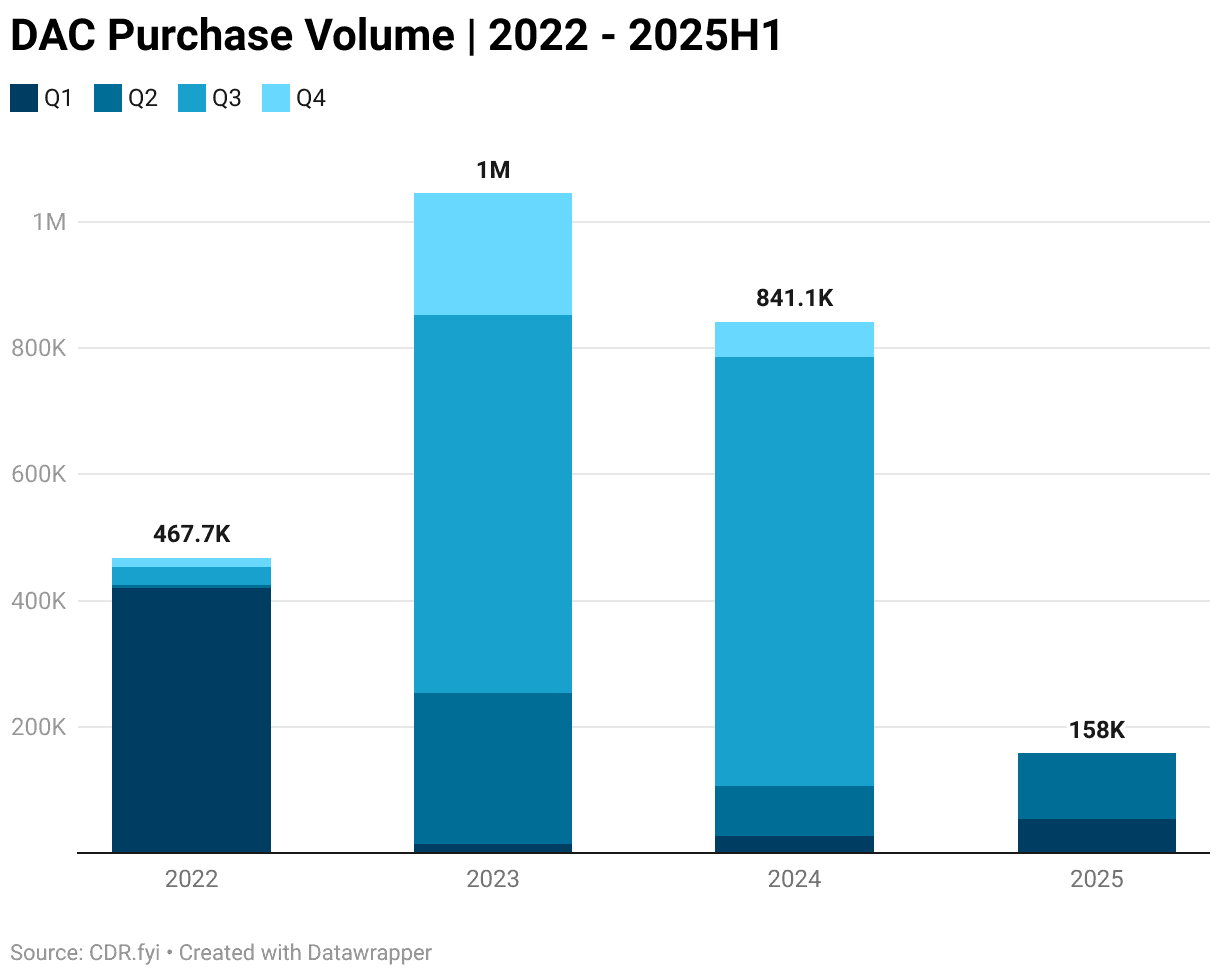

DAC Purchase Volume Declines After 2023 Peak

This chart shows a recent decline in the DAC market, providing external context that aligns with Equinor’s strategic shift away from DAC research and toward commercial CCS infrastructure.

(Source: CDR.fyi)

$714 M Northern Lights Investment, Equinor Deepens CCS Capital Allocation

In 2025, Equinor made significant capital commitments to secure its position in the CO₂ storage market in both Europe and North America, although a separate project cancellation signals sensitivity to rising costs for green initiatives.

- The primary investment is the $714 million (NOK 7.5 billion) FID for the Northern Lights Phase 2 expansion, a joint decision with partners Shell and Total Energies to create a cross-border CO₂ storage service in Europe.

- Equinor expanded its geographic reach by acquiring a 25% interest in the Bayou Bend CCS LLC project in Texas in January 2025, establishing a foothold in a key North American industrial hub.

- However, a critical counter-signal emerged in October 2025 when Equinor cancelled its offshore electrification plans due to rising costs, raising questions about the resilience of its capital-intensive CCS portfolio to similar macroeconomic pressures.

Global CO₂ Storage Reaches 45 Million Tonnes

This chart provides the global context for Equinor’s $714M Northern Lights investment, framing the project’s contribution within the overall scale of the growing carbon storage industry.

(Source: Norwegian SciTech News)

Table: Equinor 2025 Carbon Storage Investments

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Northern Lights (Phase 2) | Mar 27, 2025 | $714 Million FID with partners Shell and Total Energies to triple the project’s CO 2 injection capacity to 5 million tonnes per year, establishing a commercial-scale storage service for European industrial emitters. | Reuters |

| Bayou Bend CCS LLC | Jan 08, 2025 | Acquired a 25% stake in the project, one of the largest potential carbon storage hubs in the US, marking Equinor’s strategic entry into the North American CCS market. | Carbon Credits.com |

Carbon Removal Market Activity in Q1 2025

This chart offers a timely, high-level snapshot of market activity, serving as a macro-level introduction to the specific Equinor investment details provided in the accompanying table for 2025.

(Source: AlliedOffsets)

Equinor Builds CCS Value Chain with Microsoft and Orlen Partnerships

Equinor’s 2025 strategy depends on building a complete commercial ecosystem by forming alliances that span the entire carbon management value chain, from industrial CO₂ supply to digital tracking and infrastructure services.

- From 2021-2024, partnerships were centered on large energy peers like Shell, Total Energies, and BP to de-risk major infrastructure projects like Northern Lights and the Northern Endurance Partnership (NEP).

- In 2025, the strategy broadened to include technology and supply partners. A key agreement with Microsoft in September 2025 aims to develop the digital infrastructure for the CCS value chain, including tracking and market creation.

- To secure CO₂ supply, Equinor partnered with Polish refiner Orlen in March 2025, tapping into industrial emissions from Central Europe and supporting ORLEN’s goal of reaching 4 million tonnes of annual CCS capacity.

- The company also advanced its infrastructure service network, with the NEP joint venture contracting Halliburton in August 2025 for critical well completion and monitoring services in the UK.

Diagram Outlines the CCUS Value Chain

This diagram is a perfect visual aid for the section, as it clearly illustrates the process of capture, transport, and storage that constitutes the CCUS value chain Equinor is building with its partners.

(Source: Oil and Gas Climate Initiative | OGCI)

Table: Equinor 2025 Strategic CCS Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Microsoft | Sep 16, 2025 | Strategic agreement to support the development of CO 2 transport and storage value chains, focusing on digital infrastructure, tracking, and market development. | Data Center Dynamics |

| Halliburton (via NEP) | Aug 06, 2025 | The Northern Endurance Partnership (BP, Equinor, Total Energies) contracted Halliburton to provide completions and monitoring for the UK-based CCS project, securing a key service provider. | Carbon Herald |

| Orlen | Mar 03, 2025 | Collaboration to explore CCS opportunities in Poland, aiming to decarbonize local industry and secure a future CO 2 supply source for Equinor’s storage network. | Reuters |

North Sea vs. US Gulf Coast, Equinor’s Dual CCS Hub Strategy

Equinor’s geographic strategy for carbon management consolidated around two key industrial regions in 2025: solidifying its leadership in the North Sea while establishing a significant new operational base along the US Gulf Coast.

- Between 2021 and 2024, Equinor’s primary focus was exclusively on the North Sea, leveraging its decades of operational experience from the Sleipner field to develop the Northern Lights project in Norway and the Northern Endurance Partnership in the UK.

- The major geographic expansion in 2025 was the entry into the US market through the acquisition of a 25% stake in the Bayou Bend CCS project in Texas, targeting one of North America’s largest concentrations of industrial emissions.

- The partnership with Poland’s Orlen also signals an eastward expansion of its European service area, aiming to transport CO₂ from Central European industries for permanent storage in the North Sea.

- This dual-hub strategy positions Equinor to capitalize on two of the world’s most supportive regulatory environments for CCS: the mature operational landscape of the North Sea and the incentive-rich US market, driven by policies like the 45 Q tax credit.

Fossil Fuels Remain 80% of Global Energy Mix

This chart presents the core rationale for Equinor’s dual-hub CCS strategy by demonstrating the continued prevalence of fossil fuels, which necessitates CCS solutions in major industrial and production zones like the North Sea and US Gulf Coast.

(Source: REN21)

Equinor’s Focus on Mature CCS Storage Over Nascent DAC Technology

In 2025, Equinor prioritized the deployment of commercially mature CO₂ transportation and geological storage technologies, treating Direct Air Capture as a future, high-cost option rather than a present-day investment priority.

- The company’s core technological competence is rooted in its long-term operation of the Sleipner CCS facility since 1996, providing a deep reservoir of data on geological storage, even with the 2025 admission of overstated storage volumes which highlighted monitoring challenges.

- The $714 million investment in Northern Lights Phase 2 confirms a focus on scaling proven technology: ship-based CO₂ transport and sub-seabed injection, which are technologically ready for commercial deployment.

- While Equinor has stated a conceptual ambition for a DAC technology with costs below $200 per tonne, this remains a target. The current market reality, with DAC costs ranging from $200 to over $900 per tonne, justifies the company’s focus on more economical point-source CCS.

- The selection of an Equinor-led DAC project for UK government support in April 2025 indicates continued R&D participation, but it is a small-scale, exploratory effort compared to the massive capital deployed for storage infrastructure.

DAC Cost-Benefit Lags Behind Renewables

This chart provides a clear economic justification for Equinor’s strategy, showing that the cost-benefit of nascent DAC technology is not yet favorable, thus supporting the focus on more mature CCS storage solutions.

(Source: Nature)

SWOT Analysis of Equinor’s CCUS Infrastructure Strategy (2025)

Equinor’s CCUS strategy leverages deep operational strengths and first-mover advantage in storage infrastructure, but it faces significant execution risks from rising costs and reputational challenges related to long-term monitoring.

- Strengths: Unmatched operational experience from the Sleipner project and a clear first-mover advantage in building open-access CO₂ storage infrastructure in Europe with the Northern Lights project.

- Weaknesses: High capital intensity of projects creates vulnerability to cost inflation, as demonstrated by the October 2025 cancellation of offshore electrification plans. Reputational damage from the January 2025 admission of overstating Sleipner storage volumes undermines trust in CCS.

- Opportunities: Growing regulatory support and carbon pricing in Europe, coupled with lucrative incentives like the US 45 Q tax credit, create a strong market pull for CO₂ storage services. Strategic partnerships with industrial emitters like Orlen secure future revenue streams.

- Threats: The economic viability of these “toll road” projects depends entirely on the willingness and ability of industrial customers to pay for decarbonization, which is subject to economic cycles and policy uncertainty. Slower-than-expected cost reduction in capture technologies could limit the volume of CO₂ available for storage.

Equinor’s 2025 Cash Flow Dominated by Oil & Gas

This chart directly supports a SWOT analysis by visualizing a key ‘Strength’: Equinor’s substantial cash flow from its core business, which enables it to fund capital-intensive CCUS infrastructure projects.

(Source: Reclaim Finance)

Table: SWOT Analysis for Equinor’s CCUS Strategy

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strength | Operational experience from Sleipner and leadership position in North Sea CCS development (Northern Lights Phase 1). | Leveraged JV structure with Shell and Total Energies to approve a $714 M expansion of Northern Lights. | Validated ability to de-risk and fund large-scale infrastructure through major energy partnerships. |

| Weakness | High capital dependency for large CCS projects. Reputational reliance on long-term storage claims from Sleipner. | Admitted to overstating Sleipner storage volumes. Cancelled an offshore electrification project due to rising costs. | Confirmed vulnerability to both reputational risk (monitoring accuracy) and macroeconomic pressures (cost inflation). |

| Opportunity | Focused primarily on European market and securing anchor customers for Northern Lights. | Acquired 25% of US-based Bayou Bend project. Partnered with Poland’s Orlen. Signed agreement with Microsoft. | Expanded geographic footprint to North America and broadened partnership ecosystem to include supply and technology partners. |

| Threat | Uncertainty over long-term demand from industrial emitters and pace of policy support. | DAC costs remain high ($200-$900/tonne), limiting a key future CO₂ source. Cost pressures are impacting green projects. | Validated that the business model remains highly dependent on external factors like industrial emitter economics and supportive policy. |

DAC Market to Grow at 61.4% CAGR

This chart provides a quantifiable data point for the SWOT analysis table, representing a significant ‘Opportunity’ or ‘Threat’ related to the high-growth DAC market that Equinor is deprioritizing.

(Source: Market.us)

Equinor’s 2026 Test: Executing the $714 M Northern Lights Expansion on Budget

The central question for Equinor in the coming year is whether it can execute its multi-billion-dollar CCS infrastructure projects on time and on budget in an inflationary environment, a critical test following the cancellation of other green projects due to cost pressures.

- If Equinor successfully manages the construction of Northern Lights Phase 2 without significant cost overruns, watch for the announcement of new commercial offtake agreements to fill the expanded 5 Mtpa capacity, validating the business model.

- This could be happening if the company secures further large-scale storage licenses in the North Sea or announces a Phase 2 FID for its US-based Bayou Bend project, signaling continued investor confidence.

- If Equinor announces delays or budget revisions for its CCS projects, similar to the cancellation of its electrification plans, watch for a potential cooling of investor sentiment towards the capital-intensive carbon management sector.

- This could be happening if there is a lack of new customer agreements for Northern Lights, suggesting that the market price for carbon storage is not yet high enough to justify the costs for many industrial emitters.

Equinor Scenarios Project Future Global Energy Mix

This chart connects the successful execution of the Northern Lights project to the company’s long-term strategic vision, framing the project as a critical test of the feasibility of Equinor’s own energy transition scenarios.

(Source: RFF.org)

The questions your competitors are already asking

This report covers one angle of Equinor’s commercialization strategy for carbon management. The questions that matter most depend on your work.

- Is Equinor’s infrastructure-first CCS strategy a more de-risked investment than Occidental’s direct investment in DAC technology?

- What is actually happening with the Northern Lights project since the $714 M Phase 2 investment decision?

- Which industrial emitters are signing commercial agreements for CO₂ storage with Northern Lights?

- What is the outlook for large-scale CO₂ transport and storage deployment in the North Sea by 2030?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.