Blue Hydrogen Market 2026: Exxon Mobil’s Project Pause Signals a Market Reality Check

Blue Hydrogen Commercial Scale Projects Stall in 2026 Amid Offtake Gaps

Large-scale blue hydrogen projects, previously positioned as the primary near-term decarbonization pathway, encountered a significant commercial roadblock in 2025 due to a fundamental mismatch between ambitious supply plans and actual market demand. The inability to secure binding, long-term offtake agreements became the critical failure point, forcing a strategic re-evaluation across the industry and illustrating the high risks of a supply-driven market.

- Between 2021 and 2024, the industry was defined by announcements of massive projects, most notably Exxon Mobil’s proposed Baytown facility, which targeted production of 1 billion cubic feet per day of blue hydrogen. This period was characterized by a “build it and they will come” approach, assuming industrial customers would readily adopt low-carbon fuels.

- The strategy’s critical flaw was exposed in November 2025 when Exxon Mobil paused its flagship Baytown Blue Hydrogen Project. The company cited a pronounced lack of offtake agreements and the reluctance of potential buyers to absorb the premium costs associated with the carbon capture and storage (CCS) component essential for blue hydrogen production.

- This setback prompted a clear strategic pivot. In the same month, Exxon Mobil announced a partnership with BASF to develop a much smaller demonstration plant for methane pyrolysis. This move represents a hedge towards an alternative technology that avoids gaseous CO 2 streams and creates a potentially valuable solid carbon byproduct, signaling a shift from speculative mega-projects to de-risking new technological pathways.

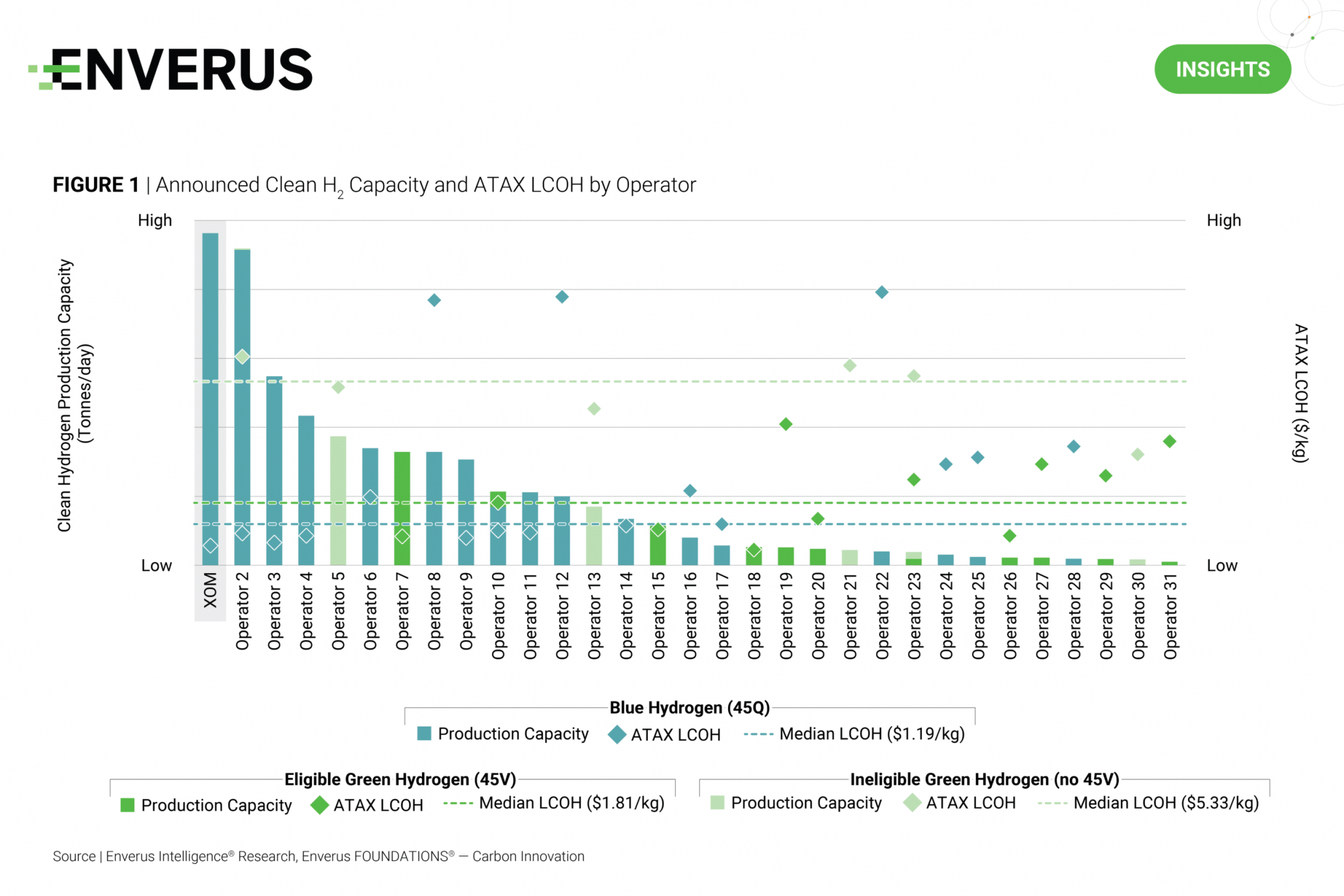

Announced Blue Hydrogen Capacity Faces Market Reality

This chart shows the massive announced production capacities for blue hydrogen, highlighting the scale of the supply-side projects that the section states are now stalling due to offtake gaps.

(Source: Enverus)

Investment Halts: Blue Hydrogen Cancellations Signal Shift in Capital Discipline

The pause of the multi-billion-dollar Baytown project marks a turning point in capital allocation for low-carbon energy, indicating that operators and investors now require firm offtake commitments before sanctioning major blue hydrogen investments. The era of speculative capital deployment based on market projections has been replaced by a demand for proven commercial viability.

Idealized Low-Carbon Growth Strategy Falters

This diagram illustrates the idealized, multi-stage growth path for low-carbon projects, which the section explains is now being rejected by investors demanding proven commercial viability before sanctioning new projects.

(Source: ExxonMobil)

- The 2021-2024 period was driven by large-scale investment announcements, including Exxon Mobil’s planned $20 billion expenditure in its Low Carbon Solutions business and the foundational $4.9 billion acquisition of Denbury to secure CCS infrastructure. These moves were predicated on future demand materializing at scale.

- The November 2025 decision to pause the Baytown Project is the most significant signal of this capital discipline shift. This was not a simple delay but a direct response to a fundamental lack of willing buyers, invalidating the economic assumptions underpinning the initial investment case.

- In contrast, the concurrent investment in the BASF methane pyrolysis pilot, while much smaller, demonstrates a new capital strategy. It focuses on targeted R&D and demonstration-scale projects to validate alternative economic models before committing to large-scale, capital-intensive construction, a prudent move considering the growing investment risks.

Table: Key Project Status Changes in 2025

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Baytown Blue Hydrogen Project | November 2025 | Project paused due to weak market demand and failure to secure offtake agreements. Planned capacity was ~2, 400 tonnes/day, representing a cornerstone of the company’s low-carbon strategy. | Gasworld |

| Baytown Methane Pyrolysis Plant | November 2025 | New demonstration project announced with BASF to produce 2, 000 tons/year of turquoise hydrogen. Represents a strategic pivot to a technology with a different economic profile and co-product value stream. | ESG News |

Hydrogen Partnership Strategy Shifts From Offtake to Technology Validation

Partnership models in the hydrogen sector pivoted sharply in 2025, moving away from securing large-scale international offtake for blue hydrogen and toward collaborations focused on de-risking and validating new production technologies. This change reflects broad market uncertainty and a recognition that technological innovation is required to close the economic viability gap.

Corporate Structure Enables Pivot to Technology

This chart shows how a dedicated “Technology” function supports the “Low Carbon Solutions” business, illustrating the organizational structure that enables the strategic pivot from offtake to technology validation.

(Source: ExxonMobil)

- From 2021 to 2024, Exxon Mobil’s primary partnership efforts, such as agreements with Japan’s JERA and South Korea’s SK Group, were centered on creating future international supply chains for blue ammonia. These alliances were designed to underwrite large production facilities by securing future demand from nations grappling with their own energy security needs.

- The defining shift occurred in November 2025 with the Exxon Mobil–BASF partnership. This collaboration is not about offtake but about joint technology development. Its objective is to prove the technical and economic viability of methane pyrolysis at a demonstration scale of 2, 000 tons per year.

- This evolution indicates a fundamental change in strategic priority. The industry’s central question has shifted from “Who will buy our hydrogen?” to “Can we develop a technology with a superior economic profile that is not solely reliant on the uncertain market for CCS and premium pricing?”.

Table: Evolution of Exxon Mobil’s Hydrogen Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| BASF | November 2025 | Technology development partnership to build a methane pyrolysis demonstration plant. Focus is on validating a new production pathway with a solid carbon co-product, de-risking future investments. | Offshore Energy |

| JERA | January 2024 | Development agreement to explore a large-scale U.S. blue hydrogen and ammonia project for export to Japan. Focus was on securing future international offtake to support a world-scale production facility. | Exxon Mobil News |

| SK Group | July 2022 | Memorandum of Understanding to develop a blue hydrogen and ammonia value chain to supply the South Korean market. The goal was to establish a long-term offtake relationship for a major export project. | Reuters |

U.S. Gulf Coast Hydrogen Hub Faces Headwinds as Baytown Project Halts

The U.S. Gulf Coast’s ambition to establish itself as the world’s preeminent blue hydrogen hub, a central theme from 2021 to 2024, suffered a major setback in 2025 with the pause of Exxon Mobil’s Baytown project. This event exposed the region’s acute vulnerability to weak market demand and the challenges of building an ecosystem based on speculative future offtake.

Visualizing the Blue Hydrogen Hub Value Chain

This diagram outlines the end-to-end blue hydrogen value chain, providing crucial context for what a “hydrogen hub” entails and why the Baytown project halt is a major setback for the Gulf Coast’s ambitions.

(Source: ExxonMobil)

- Between 2021 and 2024, the U.S. Gulf Coast, specifically Texas and Louisiana, became the global epicenter for blue hydrogen investment. Mega-projects announced by Exxon Mobil (Baytown, TX) and Air Products (Ascension Parish, LA), combined with major CCS agreements with industrial players like CF Industries and Nucor, solidified this regional concentration.

- The November 2025 halt of the Baytown facility is a pivotal regional event that casts doubt on the immediate bankability of other large-scale projects in the area that depend on a similar business model of selling premium-priced hydrogen into a nascent market.

- Despite the stall in large-scale production, the region’s importance for technology piloting remains strong, as shown by the new methane pyrolysis plant also being sited in Baytown. This suggests a consolidation of R&D and demonstration activities in the Gulf Coast, even as large-scale production plans are fundamentally re-evaluated.

Blue Hydrogen Stalls at Scale, Forcing Pivot to Emerging Methane Pyrolysis Pilots

While the foundational technologies for blue hydrogen production, steam methane reforming (SMR) and carbon capture (CCS), are mature, their commercial integration at mega-scale was invalidated in 2025 by unfavorable market economics. This commercial failure is now forcing a strategic pivot toward less mature but potentially more economically robust technologies like methane pyrolysis.

Blue Hydrogen and CCS Value Chain Strategy

This chart visualizes the specific blue hydrogen and CCS value chain that the section describes as stalling at a commercial scale, setting the stage for the pivot to emerging technologies.

(Source: ExxonMobil)

- From 2021 to 2024, the dominant strategy relied on combining two established technologies. The selection of Honeywell’s UOP technology for the Baytown project confirmed this industry-wide reliance on proven, off-the-shelf systems to ensure reliability and high capture rates.

- The 2025 pause of the Baytown project was not a technical failure but a commercial one. The market proved unwilling to bear the “green premium” for hydrogen produced with this technically mature but cost-intensive integrated system, especially with ongoing uncertainty in subsidy frameworks.

- The November 2025 announcement of the BASF partnership on methane pyrolysis marks a deliberate pivot. It is a move toward a technology with a lower Technology Readiness Level (TRL) but one that offers a distinct value proposition: the elimination of a gaseous CO 2 stream requiring costly transport and storage, and the creation of a valuable solid carbon byproduct.

SWOT Analysis: Exxon Mobil’s Hydrogen Strategy at a 2026 Crossroads

Exxon Mobil’s hydrogen strategy in 2025 starkly revealed a critical weakness in its market demand assessment, compelling a necessary recalibration away from its traditional strength in large-scale project execution toward new opportunities in technological diversification and market-driven development.

Long-Term Capital Shift to Low-Carbon

This chart models the massive, long-term capital commitment to low-carbon solutions, which visually represents the “strength in executing massive, capital-intensive projects” discussed in the section’s SWOT analysis.

(Source: ExxonMobil)

- The company’s core strength in executing massive, capital-intensive projects was insufficient to overcome the fundamental weakness of an undeveloped market for premium low-carbon fuels.

- The primary threat shifted from competitors to fundamental market economics. The opportunity now lies not in dominating a projected market, but in developing technologies with a viable business case for today’s market.

Table: SWOT Analysis for Blue Hydrogen Market Strategy

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Massive CAPEX commitment ($20 B), world-class project execution skills, and vast natural gas feedstock secured via Pioneer acquisition. | Retains extensive CCS infrastructure via Denbury acquisition and deep R&D capabilities for piloting new technologies. | Core strength shifted from an ability to build large projects to owning the physical and intellectual assets needed for technological pivots. |

| Weaknesses | Heavy reliance on nascent, unproven markets for CCS and premium-priced hydrogen; dependence on future government subsidy frameworks (45 V). | Overestimation of market demand for blue hydrogen was validated by the explicit failure to secure binding offtake agreements for the Baytown project. | A theoretical market risk was confirmed as a critical, project-halting commercial failure, exposing a major flaw in the initial strategy. |

| Opportunities | Dominate the U.S. Gulf Coast blue hydrogen market through first-mover advantage and scale, creating a new revenue stream. | Pivot to alternative technologies like methane pyrolysis (BASF partnership) that create new value streams (solid carbon) and have different cost structures. | The opportunity shifted from market-share dominance in a speculative market to achieving technological leadership in alternative pathways with more robust economics. |

| Threats | Competition from other blue hydrogen developers (Air Products) and the rapidly falling costs of green hydrogen. | The primary threat materialized: weak market demand and buyer unwillingness to pay the CCS premium. Regulatory uncertainty and geopolitical risk continue to affect long-term planning. | The most immediate threat was validated to be fundamental market economics and slow customer adoption, not competition. |

2026 Outlook: Watch for Demand-Driven Projects Over Supply-Side Speculation

The critical signal for the hydrogen market in 2026 is a definitive shift away from large, speculative supply-push projects. The focus will turn toward smaller, modular, and demand-driven initiatives that are co-located with and underwritten by firm anchor customers, reducing market risk before major capital is committed.

Hydrogen Generation Market Forecast to 2030

This chart provides a quantitative forecast for the hydrogen market’s growth, offering a concrete financial outlook that provides context for the section’s discussion of future demand-driven projects.

(Source: MarketsandMarkets)

- If this happens: If the methane pyrolysis pilot with BASF demonstrates favorable economics and scalability, watch this: a new wave of investment announcements from Exxon Mobil and its competitors into similar technologies that convert a costly waste stream (CO 2) into a valuable byproduct (solid carbon).

- And these could be happening: We are likely to see an increase in smaller, co-located hydrogen projects where an industrial user, such as a steel mill or chemical plant, serves as the anchor offtaker. This model avoids the risks of relying on nascent export markets and fluctuating commodity prices.

- A key signal to watch will be any future announcement regarding the Baytown project. A formal cancellation would confirm a long-term strategic pivot away from the mega-project model, whereas a restart would require publicly announced, binding offtake agreements, signaling that the market has finally reached a new level of maturity.

Frequently Asked Questions

Why did Exxon Mobil pause its large-scale Baytown blue hydrogen project?

Exxon Mobil paused its Baytown project in November 2025 due to a fundamental lack of binding, long-term offtake agreements. Potential buyers were reluctant to absorb the premium costs associated with the carbon capture and storage (CCS) component, making the project commercially unviable without guaranteed demand.

What is the main problem facing the blue hydrogen market in 2026?

The main problem is a commercial one: a mismatch between ambitious supply plans and actual market demand. The industry’s “build it and they will come” approach failed because it couldn’t secure enough customers willing to pay the higher price for blue hydrogen, leading to a halt in major investments.

What technology is Exxon Mobil exploring as an alternative to blue hydrogen?

Exxon Mobil is now exploring methane pyrolysis. In November 2025, it announced a partnership with BASF to build a demonstration plant for this technology. Methane pyrolysis produces hydrogen and a solid carbon byproduct, offering a different economic profile that avoids the costs and complexities of capturing, transporting, and storing gaseous CO2.

How has the strategy for hydrogen partnerships changed?

Partnership strategies have pivoted from securing large-scale offtake agreements to focusing on technology validation. Earlier partnerships (like with JERA and SK Group) were aimed at underwriting huge production facilities with future international buyers. The new model, seen in the Exxon Mobil-BASF collaboration, is about jointly developing and de-risking new production technologies before committing to large-scale capital investment.

What is the 2026 outlook for new hydrogen projects?

The outlook for 2026 favors smaller, modular, and demand-driven projects over speculative mega-projects. The market will likely see more co-located projects where an industrial user serves as a guaranteed anchor customer. This approach reduces market risk by ensuring demand is secured before major capital is committed.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.