SOFC Data Center Deals: Bloom Energy’s $5 B Brookfield Pact and 1 GW AEP Agreement (2024-2026)

Industry Adoption: Fuel Cells Shift from Niche to Critical Infrastructure

The primary driver for the surge in fuel cell company valuations is the market’s shift from viewing the technology as a long-term decarbonization tool to recognizing it as an immediate solution for the acute power crisis created by Artificial Intelligence (AI) data centers. Between 2021 and 2024, adoption was steady but dependent on policy support and niche applications. The period from 2025 to today marks a definitive commercial inflection point, where grid constraints have made on-site power generation a critical enabler for the tech sector’s growth, catapulting fuel cell stocks higher.

- In the 2021-2024 period, fuel cell adoption was driven by a general push for clean energy and grid resiliency, resulting in smaller, diversified projects. The period from 2025 to today is defined by a single, massive demand signal: the exponential power needs of AI, which has transformed the investment case from theoretical to urgent.

- Bloom Energy has become the main beneficiary, leveraging its mature Solid Oxide Fuel Cell (SOFC) technology to secure large-scale data center contracts. Its partnership with Quanta Computer, expanded in November 2024 to increase power capacity by over 150%, validates its solution for powering the AI supply chain directly.

- Other companies are pivoting to capture this demand. In January 2026, Fuel Cell Energy announced a letter of intent with SDCL to deploy up to 450 MW for AI data centers. However, its path is more challenging due to persistent financial losses and a reliance on capital raises, contrasting with Bloom Energy’s stronger market position.

- While stationary power for AI is the dominant driver, the transportation sector continues to mature. Ballard Power Systems remains focused on heavy-duty mobility, securing a $40 million Department of Energy (DOE) grant in March 2024 to build a new PEM fuel cell gigafactory in Texas, indicating progress in a different but parallel market segment.

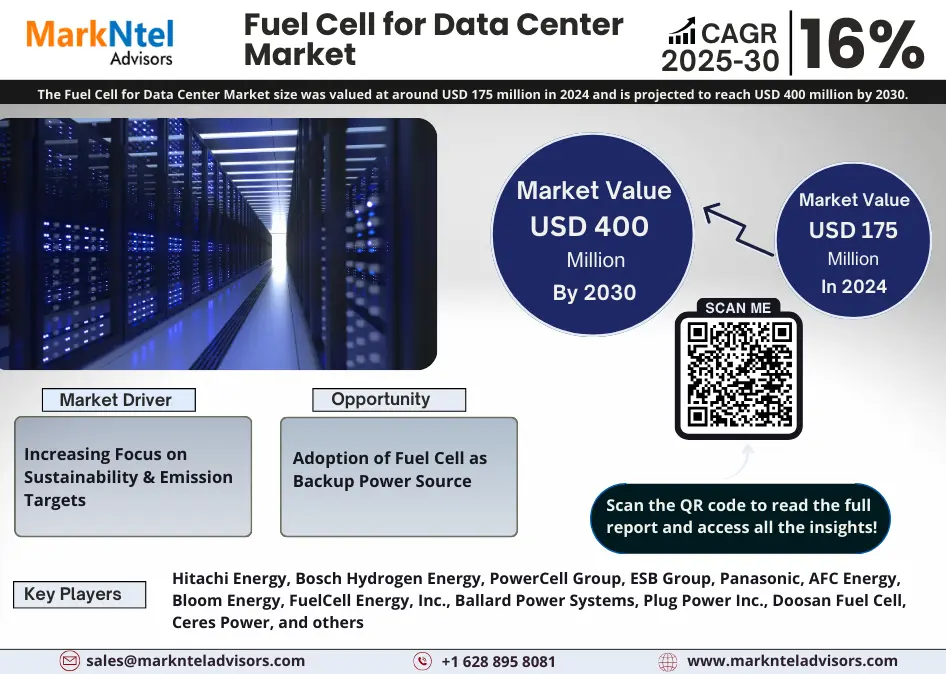

Data Center Fuel Cell Market Grows

This chart quantifies the growth of the fuel cell market specifically for data centers, directly supporting the section’s main point that AI is creating an immediate power crisis and driving adoption.

(Source: MarkNtel Advisors)

$5 B Brookfield Investment: Bloom Energy Secures Data Center Project Capital

The fuel cell sector has attracted significant institutional capital specifically targeted at the data center power bottleneck, validating the technology’s bankability and providing the necessary funding for massive scaling. This shift from venture-style investment to large-scale infrastructure financing underscores the market’s confidence in the commercial viability of fuel cells as a critical asset class for the digital economy.

Fuel Cell Market to Exceed $50B

This chart’s projection of a massive $51.5B market, which names Bloom Energy as a key player, provides the context for why large institutional investors like Brookfield would make a multi-billion dollar commitment.

(Source: Stellar Market Research)

- The landmark partnership announced in October 2025 involves Brookfield Asset Management investing up to $5 billion to deploy Bloom Energy’s fuel cell technology for data centers. This provides the dedicated capital required to execute on its massive order backlog and de-risks project financing.

- The U.S. government continues to support the sector’s scale-up through targeted grants. In March 2024, the DOE awarded Ballard Power Systems $40 million in grants to support the construction of its $160 million integrated fuel cell production facility in Rockwall, Texas.

- In January 2026, Fuel Cell Energy and investment firm SDCL forged a collaboration to deploy up to 450 megawatts of fuel cell systems for AI-driven data centers globally. This letter of intent signals growing investor appetite for financing alternative players in the stationary power market.

- Ceres Power’s asset-light licensing model attracts a different form of investment. Its successful £181 million fundraising in March 2021, tied to development agreements with industrial giants like Doosan and Hyundai, demonstrated confidence in its technology-centric approach.

Table: Fuel Cell Sector Strategic Investments and Grants (2021-2026)

| Company | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Fuel Cell Energy / SDCL | Jan. 2026 | Announced a letter of intent for up to 450 MW of fuel cell systems for AI-driven data centers, signaling a strategic pivot to the high-growth data center market. | Stock Titan |

| Bloom Energy / Brookfield | Oct. 2025 | Up to $5 billion strategic partnership to finance and deploy Bloom’s SOFC technology specifically for data center infrastructure, providing capital for massive scaling. | Reuters |

| Ballard Power Systems / U.S. DOE | Mar. 2024 | Received $40 million in DOE grants to support the construction of a new $160 million fuel cell “gigafactory” in Texas, aimed at scaling up production for heavy-duty mobility. | Ballard Power Systems |

| Ceres Power | Mar. 2021 | Raised £181 million to accelerate development and scale its licensing model with partners including Doosan and Hyundai, validating its asset-light strategy. | Fuel Cells Works |

Data Center Pacts: Bloom Energy Signs 1 GW AEP Agreement

Strategic partnerships have evolved from technology validation and pilot projects in the 2021-2024 period to multi-billion-dollar, gigawatt-scale commercial offtake agreements from 2025 onward. These deals, primarily centered on providing reliable power to data centers, represent the most tangible evidence of the fuel cell sector’s commercial maturation and are a direct cause of the recent stock appreciation.

Modular Fuel Cells Scale for Megawatts

This diagram illustrates how modular fuel cells can be scaled to meet massive power needs, providing the technical basis for the gigawatt-scale agreements discussed in the section.

(Source: Seeking Alpha)

- Bloom Energy’s agreement with American Electric Power (AEP) in November 2024 to potentially purchase up to 1 GW of fuel cells marks a pivotal moment, shifting from enterprise-level sales to utility-scale deployments for data center clients.

- The partnership between Bloom Energy and AI infrastructure manufacturer Quanta Computer, first announced in April 2024 and significantly expanded seven months later, demonstrates a tightening integration between fuel cell providers and the core AI hardware supply chain.

- Ceres Power continues to execute its technology licensing model, signing a global license agreement in September 2024 with India-based Thermax to manufacture Solid Oxide Electrolyzer Cell (SOEC) systems. This partnership opens a new geographic market and application in green hydrogen production.

- The collaboration between industrial giants Bosch and Ceres Power, strengthened in February 2022, focuses on preparing for the full-scale production of SOFC systems, underscoring the industrialization of the technology by established manufacturing leaders.

US vs. Global Markets: AI Power Demand Concentrates Growth in North America

While the long-term growth of the fuel cell industry is global, the recent and dramatic stock rally is overwhelmingly fueled by developments within the United States. The acute power deficit driven by the concentration of AI data centers in the U.S. has made it the epicenter of near-term commercial activity and investment, overshadowing slower, policy-driven growth in other regions that characterized the 2021-2024 period.

North American Market Growth Forecast

This chart focuses specifically on the North American stationary fuel cell market, directly reinforcing the section’s argument that the U.S. is the epicenter of near-term growth.

(Source: Global Market Insights)

- The 2021-2024 period was marked by geographically diverse policy initiatives, including the U.S. Inflation Reduction Act, China’s FCV promotion program, and various European hydrogen strategies. However, from 2025 onward, the dominant driver became the U.S. data center power crisis, a market-driven catalyst that is more immediate and financially lucrative.

- Bloom Energy’s major deals with Brookfield, AEP, and Quanta Computer are all centered on the U.S. market, reflecting where the most urgent and large-scale demand exists. Its reported $20 billion backlog is largely driven by this domestic data center demand.

- South Korea remains a key market for stationary fuel cells, highlighted by Bloom Energy’s partnership with SK Eternix to develop an 80 MW project. However, the scale of recent U.S. announcements has become the primary focus for investors.

- Ballard Power Systems is also concentrating its manufacturing expansion in North America with its new Texas gigafactory, strategically positioning itself to leverage U.S. incentives and serve the domestic heavy-duty transport market, even as it maintains a presence in Europe.

SWOT Analysis: AI Demand Strength vs. Execution Risk

The fuel cell sector’s primary strength is the new, inelastic demand from the AI industry, which provides a clear path to commercial scale. However, this is balanced by significant execution risks, as companies must now prove they can convert massive order backlogs into profitable operations without the persistent cash burn and shareholder dilution that have historically plagued the industry.

Market Drivers Weighed Against Restraints

This qualitative analysis of market drivers and restraints directly mirrors the section’s SWOT-style discussion of new demand (strength) versus high costs and other risks.

(Source: Coherent Market Insights)

- Strengths have been significantly amplified, shifting from reliance on government subsidies to capturing a high-value commercial market with urgent needs.

- Weaknesses remain a critical differentiator between companies, with profitability and cash flow management separating market leaders from higher-risk players.

- Opportunities have expanded from broad decarbonization goals to solving a specific, multi-billion-dollar infrastructure bottleneck for the world’s largest technology companies.

- Threats now include not just policy uncertainty but also the immense operational challenge of scaling manufacturing and deployment to meet unprecedented demand profitably.

Table: SWOT Analysis for Fuel Cell Sector Drivers (2021-2026)

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | – Maturing technology (SOFC, PEM) – Strong government policy support (IRA) |

– Proven solution for data center power – Massive order backlogs ($20 B for Bloom) – Large-scale institutional investment |

The AI power crisis provided a critical, high-value commercial use case that validated the technology beyond just policy support. Bankability was proven by large infrastructure investors like Brookfield. |

| Weaknesses | – High costs and lack of profitability – Heavy cash burn and shareholder dilution – Reliance on subsidies |

– Persistent losses for some players (Fuel Cell Energy’s -107.5% profit margin) – Execution risk in scaling production – Continued cash burn despite revenue growth |

While revenue has surged, the fundamental challenge of achieving profitability remains. The market is now differentiating between companies that show a path to profitability and those still heavily burning cash. |

| Opportunities | – Green hydrogen economy – Decarbonization of transport and industry – Grid resiliency projects |

– Immediate, massive demand from AI data centers – Utility-scale deployments (AEP’s 1 GW deal) – Expansion into new regions (Ceres in India) |

The opportunity set shifted from a broad, long-term vision to a specific, immediate, and high-margin infrastructure need, creating a powerful near-term revenue catalyst. |

| Threats | – Competing clean technologies (batteries) – Fluctuations in natural gas prices – Policy and subsidy uncertainty |

– Inability to execute on massive backlogs – Supply chain constraints at scale – Potential changes to IRA funding (speculative OBBBA) |

The primary threat is now internal: operational failure. The inability to profitably deliver on promises to major tech and utility clients poses a greater risk than external competition. |

Bloom Energy 2026 Outlook: Executing on a $20 B Backlog

The single most critical factor for the fuel cell sector in 2026 is execution. The narrative has shifted from potential to delivery, and the ability of companies, particularly market leader Bloom Energy, to profitably convert their multi-billion-dollar backlogs into tangible cash flow will determine if current valuations are sustainable.

Bloom Energy’s Data Center Dominance

This snapshot of Bloom Energy’s market capitalization and focus on data centers provides the perfect context for the section’s discussion of the company’s outlook and ability to execute on its backlog.

(Source: Arya’s Substack)

- If companies demonstrate profitable scaling, watch for continued stock appreciation and positive analyst revisions. The key signal is improving gross margins alongside strong revenue growth in quarterly earnings reports, which would indicate that economies of scale are being achieved.

- If execution falters through project delays, cost overruns, or continued high cash burn, watch for a significant cooling of investor sentiment. This could be happening if companies like Fuel Cell Energy are forced to continue raising capital and diluting shareholders to fund operations, despite a growing top line.

- A crucial forward-looking signal is the fuel source. The current boom is largely powered by natural gas. Watch for announcements of large-scale projects planning to use green hydrogen. A tangible shift toward green hydrogen would validate the long-term decarbonization thesis and attract a new wave of ESG-focused institutional capital.

The questions your competitors are already asking

This report covers one angle of the commercial drivers behind the recent surge in fuel cell stocks. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the fuel cell for data centers market?

- What is the outlook for fuel cell deployment in the AI data center sector by 2030?

- Which hyperscalers and data center operators are adopting on-site fuel cell power?

- How do solid oxide fuel cells (SOFCs) compare to other on-site power solutions for AI data centers?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.