Green Hydrogen Market Acceleration, Toyota cellcentric Partnership, €1 B Moeve Project, and 2 National Policy Shifts (2025 to 2026)

Strait of Hormuz Disruption Accelerates Green Hydrogen Adoption

The 2026 de facto closure of the Strait of Hormuz acts as a long-term accelerant for hydrogen adoption by exposing acute fossil fuel vulnerabilities, but it also introduces severe near-term supply chain risks for critical manufacturing materials. This geopolitical rupture reframes the hydrogen conversation from a climate-focused solution to a strategic imperative for national energy security, forcing a structural realignment in global energy investment and policy.

- Between 2021 and 2024, hydrogen adoption was primarily driven by decarbonization goals. Early commercial validation was seen in heavy transport through companies like Hyzon Motors and in maritime applications where firms like Ballard Power Systems secured type approval for fuel cell modules.

- From 2025, the primary driver for hydrogen shifted decisively to energy security. In response to the crisis, China launched a national pilot program to expand industrial hydrogen use, and the European Union renewed its push for green hydrogen schemes to ensure regional energy independence.

- In the heavy-duty transport sector, the crisis spurred direct action, with Toyota announcing on March 31, 2026, that it would join the cellcentric fuel cell joint venture with Volvo Group and Daimler Truck to accelerate the development of a stable, long-term alternative to diesel.

- The conflict concurrently introduced new risks, disrupting approximately 30% of the global helium supply transiting the strait from Qatar. This creates a potential bottleneck for the manufacturing of electrolyzers and fuel cells, which rely on helium for production processes.

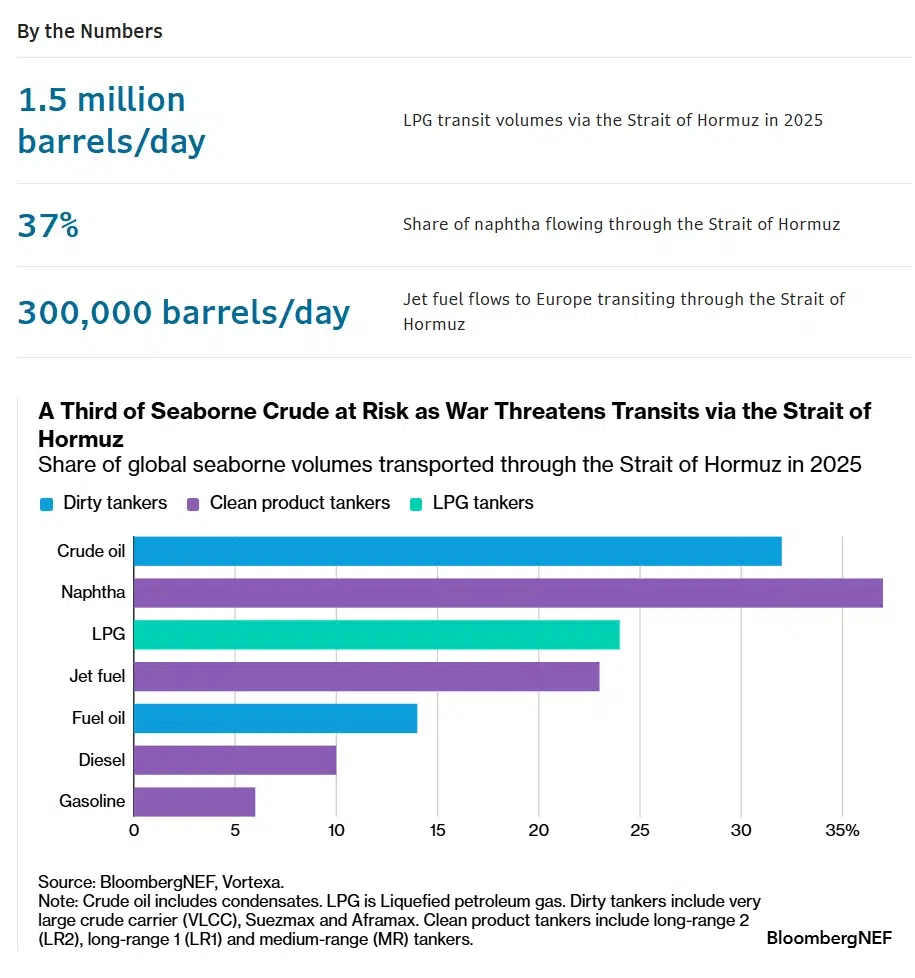

Hormuz Chokepoint Threatens Global Fuel Supply

This chart quantifies the fossil fuel vulnerability at the Strait of Hormuz, showing the significant percentage of global seaborne products like crude oil and LPG that are at risk.

(Source: BloombergNEF)

$1.2 B Moeve Investment Signals Green Hydrogen Project Acceleration

The geopolitical crisis has immediately altered the financial landscape for hydrogen projects, improving the bankability of green hydrogen in secure regions while creating new investor hesitancy for capital-intensive projects exposed to global volatility. The surge in natural gas prices has rendered grey hydrogen uneconomical, creating an immediate, market-driven incentive to finance green hydrogen infrastructure.

- The dramatic spike in natural gas prices, with European futures contracts surging nearly 70%, has directly inverted the hydrogen production cost structure. This makes green hydrogen, produced from renewables, economically competitive with grey hydrogen years ahead of prior forecasts.

- A direct signal of this investment shift occurred on March 2, 2026, when Moeve, in partnership with Masdar, secured €1 billion (approximately $1.2 billion) for a large-scale green hydrogen project in Southern Europe. This project capitalizes on the strategic push for European energy independence.

- While the long-term strategic case is stronger, the immediate market volatility and risk of a global recession could cause investors to delay Final Investment Decisions (FIDs) on multi-billion dollar green hydrogen projects, underscoring risks to project timelines.

- Some analyses suggest this investment boost may be geographically concentrated. A Bloomberg NEF analysis cautions that the effect may be strongest in China, noting that historically, interest in energy alternatives can fade once a fossil fuel crisis subsides.

Hydrogen Market Partnerships, Toyota Joins Daimler and Volvo’s cellcentric Venture (2026)

The energy security crisis is forcing strategic consolidation and new alliances across the hydrogen value chain, spanning transportation manufacturing, military applications, and geopolitical energy supply agreements. These partnerships are no longer just about market expansion; they are about building resilient supply chains insulated from geopolitical shocks.

- In a significant consolidation in the heavy-duty transport sector, Toyota announced plans to join the cellcentric fuel cell joint venture with Volvo Group and Daimler Truck. This move signals a unified effort by major automotive OEMs to accelerate fuel cell truck development as a direct response to the volatility of diesel markets.

- The U.S. Department of Defense (Do D) is actively seeking partners to prototype expeditionary hydrogen generators. This initiative, launched in July 2025, highlights a new military demand driver for fuel cells to provide operational flexibility and reduce logistical risk in contested environments.

- Geopolitical partnerships are also shifting, as seen with China’s increased financing for green hydrogen and battery initiatives in North Africa. This strategy aims to diversify its energy supply chains away from the Gulf and establish a more resilient, greener energy posture.

Table: Strategic Hydrogen and Fuel Cell Partnerships Post-Hormuz Crisis

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Toyota, Volvo Group, Daimler Truck | March 2026 | Toyota to join the cellcentric fuel cell joint venture to accelerate the development of fuel cell trucks as a stable alternative to volatile diesel markets. | Reuters |

| China and North Africa | March 2026 | Increased Chinese financing for green hydrogen initiatives in countries like Morocco to diversify energy supply chains away from the Gulf. | Stimson Center |

| U.S. Department of Defense (Do D) | July 2025 | Prototyping expeditionary hydrogen generators for ship and shore use to reduce logistical risk and increase operational flexibility in contested environments. | U.S. Department of Defense |

| Sembcorp and Bloom Energy | June 2024 | Deployment of solid oxide fuel cells in Singapore to provide low-carbon power, a partnership that gains strategic importance for energy resilience post-crisis. | Argus Media |

China vs. EU, Geopolitical Shifts in Hydrogen Market Leadership Post-Hormuz

The Hormuz crisis is accelerating a geographic bifurcation of the hydrogen economy, favoring integrated producer-consumer nations like China and the United States while exposing the vulnerabilities of import-dependent regions such as the European Union, Japan, and South Korea.

- Between 2021 and 2024, hydrogen policy development was geographically diverse, with Europe’s REPower EU plan, the U.S. Inflation Reduction Act, and Asia’s ambitious import strategies creating multiple potential growth hubs.

- The 2026 crisis allows China to leverage its existing dominance in renewable technology manufacturing. By launching a national hydrogen pilot program explicitly linked to energy security, Beijing is positioning itself to build a resilient, domestic hydrogen ecosystem.

- The EU is forced to treat its green hydrogen schemes with new urgency, with one analysis calling the conflict the “strongest accelerator” for Europe’s green industry. Investments like the €1 billion Moeve project in Southern Europe are now critical for regional energy security, not just climate goals.

- The conflict serves as a stark warning to import-dependent nations like Japan and South Korea, whose strategies relied on seaborne hydrogen trade. They are now under immense pressure to maximize domestic production and forge more resilient “green hydrogen corridors” with geopolitically stable partners.

Green Hydrogen Cost Competitiveness, Crisis Inverts Economics Versus Grey Hydrogen

The geopolitical shock has artificially but effectively advanced the economic maturity of green hydrogen, making it cost-competitive against grey hydrogen years ahead of schedule. Concurrently, the value of fuel cell technology is being redefined by its strategic resilience, shifting the focus from decarbonization alone to its role in ensuring supply chain stability.

- Prior to the crisis, green hydrogen produced via electrolysis was on a clear cost-reduction path but remained more expensive than grey hydrogen derived from natural gas. A crisis-induced surge in natural gas prices immediately inverts this, making green hydrogen the more economical production method in many regions.

- The maturity of fuel cells is now being judged by their ability to provide supply chain resilience. The Toyota/cellcentric agreement demonstrates that the heavy transport sector now values the technology as a stable alternative to volatile diesel prices.

- Military applications further validate this shift. The U.S. Do D’s prototyping of expeditionary hydrogen generators confirms fuel cell technology as a mature solution for ensuring operational assurance and energy independence in contested environments.

- The crisis reinforces the need for a robust manufacturing base for core components. A top policy priority will become onshoring the production of electrolyzers and fuel cells, a space where companies like Plug Power, Sunfire, and Doosan Fuel Cell are active.

SWOT Analysis, Green Hydrogen Market After the Hormuz Disruption

The Hormuz crisis fundamentally reshapes the strategic context for the hydrogen economy, amplifying its core strength as a secure energy source while simultaneously exposing critical dependencies in its own nascent supply chains.

Table: SWOT Analysis for the Green Hydrogen Market

| SWOT Category | 2021 – 2024 (Pre-Crisis) | 2025 – 2026 (Post-Crisis) | What Changed / Validated |

|---|---|---|---|

| Strengths | Potential as a zero-emission energy carrier for decarbonization. | Proven value as a source of domestic energy security and independence from geopolitical chokepoints. | The core value proposition shifted from environmental to strategic, becoming a non-negotiable tool for national security. |

| Weaknesses | High cost of green hydrogen production compared to grey hydrogen; reliance on subsidies. | Dependency on global supply chains for critical materials (e.g., helium, semiconductors) and components (e.g., electrolyzers, fuel cells). | The primary weakness shifted from production cost to supply chain fragility, revealing new vulnerabilities. |

| Opportunities | Falling renewable energy costs and government policies like the IRA improving the business case. | Soaring fossil fuel prices make green hydrogen cost-competitive without subsidies; emergency policies to fast-track deployment. | The opportunity evolved from a gradual, policy-driven transition to an urgent, market-driven mandate for deployment. |

| Threats | Slow pace of infrastructure build-out and lack of firm offtake agreements delaying projects. | Risk of a global recession delaying FIDs; recognition that future hydrogen trade could face similar chokepoint risks. | The threat landscape expanded from commercial hurdles to systemic macroeconomic and geopolitical risks. |

Hydrogen Market 2027 Outlook, Watch for Domestic Production Policies

If the Hormuz disruption persists or establishes a new norm of geopolitical energy risk, watch for major economies to enact emergency-level policies in the next 12-18 months to fast-track domestic hydrogen production and secure manufacturing supply chains for critical components.

US Grid Transformation Underpins Energy Independence

This projection shows the rapid growth of solar and batteries in the US energy mix, a trend that is critical for enabling domestic green hydrogen production policies.

(Source: EnergyNow.com)

- If this happens: Continued high fossil fuel prices and supply insecurity.

- Watch this: The United States may expand the Inflation Reduction Act’s hydrogen tax credits or invoke defense production authorities to accelerate domestic manufacturing of electrolyzers, moving beyond existing policy frameworks.

- Watch this: The European Union will likely fast-track permitting for hydrogen projects and establish binding domestic production targets to reduce reliance on imports, moving beyond the initial framework of its green schemes.

- These could be happening: A clear bifurcation in investment, where capital flows toward smaller, faster-to-build domestic projects over large, capital-intensive international import/export terminals which now carry higher perceived geopolitical risk.

- These could be happening: Increased M&A activity in the fuel cell and electrolyzer space as larger industrial and automotive players acquire technology to secure their supply chains, mirroring the Toyota/cellcentric consolidation.

The questions your competitors are already asking

This report covers one angle of how geopolitical conflict is reshaping the hydrogen and fuel cell market. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the heavy-duty fuel cell truck market now that Toyota has joined the cellcentric JV?

- What is the outlook for green hydrogen deployment in the EU, now that the primary driver has shifted from decarbonization to energy security?

- With 30% of the global helium supply from Qatar disrupted, what is the bottleneck risk for electrolyzer and fuel cell manufacturing?

- Which heavy transport operators are adopting hydrogen fuel cells as a long-term strategic alternative to diesel?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.