SOFC Natural Gas Risk, 450 MW SDCL Pact, Amazon’s 228 Fuel Cells Challenged, and 46 BTM Projects (2021 to 2026)

In 2026, behind-the-meter (BTM) fuel cells are emerging as the primary technology for achieving energy independence at mission-critical facilities like hospitals and campuses, driven by an urgent need to circumvent failing public grids and multi-year interconnection queues. While hyperscale data centers are the vanguard, with at least 46 planned facilities opting for BTM solutions, the core strategy of using natural gas-powered fuel cells introduces a significant and growing risk. This approach invites intense regulatory scrutiny and community opposition, as evidenced by legal challenges against major projects. The investment thesis now hinges on whether the immediate benefit of energy resilience outweighs the long-term liability of expanding fossil fuel infrastructure, a tension that will define the market’s trajectory.

BTM Adoption Risks, Amazon’s 228 Fuel Cells Face Legal Challenges

The strategic shift to BTM fuel cells to ensure power continuity is creating a new class of regulatory and community-related risks tied directly to the technology’s near-term reliance on natural gas. While adoption accelerated between 2025 and today to bypass grid constraints, this rapid growth has attracted scrutiny that was less prevalent in the 2021-2024 period, when projects were smaller and less conspicuous. This conflict between the need for power and the impact of its generation is now a central challenge for developers.

- From 2025 to today, the scale of deployments has shifted dramatically from smaller, discrete installations to massive, campus-level power plants. The proposal by Amazon for a 228-fuel-cell array in Ohio and Quinnipiac University’s 10-cell installation exemplify this trend, moving fuel cells from a backup role to primary baseload power providers.

- This scaling has triggered significant local opposition. In February 2026, the Columbus suburb of Hilliard, Ohio, filed a lawsuit to block Amazon‘s proposed fuel cell array, citing safety and zoning concerns. This represents a material escalation from general public frustration to direct legal and regulatory headwinds.

- The dependency on natural gas pipelines to fuel these large BTM plants undermines the “clean energy” narrative and links facilities to volatile commodity prices. This has drawn criticism from environmental groups and government officials alike, creating a substantial reputational and financial risk.

- High-level skepticism from public finance leaders, such as Jigar Shah of the U.S. DOE calling the BTM natural gas strategy an “engineering and economic disaster, ” signals potential difficulties in securing long-term public funding or favorable policy treatment for these projects.

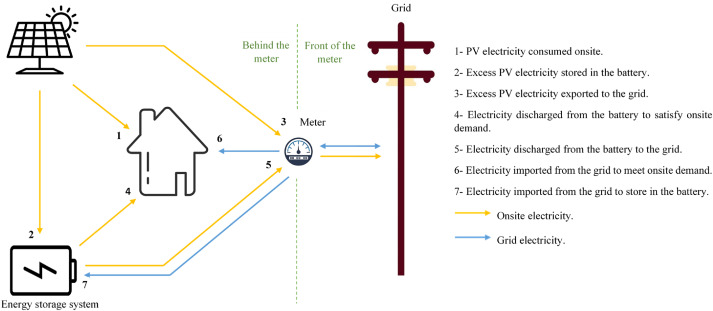

Diagram Explains Behind-the-Meter Energy Systems

This diagram visually defines the ‘Behind-the-Meter’ concept central to the section, showing how onsite power generation operates independently from the main electrical grid.

(Source: ScienceDirect.com)

Investment: $450 M Fuel Cell Energy Pact Signals Shift to Project Finance

The investment model for BTM fuel cells is evolving from direct capital purchases by end-users to sophisticated project financing structures, making large-scale deployments more accessible but also locking in long-term fuel dependencies. This shift is critical for enabling institutions like hospitals and universities, which may lack the capital for multi-million dollar energy projects, to adopt the technology. The primary mechanism is the use of third-party financing to build, own, and operate the power plants under long-term Power Purchase Agreements (PPAs).

- In February 2026, Fuel Cell Energy formed a strategic partnership with Sustainable Development Capital LLP (SDCL) to finance and deploy up to 450 MW of fuel cell systems globally. This collaboration is designed to provide capital for BTM power projects at data centers and industrial sites, removing the upfront cost barrier for customers.

- Government incentives are also de-risking investment in key sectors. In January 2026, the U.S. Department of Energy (DOE) announced a grant program specifically to fund the deployment of fuel cell-based distributed generation systems for healthcare facilities, directly targeting the resilience needs of hospitals.

- The financial viability of these projects is directly tied to the cost of natural gas. While the PPA model insulates the end-user from operational risk, the project owner, such as the SDCL partnership, assumes the risk of fuel price volatility, which can impact long-term profitability and investor returns.

Partnerships: Fuel Cell Energy 450 MW SDCL Partnership for BTM Power (2026)

Strategic partnerships that combine technology manufacturing with project financing and development expertise have become the dominant model for scaling BTM fuel cell deployments in 2026. These alliances are essential for managing the complexity and capital intensity of campus-scale microgrids. The focus has shifted from simple equipment sales to offering fully-financed, turnkey energy-as-a-service solutions.

Diagram Shows Integrated Fuel Cell System

This diagram illustrates the complex, integrated power systems that strategic partnerships are formed to build and manage as turnkey, energy-as-a-service solutions.

(Source: ScienceDirect.com)

- The most significant recent alliance is the February 2026 partnership between Fuel Cell Energy and Sustainable Development Capital LLP (SDCL). The agreement to jointly develop and finance up to 450 MW of BTM projects for data centers and industrial clients validates the energy-as-a-service model for large-scale deployments.

- Collaboration is also advancing the underlying technology. In April 2026, Advent Technologies and EH Group Engineering AG signed a joint development agreement to advance high-temperature PEM (HTPEM) fuel cell technology specifically for stationary power applications, aiming to improve performance and cost-effectiveness.

- Adjacent partnerships are emerging to create new value streams from BTM assets. The collaboration between Vertiv and CPower to connect BTM battery storage to grid services markets demonstrates a future where campus microgrids can generate revenue by providing ancillary services, improving the overall economic case.

Table: BTM Fuel Cell Strategic Partnerships and Deployments (2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Advent Technologies / EH Group Engineering AG | Apr 2026 | Joint development agreement to advance HTPEM fuel cell technology for stationary power, targeting improved performance for next-generation systems. | Globe Newswire |

| Fuel Cell Energy / Sustainable Development Capital LLP (SDCL) | Feb 2026 | Partnership to finance and deploy up to 450 MW of fuel cell power systems, providing a turnkey energy-as-a-service model for AI data centers and industrial customers. | Yahoo Finance |

| Amazon Ohio Data Center | Feb 2026 | A proposed 228-fuel-cell array to power a data center campus. The project is facing a lawsuit from the local municipality, highlighting community and regulatory risk. | Signal Ohio |

| Quinnipiac University Campus Microgrid | Jan 2026 | Installation of 10 high-efficiency fuel cells to provide primary power across three campuses, demonstrating adoption by the higher education sector for energy resilience. | Quinnipiac Today |

Geography: US Dominates BTM Fuel Cell Deployments Amid Grid Constraints

North America, and specifically the United States, has solidified its position as the global hotspot for BTM fuel cell deployment in 2026, a geographic concentration driven almost entirely by extreme data center power demand and severe grid limitations. While activity between 2021 and 2024 was more varied, the period from 2025 to today has seen project announcements consolidate in US regions with strained grids, such as Ohio. This intense regional focus amplifies both the market opportunity and the associated regulatory risks.

Renewable Curtailment Rises Across US

This chart provides direct evidence for the ‘severe grid limitations’ in the US mentioned in the heading, showing a clear trend of worsening grid congestion.

(Source: Deloitte)

- The overwhelming majority of large-scale BTM fuel cell projects announced in 2026 are located in the United States. Projects like Amazon‘s in Ohio, Quinnipiac University’s in Connecticut, and Trinity College’s in Hartford highlight this trend, with deployments directly correlated to areas facing grid congestion and interconnection delays.

- The market growth is primarily propelled by hyperscale data centers seeking to circumvent multi-year waits for utility power. This single-sector dependency makes the US market for BTM fuel cells highly sensitive to the build-out plans and energy strategies of a few large tech companies.

- While the Fuel Cell Energy/SDCL partnership has a global mandate, its initial focus is explicitly on the acute power needs of AI data centers, which are currently most concentrated in the U.S. This suggests international expansion will follow the geographic spread of data center construction.

- In contrast, market reports note that growth in Asia-Pacific and Europe is driven by a more diverse set of applications, including industrial CHP and policy-supported decarbonization efforts, indicating different market dynamics and a less acute focus on BTM solutions to bypass grid access issues.

Technology Maturity: Commercially Proven Fuel Cells Face a Fuel Source Gap

The core fuel cell technologies, particularly Solid Oxide (SOFC) and Molten Carbonate (MCFC), are commercially mature and field-proven for providing continuous, reliable baseload power at the multi-megawatt scale (TRL 8-9). The critical maturity gap is not in the power generation hardware itself but in the supporting infrastructure required for true decarbonization. The “hydrogen-ready” status of current systems is a forward-looking promise that is disconnected from the near-term reality of a non-existent green hydrogen supply chain.

Hydrogen’s Role in Long-Duration Storage

This infographic explains the strategic value of hydrogen as a long-duration energy source, which contextualizes the ‘fuel source gap’ between mature hardware and green fuel availability.

(Source: Issuu)

- Deployments in 2025-2026, such as those at Quinnipiac University and planned by Amazon, validate that fuel cells have moved beyond the pilot phase and are commercially ready for campus-scale applications. This represents a significant progression from the smaller, more tentative deployments seen between 2021 and 2024.

- The primary technological barrier is the fuel feedstock. While leading systems from providers like Bloom Energy and Fuel Cell Energy can run on hydrogen, the infrastructure for producing and distributing cost-effective green hydrogen at scale remains at a low level of maturity (TRL 5-7).

- This forces a reliance on natural gas, creating a mismatch between the long-term clean energy goals of customers and the immediate fossil-fuel reality of their BTM power plants. This is the central technological and commercial challenge facing the sector.

- While research into cost reduction, such as Cornell University’s development of a nickel-based catalyst in March 2026, will improve system economics, it does not address the fundamental constraint of clean fuel availability.

SWOT Analysis: BTM Fuel Cell Strengths and Natural Gas Threats

The strategic position of BTM fuel cells is defined by a powerful value proposition for energy resilience that is directly threatened by its operational dependence on the natural gas grid. The technology’s key strength, its ability to be deployed rapidly to provide reliable power, has been validated by immense data center demand. However, this same success has exposed its greatest weakness: a vulnerability to fuel price volatility and mounting public opposition to new fossil fuel infrastructure.

Chart Outlines Benefits of BTM Systems

This flowchart directly corresponds to the ‘Strengths’ portion of the SWOT analysis by detailing key BTM benefits like service reliability and cost reduction.

(Source: ScienceDirect.com)

Table: SWOT Analysis for Behind-the-Meter Fuel Cells (2026)

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Demonstrated high reliability in niche applications; higher efficiency than grid power in some regions. | Provides “speed-to-power” in months, bypassing multi-year grid queues; high CHP efficiency (up to 85%+) ideal for campuses and hospitals. | The value of bypassing grid queues became the primary driver, validated by massive data center adoption from Amazon, Microsoft, and others. |

| Weaknesses | High capital cost compared to diesel generators; reliance on natural gas infrastructure. | Deep dependency on volatile natural gas prices; projects are perceived as an expansion of fossil fuel use, undermining ESG goals. | The “clean energy” marketing narrative was directly challenged by community opposition and expert criticism (e.g., Jigar Shah) in 2026. |

| Opportunities | Growing need for data center power; potential for “hydrogen-ready” systems. | Massive addressable market from AI data centers (56 GW of planned BTM capacity); DOE grants for healthcare; new revenue from grid services (e.g., Vertiv/CPower). | The scale of the AI-driven power demand became clear, transforming fuel cells from a backup option to a primary power strategy. |

| Threats | Potential for policy shifts away from natural gas; competition from solar+storage. | Direct legal and regulatory opposition from local communities (e.g., Amazon Ohio lawsuit); sustained spikes in natural gas prices could make projects uneconomical. | The threat of community opposition transitioned from a theoretical risk to a concrete legal and project-delaying reality in February 2026. |

2027 Outlook: A Permitting Slowdown for Natural Gas Fuel Cells

If community opposition and regulatory pushback against natural gas-powered BTM projects intensify through 2026, the market should anticipate a slowdown in permitting for large new fuel cell deployments in 2027. In this scenario, watch for a strategic pivot from developers and customers towards hybrid solutions that integrate significant renewable generation or a more aggressive pursuit of binding green hydrogen offtake agreements, even at a premium, to mitigate regulatory and social license risks.

- If this happens: A ruling against Amazon in the Ohio lawsuit would set a powerful legal precedent, likely emboldening community groups across the country and making it significantly harder to site and permit large BTM fuel cell plants near populated areas.

- Watch this: Monitor natural gas price futures. A sustained price increase would severely damage the levelized cost of energy (LCOE) for these projects, making alternatives like solar-plus-storage more financially attractive and potentially stalling new investment decisions.

- This could be happening: The narrative is already shifting. The move by Vertiv and CPower to integrate BTM assets with grid services signals a trend towards more complex, multi-asset microgrids that are not solely reliant on natural gas, offering a more resilient and defensible energy strategy.

- This could be happening: Companies may accelerate efforts to secure green hydrogen offtake agreements. The first major deal between a campus-scale fuel cell operator and a green hydrogen producer would be a critical signal that the industry is moving to address its core feedstock vulnerability.

The questions your competitors are already asking

This report covers one angle of the growing conflict between behind-the-meter fuel cell adoption for energy independence and the risks associated with natural gas. The questions that matter most depend on your work.

- What is actually happening with Amazon’s 228 BTM fuel cell project since the legal challenges were filed?

- What is the outlook for natural gas-powered BTM fuel cell deployment in hospitals and campuses by 2026?

- Which hospital and university campus operators are adopting BTM fuel cells for grid independence?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.