Ammonia Cracking Deployment, AFC Energy $2 M Komatsu Deal, 30 Ton/Day Air Liquide Pilot, and 5+ Projects (2021 to 2026)

Commercial Adoption, AFC Energy’s Decentralized Model vs. Air Liquide’s Centralized Hubs

The ammonia cracking market is bifurcating into two distinct commercialization pathways, a strategic divergence that became clear in 2026. The first track involves large-scale, centralized cracking facilities at industrial ports to enable global hydrogen trade, while the second focuses on decentralized, modular systems designed for on-site power generation and transportation.

- Prior to 2025, market activity was dominated by research, development, and small-scale component testing. The primary focus was on catalyst efficiency and reactor design in laboratory settings, with limited real-world deployment data available.

- In 2026, Air Liquide operationalized this centralized model by starting the world’s first industrial-scale ammonia cracking pilot at the Port of Antwerp-Bruges, with a capacity of 30 tons per day. This approach targets the decarbonization of shipping and major industrial clusters.

- Concurrently, AFC Energy is validating the decentralized model, securing a UK permit to sell hydrogen from its pilot plant and signing a $2 million joint development agreement with Komatsu to integrate its modular crackers with industrial engines. This strategy aims to eliminate hydrogen transport logistics for end-users in mining, construction, and off-grid power.

- This dual-track development shows the market is not converging on a single solution but is instead creating tailored systems for different value chains. Centralized hubs serve commodity hydrogen markets, while decentralized units serve specialized, high-value end-use applications.

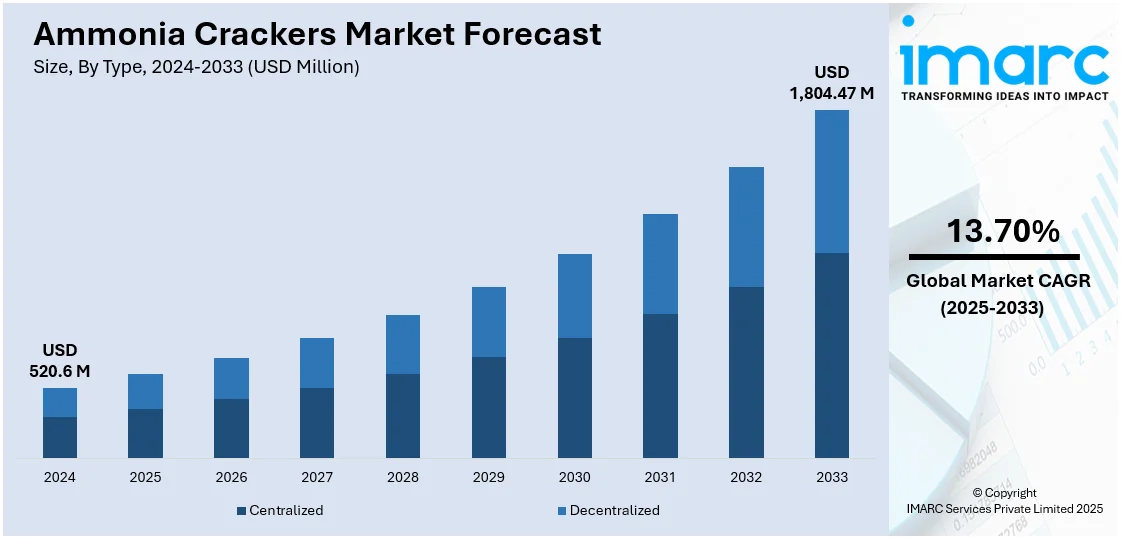

Decentralized vs. Centralized Market Split Forecast

This chart perfectly visualizes the section’s core theme, the market’s bifurcation into centralized and decentralized models, by forecasting the growth and changing share of each segment.

(Source: IMARC Group)

$9.5 M+ in Startup Funding, AFC Energy and Ammobia Secure Capital

Investment patterns in 2026 reveal a flow of capital toward both integrated technology developers and specialized component innovators, signaling investor confidence in the entire value chain. Funding has moved from early-stage R&D toward companies with clear commercialization roadmaps and partnerships with established industrial players.

- Venture capital is backing novel catalyst and process technologies that promise significant efficiency gains. In January 2026, Ammobia raised $7.5 million to scale its low-cost ammonia production technology, while deep-tech startup Cat Ammon is developing ceramic-based catalysts it claims can reduce the cracking process energy requirement by 50%.

- Established industrial end-users are now directly funding technology integration. Komatsu’s $2 million agreement with AFC Energy represents strategic capital deployed to accelerate the development of a specific application, de-risking the technology for its own heavy equipment market.

- The market is also seeing investments from project developers into scaling up. Amogy, a US-based startup, secured a joint venture with GS E&C to advance ammonia-based distributed power generation, demonstrating a financial commitment to move from standalone systems to integrated power projects.

Table: Ammonia Cracking Investments and Funding (2026)

| Company / Funder | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Amogy / GS E&C | Apr 2026 | Signed a joint venture agreement to combine Amogy’s cracking technology with GS E&C’s EPC expertise for distributed power generation projects. | Yahoo Finance |

| Ammobia | Jan 2026 | Raised $7.5 million to scale its low-cost, low-pressure ammonia production technology, which is critical for supplying feedstock to the cracking value chain. | Tech Crunch |

| AFC Energy / Komatsu Ltd. | Feb 2026 | Komatsu committed approximately $2 million through a Joint Development Agreement to integrate AFC’s ammonia cracker with its industrial diesel engines, directly funding application-specific development. | Gasworld |

AFC Energy’s $2 M Komatsu Deal Signals End-Use Integration Focus

Strategic partnerships in 2026 have pivoted from pure research collaboration to application-focused integration, directly linking cracker technology with specific commercial end-uses. These alliances are designed to create clear demand pathways and validate the economic case for ammonia-to-power solutions in heavy industry, shipping, and data centers.

AFC Energy Cracker Integrated With Engine

The chart provides a technical schematic for the exact concept discussed in the section—AFC Energy’s technology integrated with an engine, illustrating the “end-use integration focus.”

(Source: Ammonia Energy Association)

- Between 2021 and 2024, partnerships were primarily among research institutions and technology developers focused on fundamental science. The goal was to prove technical feasibility rather than to develop a commercial product.

- The AFC Energy and Komatsu JDA signed in February 2026 marks a significant shift. It pairs a technology provider with a major OEM to co-develop a market-ready solution for retrofitting heavy machinery, with plans to scale up to 40 MW installations.

- Similarly, Amogy’s memorandum of understanding to explore deploying its systems in Asia’s digital sector and its partnership with Hoku Infrastructure for data centers in Japan targets a high-value, high-reliability power market.

- Industrial consortiums are also forming to tackle large-scale integration. Mitsubishi Heavy Industries and NGK Insulators are jointly developing a membrane purification system for cracked ammonia, a critical enabling technology for producing high-purity hydrogen required by fuel cell applications.

Table: Ammonia Cracking Strategic Partnerships (2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Amogy / Hoku Infrastructure | Mar 2026 | Partnered to advance ammonia-to-power projects specifically for data centers in Japan, targeting a high-growth sector with significant decarbonization needs. | Globe Newswire |

| AFC Energy / Komatsu Ltd. | Feb 2026 | Signed a $2 million JDA to integrate AFC’s ammonia cracker with Komatsu’s industrial engines, aiming to create a decarbonization pathway for heavy equipment. | International Rental News |

| H 2 SITE / Norwegian Maritime Sector | Jan 2026 | Launched a Norwegian subsidiary to accelerate the supply of its membrane reactor-based ammonia crackers for onboard maritime applications, targeting a key decarbonization market. | Offshore Energy |

| Uniper / Thyssenkrupp Uhde | Mar 2026 | Collaborating to build the world’s first megawatt-scale ammonia cracking demonstration plant, signaling a push to integrate the technology into Germany’s industrial energy system. | Table.Media |

Europe and Asia Lead, AFC Energy and Uniper Build Out Infrastructure

Europe has established itself as the primary hub for ammonia cracking pilot projects and technology validation, while Asia is emerging as the key demand center driving long-term offtake agreements and market pull. This geographical split reflects Europe’s focus on building a hydrogen supply infrastructure and Asia’s strategic need for new energy import vectors.

New Uses to Triple Ammonia Demand

This chart quantifies the long-term market pull from new applications, explaining why regions like Asia are emerging as the “key demand center” mentioned in the section.

- From 2021 to 2024, nearly all significant research and early-stage development was concentrated in Europe and North America, driven by public funding and academic research consortia.

- In 2026, Europe is the clear leader in physical deployment. Key projects include Air Liquide’s industrial pilot in Belgium, Duiker Clean Technologies’ system in the Port of Rotterdam, and the Uniper–Thyssenkrupp megawatt-scale plant in Germany. The UK’s AFC Energy also secured its commercial permit in 2026.

- Asia, particularly Japan and South Korea, is creating the demand signals necessary for large-scale investment. Amogy’s partnerships targeting Japanese data centers and the $3 billion green ammonia supply agreement between India’s Reliance and South Korea’s Samsung C&T underscore the region’s role as the principal offtaker.

- The Middle East, specifically Saudi Arabia, is positioning itself as a major production hub, with projects like the Acwa Power facility using Topsoe’s technology to produce green ammonia intended for export to markets like Germany.

Technology Validation, AFC Energy Permit and Topsoe’s Low-Risk Assessment

Ammonia cracking technology has matured from the concept validation phase to the operational deployment phase, with key milestones in 2026 confirming its technical and commercial readiness for near-term investment. The focus has shifted from proving that ammonia can be cracked to demonstrating it can be done reliably, efficiently, and economically at scale.

Topsoe Validates High-Efficiency Cracking Technology

The section highlights Topsoe’s technology validation, and this chart from Topsoe directly illustrates that point by detailing the process’s high efficiency and capacity, confirming its commercial readiness.

(Source: Ammonia Energy Association)

- In the period of 2021-2024, technology readiness was low, with most systems operating at the laboratory or small prototype level. Key challenges included catalyst degradation, low efficiency, and the inability to produce high-purity hydrogen required for sensitive applications.

- AFC Energy’s revised permit from the UK Environment Agency in February 2026 is a critical validation point. It allows the company to sell hydrogen, transforming the technology from a cost center into a potential revenue-generating asset and proving it meets regulatory standards.

- The positive independent assessment of Topsoe’s H 2 Retake™ technology in January 2026 provided a third-party validation of a low commercialization risk, giving investors and project financiers the confidence needed to back large-scale projects.

- Companies are now demonstrating integrated systems that address specific market needs. The EU-backed COUPLE Project, launched in 2026, aims to showcase a system that produces high-purity, pressurized hydrogen suitable for PEM systems and other fuel cell types.

SWOT Analysis, AFC Energy and the Ammonia Cracking Market (2021 to 2026)

The strategic position of ammonia cracking has strengthened considerably, moving from a technology with theoretical potential to one with demonstrated commercial applications and regulatory approval. However, challenges related to cost competitiveness and infrastructure build-out remain.

Advanced Reactors Address Cracking Efficiency Weakness

This chart illustrates a technological solution to the “high energy penalty,” a key weakness identified in the section’s SWOT analysis, by showing how advanced reactors can dramatically improve efficiency.

(Source: Ammonia Energy Association)

- Strengths: The core strength has shifted from ammonia’s energy density to the proven viability of cracking technology, as demonstrated by multiple industrial-scale pilots in 2026.

- Weaknesses: The inherent energy loss and associated cost of the cracking process remains a primary weakness, though companies like Duiker claim efficiencies over 90%.

- Opportunities: The biggest opportunity is the integration with specific end-use markets like heavy machinery (AFC Energy/Komatsu) and data centers (Amogy), creating new value propositions.

- Threats: The primary threat is the timeline and cost of building out both green ammonia production facilities and the associated logistics infrastructure required to supply the crackers.

Table: SWOT Analysis for Ammonia Cracking for Power (2021 to 2026)

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | High energy density of ammonia and existing global transport infrastructure. Technology was largely theoretical. | Demonstrated operational viability at scale (Air Liquide’s 30-ton/day pilot). Low commercialization risk validated by third parties (Topsoe assessment). | The technology moved from a theoretical advantage to a proven, de-risked system with regulatory approval (AFC Energy’s permit). |

| Weaknesses | High energy penalty of cracking process. Concerns over catalyst durability and purity of hydrogen output. | Energy efficiency remains a focus, but companies claim high performance (AFC’s 9.5 k Wh/kg H₂). Purity is being addressed by integrated membrane systems (MHI/NGK). | Performance claims are becoming more concrete and are being addressed with integrated system designs, though levelized cost remains a key hurdle. |

| Opportunities | Broad potential in decarbonizing power and transport sectors. Largely undefined market segments. | Specific high-value markets are being targeted: heavy machinery (Komatsu), data centers (Amogy), and off-grid power (AFC’s Balearic Islands project). | The market opportunity has become more defined and tangible, shifting from broad concepts to targeted, application-specific business cases. |

| Threats | Competition from other hydrogen carriers (LOHCs, methanol). High cost of green ammonia production. | Pace of infrastructure build-out for green ammonia supply. Volatility in energy prices impacting the economics of cracking versus alternatives. | The primary threat has shifted from technological competition to the logistical and economic challenges of scaling the entire green ammonia value chain. |

Scenario Outlook: Cost Reduction and Bankability Will Determine Market Leaders

The next 24-36 months will be defined by a race to achieve economic viability and bankability, shifting the competitive focus from proving technical feasibility to driving down the levelized cost of cracked hydrogen. If developers can successfully demonstrate cost-effective and reliable operations in their pilot projects, we will see a rapid acceleration in large-scale commercial offtake agreements.

Hydrogen Purity Demands Drive System Costs

This chart highlights the stringent hydrogen purity requirements for key applications like fuel cells, a key challenge that directly impacts the “cost reduction and bankability” theme of the section.

(Source: Ammonia Energy Association)

- Watch for efficiency improvements: The most critical signal will be operational data from pilots run by Air Liquide, Duiker, and Uniper. Evidence of sustained high energy efficiency (above 90%) and catalyst performance will be necessary to secure project financing for next-generation plants.

- Monitor end-use integration success: The progress of the AFC Energy/Komatsu partnership is a key indicator. A successful demonstration of cracked ammonia powering heavy equipment would unlock a massive and replicable market, validating the decentralized model.

- Track the first wave of commercial contracts: The first significant, multi-year contracts for cracked hydrogen will signal true market creation. AFC Energy’s 20 MW plant for the Balearic Islands is an early example; more such deals are needed to prove bankability.

- Expect divergence in technology choice: Companies focused on high-purity applications like solid oxide fuel cells will favor more complex systems with integrated purification, while those in industrial heating or engine combustion may opt for simpler, lower-cost crackers that tolerate trace ammonia.

The questions your competitors are already asking

This report covers one angle of the ammonia cracking market’s bifurcation into centralized and decentralized commercial models. The questions that matter most depend on your work.

- Which companies are gaining ground in the ammonia cracking market: AFC Energy with its decentralized model or Air Liquide with its centralized hubs?

- Is AFC Energy’s $2 million partnership with Komatsu progressing from pilot to commercial deployment for industrial engines?

- How do decentralized, modular crackers for on-site power compare to centralized, industrial-scale systems for hydrogen trade?

- Which mining and construction operators are adopting on-site ammonia cracking for power?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.