Halliburton’s Hydrogen Pivot 2026: Why Subsurface Services Outweigh Production

From Theory to Commercial Scale: Halliburton’s Hydrogen Service Evolution

Halliburton’s hydrogen strategy has decisively shifted from broad exploration to the commercial deployment of enabling services, focusing on subsurface storage and technology incubation rather than direct hydrogen production. Between 2021 and 2024, the company established its approach by repurposing existing oil and gas tools for hydrogen pilots and building a portfolio of clean-tech startups through Halliburton Labs. The period from 2025 to today marks a significant acceleration, with the company securing major commercial contracts for carbon capture projects that serve as direct analogues for hydrogen storage and advancing specific hardware solutions designed to bypass critical infrastructure bottlenecks.

- The early period (2021-2024) was defined by foundational projects and partnerships. This included a contract for the Hy Net North West blue hydrogen project’s carbon storage component and a successful pilot with Energy Stock in the Netherlands, which proved that existing well completion tools could be used for pure hydrogen storage in salt caverns.

- From 2025 onwards, the strategy translated into larger, more complex commercial agreements. Halliburton secured contracts for major Carbon Capture and Storage (CCS) projects like the Northern Endurance Partnership (NEP) in the UK and the In Capture JV project in Australia, leveraging its digital and subsurface expertise to build workflows directly transferable to Underground Hydrogen Storage (UHS).

- Technology incubation via Halliburton Labs evolved from investing in a range of concepts to a focused push on market-ready solutions. The March 2026 inclusion of Proof Energy demonstrates this, as its metallic solid oxide fuel cell (SOFC) technology utilizes hydrogen carriers like ammonia and methanol, addressing the core challenge of hydrogen transportation and storage.

- The company also began positioning its core competencies for emerging frontiers. By adapting its drilling and seismic imaging technologies, Halliburton is preparing for the geological hydrogen (“white” hydrogen) market, a domain that was purely conceptual in the prior period but is now a target for commercial exploration services.

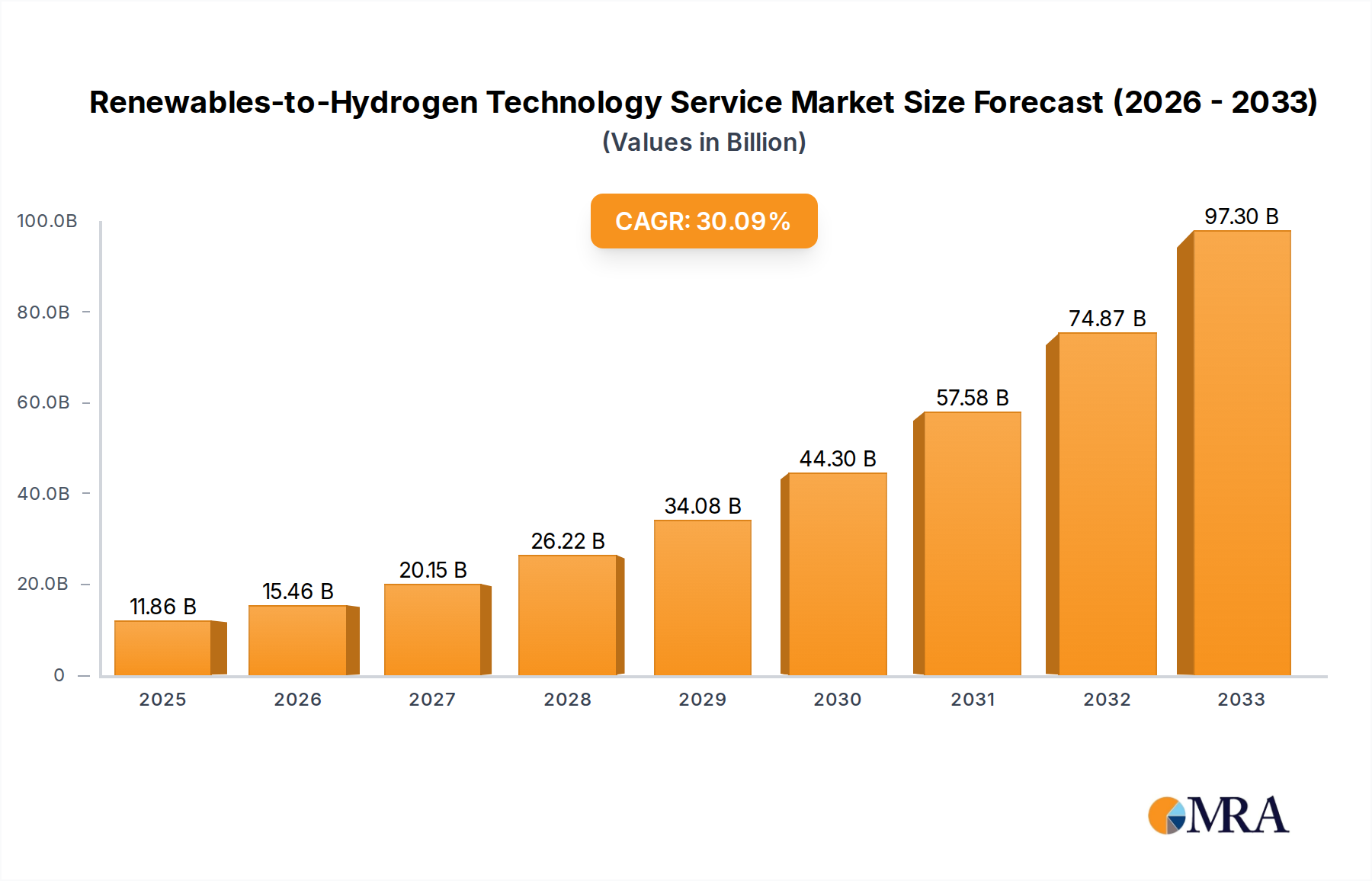

Hydrogen Service Market Poised for Growth

The projected growth of the hydrogen service market to over $97 billion provides the commercial context for Halliburton’s strategic shift from theory to deployment.

(Source: www.marketreportanalytics.com)

Investment Shifts to Strategic Infrastructure and Technology Scaling

Halliburton’s investment pattern has transitioned from providing seed-stage support across a wide array of clean technologies to making targeted capital injections into physical infrastructure and mature startups poised for commercial scaling. While Halliburton Labs continues to be the primary vehicle for early-stage exposure, the 2024 direct investment in Namibia signifies a new phase of enabling entire hydrogen ecosystems in frontier markets. This approach minimizes capital risk while positioning the company as an indispensable service partner for large-scale hydrogen development.

- The Halliburton Labs program represents a consistent, low-capital investment strategy to gain insight and potential ownership in disruptive technologies. Between 2021 and 2024, it onboarded multiple hydrogen-related startups, including Sun Green H 2 (electrolyzer components), Fuel X (solid-state hydrogen), and Ayrton Energy (liquid hydrogen transport).

- A major strategic shift occurred in May 2024 with the direct investment of approximately $10 million (N$183 M) in a new liquid mud and completion fluids plant in Walvis Bay, Namibia. This investment was explicitly linked to supporting the nation’s ambitious green hydrogen development plans, moving beyond incubation to building tangible, on-the-ground infrastructure.

- The continued support for Proof Energy, which joined the lab program in 2022 and was highlighted again in March 2026, shows a focus on shepherding promising technologies toward commercial readiness. This demonstrates a long-term commitment to a select few high-potential companies.

Table: Halliburton Hydrogen-Related Investments (2023-2024)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| New Liquid Mud & Completion Fluids Plant | May 2024 | Direct investment of ~$10 Million in a plant in Walvis Bay to support Namibia’s emerging green hydrogen sector, marking a pivot to physical infrastructure. | [PDF] Mining and Energy |

| Ayrton Energy | Dec 2023 | Incubation through Halliburton Labs to develop technology for liquid hydrogen storage and transport, addressing a key infrastructure gap. | Halliburton |

| Fuel X | Apr 2023 | Accelerator support for commercializing solid-state hydrogen fuel systems, offering a high-density alternative to batteries and compressed hydrogen. | Fuel Cells Works |

| Sun Green H 2 | Jan 2023 | Accelerator support to scale manufacturing of high-performance electrolyzer components, aiming to reduce the cost of green hydrogen production. | Business Wire |

Partnerships Mature From Research to Major Commercial Contracts

Halliburton’s partnership strategy has matured from academic and early-stage technology collaborations to securing service contracts with global energy majors for large-scale decarbonization projects. The initial phase focused on building knowledge and exploring possibilities, such as the 2023 partnership with TU Delft on underground hydrogen storage research. By 2025, these foundational efforts evolved into multi-year commercial agreements with consortia led by BP, Equinor, and Total Energies, cementing Halliburton’s role as a key service provider for the infrastructure underpinning the hydrogen economy.

Hydrogen Storage Market Opportunity Soars

The significant expansion of the hydrogen storage market to nearly $90 billion justifies Halliburton’s focus on maturing research partnerships into large-scale commercial contracts.

(Source: www.fortunebusinessinsights.com)

- In 2022 and 2023, partnerships were primarily geared towards technology integration and research. This included an agreement with Cera Phi Energy to support geothermal projects for green hydrogen and a collaboration with TU Delft to foster talent in the UHS sector.

- The period from 2025 to 2026 is characterized by high-value service contracts. The agreement with the Northern Endurance Partnership (NEP) in August 2025 to provide digital monitoring for the UK’s first offshore CCS project is a landmark deal, establishing a commercial blueprint for future hydrogen storage monitoring.

- The collaboration with Pertamina in March 2026 on an unconventional fracturing program in Indonesia, while focused on oil and gas, builds critical subsurface characterization capabilities directly applicable to future UHS and geological hydrogen projects in the strategic Southeast Asian market.

- Technology incubation partnerships also deepened, with the March 2026 announcement on Proof Energy highlighting a focus on scaling proven concepts rather than just exploring new ones. This signals a move from sourcing innovation to commercializing it.

Table: Key Halliburton Hydrogen-Relevant Partnerships (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Pertamina | Mar 2026 | Strategic collaboration on unconventional fracturing, building subsurface expertise applicable to future hydrogen storage and exploration in Indonesia. | Energies Media |

| Proof Energy | Mar 2026 | Technology incubation to scale metallic solid oxide fuel cells that use hydrogen-carrier fuels, bypassing H 2 infrastructure hurdles. | Business Wire |

| Northern Endurance Partnership (BP, Equinor, Total Energies) | Aug 2025 | Service contract for digital subsurface monitoring on a major UK CCS project, developing commercial workflows transferable to hydrogen storage. | Offshore Energy |

| In Capture Joint Venture | Mar 2025 | Collaboration agreement for technical assessment of a commercial-scale CCS project in Australia, building expertise for underground hydrogen storage. | World Oil |

Geographic Focus Expands From Europe to Frontier Hydrogen Markets

Halliburton’s geographical strategy for hydrogen-related services has expanded from established European energy hubs to high-potential frontier markets in Africa and Australia. Between 2021 and 2024, activities were concentrated in the UK and the Netherlands, focusing on pilot projects and the CCS components of blue hydrogen initiatives like Hy Net North West. The period from 2025 to today shows a clear strategy to secure early-mover advantage in new regions, evidenced by the $10 million infrastructure investment in Namibia and major CCS assessment work in Australia, positioning the company for future green and geological hydrogen growth.

Frontier Hydrogen Markets Show Strong Growth

Rapid growth in new regions, such as the Middle East’s projected market, validates Halliburton’s strategy of expanding its geographic focus to capture early-mover advantage.

(Source: www.grandviewresearch.com)

- The early focus (2021-2024) was on Europe, leveraging existing infrastructure and strong regulatory support for decarbonization. The Energy Stock pilot in the Netherlands and the Hy Net project in the UK were critical for proving the technical and commercial viability of repurposing oil and gas services.

- In 2024, Halliburton made a significant strategic move into Africa with its investment in Walvis Bay, Namibia. This positions the company to support Namibia’s large-scale green hydrogen ambitions, moving beyond established markets to capture growth in a region with immense renewable potential.

- Australia emerged as another key region in 2025 with the In Capture JV agreement for a commercial-scale CCS project. This work provides a direct technical and commercial analogue for developing the large-scale underground hydrogen storage required to support Australia’s hydrogen export goals.

- The continued work in the UK with the Northern Endurance Partnership project in 2025 demonstrates a commitment to maintaining leadership in mature markets while simultaneously expanding into new territories.

Technology Matures From Adaptation to Purpose-Built Solutions

Halliburton’s technology strategy has evolved from adapting existing oil and gas products for hydrogen applications to developing purpose-built systems for adjacent markets and incubating hardware that solves fundamental hydrogen challenges. The initial period (2021-2024) focused on proving that tools like subsurface safety valves and packers could work in pure hydrogen environments. By 2025-2026, the focus shifted to launching specialized products like the XTR CS injection system for CCUS and supporting technologies like Proof Energy’s SOFC, which are designed to accelerate decarbonization by circumventing infrastructure constraints.

Overcoming Key Hydrogen Technology Barriers

This overview highlights the technical and cost barriers in storage and transport that Halliburton’s new purpose-built technology solutions are designed to address.

(Source: www.sciencedirect.com)

- During 2021-2024, the primary technological achievement was validating existing completion tools for pure hydrogen storage, as demonstrated in the Energy Stock pilot. This confirmed the relevance of Halliburton’s core product portfolio.

- In January 2026, Halliburton launched the XTR CS injection system. While designed for CCUS, its development of reliable, long-term injection and well integrity principles is foundational for creating secure underground hydrogen storage facilities.

- The incubation of Proof Energy’s metallic SOFC technology in March 2026 marks a move up the value chain. Instead of only providing services for storage, Halliburton is now enabling a technology that reduces the need for costly, high-pressure hydrogen infrastructure altogether by using carrier fuels.

- The company is also strategically positioning its existing suite of subsurface characterization and drilling technologies for the emerging geological (“white”) hydrogen market. This represents an adaptation of mature, world-leading technologies for a new, high-growth energy sector without requiring new product development.

SWOT Analysis: Halliburton’s Subsurface Hydrogen Strategy

Halliburton’s strategic position in the hydrogen economy is defined by its core strength in subsurface engineering, creating a defensible niche in storage and exploration. This approach, however, leaves it dependent on the pace of market development for storage services and the success of its incubated technologies. The key change from the early 2020 s to 2025-2026 has been the validation of this strategy through major commercial contracts, moving from a theoretical advantage to a proven business model.

Storage Market Growth Validates Niche Strategy

A projected $27 billion hydrogen storage market underscores the opportunity in Halliburton’s niche strategy, while also highlighting its dependence on this market’s development.

(Source: straitsresearch.com)

Table: SWOT Analysis for Halliburton’s Hydrogen Initiatives

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Deep expertise in subsurface characterization, drilling, and well completions. Established Halliburton Labs as an innovation pipeline. | Leveraging core competencies to win major CCS contracts (NEP, In Capture). Adapting technology for geological hydrogen exploration. | The company validated its ability to convert subsurface expertise into commercial contracts for energy transition projects, proving its core O&G business is a direct strength. |

| Weaknesses | Indirect exposure to the hydrogen market, reliant on others’ production projects. Incubation model carried startup failure risk. | Strategy remains focused on enabling services, potentially missing out on direct hydrogen production revenue. Success is tied to the scaling of UHS and geological H 2 markets. | The weakness remains but is mitigated. By focusing on enabling services, Halliburton avoids direct competition with producers like Shell and reduces capital exposure, turning a potential weakness into a calculated risk management strategy. |

| Opportunities | Emerging market for Carbon Capture and Storage (CCS) as a proxy for hydrogen storage. Early-stage exploration of natural hydrogen. | Leading role in the global build-out of Underground Hydrogen Storage (UHS). First-mover advantage in geological hydrogen services. Commercialization of incubated tech like Proof Energy’s SOFC. | Opportunities have become more concrete. The global need for large-scale energy storage has made UHS a major commercial prospect, and geological hydrogen has moved from academic papers to an active exploration target. |

| Threats | Competitors (e.g., SLB) investing directly in electrolysis technology. Slower-than-expected development of blue/green hydrogen projects. | Alternative storage solutions could gain traction. A slowdown in CCS project approvals could delay the development of shared infrastructure and expertise for UHS. | The primary threat shifted from being technologically outmaneuvered in production to the market/regulatory risk of the storage sector itself. Delays in CCS projects are now a direct threat to the development of Halliburton’s core hydrogen-related business. |

Scenario Modelling: 2026 Hydrogen Trajectory and Key Signals

The critical catalyst for Halliburton’s next growth phase in hydrogen will be securing its first commercial contract for a dedicated geological hydrogen exploration project or the formal launch of a bundled Underground Hydrogen Storage (UHS) service line. This event would confirm the transition from leveraging adjacent projects (CCS) to directly commercializing its core competencies in new hydrogen frontiers. The company has laid the groundwork; now, market adoption is the key variable.

Global Hydrogen Market Projects Strong Growth

The forecasted growth of the total hydrogen market to over $360 billion by 2032 provides the macro-level context for Halliburton’s future scenarios and next growth phase.

(Source: www.persistencemarketresearch.com)

- If market demand for large-scale storage accelerates, watch this: Monitor for the formal launch of a dedicated UHS business unit. The hiring of roles like a “Low Carbon Solutions Marketing Manager” in February 2026 indicates a strategic push to commercialize these services, and a formal business line would be the next logical step.

- This could be happening now: The company is actively bundling its expertise from recent CCS projects (NEP, In Capture) into a standardized offering for UHS site selection, well design, and long-term monitoring.

- If incubated technology proves viable, watch this: Look for the first pilot or commercial deployment of Proof Energy’s SOFC technology, potentially in partnership with a major logistics or power company. This would validate the Halliburton Labs model and could lead to a deeper partnership or acquisition.

- This could be happening now: Following its March 2026 inclusion in the accelerator, Proof Energy is likely using Halliburton’s network to engage with potential offtakers and industrial partners to plan its first field deployment.

- If geological hydrogen gains commercial traction, watch this: The first announcement of Halliburton securing a contract specifically for “white” hydrogen exploration and drilling. Events like the “Drilling for Hydrogen 2026” conference are key venues for such developments.

- This could be happening now: Halliburton is likely in confidential discussions with junior exploration companies and research consortiums, adapting its seismic and reservoir modeling software for natural hydrogen targets.

Frequently Asked Questions

Why is Halliburton focusing on hydrogen storage and services instead of producing hydrogen?

Halliburton is leveraging its core strengths in subsurface engineering, drilling, and well completions. This strategy allows the company to dominate a specialized service niche (storage and exploration) where it has a clear competitive advantage, rather than entering the capital-intensive hydrogen production market. This approach minimizes financial risk while making Halliburton an indispensable infrastructure partner for the hydrogen economy.

What is the significance of Halliburton’s work on Carbon Capture and Storage (CCS) projects?

The CCS projects are crucial because they serve as direct commercial and technical analogues for Underground Hydrogen Storage (UHS). The expertise, digital workflows, and well integrity technologies developed for injecting and monitoring CO2 in projects like the Northern Endurance Partnership are directly transferable to storing hydrogen. This allows Halliburton to build and prove its business model for the future hydrogen storage market.

How has Halliburton’s investment strategy for hydrogen evolved?

The company’s investment pattern has shifted from providing broad, low-capital seed support to startups via Halliburton Labs to making targeted, direct capital injections into physical infrastructure. The May 2024 investment of approximately $10 million in a new plant in Namibia to support its green hydrogen sector marks this pivot, showing a move from incubating ideas to building tangible, on-the-ground assets in frontier markets.

What is ‘geological hydrogen’ and what is Halliburton’s role in it?

Geological hydrogen, also known as ‘white’ hydrogen, is naturally occurring hydrogen found in underground deposits. Halliburton is positioning itself to become a key service provider for this emerging market by adapting its existing, world-leading technologies in seismic imaging, drilling, and subsurface characterization to help find and produce this new energy source.

How does incubating a company like Proof Energy fit into Halliburton’s overall strategy?

Supporting Proof Energy, which develops fuel cells that use hydrogen carriers like ammonia and methanol, is a strategic move to solve a key industry bottleneck: hydrogen transportation and storage. By backing a technology that bypasses the need for costly, high-pressure hydrogen infrastructure, Halliburton is moving up the value chain from just providing storage services to enabling technologies that can accelerate the adoption of hydrogen altogether.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.