Direct Air Capture 2026: How Policy and Capital Force Commercial Maturity

Direct Air Capture Adoption: From Pilots to Integrated Industrial Value Chains

Corporate adoption of Direct Air Capture (DAC) has fundamentally shifted from small-scale carbon credit purchases to strategic integration into industrial value chains, a transition driven by the need for high-quality carbon removal and new revenue streams from carbon utilization. This evolution marks the sector’s move from speculative pilots to commercially grounded projects with bankable offtake agreements.

- Between 2021 and 2024, corporate engagement was characterized by early, high-cost carbon credit purchases from pilot plants, such as Swiss Re‘s $10 million, 10-year deal with Climeworks in 2021. These deals were critical for validating the voluntary carbon market for DAC but were limited in scale.

- The period from 2025 to today shows a distinct shift towards large-scale offtake agreements and carbon-to-value applications. Buyer coalitions like Frontier committed millions to pre-purchase carbon removal, as seen in its $41 million deal with Arbor for bioenergy with carbon capture and storage (BECCS). This provides the revenue certainty needed for project financing.

- Recent activity demonstrates a broadening of applications beyond simple sequestration. The partnership between Dutch company Skytree and Koppercress uses captured CO₂ to enhance crop growth, while the joint venture between Occidental and ADNOC to evaluate a $500 million DAC facility in Texas signals integration with the energy sector’s core operations.

- The expansion into sectors like sustainable aviation fuel (SAF) and building materials is creating new, high-value end markets. This diversification de-risks project economics by moving beyond a sole reliance on the volatile carbon credit market.

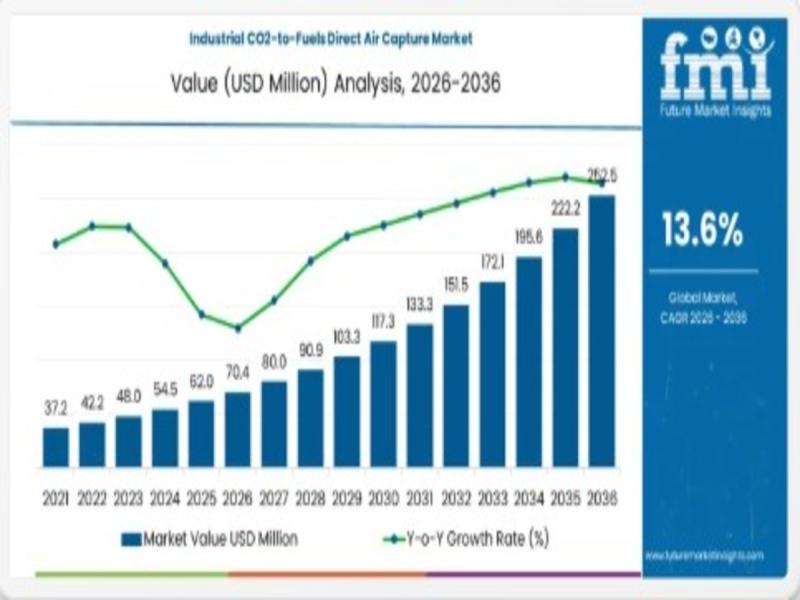

CO2-to-Fuels Market Growth Forecast

This chart illustrates a key industrial value chain, projecting the growth of the CO2-to-fuels market, which aligns with the section’s focus on new revenue streams from carbon utilization.

(Source: openPR.com)

Investment Analysis: From Venture Hype to Strategic Project Finance

Investment in Direct Air Capture has transitioned from large, generalized venture capital rounds that fueled technology hype to more targeted, strategic financing aimed at deploying specific commercial-scale projects. This change reflects a maturing market where investors now require clear line-of-sight to revenue, often secured by policy incentives and long-term offtake agreements.

DAC Venture Investment Peaked in 2022

The chart directly supports the section’s analysis by showing the 2022 spike in venture capital, followed by a decline, visualizing the shift from hype-driven mega-rounds.

(Source: Global Venturing)

- The 2022 period was defined by record-breaking venture funding, exemplified by Climeworks‘ massive $650 million financing round, which signaled strong investor belief in the technology’s long-term potential but was not tied to immediate project deployment.

- By 2024 and 2025, the investment pattern shifted towards project-specific and strategic corporate financing. Carbon Capture Inc.‘s $80 million Series A in March 2024 was explicitly for scaling its modular DAC systems, while Aramco Ventures‘ seed funding for Ucaneo in March 2025 demonstrates strategic investment by energy majors to gain access to new DAC technology.

- The decline in average VC deal size from a peak in 2022, despite a rising number of deals through 2024, indicates a move away from “moonshot” funding toward more milestone-driven, capital-efficient investments in a new generation of startups like Spiritus.

- The primary driver of large-scale capital deployment is now government programs, such as the U.S. Department of Energy’s $1.2 billion allocation for DAC hubs, which leverages private capital and de-risks the enormous upfront costs of first-of-a-kind commercial plants.

Table: Key Investments in Direct Air Capture & Carbon Removal

| Recipient / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Pronoe and Cella | Jan 2026 | Frontier signed pre-purchase agreements worth $3.05 million with two early-stage carbon removal companies, providing catalytic capital to scale new technologies. | Data Center Dynamics |

| Ucaneo | Mar 2025 | Aramco Ventures joined a seed funding round to advance Ucaneo‘s novel, solvent-based DAC technology, signaling strategic interest from a major energy firm. | IBB Ventures |

| Carbon Capture Inc. | Mar 2024 | Closed an $80 million Series A financing round led by Prime Movers Lab to accelerate the development and deployment of its modular DAC systems. | PR Newswire |

| Climeworks | Apr 2022 | Raised approximately $650 million (EUR 582 M) in a record-breaking equity round from investors including GIC and Baillie Gifford to scale up its DAC technology. | Club CO 2 |

Partnership Dynamics: Alliances Shift to Underwrite Commercial Deployment in 2026

Strategic partnerships in the Direct Air Capture market have evolved from technology-focused collaborations to offtake-driven alliances designed to underwrite the development of large-scale commercial facilities. This shift from R&D to revenue generation is a primary signal of the industry’s progression toward commercial maturity.

- Before 2024, partnerships were often centered on technology validation and pilot projects. These early collaborations were crucial for proving technical concepts but lacked the scale to drive significant market growth.

- Starting in 2025, partnerships became dominated by major corporate and industrial players forming joint ventures and signing large-scale offtake agreements. The proposed $500 million joint venture between Occidental and ADNOC to build a DAC plant is a landmark event, combining project execution expertise with access to capital.

- Corporate buying coalitions have become a dominant force. Frontier, a coalition including Google and Meta, has committed millions through offtake agreements, creating a bankable demand signal that allows developers like Arbor and Charm Industrial to secure project financing.

- Partnerships are also emerging in adjacent sectors to create integrated value chains. Caterpillar‘s collaboration with One PWR and Vero 3 on a carbon capture system for data centers, with a 500 MW project planned for 2026, highlights the growing demand for decarbonization solutions in high-growth industries.

Table: Notable Strategic Partnerships in Direct Air Capture

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Boeing & Charm Industrial | Nov 2025 | Boeing signed an offtake agreement to purchase carbon removal credits corresponding to 100, 000 tons of CO₂, demonstrating demand from the hard-to-abate aviation sector. | Carbon Credits |

| Occidental & ADNOC | May 2025 | The two energy majors are evaluating a joint venture to build a DAC facility in Texas with a potential investment of up to $500 million, aiming for large-scale carbon removal. | ESG Today |

| Capgemini & Charm Industrial | May 2025 | Capgemini entered a long-term offtake agreement to remove 16, 500 tons of CO₂ via bio-oil sequestration, showcasing durable corporate demand. | Charm Industrial |

| Heirloom & Carbon Cure | Feb 2023 | A partnership to permanently store CO₂ captured via DAC in concrete, creating a scalable carbon utilization pathway and a value-added product. | Carbon Direct |

Geographic Analysis: North America’s Policy Creates DAC Epicenter as Global Interest Grows

North America has solidified its position as the global epicenter for Direct Air Capture deployment, driven by unparalleled policy incentives, while Europe maintains its role as a technology development hub and the Middle East emerges as a region with significant long-term potential. This geographic concentration is a direct result of government actions that have de-risked large-scale investment.

North America to Dominate Global DAC Market

This forecast quantifies North America’s leading role, projecting it will command nearly half the global market, directly supporting the section’s thesis that the region is the DAC epicenter.

(Source: Research Nester)

- Between 2021 and 2024, Europe, particularly Switzerland and Iceland, was at the forefront with Climeworks operating the first commercial-scale plants, Orca and Mammoth. However, these projects were modest in capacity, capturing thousands of tons annually.

- The passage of the U.S. Inflation Reduction Act (IRA) in 2022 marked a decisive shift. Its $180/tonne tax credit, combined with the Department of Energy’s $3.5 billion DAC Hubs program, made the U.S. the most attractive location for large-scale projects. This led to the planning of megaton-scale facilities in Texas and Louisiana.

- By 2025, the impact of U.S. policy became clear, with North America projected to capture nearly 50% of the global DAC market by 2030. Canada is also a key player, with its rising carbon price creating a compliance-driven market for carbon removal.

- The Middle East, particularly the UAE, is an emerging geography to watch. Strategic investments by national oil companies like ADNOC, coupled with abundant low-cost solar resources and favorable geology for storage, position the region for future growth, despite current costs being a barrier.

Technology Maturity: DAC Advances to Commercial Scale (TRL 8-9) Amid Cost Hurdles

Direct Air Capture technology has successfully advanced from the pilot and demonstration phase (TRL 6-7) to the deployment of first-of-a-kind commercial-scale plants (TRL 8-9), yet high costs and energy consumption remain the primary barriers to mass adoption. The critical challenge for the period through 2026 is to validate cost-down curves through operational learning at these new, larger facilities.

DAC Project Scale to Increase Exponentially

The chart visualizes the section’s core theme of technology maturation by showing the projected growth in the average size of DAC projects, reflecting the shift to commercial-scale deployment.

(Source: Sylvera)

- From 2021 to 2024, the market was defined by small-scale commercial plants. Climeworks‘ Orca plant (2021) had a capacity of 4, 000 tons per year, proving the technology’s viability but at a high cost, estimated at over $600/tonne. The commissioning of its Mammoth plant in 2024, with a capacity of 36, 000 tons, demonstrated a clear scaling vector.

- The post-2025 era is defined by the development of megaton-scale projects. Occidental‘s 1 Point Five project in Texas, based on Carbon Engineering‘s liquid-solvent technology, aims to capture up to 1 million tons annually, representing a significant leap in scale.

- While costs remain high ($400-$1, 500/tonne), there is a clear pathway to reduction. Projections target $150-$200/tonne by 2030, driven by economies of scale, manufacturing improvements from modular designs like those of Carbon Capture Inc., and integration with low-cost renewable energy. The central test is whether operational data from new plants validates these projections.

- Emerging technologies, such as electrochemical and membrane-based systems, are in the R&D phase (TRL 4-6) but offer the potential for lower energy consumption. Direct Ocean Capture (DOC) is also being evaluated as a complementary carbon removal pathway.

SWOT Analysis: Direct Air Capture Market 2026

The Direct Air Capture market is at an inflection point where foundational strengths in technology are being amplified by unprecedented policy support, creating opportunities for integrated value chains. However, weaknesses related to cost and scalability, coupled with threats from political and financial volatility, present significant risks to its growth trajectory.

DAC Market Shows Strong Growth to 2026

Aligning with the section’s 2026 SWOT analysis, this chart provides a near-term growth forecast, illustrating the market opportunity that forms a key part of the strategic outlook.

(Source: Fortune Business Insights)

Table: SWOT Analysis for the Direct Air Capture Market

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Demonstrated technical viability at pilot scale (e.g., Climeworks‘ Orca plant). Strong backing from early corporate adopters (e.g., Stripe, Shopify). | Massive policy support (U.S. IRA 45 Q credit). Deployment of first megaton-scale projects (Occidental‘s 1 Point Five). Engagement from energy majors (ADNOC). | The market has moved from being technology-led to policy- and demand-driven. The financial viability of large projects is now anchored by government incentives and large-scale corporate offtake, not just VC funding. |

| Weaknesses | Prohibitively high costs ($600+/tonne). High energy consumption. Unproven scalability beyond thousands of tons per year. | Continued high CAPEX and OPEX for first-of-a-kind commercial plants. Heavy reliance on subsidies, creating dependency risk. Nascent supply chains for key components. | While scale has been demonstrated on paper, the fundamental weakness of high cost remains unresolved. The industry’s reliance on subsidies has deepened, making it vulnerable to the political climate. |

| Opportunities | Sale of high-value carbon credits in the voluntary market. Niche applications and technology licensing. | Integration into industrial value chains (e-fuels, chemicals, building materials). Development of CO₂ transportation and storage infrastructure as a service. Decarbonization of high-growth sectors like data centers. | The business case has expanded from selling a single product (carbon credits) to enabling a circular carbon economy. This diversifies revenue streams and integrates DAC into broader industrial decarbonization efforts. |

| Threats | Investor skepticism about scalability and profitability. Volatility in the voluntary carbon market. | Political risk of subsidy changes or repeal. Sustained high interest rates increasing project financing costs. Failure of initial large-scale projects to meet cost and performance targets. | The primary threat has shifted from technological skepticism to macroeconomic and political uncertainty. Execution risk on the first wave of large projects is now the single biggest threat to investor confidence. |

Scenario Modelling and 2026 Outlook

If the first wave of megaton-scale Direct Air Capture facilities, such as Occidental‘s 1 Point Five project, successfully commence operations by their target dates and provide verifiable data showing a cost trajectory toward $200/tonne, it will trigger a significant de-risking of the sector and unlock the next wave of project finance. Conversely, major delays or performance shortfalls at these flagship projects would severely damage investor confidence and could stall market growth for years.

DAC Market Projected to Exceed $120B

This aggressive long-term forecast visualizes the high-growth scenario discussed in the text, showing the potential market size if key projects succeed and unlock further investment.

(Source: Market.us)

- Watch Signal 1: Operational Performance of Flagship Projects. The most critical signal to monitor is the operational data (uptime, energy consumption, sorbent degradation) from Climeworks‘ Mammoth plant and the initial construction and commissioning phases of the U.S. DAC Hubs. Success is crucial for validating engineering models and cost projections.

- Watch Signal 2: Durability of Corporate Offtake Agreements. The expansion of long-term, binding offtake agreements from corporate buyers, especially through coalitions like Frontier and the First Movers Coalition, is essential. A shift from pre-purchase agreements to legally binding contracts for future capacity will be a key sign of market maturation.

- Watch Signal 3: Stability of Policy Incentives. Any legislative or administrative action in the U.S. that alters the value or duration of the IRA’s 45 Q tax credits would have an immediate and significant impact on project economics across North America, which is currently the market’s center of gravity.

- Traction Gaining: Carbon-to-Value Pathways. The integration of DAC with sustainable aviation fuel (SAF) and green hydrogen production is gaining significant traction. These applications provide an alternative, potentially higher-value revenue stream compared to sequestration, addressing the challenge of the high energy cost of capture.

Frequently Asked Questions

What has been the biggest shift in corporate adoption of Direct Air Capture (DAC) since 2025?

The biggest shift has been from small, high-cost carbon credit purchases to strategic integration into industrial value chains. Companies are now signing large-scale offtake agreements (e.g., through buyer coalitions like Frontier) and forming joint ventures (like Occidental and ADNOC) to build commercial-scale facilities, creating bankable revenue streams beyond the voluntary carbon market.

Why is the U.S. considered the epicenter for DAC development?

The U.S. has become the DAC epicenter due to unparalleled policy support, specifically the Inflation Reduction Act (IRA), which offers a $180/tonne tax credit (45Q). This, combined with the Department of Energy’s $3.5 billion DAC Hubs program, has de-risked large-scale investment and made the U.S. the most financially attractive location for deploying megaton-scale projects.

What are the main challenges still facing the DAC market in 2026?

The primary challenges remain the high cost ($400-$1,500/tonne) and energy consumption of the technology. The industry is also heavily reliant on government subsidies, making it vulnerable to political risks, such as changes to the IRA. Finally, there is significant execution risk, as the failure of the first large-scale commercial plants to meet cost and performance targets could damage investor confidence.

How has investment in DAC technology evolved?

Investment has transitioned from large, speculative venture capital rounds that fueled technology hype (like Climeworks’ $650M round in 2022) to more targeted, strategic financing aimed at deploying specific commercial projects. This new phase is driven by government programs that leverage private capital and long-term offtake agreements that secure revenue for project financing.

What are ‘carbon-to-value’ pathways and why are they important for DAC’s future?

‘Carbon-to-value’ pathways involve using captured CO₂ as a feedstock to create valuable products, rather than simply storing it. Examples from the text include creating sustainable aviation fuel (SAF), concrete, and enhancing crop growth. This is important because it diversifies revenue streams, de-risking project economics and reducing sole reliance on the volatile carbon credit market.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.