China’s Offshore Wind Manufacturing Dominance: How 26 MW Turbines Will Reshape Global Markets in 2026

China’s Industrial Scale Creates Insurmountable Offshore Wind Entry Barriers

By 2025, China’s manufacturing ecosystem for offshore wind achieved a scale and velocity that established a nearly insurmountable competitive barrier for international rivals. The country’s ability to produce and install turbines at an unprecedented rate, driven by a protected domestic market, has fundamentally altered the global risk equation for Western original equipment manufacturers (OEMs) and developers, shifting the competitive focus from regional market share to fundamental supply chain control.

- Between 2021 and 2024, China’s offshore wind capacity grew rapidly, with cumulative installations reaching 27.7 GW by early 2024, effectively matching Europe’s entire historical development. During this period, Chinese OEMs began to dominate global turbine order books, signaling a major shift in manufacturing power.

- The period from 2025 onward marks a dramatic acceleration. In 2025 alone, Goldwind installed 25.9 GW of new capacity within China, a figure that single-handedly surpassed the total global offshore wind additions for the year (19 GW). This industrial velocity was confirmed as Chinese OEMs secured eight of the top ten positions in global turbine orders, which reached a total of 215 GW.

- This scale is a direct result of a self-reinforcing domestic market. Projections for the 2025-2034 period show that Chinese OEMs like Goldwind and Ming Yang will maintain an extreme domestic focus, with over 98% of their connections remaining within China. This protected demand allows them to scale operations and innovate without the immediate pressures of global market diversification.

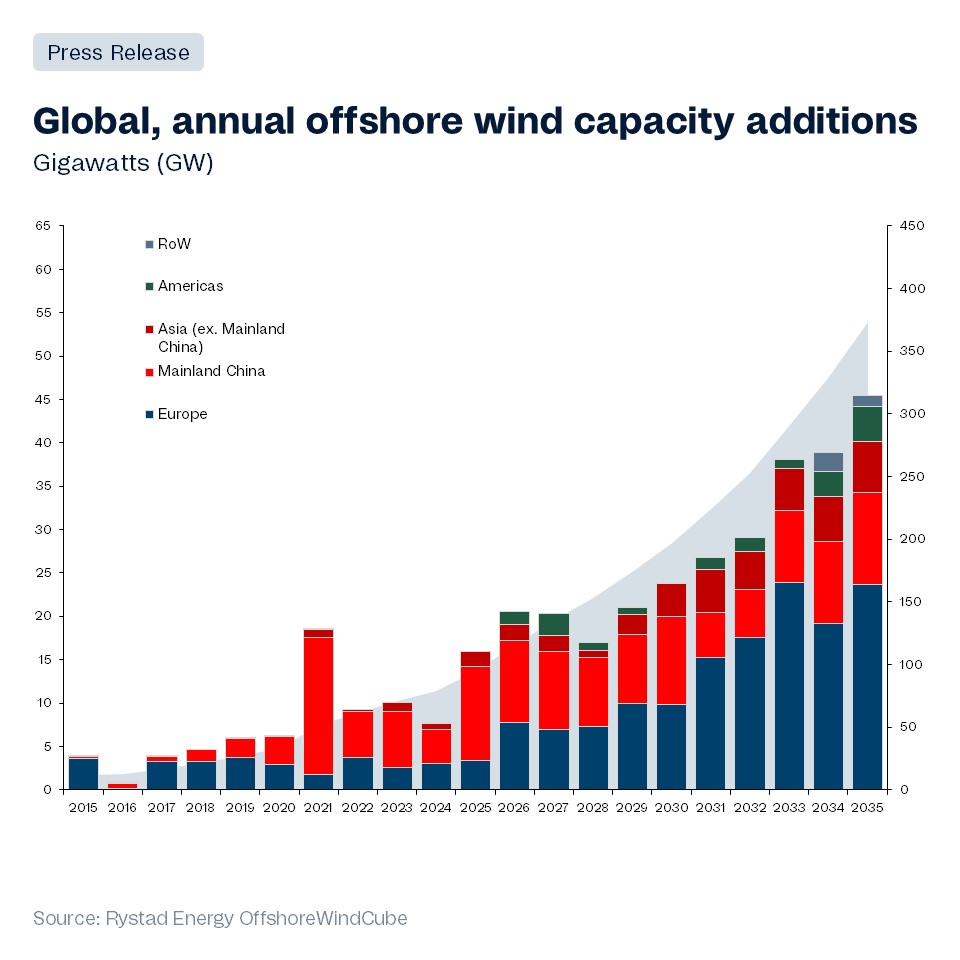

China’s Offshore Wind Dominance to Continue

This chart visualizes the “insurmountable” industrial scale by showing China’s projected annual capacity additions consistently dwarfing all other global regions through 2035.

(Source: Rystad Energy)

Policy Mandates Drive Unprecedented Market Expansion and Investment

China’s market expansion is not speculative but is underwritten by firm, long-term government policy, which de-risks capital investment in manufacturing and project development. These clear demand signals provide Chinese companies with the stability needed to invest in next-generation technology and massive production facilities, a stark contrast to the policy uncertainty seen in other global markets.

China’s Offshore Wind Installations to Dwarf Rivals

The chart shows China’s projected installations reaching 20,000 MW annually, directly visualizing the massive market expansion underwritten by the government policy mandates described in the section.

(Source: EnkiAI)

- The country’s upcoming 15 th Five-Year Plan (2026-2030) sets a clear and aggressive target to add at least 120 GW of new wind power capacity annually. This long-term mandate creates a predictable, high-volume domestic market that justifies massive investment in the supply chain.

- Within this goal, the offshore wind segment is specifically targeted for major growth, with the plan mandating the addition of at least 15 GW of new offshore capacity each year from 2026 to 2030. This provides a stable demand floor for leading OEMs like Goldwind, Envision, and Mingyang Smart Energy.

- This state-directed growth is reflected in market forecasts. China’s total wind energy capacity is projected to reach 640 GW in 2025 and grow at a CAGR of 13.40% to hit 1, 200 GW by 2030, cementing its role as the primary engine of global wind market expansion.

Table: China’s Wind Energy Growth Projections and Policy Targets

| Metric / Policy | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| 15 th Five-Year Plan (Total Wind) | 2026 – 2030 | Mandates adding at least 120 GW of wind capacity annually, creating massive, predictable domestic demand for the entire supply chain. | The Maritime Executive |

| 15 th Five-Year Plan (Offshore) | 2026 – 2030 | Specifies adding a minimum of 15 GW of new offshore wind capacity each year, ensuring a stable, high-volume market for specialized marine technology and vessels. | The Maritime Executive |

| Total Wind Capacity Projection | 2025 – 2030 | Market forecast projects total capacity will grow from 640 GW in 2025 to 1, 200 GW by 2030, reflecting a 13.4% CAGR. | Mordor Intelligence |

Geographic Concentration Creates a Fortress Market

China’s offshore wind growth is intensely concentrated within its own coastal provinces, creating a “fortress market” that is almost entirely supplied by domestic champions. This hyper-localization provides a formidable barrier to entry for foreign competitors and serves as a large-scale, protected incubator for developing and refining new technologies before they are introduced to the global market.

Chart Reveals China’s ‘Fortress’ Wind Market

This chart perfectly matches the section’s theme by showing that Chinese OEMs’ business is almost entirely domestic, which visually defines the “fortress market” concept.

(Source: Wood Mackenzie)

China’s Wind Capacity and Cost Trends

As this section presents a table of policy targets, this chart provides a visual summary, illustrating the massive capacity growth in coastal provinces and declining energy costs that result from them.

(Source: EnkiAI)

- Between 2021 and 2024, development was heavily focused along the coasts of provinces like Guangdong, Jiangsu, and Fujian. Mega-projects like the 1.0 GW Qingzhou Offshore Wind Farm and the 1.7 GW Yangjiang Shapa project became operational, solidifying these regions as hubs for large-scale deployment.

- This domestic concentration intensified in 2025, with provincial-level ambitions driving further growth. Shanghai, for example, announced plans to install 29.3 GW of offshore wind capacity, a pipeline that will be captured almost exclusively by Chinese OEMs and their supply chains.

- The result is a market where over 98% of connections for Chinese OEMs are within China. This extreme domestic focus, projected to continue through 2034, allows companies like Ming Yang and Goldwind to achieve massive economies of scale and operational expertise without facing direct international competition on their home turf.

Technology Maturity: China’s Leap to 26 MW Turbines Widens Global Gap

By 2025, China transitioned from a technology follower to a definitive leader, particularly in the race to develop ultra-large-capacity offshore wind turbines. This technological leapfrog has created a significant capabilities gap with Western competitors, enabling China to drive down its Levelized Cost of Energy (LCOE) and establish new global benchmarks for turbine power ratings.

- In the 2021-2024 period, the technology race was escalating. While Western OEMs like Vestas were commercializing their 15 MW platform, Chinese firms like Mingyang Smart Energy announced plans for a 22 MW turbine, signaling a clear ambition to surpass existing technology.

- This ambition became reality between 2024 and 2025. In late 2024, Dongfang Electric announced it was developing a 26 MW offshore turbine. By early 2026, details emerged that this turbine featured immense 153-meter blades, dwarfing the 115.5-meter blades of the Vestas 15 MW model being installed in Europe during 2025.

- This divergence is not just theoretical. In March 2025, components for Chinese 14 MW turbines were already being transported to project sites, demonstrating that the country was deploying turbines at a scale that Western firms were still in the process of commercializing. This rapid progression from R&D to deployment validates China’s technological supremacy.

SWOT Analysis: China’s Offshore Wind Sector

China’s offshore wind industry has solidified its strengths in manufacturing scale and policy support, creating opportunities for global supply chain dominance. However, its intense domestic focus and the potential for geopolitical friction present clear threats to its international expansion plans. The critical shift between the two periods has been the validation of its technological leadership and cost-competitiveness.

Western OEMs Dominate Market Outside China

This chart illustrates the “domestic focus” weakness and “geopolitical friction” threat mentioned in the SWOT analysis by showing how the global market is bifurcated, with Western firms dominant only when China is excluded.

(Source: Wood Mackenzie)

Table: SWOT Analysis for China’s Offshore Wind Industry (2021-2025)

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Growing manufacturing capacity, strong government subsidies, and rapid installation pace. | Unmatched industrial scale (e.g., Goldwind‘s 25.9 GW in 2025), proven low LCOE ($66/MWh), and demonstrated technological leadership with 26 MW turbines. | The strength shifted from simply having scale to proving that this scale delivers superior technology at a lower cost than global competitors. |

| Weaknesses | Heavy reliance on domestic market, questions over technology parity with Western OEMs. | Continued hyper-localization (>98% domestic focus) could be a vulnerability if local demand slows. Geopolitical tensions create barriers to export in key Western markets. | The technology parity question was resolved; China is now leading. However, the reliance on the domestic market is now a more pronounced strategic risk for global expansion plans. |

| Opportunities | Export to emerging markets, potential to lower global offshore wind costs. | Dominate global supply chains for critical components. Leverage superior technology (20+ MW turbines) to win contracts in Southeast Asia, Latin America, and the Middle East. | The opportunity evolved from simply exporting turbines to setting the global technology standard and controlling the underlying value chain for next-generation projects. |

| Threats | Potential for subsidy cuts to slow domestic growth, competition from established Western OEMs. | Increased trade barriers and tariffs from Europe and North America. Potential for domestic policy to shift priorities after 2030. Supply chain bottlenecks for ultra-large components. | The primary threat is now external and geopolitical rather than internal or competitive. Western policy, not Western technology, is the main obstacle to China’s global dominance. |

Scenario Modeling: China’s Export Offensive in 2026

In 2026, expect Chinese offshore wind OEMs to launch a concerted export offensive, leveraging their proven cost and technology advantages to capture market share in developing nations. The primary indicator to watch will be the first major international project to select a Chinese turbine with a rating of 20 MW or higher, as this will validate their global competitiveness and trigger a pricing reset in the industry.

Chinese Wind OEMs Rapidly Gain Global Orders

This chart directly supports the section’s scenario of a future “export offensive” by showing a massive recent surge in firm orders for Chinese OEMs in markets outside of China.

(Source: Wood Mackenzie)

Chinese OEMs Dominated 2023 Wind Market

This chart supports the “Strengths” component of the SWOT table by ranking global OEMs and showing Chinese firms like Goldwind in the lead, demonstrating the industrial scale driven by domestic demand.

(Source: Wood Mackenzie)

- If Chinese firms secure even one or two significant offshore wind contracts in regions like Southeast Asia or Latin America in 2026, watch for a rapid acceleration of their international activities. Their ability to offer a complete package of technology, financing, and EPC services at a low cost will be difficult for emerging markets to refuse.

- This could be happening: Western developers, facing their own supply chain constraints and cost pressures, may begin sourcing more critical sub-components (like gearboxes, generators, and castings) from Chinese suppliers, even for projects using Western turbines. This would further embed China at the center of the global value chain.

- The key signal of this shift losing steam would be the successful implementation of prohibitive trade barriers or local content requirements in major target markets outside of the US and Europe. A failure to break into markets beyond its immediate sphere of influence would indicate that geopolitical concerns are successfully containing China’s industrial might for now.

Frequently Asked Questions

How did China achieve such a dominant position in offshore wind manufacturing?

China’s dominance stems from its massive, protected domestic market, which allows its companies to achieve unparalleled industrial scale. For example, in 2025 alone, a single company, Goldwind, installed 25.9 GW of capacity in China, exceeding the total global additions for that year. This state-supported, high-volume environment de-risks investment and creates insurmountable competitive barriers for international rivals.

What is the significance of the 26 MW turbine mentioned in the article?

The development of a 26 MW turbine by Dongfang Electric by 2026 signifies a major technological leap, establishing China as a definitive leader, not just a follower, in offshore wind technology. With immense 153-meter blades, it dwarfs the 15 MW models being installed by Western competitors, demonstrating China’s ability to create a significant capabilities gap and set new global benchmarks for power and efficiency.

How does Chinese government policy support this rapid growth?

The Chinese government provides firm, long-term policy mandates that create a stable and predictable high-volume market. The upcoming 15th Five-Year Plan (2026-2030), for instance, mandates adding at least 120 GW of wind power annually, with a specific target of at least 15 GW of new offshore capacity each year. This clear demand signal underwrites massive investment in the supply chain.

Are Chinese wind turbines primarily used within China?

Yes, currently the market is extremely localized. The article states that over 98% of connections for major Chinese OEMs like Goldwind and Ming Yang are within China, creating a ‘fortress market.’ However, the analysis projects a significant export offensive beginning in 2026, where these companies will leverage their cost and technology advantages to enter markets in Southeast Asia, Latin America, and the Middle East.

What is the biggest threat to China’s global expansion in the offshore wind market?

According to the SWOT analysis, the primary threat is no longer competition from Western technology but is instead external and geopolitical. The biggest risk is the implementation of increased trade barriers, tariffs, and local content requirements by Europe, North America, and other potential export markets, which could contain China’s industrial expansion despite its technological and cost superiority.