Hydrogen Market 2026: Why Corporate Strategies Are Splitting as Billions Are Invested

Hydrogen Adoption in 2026: A Market of Contradictory Signals

The hydrogen market in 2025-2026 is defined by a clear divergence between aggressive, large-scale project commitments and strategic withdrawals by major industrial players. While market forecasts project exponential growth and substantial capital is being deployed, execution hurdles and uncertain demand are causing some companies to halt development, creating a fragmented adoption landscape.

- The period from 2021 to 2024 was characterized by broad optimism and strategic planning, with countries like Spain setting ambitious targets for 4 GW of electrolyzer capacity by 2030. In contrast, 2025 has brought both landmark project initiations and significant cancellations. For example, in November 2025, OMV and Masdar signed a binding agreement for a new 140 MW green hydrogen plant in Austria, demonstrating commitment to scale.

- This forward momentum is contrasted by strategic pivots. On July 16, 2025, automotive giant Stellantis announced the discontinuation of its hydrogen fuel cell technology program, citing a lack of mid-term market prospects. This move shows that despite the overall market growth, the business case for certain applications remains unproven for some major corporations.

- Market forecasts remain extremely strong, with Fortune Business Insights projecting the green hydrogen market to grow from $1.92 billion in 2025 to over $14.48 billion by 2032. This long-term optimism fuels continued activity, such as HNO International’s March 2026 offtake agreement to supply hydrogen for a fleet of fuel cell electric trucks.

- The application landscape is broadening beyond traditional industrial uses. In June 2025, HNO International announced a project to convert toxic fracking water into clean hydrogen, while IFF pioneered an on-site green hydrogen facility in Spain for manufacturing fragrance ingredients in November 2025. This diversification indicates new revenue streams but also increases the complexity of infrastructure and business models.

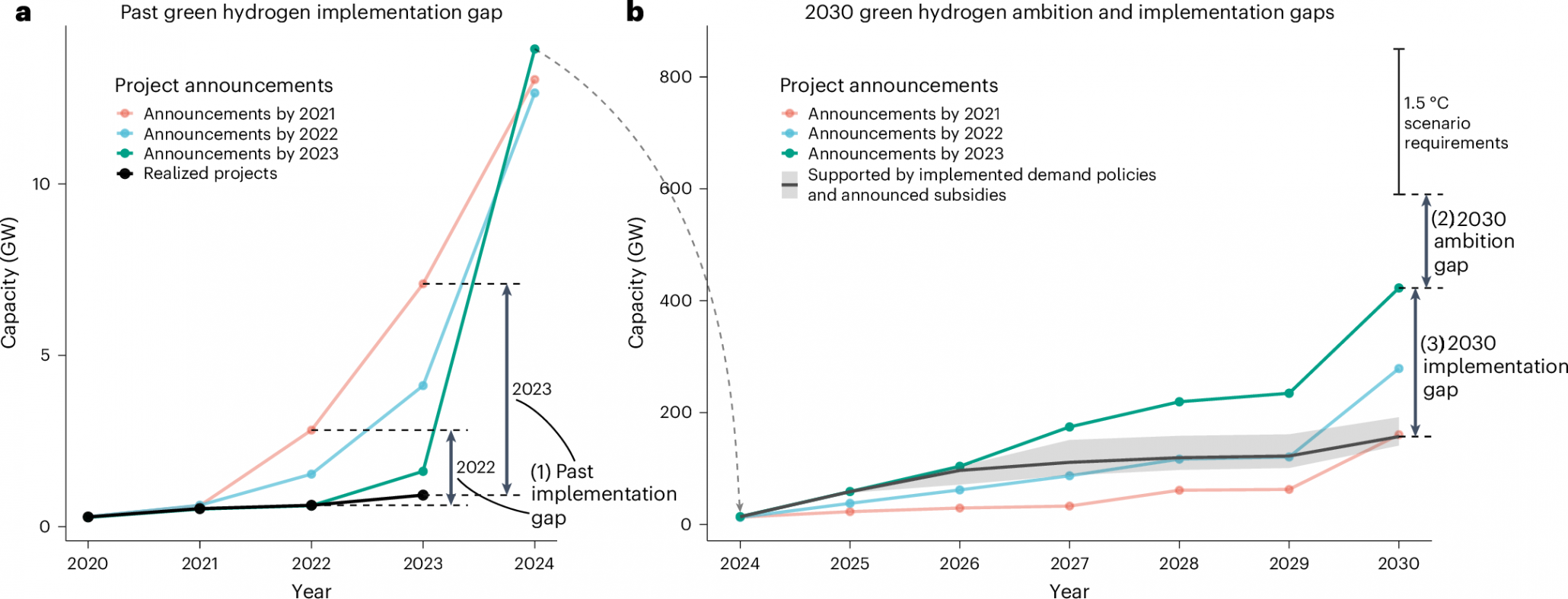

Hydrogen’s Ambition vs. Reality Gap

This chart’s depiction of the widening “implementation gap” perfectly visualizes the section’s theme of “contradictory signals” and the divergence between project commitments and actual execution.

(Source: Nature)

Hydrogen Investment 2025: Tracking Capital Flows Amidst Uncertainty

Financial activity in the hydrogen sector reflects the market’s duality, with a mix of strong fundraising for specific projects and signs of budget tightening. While venture and public funding continues to flow into promising technologies and early-stage projects, some established players are recalibrating their investment scale, signaling a more cautious approach to capital expenditure as projects move from planning to execution.

Capital Fuels Explosive Market Growth

This chart quantifies the “strong fundraising” and “capital flows” described in the text. It projects explosive market growth, validating the bullish side of the investment activity mentioned in the section.

(Source: Insightace Analytic)

- Public funding remains a critical enabler. In August 2025, New York State awarded over $11 million to five clean hydrogen R&D projects, including a $2 million grant to National Grid Ventures. Similarly, UK-based policy like the Hydrogen Production Business Model provides crucial revenue support to bridge the cost gap for producers.

- Private capital is still accessible for companies with clear growth paths. In November 2025, Next Hydrogen closed a $20.7 million equity private placement to fund its operations, and UK Oil & Gas (UKOG) raised £520, 000 for its hydrogen initiatives through a share placement.

- However, there are indicators of financial discipline and recalibration. In March 2025, HDF Energy reported a reduction in its total project investment budget from $3.2 billion to $3 billion. This decrease, attributed to a smaller average project size, suggests a potential market adjustment toward more manageable, de-risked deployments.

Table: Key Hydrogen Sector Financial Activities (2025)

| Company / Entity | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| UK Oil & Gas (UKOG) | November 20, 2025 | Raised £520, 000 via a share placement to provide additional funding for its UKEn Hydrogen projects, indicating investor appetite for early-stage regional developments. | London Stock Exchange |

| Next Hydrogen | November 14, 2025 | Closed a $20.7 million equity private placement to fund its operations and growth in green hydrogen technology, demonstrating continued venture confidence. | Next Hydrogen |

| New York State (NYSERDA) | August 21, 2025 | Awarded over $11 million to five clean hydrogen R&D projects to accelerate innovation, with $2 million going to National Grid Ventures for a generator project. | NYSERDA |

| HDF Energy | March 20, 2025 | Reduced its total investment budget for projects from $3.2 billion to $3 billion, reflecting a shift in project scope and a more cautious capital deployment strategy. | HDF Energy |

| Stellantis | July 16, 2025 | Discontinued its hydrogen fuel cell technology development program, a major cancellation signaling a strategic retreat from the technology due to perceived lack of near-term viability. | Stellantis |

Hydrogen Partnerships in 2025: Alliances Target Scale and Technology

Strategic partnerships formed in 2025-2026 are focused on de-risking capital-intensive projects and accelerating technology development to overcome market barriers. These collaborations range from international supply chain development to joint efforts between industrial giants to advance low-emission production technologies, underscoring that no single entity can build out the hydrogen ecosystem alone.

- During the 2021-2024 period, partnerships like the one between Nel ASA and General Motors focused on foundational R&D to lower electrolyzer costs. The new wave of partnerships in 2025-2026 is geared toward commercial deployment and creating integrated value chains.

- In November 2025, chemical leader BASF and energy major Exxon Mobil joined forces to advance low-emission hydrogen technologies. This alliance combines BASF’s process innovation with Exxon Mobil’s industrial scale to accelerate technological progress.

- Also in November 2025, OMV and Masdar signed a binding joint development agreement for a 140 MW green hydrogen plant. This collaboration leverages OMV’s regional footprint and Masdar’s ambition to be a global green hydrogen leader.

- International cooperation is solidifying supply routes. In early 2026, the establishment of the Japan-New Zealand Hydrogen Corridor was announced. The initiative aims to commercialize green hydrogen production in New Zealand for export to Japan, creating a tangible international supply chain.

Table: Key Hydrogen Market Partnerships (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Japan-New Zealand Hydrogen Corridor | March 5, 2026 | Initiated a study to establish a commercial-scale hydrogen corridor, aiming to produce green hydrogen in New Zealand for export and use in Japan. | Obayashi Corporation |

| BASF & Exxon Mobil | November 17, 2025 | A technology collaboration to combine industrial and technological expertise, with the goal of accelerating the development of low-emission hydrogen production methods. | BASF |

| OMV & Masdar | November 6, 2025 | A binding agreement to jointly develop and operate a new 140 MW green hydrogen plant in Austria, supporting Masdar’s goal of becoming a leading global producer. | OMV |

Global Hydrogen Hotspots: Where Capital and Policy Converge

Geographic activity in the hydrogen sector is concentrating in regions with strong policy support, established industrial demand, and clear decarbonization mandates. While the 2021-2024 period saw widespread national strategy announcements, 2025-2026 activity shows Europe and parts of North America emerging as first-mover hubs where projects are moving from plans to physical development.

National Ambitions Define Hydrogen Hotspots

This chart illustrates the “Global Hotspots” theme by comparing the gigawatt-scale hydrogen ambitions of various nations. It provides a visual for the national strategies that create the hubs mentioned in the section.

(Source: Center on Global Energy Policy – Columbia University)

- Europe is a clear leader, driven by initiatives like the EU Hydrogen Bank. The OMV and Masdar 140 MW plant in Austria and IFF’s on-site green hydrogen facility in Spain are concrete examples of this regional momentum, building on Spain’s earlier plan to invest $9.6 billion in hydrogen infrastructure.

- North America is showing targeted growth, particularly in Canada and select US states. In November 2025, Max Power began drilling Canada’s first natural hydrogen well in Saskatchewan. In Quebec, First Hydrogen is developing a 35 MW green hydrogen production facility.

- In the United States, state-level initiatives are critical. The $11 million in R&D grants awarded by New York State in August 2025 highlights a strategy of fostering regional innovation hubs to drive technological advancement and local supply chains.

- Asia-Pacific is focusing on building international supply chains. The Japan-New Zealand Hydrogen Corridor announced in 2026 and Marubeni’s November 2025 completion of a demonstration project between Australia and Indonesia illustrate a strategic focus on securing long-term energy supply through hydrogen trade.

Hydrogen Technology 2026: From Pilot to Commercial Reality

The hydrogen sector is progressing from R&D toward commercial-scale technological validation, but maturity varies significantly across the value chain. While foundational production technologies are advancing, significant challenges remain in cost reduction, standardization, and developing viable business cases for end-use applications, as evidenced by the mix of project launches and cancellations.

Hydrogen’s Technological and Cost Hurdles

This infographic directly relates to the section by detailing production methods and key barriers like high cost and capital expenditure. This echoes the text’s focus on technological challenges and cost reduction.

(Source: ScienceDirect.com)

- The 2021-2024 period focused on improving core technologies, with efforts like Hydrofuel’s acquisition of patented ammonia-release technology. In 2025-2026, the focus has shifted to proving these technologies at scale. The successful operation of IFF’s on-site production facility for industrial use is a key validation point. The importance of logistics is also growing, with many of the top green ammonia projects designed to solve transportation bottlenecks.

- Standardization is becoming critical for market expansion. The ballot for ISO 13985, a standard for liquid hydrogen vehicle fuel storage systems, closing in November 2025, is a crucial step toward ensuring safety and interoperability in the mobility sector, an area where lack of standards has previously hindered progress.

- Despite advances, technology risk remains a key factor in corporate strategy. Stellantis’s decision to exit the fuel cell sector in July 2025 highlights that for some applications, particularly passenger vehicles, the technology has not matured sufficiently to present a compelling business case against alternatives like battery electric vehicles.

- New, potentially disruptive technologies are emerging from the exploration phase. The drilling of Canada’s first natural hydrogen well by Max Power in November 2025 represents a first-mover effort into a sector that could offer a low-cost alternative to manufactured hydrogen if proven commercially viable.

Hydrogen Market SWOT Analysis: Growth vs. Volatility

The hydrogen market is at a pivotal juncture where immense growth opportunities are tempered by significant weaknesses and external threats. The primary strategic challenge is navigating the gap between long-term potential, driven by decarbonization goals, and the near-term realities of high costs, uncertain demand, and divergent corporate strategies.

Scenarios Reveal Market’s Wide Uncertainty

The chart’s presentation of multiple production scenarios, from minimal to high-growth, perfectly visualizes the “Growth vs. Volatility” tension described in the SWOT analysis.

(Source: Natural Resources Canada – Canada.ca)

- Strengths are rooted in strong market growth projections and significant public and private investment, validated by major partnerships between industrial leaders.

- Weaknesses are internal to the market, primarily the high cost of low-carbon hydrogen compared to conventional alternatives and the persistent infrastructure gaps that hinder widespread adoption.

- Opportunities are expanding beyond traditional sectors into new applications and geographies, driven by global decarbonization mandates.

- Threats are largely external and strategic, including the risk of market fragmentation as major players adopt opposing strategies and the market’s continued reliance on government subsidies to remain viable.

Table: SWOT Analysis for the Global Hydrogen Market

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | High-level government strategy announcements (e.g., Spain’s 4 GW target). General market optimism and R&D partnerships (Nel/GM). | Binding agreements for large-scale projects (OMV/Masdar 140 MW plant). Major industrial partnerships (BASF/Exxon Mobil). Strong market growth forecast (33.46% CAGR). | The market has moved from strategic intent to concrete, large-scale commercial commitments and collaborations between major industrial players. |

| Weaknesses | Acknowledged high cost of green hydrogen and lack of infrastructure. Focus on R&D to solve cost issues. | The cost gap remains a primary barrier, requiring revenue support models (UK’s HPBM). Technology immaturity in certain sectors leads to major cancellations (Stellantis). | The cost problem has not been resolved, forcing a reliance on subsidies. Technology risk is now tangible, causing major players to exit specific segments. |

| Opportunities | Focus on decarbonizing hard-to-abate sectors like heavy industry and transport. | New applications emerge (IFF fragrances, HNO’s fracking water). New resource exploration begins (Max Power’s natural hydrogen). International supply chains solidify (Japan-NZ corridor). | The scope of opportunity has widened beyond traditional use cases, including novel feedstocks and entirely new geological sources for hydrogen. |

| Threats | General concerns about policy consistency and the long-term economic viability of projects. | Diverging corporate strategies create market uncertainty. Project budgets are being trimmed (HDF Energy). Market viability is heavily dependent on policy mechanisms like EU Hydrogen Bank auctions. | Strategic risk has become a primary threat. The market is fragmenting, and its financial health is visibly tied to ongoing government intervention. |

2026 Hydrogen Outlook: What to Watch as the Market Matures

The critical test for the hydrogen market in 2026 is whether revenue support mechanisms and technology cost-downs can align divergent corporate strategies, converting project announcements into operational assets. Success will depend on bridging the gap between bullish forecasts and the on-the-ground challenges of project execution and demand creation. The key is to watch for signals that confirm a convergence, not a further splintering, of market direction.

Gap Between Announced and Operational Projects

This chart directly supports the 2026 outlook by showing that most announced projects remain in early stages. It highlights the critical challenge of converting announcements into operational assets, a key theme of the section.

(Source: Nature)

- Watch corporate financials closely. The Q 3 2025 results from leading players like Plug Power will provide a direct indicator of commercial health and investor confidence. Strong revenues would signal that demand is materializing, while weak performance could validate the caution shown by players like Stellantis.

- Monitor the effectiveness of policy mechanisms. The scale and success of the EU Hydrogen Bank auctions will be a critical measure of the market’s ability to scale. An increase in the auction budget and frequency would be a strong positive signal, confirming government commitment to bridging the viability gap for producers.

- Track the finalization of technical standards. The progression of standards like ISO 13985 for liquid hydrogen fuel systems is a vital, albeit less visible, signal of market maturity. The adoption of clear, international standards is essential for ensuring safety, interoperability, and reducing risk for infrastructure investors.

Frequently Asked Questions

Why are corporate strategies in the hydrogen market described as ‘splitting’?

Strategies are splitting because while some companies, like OMV and Masdar, are committing to new, large-scale projects (e.g., a 140 MW plant in Austria), other major players, like Stellantis, are discontinuing their hydrogen programs due to a perceived lack of near-term market viability. This creates a contrast between aggressive investment and strategic withdrawal.

What are the main challenges currently holding back the hydrogen market?

The primary challenges identified are the high cost of low-carbon hydrogen compared to conventional alternatives, which makes projects dependent on government subsidies (like the UK’s HPBM), and persistent infrastructure gaps. Furthermore, technology immaturity in certain sectors and a lack of finalized technical standards create risk and hinder widespread adoption.

Is the hydrogen market actually growing despite some companies pulling back?

Yes, the overall market is projected to grow significantly. Fortune Business Insights forecasts the green hydrogen market will expand from $1.92 billion in 2025 to over $14.48 billion by 2032. The ‘pullback’ from certain companies reflects a fragmentation of the market and caution in specific applications, rather than an overall market decline.

Where are the global hotspots for hydrogen development activity?

Europe is a leading hotspot, driven by policy and concrete projects in Austria and Spain. North America shows targeted growth, with state-level R&D funding in New York and new production and exploration projects in Canada (Quebec and Saskatchewan). The Asia-Pacific region is focused on creating international supply chains, highlighted by the Japan-New Zealand Hydrogen Corridor.

Why are partnerships like the one between BASF and Exxon Mobil important?

Partnerships are crucial for de-risking capital-intensive projects and combining different areas of expertise to accelerate technological progress. The report notes that no single company can build the entire hydrogen ecosystem alone. Alliances like BASF and Exxon Mobil bring together process innovation and industrial scale, while others like the OMV-Masdar agreement leverage regional footprints and global production ambitions.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.