Offshore Wind’s 2026 Bottleneck: Why Next-Gen Installation Vessels Are Failing to Keep Pace

Offshore Wind Installation Risk: The Growing Mismatch Between Turbine Size and Vessel Capacity

The offshore wind industry’s rapid scaling of turbine technology has created a critical supply chain bottleneck in the availability of specialized Wind Turbine Installation Vessels (WTIVs), a risk that shifted from a future concern between 2021-2024 to an acute commercial reality in 2025. While turbine manufacturers have accelerated the development of 15-25 MW models, the global fleet of vessels capable of lifting and installing these massive structures has not kept pace, threatening project timelines and inflating costs. This mismatch forces developers to compete for a limited pool of high-specification assets, making vessel availability a primary constraint on sector growth.

- Between 2021 and 2024, the industry responded to future turbine growth by placing a wave of orders for next-generation WTIVs. Major contractors like Cadeler, Havfram, and Seaway 7 committed to newbuilds based on advanced designs, such as NOV‘s Gusto MSC NG-20000 X, and equipped them with heavy-lift cranes with capacities from 2, 500 to over 3, 000 tonnes. This period was defined by strategic procurement to prepare for future installation requirements.

- The market dynamic shifted in 2025, as the vessel shortage became an immediate operational challenge. The landmark contract secured by NOV on December 15, 2025, with South Korean shipbuilder Hanwha Ocean for another Gusto MSC™ NG-16000 X WTIV demonstrates that demand continues to outstrip supply. Concurrently, developers like Ørsted faced significant project disruptions, including a stop-work order for its Revolution Wind project in August 2025, highlighting how supply chain fragility can directly impact project execution.

- The vessel scarcity is intensified by the dual-use requirement for these high-specification assets. They are needed not only for installing turbines but also for handling the increasingly large monopile foundations. Projects like Cadeler‘s F-Class foundation installation vessel, based on NOV‘s Gusto MSC NG-16000 X design, are specifically built for this purpose, which further segments and strains the already limited fleet of advanced offshore construction vessels.

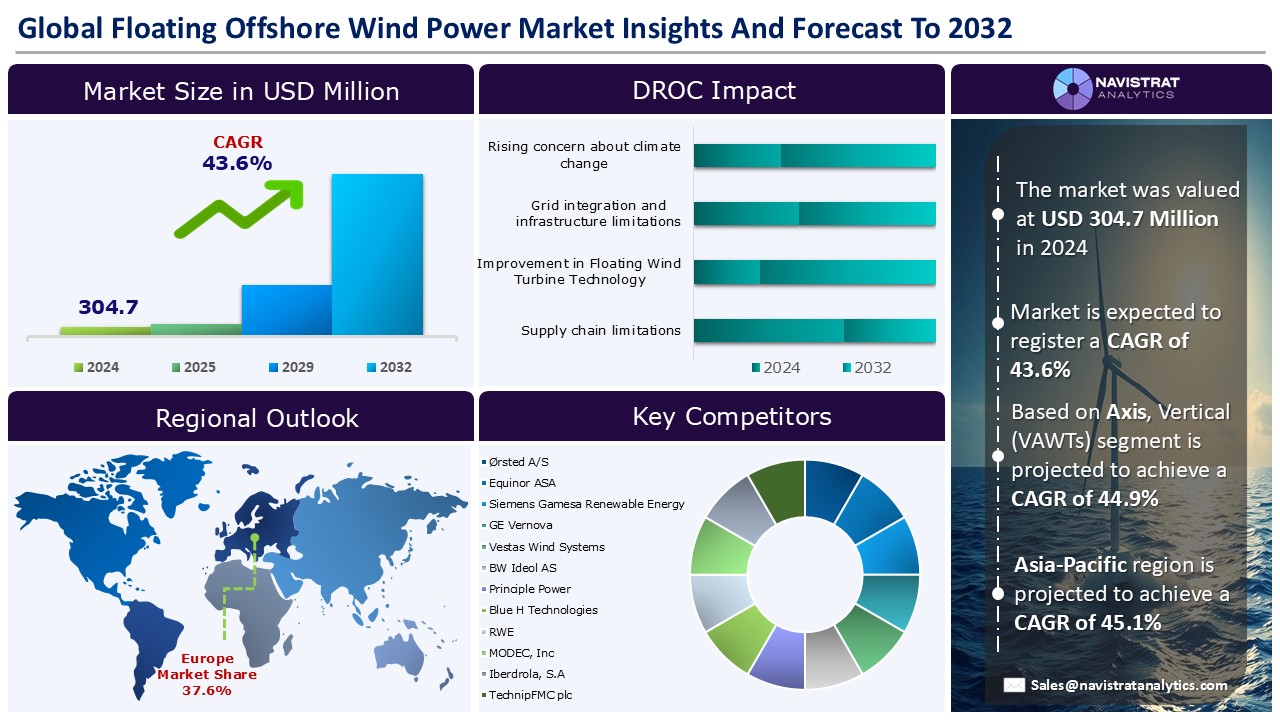

Floating Wind Growth Hinges on Supply Chain

This chart directly supports the section’s theme of a supply chain bottleneck by explicitly identifying ‘Supply chain limitations’ as a key factor impacting the market’s explosive growth.

(Source: Navistrat Analytics)

Strategic Alliances in Offshore Wind: Partnerships Form to Overcome Vessel Scarcity

In response to the installation vessel bottleneck, a network of strategic partnerships has solidified, connecting technology designers, shipbuilders, installation contractors, and even energy majors to secure access to next-generation capacity and develop enabling technologies. These alliances are no longer just transactional; they represent a coordinated effort to de-risk the supply chain by locking in critical hardware and co-developing solutions for both current fixed-bottom and future floating wind projects.

- During the 2021-2024 period, foundational partnerships formed between technology providers and contractors. NOV‘s Gusto MSC subsidiary established itself as the core designer in alliances with contractors like Cadeler and Havfram, and shipyards such as Keppel O&M (now Seatrium), to bring the NG-20000 X and NG-16000 X vessel designs from blueprint to reality.

- In 2025, these partnerships evolved to address both immediate and future needs. The contract between NOV and Hanwha Ocean extended the existing ecosystem of builders for its market-leading designs. Simultaneously, NOV’s pre-commercial agreement with Petrobras in March 2025 to develop high CO₂ resistant flexible pipes for deepwater Carbon Capture, Utilization, and Storage (CCUS) showcases a forward-looking strategy. This collaboration advances materials science with dual-use potential for the dynamic cables required by floating wind, a field where the high energy cost of DAC remains a critical factor.

- The focus on installation solutions is an industry-wide phenomenon. A November 2025 agreement saw developer Luxcara select Ørsted as a preferred supplier for its low-noise monopile installation technology. This move by a major developer to secure specific installation tooling underscores the intense focus on optimizing every aspect of the offshore construction process to mitigate delays and cost overruns.

Table: Offshore Wind Supply Chain Partnerships (2021-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| NOV (SPS Unit) & Petrobras | March 2025 | Pre-commercial agreement to co-develop flexible pipes for high CO₂ deepwater use, with applications in CCUS and floating wind. | Offshore Energy |

| Oersted & Trelleborg & NOV | September 2023 | Technology collaboration to develop and test a standardized dynamic power cable and subsea connection for floating wind farms. | NOV |

| GE Renewable Energy & NOV | May 2022 | Framework agreement to optimize NOV‘s Tri-Floater substructure for GE‘s Haliade-X turbines, targeting serial production for floating wind. | Offshore Wind.biz |

| Sembcorp Marine (Seatrium) & Gusto MSC (NOV) | March 2021 | Design collaboration for a next-generation WTIV capable of handling 20 MW turbines and operating on zero-emission fuels. | Gusto MSC |

Geographic Hotspots: Where the Race for Offshore Wind Installation Capacity is Centered

While offshore wind farm development is a global ambition, the design, manufacturing, and control of the critical installation vessel supply chain are highly concentrated, creating significant geopolitical and logistical dependencies. The ecosystem is primarily split between European design and contracting leadership and Asian shipbuilding dominance, leaving markets like the United States in a structurally vulnerable position as they attempt to build out their domestic project pipelines.

Europe Leads Surge in Offshore Wind Investment

The chart validates the section’s point on geographic hotspots by showing that Europe, particularly Poland and Germany, is leading the strong rebound in final investment decisions.

(Source: Offshore Engineer)

- European Design & Contracting Hub: Europe is the undisputed center for high-specification vessel design and operations management. NOV‘s Gusto MSC, based in the Netherlands, is the market’s dominant designer. The key installation contractors who commission, own, and operate these vessels, such as Cadeler (Denmark), Havfram (Norway), and Seaway 7 (Norway), are also headquartered in the region.

- Asian Shipbuilding Dominance: The physical construction of these complex vessels is concentrated in Asian shipyards. The data shows major contracts awarded to South Korea’s Hanwha Ocean and Singapore’s Keppel O&M (now Seatrium), as well as China’s COSCO. These yards possess the heavy industrial capacity and specialized expertise required for such newbuilds, making them indispensable to the global fleet’s expansion. This concentration exposes the supply chain to regional risks, a vulnerability highlighted by analyses of how geopolitical conflict can trigger a shock to the global energy transition.

- The U.S. Jones Act Dilemma: The United States market faces a unique and severe vessel shortage due to the Jones Act, which mandates that goods transported between U.S. ports be carried on U.S.-flagged, U.S.-built, and U.S.-crewed ships. The first-of-its-kind WTIV, Dominion Energy‘s *Charybdis*, is based on a Gusto MSC design but its status as the sole Jones Act-compliant newbuild highlights the critical domestic bottleneck. The U.S. offshore wind industry’s growth is therefore directly dependent on the timely delivery and performance of this single asset, and its ability to secure additional, costly Jones Act vessels in the future.

Technology Readiness: Next-Gen WTIVs Move from Design to Deployment

The core technology for next-generation installation vessels has reached commercial maturity, with leading designs having moved from blueprint to steel between 2021 and 2025. The primary barrier to alleviating the market bottleneck is no longer a question of technological feasibility but rather the industrial capacity and time required for scaled production. The focus has now shifted from design validation to construction, delivery, and operational efficiency as the first of these advanced vessels enter the global fleet.

- From 2021 to 2024, the industry focused on validating and contracting new vessel designs. NOV‘s Gusto MSC launched its NG-20000 X and NG-16000 X designs, which were quickly adopted by leading contractors. This period was about securing the technical capability on paper to handle future 20+ MW turbines, with key features including 3, 000+ tonne crane capacities and advanced jacking systems.

- The 2025 timeframe marks the beginning of the delivery and deployment phase. The first WTIVs based on these next-gen designs, ordered by companies like Cadeler and Havfram, are scheduled for delivery. The December 2025 contract with Hanwha Ocean for another NG-16000 X serves as commercial validation that these designs remain the industry standard. The technology is proven; the challenge is building the vessels fast enough to meet demand.

- While fixed-bottom installation technology matures, early-stage development for the next frontier is underway. NOV‘s partnership with GE Renewable Energy on the Tri-Floater foundation and its collaboration with Oersted on dynamic power cables represent R&D efforts to solve the unique installation and operational challenges of floating offshore wind, indicating the industry is already preparing for the subsequent technological shift.

SWOT Analysis: Strengths and Weaknesses in the Offshore Wind Vessel Supply Chain

The offshore wind installation market’s primary strength is its advanced and proven vessel technology, which is capable of handling the largest planned turbines. However, this strength is critically undermined by weaknesses in global manufacturing capacity and long construction lead times. This dynamic creates significant opportunities for integrated equipment suppliers but poses a systemic threat to the execution of global offshore wind deployment targets.

Massive Capacity Pipeline Creates Opportunity and Risk

This infographic illustrates the scale of the ‘Opportunity’ discussed in the SWOT analysis, as the massive pipeline (100 GW to be auctioned) puts pressure on the supply chain’s known weaknesses.

(Source: offshoreWIND.biz)

- Strengths: The market benefits from highly advanced, commercially validated WTIV designs and associated heavy-lift equipment.

- Weaknesses: Severe bottlenecks in specialized shipyard capacity and multi-year lead times for new vessel construction are the most significant constraints.

- Opportunities: The “picks and shovels” business model for equipment and design providers is highly profitable, while new markets like the U.S. under the Jones Act present high-margin opportunities.

- Threats: The high cost and limited availability of vessels contribute to developer project delays and cancellations, which in turn threatens the order books for new vessels.

Table: SWOT Analysis for the Offshore Wind Installation Vessel Market

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Designs for next-gen WTIVs (e.g., Gusto MSC NG-20000 X) were launched and validated through initial orders from contractors like Cadeler and Seaway 7. | The first of these next-gen vessels neared delivery. Designs were further validated with follow-on orders, such as NOV‘s contract with Hanwha Ocean in late 2025. | The technology moved from theoretical design to proven, in-demand commercial products. The integrated model of providing both design and critical equipment (cranes, jacking systems) was validated as a winning strategy. |

| Weaknesses | Long lead times for vessel construction were an accepted part of planning. The scarcity was a future, anticipated problem. | Vessel scarcity became an acute, present-day constraint, contributing to developer challenges like Ørsted‘s project stop-work order. The limited number of specialized shipyards became a clear bottleneck. | The weakness shifted from a manageable planning parameter to a critical path risk for the entire industry’s growth targets. |

| Opportunities | The “picks and shovels” strategy for suppliers like NOV was emerging, with a strong order book ($502 M in 2023) as evidence. Early R&D into floating wind (e.g., Tri-Floater) began. | The strategy was validated as developers faced financial pressure, making the de-risked supplier role more attractive. The NOV-Petrobras CCUS partnership opened a parallel, high-tech market with crossover potential. | The opportunity was confirmed and expanded. Suppliers captured value while developers absorbed risk. New adjacent market opportunities (CCUS) were solidified. |

| Threats | Competition from other equipment suppliers (e.g., Huisman supplying the crane for *Charybdis*) was present. The risk of project cancellations was a background concern. | Developer financial distress and project cancellations (e.g., issues facing Ørsted) became a tangible threat to the future demand pipeline for vessels. | The threat of a boom-bust cycle intensified. A mismatch between vessel supply and the final investment decisions on wind farm projects became the central market risk. |

2026 Outlook: Key Signals for the Offshore Wind Installation Market

For 2026, the single most critical factor to monitor is the real-world operational performance of the first wave of next-generation WTIVs as they are delivered to contractors like Cadeler and Havfram. Their success or failure in efficiently installing 15-20 MW turbines will directly influence vessel day rates, future investment decisions in the supply chain, and the bankability of offshore wind projects globally.

Offshore Wind Market to Double by 2030

This chart provides the financial context for the ‘2026 Outlook’ by projecting substantial market growth, which underscores the importance of the investment decisions and project bankability mentioned in the section.

(Source: The Business Research Company)

- If this happens, watch this: If the new Gusto MSC-designed vessels for Cadeler and Havfram demonstrate high operational uptime and meet installation efficiency targets throughout 2026, watch for a new wave of investment in both WTIVs and foundation installation vessels. This would signal confidence that the technology can keep pace with turbines, potentially stabilizing day rates as more supply is confirmed.

- Watch this critical signal: The operational debut and subsequent performance of Dominion Energy’s *Charybdis* is the paramount signal for the U.S. market. A successful year of operations on the Coastal Virginia Offshore Wind project would likely trigger serious consideration for additional Jones Act vessel orders, cementing a multi-billion dollar domestic market. Underperformance or extended downtime would send a chilling signal to investors and could stall the U.S. project pipeline.

- These could be happening: Monitor announcements for the first commercial-scale, non-pilot orders for floating wind-specific solutions. A contract for a serialized floating foundation like NOV‘s Tri-Floater or a dedicated vessel for floating wind installation would indicate that the industry’s investment focus is beginning to shift to the next major growth frontier beyond 2026.

Frequently Asked Questions

Why is there a bottleneck for offshore wind installation vessels starting in 2025?

The bottleneck exists because wind turbines have rapidly scaled up to 15-25 MW, but the global fleet of Wind Turbine Installation Vessels (WTIVs) has not kept pace. Most existing vessels lack the crane capacity and deck space to handle these massive new components, creating a supply-demand mismatch that became an acute operational problem in 2025.

Who are the key players in the next-generation vessel supply chain?

The supply chain is geographically specialized. European companies like NOV’s Gusto MSC (Netherlands) dominate vessel design, and contractors like Cadeler (Denmark) and Havfram (Norway) operate them. However, the physical construction is concentrated in Asian shipyards, such as Hanwha Ocean in South Korea and Seatrium in Singapore.

What is the ‘Jones Act Dilemma’ and how does it affect the U.S. market?

The Jones Act requires that vessels transporting goods between U.S. ports be U.S.-built and flagged. This creates a severe bottleneck for the U.S. offshore wind industry, as it can’t use the more widely available foreign-flagged installation vessels. The entire near-term project pipeline is heavily reliant on a single newbuild, Dominion Energy’s *Charybdis*, making the U.S. uniquely vulnerable to vessel shortages.

Is the technology for these new vessels the problem?

No, the technology for next-generation WTIVs is considered mature and commercially validated. Designs like the Gusto MSC NG-20000 X, capable of handling 20+ MW turbines, have been ordered and are under construction. The primary barrier is not technological feasibility but the limited global shipyard capacity and the long lead times (multi-year) required to build these highly specialized assets.

What is the most critical factor to watch in the offshore wind installation market for 2026?

The single most critical factor for 2026 is the real-world operational performance of the first wave of next-generation WTIVs as they are delivered to contractors. Their success or failure in efficiently installing large turbines will directly influence future investment, vessel day rates, and the financial viability of offshore wind projects globally. Specifically, the performance of the U.S. vessel *Charybdis* will be a decisive signal for the American market.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.