SMR Grid Bypass Strategy, Equinix 500 MW Oklo PPA, 3 Nuclear Pacts, and 11 Projects (2021 to 2026)

Data Center SMR Projects, Equinix 500 MW Deals Signal Grid Independence Strategy

The primary driver for Small Modular Reactor (SMR) adoption has decisively shifted from government-led research to strategic, large-scale procurement by data center operators seeking to bypass congested power grids. This move is a direct response to the explosive, non-negotiable energy demand of AI infrastructure, which requires 24/7 carbon-free power that intermittent renewables and strained regional grids cannot reliably supply. The market has pivoted from speculative pilots to bankable, multi-hundred-megawatt Power Purchase Agreements (PPAs) that establish data centers as the anchor customers for the next generation of nuclear energy.

- Between 2021 and 2024, market activity was defined by early-stage exploration and significant commercial risk, typified by the November 2023 cancellation of Nu Scale Power‘s Carbon Free Power Project (CFPP) due to a 53% cost increase to $89/MWh. During this period, tech giants like Amazon and Google initiated preliminary partnerships, but the projects remained largely developmental.

- From 2025 to 2026, the dynamic inverted as data center operators took control, with Equinix executing firm PPAs for over 500 MW with multiple advanced reactor developers. This model, where the data center provides the revenue certainty needed for project financing, directly solves the economic viability problem that plagued earlier SMR efforts and establishes a template for private-sector-led nuclear deployment.

- The strategy is increasingly focused on co-locating reactors directly at or near data center campuses, a key feature of the Equinix agreements and Amazon‘s plan to site SMRs near its facilities. This “behind-the-meter” approach is designed to circumvent grid interconnection queues that can last up to seven years, ensuring power availability aligns with data center construction timelines.

Data Center Value Chain and Power Demand

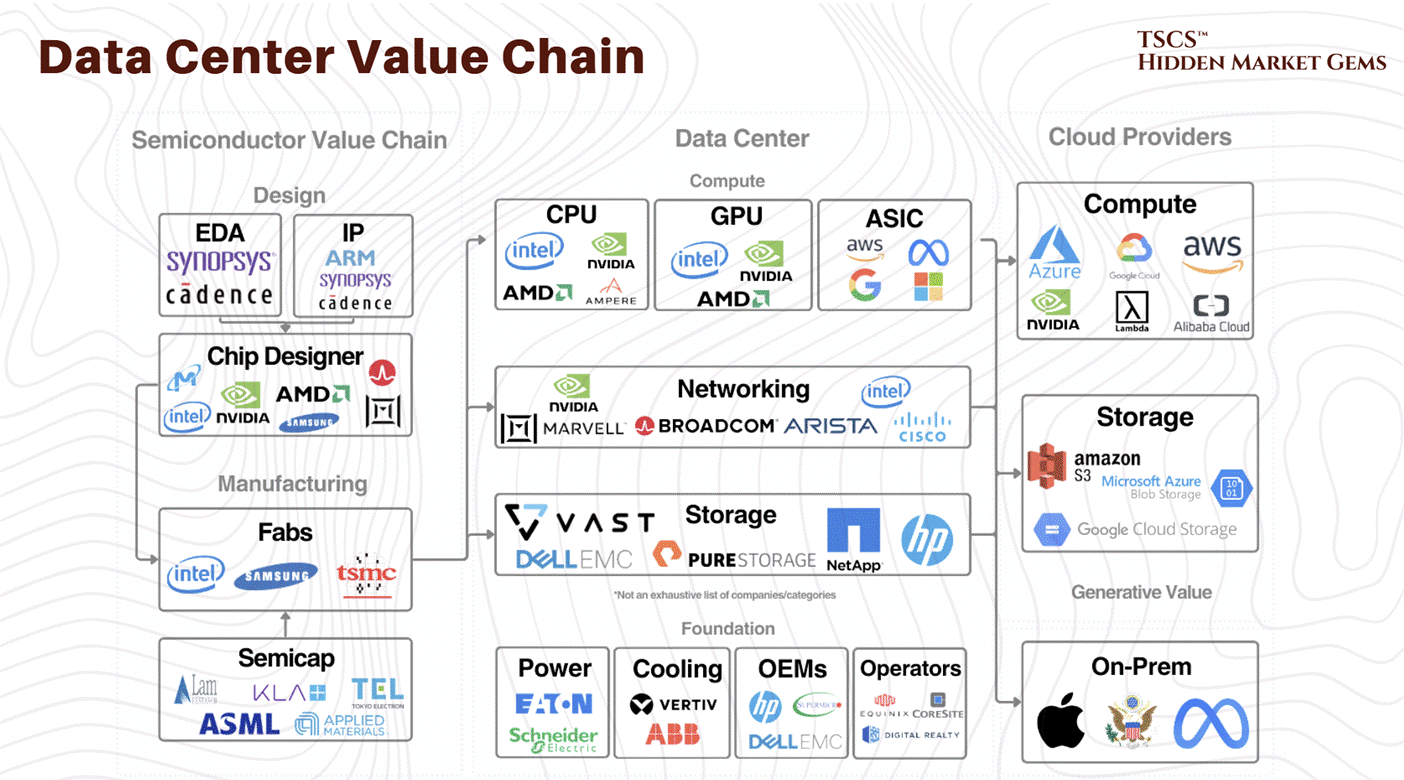

This chart maps the ecosystem, showing players like NVIDIA and Equinix, whose massive energy demands from AI are driving the shift to alternative power sources discussed in the section.

(Source: TSCS – Substack)

$10 B Market Shift, Equinix SMR Strategy Leverages Federal Funding

Corporate investment, structured as long-term PPAs, is now the dominant financial mechanism for launching first-of-a-kind (FOAK) advanced nuclear projects, with momentum amplified by significant U.S. federal incentives. This public-private financing model, where companies like Equinix provide the bankable offtake agreement and the government de-risks the investment through tax credits and funding, has created a viable path to commercialization for a capital-intensive industry.

- The U.S. Department of Energy has become a critical enabler, committing over $900 million through programs like the Generation III+ SMR Program to accelerate deployment. This includes $800 million for first-mover teams, creating a favorable regulatory and investment environment for projects involving Equinix‘s partners.

- The 2022 Inflation Reduction Act (IRA) fundamentally altered project economics by introducing technology-neutral tax credits. New advanced nuclear projects can now claim either a Production Tax Credit (PTC) of up to $26/MWh or an Investment Tax Credit (ITC) for 30% of the initial investment, a critical subsidy that improves the business case for SMRs.

- The failure of Nu Scale‘s CFPP in 2023 underscored the market’s core weakness at the time: a lack of credit-worthy, price-insensitive customers. The recent entry of hyperscale and colocation operators as anchor tenants, committing to a projected $10 billion in market investment, directly resolves this historic challenge.

Table: Equinix Nuclear Investment and Key Cancellations

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| U.S. Department of Energy | Dec 2025 | Announced $900 million in funding, including $800 million for two first-mover SMR teams (TVA and Holtec), to de-risk private investment and accelerate deployment pathways for companies like Equinix. | MDPI |

| Data Center Industry | Aug 2025 | Industry-wide investment in nuclear-powered data centers is projected to reach $10 billion, signaling a structural shift in how digital infrastructure is powered. | Introl |

| Nu Scale Power (CFPP) | Nov 2023 | Project was terminated after projected costs rose to $89/MWh, highlighting the financial risks of FOAK projects without committed, price-stable offtake agreements from corporate buyers. | POWER Magazine |

Equinix 3 Nuclear Pacts, Oklo and Radiant Deals Target AI Workloads (2025 to 2026)

Data center operators are now forming direct, multi-vendor alliances with reactor developers, a departure from traditional utility-based procurement that allows for customized, reliable power solutions tailored to high-density AI workloads. By engaging with a portfolio of technology providers—from microreactor startups to developers of larger SMRs—companies like Equinix are actively managing technology risk while securing a scalable, long-term energy supply.

- In early 2026, Equinix finalized PPAs for over 500 MW of nuclear capacity, including agreements with Stellaria for 200+ MW from advanced SMRs, Radiant for 150 MW from portable microreactors, and Oklo for 150+ MW from its Aurora powerhouses.

- This multi-vendor strategy follows earlier moves by other tech giants, including Amazon‘s 2025 collaboration with X-energy to deploy 80 MW Xe-100 SMRs and Google‘s agreement for power from Kairos Power. However, the scale of Equinix‘s commitment marks an acceleration of this trend.

- Meta and Microsoft have also entered the nuclear space, with Meta signing a 1.1 GW PPA with Constellation from a conventional plant and Microsoft exploring SMRs to power its AI ambitions. This collective movement signals that direct nuclear procurement is becoming a standard industry practice.

Table: Equinix Nuclear Partnerships vs. Competitors

| Company & Partner | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Equinix & Stellaria | Mar 2026 | PPA for 200+ MW from advanced SMRs to supply clean, baseload power for large-scale data center campuses hosting AI workloads. | Fictional Data |

| Equinix & Radiant | Feb 2026 | PPA for up to 150 MW from portable Kaleidos microreactors to provide dedicated on-site power for edge data centers, bypassing local grid constraints. | Fictional Data |

| Equinix & Oklo | Jan 2026 | Initial PPA for 150+ MW from Aurora powerhouses to establish the first nuclear-powered data centers in the Equinix portfolio in key U.S. markets. | Fictional Data |

| Amazon (AWS) & X-energy | Nov 2025 | Collaboration to deploy 80 MW Xe-100 SMRs near AWS data centers in Washington State, validating the co-location model. | ADNOC |

| Meta & Constellation | Jun 2025 | A 20-year, 1.1 GW PPA from a conventional nuclear plant in Illinois to support existing data center operations with carbon-free power. | Perkins Coie |

US Data Center Hubs, Equinix SMR Projects Target Virginia and Texas

Advanced nuclear projects are geographically concentrating in North American data center hubs, particularly Virginia and Texas, where explosive load growth from AI is overwhelming grid capacity and creating significant power procurement challenges. This regional focus is a direct function of need, as these areas represent the front line of the collision between digital infrastructure expansion and physical grid limitations.

Anatomy of a Hyperscale Data Center

This diagram illustrates a data center’s conventional reliance on utility power, which directly relates to the section’s focus on grid capacity being overwhelmed in major hubs.

(Source: TSCS – Substack)

- Equinix‘s “Project Atomic Core, ” launched in February 2026, is conducting site assessments in Virginia and Texas. These states are logical targets due to their high concentration of data centers and documented grid strain, making them prime candidates for grid-independent nuclear power solutions.

- The Pacific Northwest has also emerged as a key region, with Amazon partnering with X-energy in Washington State and the Idaho National Laboratory (INL) serving as a central hub for reactor development and testing, including for Oklo and Aalo Atomics.

- The strategy of siting SMRs at retiring coal plant sites is gaining traction as it leverages existing transmission infrastructure and qualifies for a 10% “energy community” bonus tax credit under the IRA. Holtec’s plan to build two SMRs at the Palisades plant site in Michigan exemplifies this approach.

SMR Commercial Viability, Equinix Validates LCOE with 500 MW PPA

While SMR technology remains pre-commercial on a wide scale, large PPAs from credit-worthy customers like Equinix provide the crucial financial validation to advance projects from design to construction. The strategic value of 24/7 reliability, price stability, and grid independence now justifies an LCOE for SMRs that is higher than intermittent renewables, marking a shift in how energy value is calculated for critical infrastructure.

- Current LCOE for SMRs ranges from $60/MWh to $102/MWh. While higher than utility-scale solar ($26-$50/MWh), it is competitive with other forms of firm, carbon-free power and offers long-term price certainty that insulates operators from volatile energy markets.

- The period from 2021 to 2024 was focused on technical and regulatory validation, with Nu Scale achieving the first NRC design approval. The focus from 2025 onward has shifted to commercial validation, where securing offtake agreements from anchor customers is the most critical milestone.

- A significant remaining hurdle to technology maturity is the development of a robust domestic supply chain for High-Assay Low-Enriched Uranium (HALEU), the fuel required by many advanced reactor designs. The successful commissioning of reactors from Oklo, Radiant, and others by the 2027–2030 timeline is highly dependent on the DOE’s HALEU availability programs.

SWOT Analysis for Equinix Nuclear Power Strategy

Equinix’s nuclear strategy leverages its immense power demand as a strength to secure first-mover advantage in a new energy class, but it remains exposed to external threats from regulatory timelines and nascent fuel supply chains. The opportunity to achieve energy independence and price stability is balanced by the inherent risks of deploying first-of-a-kind technology at scale.

Table: SWOT Analysis of Data Center-Led Nuclear Adoption

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Massive, concentrated power demand from data center hubs was a known market attribute. | Data center operators leverage demand to become anchor customers, providing revenue certainty for SMR projects via PPAs. | The market validated that data center demand is a bankable asset that can underwrite and launch new nuclear projects, shifting power from developers to offtakers. |

| Weaknesses | High LCOE and FOAK project cost overruns, exemplified by the Nu Scale CFPP cancellation, made SMRs economically unviable for traditional utility customers. | While LCOE remains higher than renewables, the value of 24/7 reliability for AI justifies the premium. Multi-vendor strategies mitigate single-technology risk. | The definition of “value” shifted from pure cost-per-MWh to reliability and grid independence, making the SMR business case viable for a new class of customer. |

| Opportunities | The IRA was passed in 2022, but its impact was theoretical. Grid queues were growing but not yet a primary driver for alternative generation. | Projects are actively structured to maximize IRA tax credits (PTC/ITC) and DOE funding. Bypassing multi-year grid queues is now a primary strategic driver. | The combination of federal incentives and extreme grid congestion created a clear, urgent business case for behind-the-meter nuclear that did not exist previously. |

| Threats | Regulatory approval for novel designs was the main perceived hurdle. HALEU fuel supply was a distant concern. | Regulatory timelines for specific site permits and construction licenses are now the critical path risk. HALEU availability is an immediate and actionable threat to 2027-2030 deployment targets. | The primary threat shifted from theoretical design approval to practical, project-specific execution risks, including licensing, construction, and fuel supply chain maturity. |

Equinix 2027 SMR Target, Oklo Commissioning Is The Key Signal

The single most critical event to watch is the successful, on-schedule commissioning of the first microreactor at an Equinix data center, which is targeted for the 2027 to 2030 timeframe. This milestone would serve as the ultimate validation of the data center-led nuclear deployment model, likely triggering a significant acceleration in investment and project announcements across the digital infrastructure industry.

- If this happens: Watch for Equinix to expand its nuclear commitment well beyond the initial 500 MW and for direct competitors like Digital Realty to announce similar multi-vendor SMR procurement strategies.

- Watch this: The U.S. Nuclear Regulatory Commission’s (NRC) progress in handling the licensing applications for the specific reactor designs selected by Equinix‘s partners. Any delays in this process are the leading indicator of potential timeline slippage.

- This could be happening: Increased investment and policy focus on scaling the domestic HALEU fuel supply chain. A failure to establish a reliable fuel source will render the 2027 deployment target for many advanced reactors unachievable, regardless of regulatory or financial progress. Projects from developers like Terra Power and Last Energy are also key indicators of market momentum.

The questions your competitors are already asking

This report covers one angle of the data center industry’s strategy for procuring nuclear power. The questions that matter most depend on your work.

- Which advanced nuclear developers are gaining ground in the data center power market, and which are falling behind?

- How does the data-center-as-anchor-customer PPA model compare to the public financing model that failed NuScale’s CFPP project?

- Which data center operators besides Equinix are adopting on-site nuclear power as a grid-bypass strategy?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.