Europe’s Offshore Wind Boom Hits a Wall: Supply Chain Risks & Cost Crisis Define 2026

Offshore Wind Project Pipeline Faces 2026 Execution Risk Amid Cost Pressures

The European offshore wind sector’s expansion is now governed by disciplined execution and profitability, a stark departure from the growth-at-all-costs mentality that defined the market prior to 2024. While gigawatt-scale projects continue to come online, demonstrating immense technical capability, severe economic headwinds are forcing a systemic market correction. The industry has shifted from celebrating subsidy-free bids to confronting project cancellations and re-evaluating financial models to account for persistent cost inflation and supply chain instability.

- Between 2021 and 2023, the industry reached a peak of optimism with the commissioning of the world’s first major subsidy-free project, Hollandse Kust Zuid (1.5 GW) in the Netherlands, suggesting a future independent of government support.

- This outlook was fractured in 2024-2025, when cost inflation and rising capital costs became undeniable threats. Vattenfall’s decision to halt its 1.4 GW Norfolk Boreas project in the UK after costs surged by 40% served as a critical market signal that the previous economic model was no longer viable.

- In response, successful projects in 2025 demonstrate a new model. Ørsted’s Final Investment Decision (FID) on the 2.9 GW Hornsea 3 project was secured not on a low bid, but with an inflation-indexed contract awarded years prior, highlighting that revenue security has replaced aggressive pricing as the key enabler for new builds.

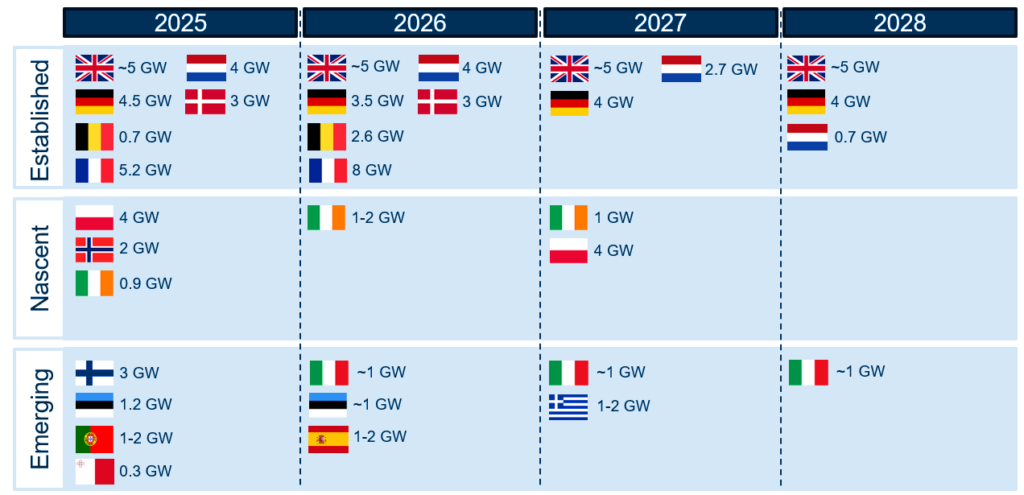

European Offshore Wind Pipeline Faces Uncertainty

This chart illustrates the European offshore wind pipeline through 2028, providing context for the execution risks and market correction discussed in the section.

(Source: OWC)

Offshore Wind Cancellations and Impairments Signal a Market Reset for 2026

Significant project cancellations and financial write-downs in 2023 and 2024 are not isolated incidents but direct evidence of a systemic financial crisis impacting the offshore wind development pipeline. These events reveal a deep mismatch between revenue assumptions made in past auctions and the current reality of high construction and capital costs. This has forced developers to either absorb massive losses, cancel projects, or demand new contract terms, fundamentally altering the risk profile for future investments heading into 2026.

Europe’s Offshore Growth Slows Amid Market Reset

This chart’s depiction of declining annual capacity additions in Europe visually represents the ‘market reset’ and systemic crisis caused by project cancellations.

(Source: EnkiAI)

- Vattenfall‘s decision to halt development of the Norfolk Boreas project in the UK stands as the most prominent signal of market distress. The developer determined the project was no longer profitable under its existing Contract for Difference (Cf D) due to soaring supply chain costs.

- Ørsted, the market’s largest developer, announced impairments of approximately $4 billion in late 2023, primarily linked to its US project portfolio, which faced similar supply chain and interest rate pressures. This financial hit forced the company to revise its entire business model toward stricter risk management and capital discipline.

- These high-profile financial struggles illustrate that even the most experienced developers are vulnerable, recalibrating investor expectations for the returns and risks associated with large-scale offshore wind development.

Table: Key Project Cancellations and Financial Revisions (2023-2024)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Vattenfall / Norfolk Boreas | Mid-2023 | Development of the 1.4 GW project was halted due to a reported 40% increase in costs, making it unprofitable under its existing Cf D revenue contract. This was a landmark event signaling systemic cost inflation. | Vattenfall |

| Ørsted / US Portfolio | Q 3 2023 | Announced impairments of $4 billion (DKK 28.4 billion) and ceased development of its Ocean Wind 1 and 2 projects in the US due to supply chain issues, high interest rates, and lack of favorable tax credit guidance. | Ørsted |

Strategic Alliances in European Offshore Wind Evolve to Mitigate 2026 Financial Risks

Partnerships in the European offshore wind sector are evolving from simple joint development ventures to complex, risk-mitigating alliances that incorporate financial institutions and industrial offtakers early in the project lifecycle. This shift is a direct reaction to rising capital costs and revenue uncertainty. By securing investment partners and corporate power purchasers before major capital commitments are made, developers are creating more resilient financial structures to weather market volatility through 2026.

- The Dogger Bank project (3.6 GW) exemplifies the traditional large-scale developer partnership, with energy majors Equinor and SSE leveraging their combined balance sheets and execution expertise, later bringing in Vårgrønn.

- A more evolved model is seen in the Hollandse Kust Zuid (1.5 GW) project, where developer Vattenfall brought in chemical giant BASF and financial services company Allianz as partners. This structure secured a major offtaker for a portion of the power and brought in long-term financial backing, de-risking the subsidy-free project.

- Similarly, En BW sold significant stakes in its 960 MW He Dreiht project to co-investors including Norges Bank Investment Management, Allianz Capital Partners, and AIP before reaching a final investment decision, distributing financial risk at an early stage.

Table: Key Strategic Partnerships in European Offshore Wind (2023-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| En BW / He Dreiht | 2023 | En BW secured Norges Bank Investment Management, Allianz Capital Partners, and AIP as co-investors, each taking a stake. This distributed the €2.4 billion investment, reducing En BW‘s capital exposure before construction began. | En BW |

| Vattenfall / Hollandse Kust Zuid | 2023 | Vattenfall partnered with BASF and Allianz. BASF secured a 49.5% stake to offtake power for its chemical production, while Allianz provided capital, creating a financially robust, subsidy-free model. | Vattenfall |

| Ørsted / Hornsea 3 | Dec 2023 | After taking the FID alone, Ørsted announced its intent to farm-down a stake in the 2.9 GW project in 2024. This follows a standard industry model of developing a project and then selling equity to recycle capital for future developments. | Ørsted |

UK, Germany, and France Dominate European Offshore Wind Construction into 2026

The United Kingdom, Germany, and France represent the core of European offshore wind construction activity for the 2024-2025 period, but each market demonstrates a different strategic priority. The UK continues to lead on sheer scale with multi-gigawatt projects, Germany is pioneering new auction models with negative bidding, and France is focused on an accelerated build-out to establish its foundational offshore wind capacity. Collectively, these three nations are driving the bulk of European capacity additions and supply chain demand.

UK, Germany, and France Lead 2024 Installations

This chart directly supports the section’s claim by showing that the UK, Germany, and France were the top three countries for new offshore wind capacity in 2024.

(Source: WindEurope)

- The UK remains the epicenter of mega-projects, defined by the construction of Dogger Bank (3.6 GW), Hornsea 3 (2.9 GW), and East Anglia THREE (1.4 GW). These projects solidify its status as the world’s second-largest offshore wind market and a critical hub for the entire European supply chain.

- Germany’s market is characterized by a push for subsidy-free projects and intense auction competition. The concurrent construction of Ørsted‘s Borkum Riffgrund 3 (900 MW) and Gode Wind 3 (242 MW), along with En BW‘s He Dreiht (960 MW), are all outcomes of zero-subsidy bids, with developers like RWE now paying billions for site rights.

- France is rapidly scaling up its operational fleet after years of slow development. The commissioning of Saint-Brieuc (496 MW) and Fécamp (498 MW) in 2024, followed by Courseulles-sur-Mer (448 MW), marks a significant milestone, establishing a domestic industry and supply chain.

Offshore Wind Turbine Technology: 15 MW+ Scale-Up Creates Profitability Crisis for 2026

The race to develop and deploy next-generation 15 MW+ offshore wind turbines has created a severe profitability crisis for manufacturers, a critical threat to the entire European supply chain heading into 2026. While these larger turbines are essential for improving project economics, the rapid pace of innovation has led to soaring warranty costs, quality control issues, and immense financial strain on OEMs. The stability of turbine manufacturers like Siemens Gamesa and Vestas is now a central risk for the industry’s growth targets.

Turbine Scale-Up Trend Toward 15 MW+

This chart illustrates the technological trend of scaling up turbines to 15 MW and beyond, which is the central topic and cause of the profitability crisis described.

(Source: Windletter – Substack)

- From 2021 to 2023, the focus was on technological advancement, with GE‘s Haliade-X, Vestas‘s V 236-15.0 MW, and Siemens Gamesa‘s 14-236 DD platform competing for dominance. These turbines were key to enabling the gigawatt-scale projects now under construction.

- By 2024-2025, the narrative shifted to the financial fallout. Siemens Energy required billions in provisions to fix extensive quality issues in Siemens Gamesa‘s onshore platforms, raising concerns about the reliability of rapidly scaled-up offshore models and crippling the company’s profitability.

- The primary challenge for 2026 is execution. Both Vestas and Siemens Gamesa must now prove they can manufacture their massive turbine backlogs profitably and without defects. Their success or failure will directly impact the delivery schedules and financial viability of nearly every major offshore wind project in Europe.

SWOT Analysis for European Offshore Wind Market (2026 Outlook)

The European offshore wind market is at an inflection point where its proven strengths in project execution are being directly challenged by severe economic and supply chain threats. Opportunities in new technologies like floating wind are promising but require navigating the immediate weaknesses of financial instability and manufacturing bottlenecks. The analysis below contrasts the market sentiment and realities between the 2021-2023 growth phase and the 2024-2025 correction period.

Table: SWOT Analysis for European Offshore Wind (2021-2025)

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Demonstrated ability to develop and finance subsidy-free projects like Hollandse Kust Zuid. Strong project pipeline and government targets. | Proven execution capability on massive, complex projects like Dogger Bank (3.6 GW). Established leadership by developers like Ørsted, Equinor, and RWE. | The industry validated its technical ability to build at an unprecedented scale, but this strength is now constrained by economic factors. |

| Weaknesses | Nascent supply chain for next-generation 12 MW+ turbines. Dependence on a few key OEMs. | Extreme financial pressure on turbine OEMs (e.g., Siemens Gamesa‘s quality issues). Project margins eroded by cost inflation and high interest rates. | The weakness shifted from a potential supply chain bottleneck to an acute profitability and quality crisis at the heart of the supply chain. |

| Opportunities | Expanding into new markets and pioneering floating offshore wind technology (e.g., Hywind Tampen‘s construction). | Commercialization of floating wind to unlock deeper water sites. Development of new auction models that account for inflation and non-price criteria. | The crisis in fixed-bottom economics makes the long-term potential of floating wind even more critical, as it opens up new, higher-quality wind resources. |

| Threats | Potential for supply chain delays and cost overruns on large projects. | Systemic risk from OEM instability. Project cancellations (Norfolk Boreas) due to unviable economics. Intense auction competition (negative bidding) creating winner’s curse scenarios. | The threat of cost overruns materialized into a full-blown crisis, leading to actual cancellations and threatening the financial health of core industry players. |

2026 Offshore Wind Outlook: Expect Project Delays and a Focus on Capital Discipline

If cost inflation and supply chain instability persist through 2025, the European offshore wind industry will see a clear bifurcation between well-structured, financially resilient projects and those awarded under outdated, low-cost auction models. The critical signal to watch is a shift in government auction design away from pure price competition toward frameworks that value supply chain security and offer inflation protection. The market leaders of 2026 will be defined not by the size of their announced pipelines, but by their ability to execute projects profitably.

Future Supply Shortages Signal Project Delays

This chart, forecasting a significant tower shortage, provides a concrete example of the supply chain instability that will cause the project delays predicted in the 2026 outlook.

(Source: Rystad Energy)

- Watch for project timeline revisions: Developers holding contracts from low-priced auction rounds pre-2022 may announce further delays or attempt to renegotiate terms, citing continued economic pressure.

- Monitor OEM financial reports: The quarterly results of Siemens Gamesa and Vestas will be a direct indicator of whether the supply chain is stabilizing. Continued losses or quality provisions would signal ongoing systemic risk.

- Track auction results in the UK and Germany: The structure and clearing prices of the next major auction rounds will confirm if governments are adjusting to the new cost reality. A move toward inflation-indexed contracts or non-price criteria would be a positive signal for sustainable growth.

- Floating wind FIDs are the next frontier: A final investment decision on a commercial-scale (500 MW+) floating wind project in Europe would validate the technology’s path to bankability and signal the opening of a major new growth market.

Frequently Asked Questions

Why are offshore wind projects being cancelled or delayed if there is so much demand for clean energy?

Projects are being cancelled or delayed primarily due to a severe financial crisis. Contracts awarded in previous years were based on low-cost assumptions that are no longer viable. For example, Vattenfall halted its 1.4 GW Norfolk Boreas project after costs surged by 40%, making it unprofitable under its existing contract. This mismatch between old revenue agreements and current high inflation, supply chain costs, and interest rates is forcing developers to reconsider their projects.

What is the single biggest risk facing the European offshore wind industry leading into 2026?

The biggest risk is the financial instability and profitability crisis affecting the major turbine manufacturers (OEMs). The rapid race to scale up to 15 MW+ turbines has led to significant quality control issues and warranty costs, as seen with Siemens Gamesa. Since these companies are at the heart of the supply chain, their financial health and ability to deliver reliable turbines on schedule is a critical threat to nearly every major project in Europe.

The article mentions a shift from ‘subsidy-free’ optimism. Does this mean offshore wind is no longer economically viable without government support?

It means the model for achieving viability has changed. The initial optimism for subsidy-free projects like Hollandse Kust Zuid was based on a low-cost environment. The current market correction shows that projects need more secure revenue streams to cope with inflation and risk. Successful new projects are now enabled by inflation-indexed contracts (like Ørsted’s Hornsea 3) or by bringing in industrial and financial partners early on to de-risk the investment, rather than relying solely on aggressive, low-price auction bids.

How are successful offshore wind developers adapting to the current cost crisis?

Successful developers are moving away from simple joint ventures and are building complex, risk-mitigating alliances. They are securing investment partners and corporate power purchasers (offtakers) much earlier in the project lifecycle. For instance, EnBW sold stakes in its He Dreiht project to investors like Allianz Capital Partners before the final investment decision to distribute financial risk. Similarly, Vattenfall partnered with BASF (as an offtaker) and Allianz (as a capital partner) for its Hollandse Kust Zuid project to create a more resilient financial structure.

What key signs will indicate if the offshore wind market is stabilizing in 2026?

According to the outlook, three key signals to watch for are: 1) Governments reforming auction designs to move away from pure price competition and include inflation protection. 2) The quarterly financial reports of turbine manufacturers like Siemens Gamesa and Vestas showing a return to profitability, indicating the supply chain is stabilizing. 3) A final investment decision (FID) on a commercial-scale (500 MW+) floating offshore wind project, which would signal the bankability of the next major growth technology.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.