China’s Onshore Wind Strategy 2026: How Integrated Energy Bases Threaten Global Supply Chains

From Wind Farms to Giga-Bases: China’s Onshore Wind Project Evolution

China’s onshore wind strategy has fundamentally shifted from deploying individual wind farms to constructing integrated, giga-scale energy bases that combine wind power with downstream industrial applications like green hydrogen production. This pivot redefines the purpose of wind assets, transforming them from pure electricity generators into engines for a state-controlled green industrial ecosystem. This model leverages immense domestic scale to create a nearly insurmountable competitive advantage, setting the stage for a disruptive global export push.

- Between 2021 and 2024, the primary focus was on rapid capacity addition to meet national renewable energy targets. Projects were often large but functionally siloed, such as the 84 MW Hunan Guidong Wind Farm Project, which served regional electricity needs. During this period, China added a staggering 75 GW of wind capacity in 2023 alone.

- Starting in 2025, the model evolved toward deep vertical integration. The announcement of State Power Investment Corp (SPIC)‘s $5.9 billion investment in Inner Mongolia exemplifies this change. This project combines a 3.5 GW wind power plant directly with a 164, 000 metric ton-per-year green hydrogen facility, internalizing electricity demand and creating a direct link between generation and industrial output.

- The record-breaking installation of 119 GW of new wind capacity in 2025 was not merely for grid supply but was driven by the necessity to power these new industrial bases. This massive domestic demand allows OEMs like Goldwind and Envision Energy to refine technology and achieve economies of scale that are impossible for international rivals to replicate.

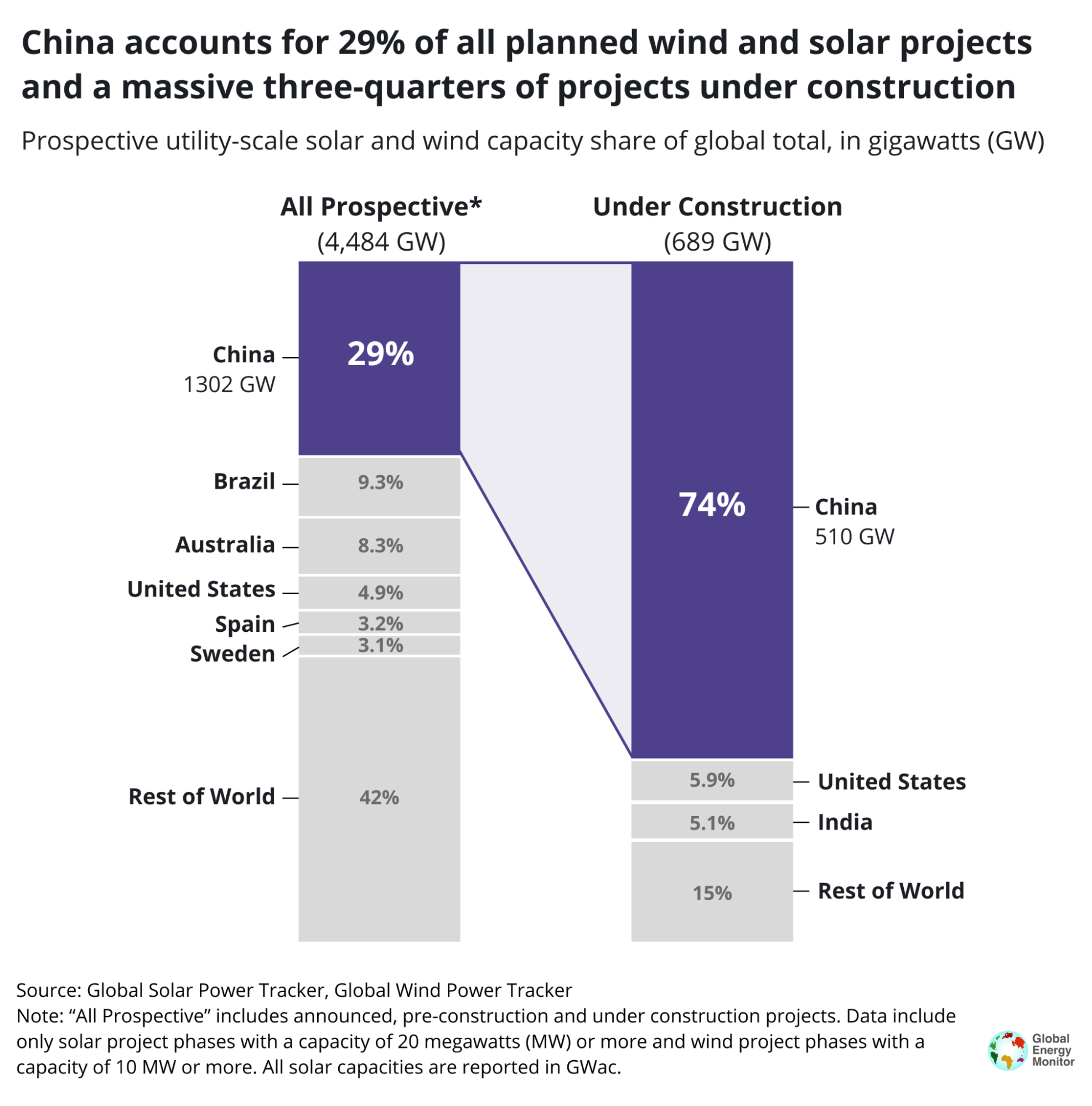

China Dominates Global Renewable Construction

This chart’s data on China’s massive share of global projects under construction (510 GW) directly visualizes the scale of the ‘giga-base’ strategy mentioned in this section.

(Source: EnkiAI)

State-Directed Capital: Analyzing China’s Onshore Wind Investment Surge

A massive wave of state-directed capital is accelerating the development of China’s onshore wind sector and its integration with strategic industries. This financial firepower, guided by national policy rather than purely commercial returns, enables the construction of integrated energy bases at a pace and scale that private markets cannot match. This creates a significant structural advantage that is reshaping global energy dynamics.

- According to ANZ Research, China was projected to invest 13 trillion RMB ($1.8 trillion) in green infrastructure through 2025, with an estimated 3.4 trillion RMB ($470 billion) specifically allocated to new wind and photovoltaic power sectors.

- The intensity of this capital deployment became clear in 2025, when investment in key onshore wind projects surged by nearly 50% year-over-year, confirming a deliberate acceleration of the national strategy.

- Individual project investments underscore this trend. The $5.9 billion commitment by SPIC for its Inner Mongolia green fuel facility demonstrates how capital is being allocated to integrated projects that secure the entire value chain, from turbine to final product.

Table: Key Onshore Wind Investments and Financial Commitments (2023-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Green Infrastructure National Target | Through 2025 | 13 trillion RMB ($1.8 trillion) allocated for broad green infrastructure, creating a massive pool of capital for renewable projects. | ANZ |

| Wind & PV Sector Investment | 2023 | An estimated 3.4 trillion RMB ($470 billion) in new investment was directed into the wind and photovoltaic power sectors. | Global Times |

| SPIC Green Fuel Project | Announced Dec 2023 | $5.9 billion (42.7 billion yuan) investment in an integrated green fuel project in Inner Mongolia, including a 3.5 GW wind plant to power hydrogen production. | Reuters |

| Key Project Investment Growth | Full Year 2025 | Investment in key onshore wind projects increased by nearly 50% year-over-year, indicating an acceleration of capital deployment. | China Daily |

Geographic Concentration: How China’s Northern Wind Corridors Dominate Development

China’s onshore wind development is heavily concentrated in its northern and western provinces, which serve as massive “Giga-Bases” due to superior wind resources and vast land availability. This geographic strategy allows for centralized planning and scaled deployment but creates significant challenges for grid integration and long-distance power transmission to coastal demand centers. This regional focus is part of a broader national strategy to secure Asia’s Energy Security by minimizing reliance on volatile global energy markets.

China’s Wind Growth Concentrated in North

This chart is a perfect match, as its description explicitly states that China’s wind capacity growth is ‘heavily concentrated in the North and Northwest regions,’ the exact topic of this section.

(Source: Wood Mackenzie)

- Between 2021 and 2024, Inner Mongolia, Xinjiang, and Gansu were cemented as the core development hubs for large-scale wind power. In 2023 alone, Inner Mongolia led all provinces with over 24 GW of new wind installations, more than the total capacity of many countries.

- This concentration intensified in 2025. Projections for the first half of the year showed the North and Northwest regions leading a national growth surge of 99% in new wind additions compared to the previous year, with the North region’s capacity additions rising to 15.9 GW.

- While these northern bases represent the core of China’s strategy, smaller projects in other provinces, like the Hunan Guidong Wind Farm, continue to be developed. These projects play a crucial role in improving regional grid stability and meeting local demand, but the strategic focus remains on the giga-scale northern corridors.

Technology Maturity: China’s Rapid Onshore Wind Turbine Innovation at Commercial Scale

Chinese wind turbine technology has reached full commercial maturity and is now iterating at a speed that outpaces global competitors, driven by the immense scale and specific demands of its domestic market. The focus has shifted from merely producing turbines to designing and deploying highly efficient, specialized models integrated directly with downstream applications. This rapid innovation cycle solidifies China’s technological leadership and cost advantage.

Chinese Firms Dominate Wind Turbine Market

This chart, showing Chinese firms in the top four global spots for 2024, directly proves the ‘commercial maturity’ and ‘technological leadership’ of China’s turbine industry discussed in this section.

(Source: Windletter – Substack)

- In the period leading up to 2024, Chinese OEMs were already pushing the technological frontier. For instance, China Haizhuang installed its first 5 MW onshore wind turbine in 2021, a platform with a large rotor diameter designed for the country’s specific wind conditions, signaling a move beyond smaller, less efficient models.

- This trend accelerated dramatically into 2025. At the China Wind Power 2025 conference, 12 domestic manufacturers collectively launched 27 new wind turbine models, a clear demonstration of a hyper-competitive and rapidly innovating domestic ecosystem.

- Technological advancement extends beyond the turbines themselves to full system integration. The development of “typhoon-proof” wind farms and a successful pilot project by Dongfang Electric to produce green hydrogen directly from seawater using dedicated wind power showcases a sophisticated, systems-level approach to energy production and conversion.

SWOT Analysis: China’s Onshore Wind Market Dynamics and Strategic Risks

China’s onshore wind sector leverages unparalleled manufacturing scale and state support to dominate the global market, but it faces growing internal pressures from grid constraints and the external threat of international trade friction. As the industry pivots from a domestic build-out to a global export strategy, its immense strengths also expose new vulnerabilities. The potential for geopolitical events to disrupt the global energy transition makes control over renewable energy supply chains a critical strategic asset.

China Drives 70% of New Onshore Wind

This chart illustrates a primary ‘Strength’ for the SWOT analysis by showing China’s massive share of new installations, which underpins the ‘unparalleled manufacturing scale’ mentioned in the text.

(Source: Windletter – Substack)

- Strengths: The key strength has evolved from pure installation volume to deep industrial integration, creating a closed-loop system that reduces costs and accelerates innovation.

- Weaknesses: The primary weakness remains the strain on the national grid, with the risk of power curtailment growing in lockstep with massive capacity additions.

- Opportunities: The main opportunity has shifted from meeting domestic energy targets to establishing global leadership in the entire green energy value chain, including equipment manufacturing and green fuel production.

- Threats: Risks are now increasingly external, manifesting as international trade disputes and accusations of unfair competition, which could limit access to key export markets.

Table: SWOT Analysis for China’s Onshore Wind Sector

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Massive installation capacity (75 GW in 2023) and economies of scale in manufacturing. Dominance of domestic OEMs like Goldwind. | Vertically integrated “Giga-Bases” combining wind with green hydrogen (SPIC project). Rapid innovation cycle (27 new turbine models launched in 2025). | The strategic advantage shifted from simply building more turbines to building a fully integrated industrial ecosystem, validating the state-led model. |

| Weaknesses | Grid congestion and high curtailment rates in key wind-rich provinces. Reliance on state subsidies to drive growth. | Intensified grid pressure from record installations (119 GW in 2025). Risk of manufacturing oversupply as domestic demand saturates. | The problems of scale have worsened. The grid cannot keep pace with generation growth, creating a powerful incentive for manufacturers to export. |

| Opportunities | Meeting and exceeding the 1, 200 GW wind and solar target for 2030. Reducing domestic reliance on coal. | Leading the global green hydrogen economy. Becoming the dominant global exporter of low-cost, high-tech wind turbines. | The ambition has expanded from domestic energy security to global market dominance across the entire renewable energy technology stack. |

| Threats | Internal technical challenges related to grid stability and long-distance power transmission. | Growing international trade friction, evidenced by the EU’s April 2024 investigation into Chinese turbine subsidies. Potential for price wars that damage global market stability. | The primary risks have externalized from domestic technical issues to international geopolitical and trade conflicts. |

2026 Outlook: China’s Export Push and Global Wind Market Fragmentation

If China’s domestic grid and industrial offtake capacity cannot fully absorb its rapidly expanding manufacturing output, its state-backed OEMs will be compelled to initiate an aggressive export push in 2026. This will likely trigger intense price competition, disrupt established markets, and potentially lead to a fragmentation of the global wind supply chain as Western nations respond with protectionist measures. The stability of global LNG Supply Chains could also be impacted as energy-importing nations weigh the geopolitical risks of fossil fuels against the supply chain risks of Chinese-dominated renewables.

Chinese Wind Turbine Exports Are Surging

This chart directly supports the section’s 2026 outlook by showing that the ‘aggressive export push’ is already underway, with a dramatic projected increase in overseas orders.

(Source: Wood Mackenzie)

- If this happens, watch this: A significant increase in export volumes of Chinese turbines in late 2025 and early 2026 will be the primary signal. Envision Energy‘s successful project bids in Central Asia serve as an early template for this international expansion.

- This could be happening: Western turbine manufacturers like Vestas will face sustained pressure on margins and will likely intensify lobbying efforts for trade protections. The EU’s investigation into Chinese subsidies in April 2024 is a clear indicator of this emerging conflict.

- If this happens, watch this: The rate of new, large-scale green hydrogen project announcements within China. A slowdown in these offtake projects would signal a growing mismatch between renewable generation and industrial demand, forcing more turbine manufacturing capacity onto the global market at depressed prices.

Frequently Asked Questions

What is the main change in China’s onshore wind strategy described in the article?

The main change is a strategic pivot from building individual, siloed wind farms for electricity generation to constructing massive, integrated ‘Giga-Bases.’ These new projects combine wind power generation directly with downstream industrial applications, such as green hydrogen production, creating a state-controlled green industrial ecosystem.

How do China’s integrated energy bases create a competitive advantage?

These bases create a huge, guaranteed domestic demand for turbines, allowing Chinese OEMs like Goldwind and Envision to achieve immense economies of scale. This vertically integrated model, linking generation directly to industrial use (like SPIC’s $5.9 billion project), drives down costs and accelerates technological innovation at a speed and scale that international competitors cannot replicate.

What is the primary internal risk or weakness in China’s wind power expansion?

The primary weakness is the immense strain on the national power grid. The massive and rapid addition of wind capacity, especially in the northern provinces, is outpacing the grid’s ability to transmit the power to demand centers. This leads to a significant and growing risk of ‘power curtailment,’ where generated electricity is wasted because it cannot be absorbed or transmitted.

Why is China’s strategy considered a threat to global supply chains?

The strategy is a threat because it’s designed to create manufacturing overcapacity that will be pushed onto the global market. If domestic demand from the grid or industrial bases can’t absorb the massive output, state-backed OEMs will be compelled to launch an aggressive export push. This would likely trigger intense price competition, disrupt established Western manufacturers, and lead to a fragmentation of the global wind supply chain as nations respond with protectionist measures.

What key indicator suggests that China might be preparing for a major export push in 2026?

A key indicator to watch is a slowdown in the rate of new, large-scale green hydrogen project announcements within China. These projects are designed to act as industrial offtakers for the new wind power capacity. If the number of these projects stalls, it would signal a growing mismatch between generation and domestic demand, forcing turbine manufacturers to find new export markets for their surplus products.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.