Hydrogen Project De-Risking 2026: Why Internal Offtake is Phillips 66’s Winning Strategy

Hydrogen Project Viability: The Shift to Internal Offtake Models

Major energy operators are abandoning speculative hydrogen projects in favor of a de-risked model where new production capacity is anchored by guaranteed internal demand from their own industrial facilities. This strategic pivot from building for a nascent merchant market to building for self-consumption resolves the critical chicken-and-egg problem of securing reliable offtakers, making large-scale capital investments viable. The contrast in strategy before and after 2025 shows a clear market maturation, with companies like Phillips 66 moving from broad, exploratory initiatives to focused projects directly integrated into existing refinery operations.

- Between 2021 and 2024, industry focus included ambitious green hydrogen projects tied to external partners and uncertain demand, exemplified by the Gigastack project with Ørsted, which aimed to supply the Phillips 66 Humber Refinery but was ultimately stalled.

- From 2025 onward, the strategy has consolidated around projects with built-in offtake. The plan to commission a green hydrogen plant at the Ferndale refinery in early 2025 and the collaboration with Uniper on the Humber H₂ub® (Green) Project show a clear focus on using hydrogen to decarbonize existing assets first.

- This “inside-out” approach uses the company’s own refineries as the primary customer, ensuring project bankability and providing a practical platform to gain operational expertise in electrolytic hydrogen production and use at an industrial scale.

- The model extends to creating value from byproducts. The 2023 commissioning of a hydrogen blending initiative at the Bayway Refinery, where refinery off-gas is supplied to the Linden Cogen plant, demonstrates how existing hydrogen streams can be used to lower emissions in adjacent power generation.

Project Cancellations and Strategic Reprioritization

The hydrogen sector is undergoing a consolidation, where ambitious but commercially unsecured projects are being shelved in favor of initiatives with clear, immediate applications. The stalling of the Gigastack project serves as a key market signal, illustrating the high risk associated with large-scale green hydrogen developments that are dependent on external partners and fluctuating government support without a firm, internal offtake commitment. This trend underscores a strategic shift toward capital discipline and risk mitigation.

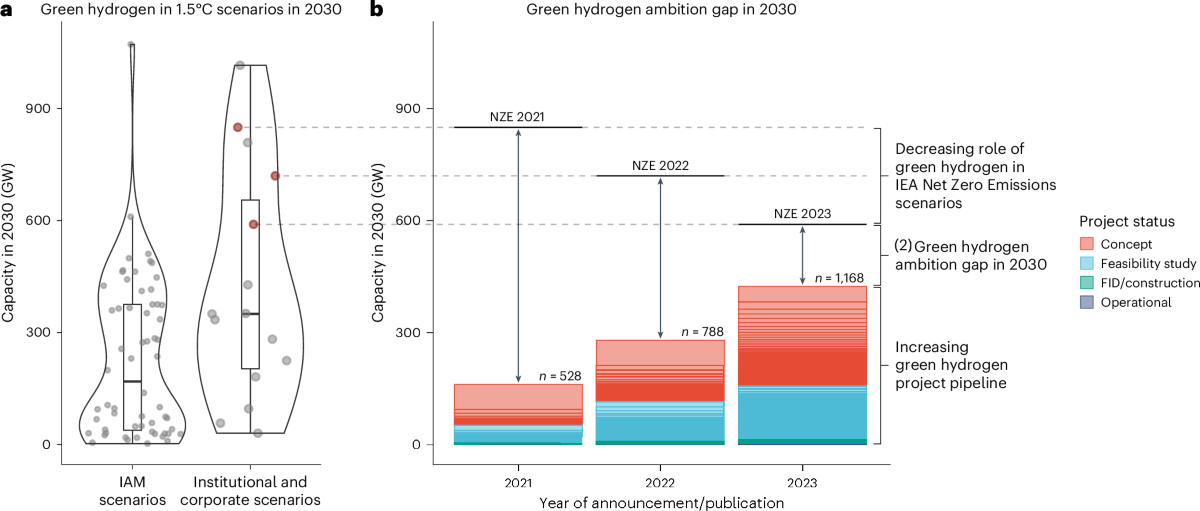

Hydrogen Project Pipeline Lags Ambition

This chart explains why projects are being cancelled by showing that the vast majority remain in early ‘concept’ or ‘feasibility’ stages, underscoring the reprioritization trend.

(Source: Nature)

Table: Hydrogen Project Status and Strategic Shifts

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Uniper / Humber H₂ub® (Green) | 2025–2029 (Active) | A proposed 120 MW green hydrogen facility to supply the Phillips 66 Humber Refinery directly. A Final Investment Decision (FID) is expected in early 2026, locking in a key internal offtaker. | Uniper |

| Ferndale Refinery Project | 2025 (Active) | Commissioning a green hydrogen plant to produce and supply hydrogen for on-site refinery operations, directly reducing the facility’s carbon footprint. | Energy, Oil & Gas Magazine |

| Ørsted / ITM Power / Gigastack | 2023 (On Hold) | A planned 100 MW electrolyzer to supply the Humber Refinery, powered by offshore wind. The project was put on hold by partner Ørsted in August 2023, highlighting partnership and policy-related risks. | Energy Watch |

Partnership Evolution for Phillips 66 Hydrogen Initiatives

Partnerships have evolved from broad, technology-exploration agreements to highly specific, commercially-driven ventures targeting defined outcomes. Early-stage collaborations focused on assessing possibilities, while recent joint ventures and agreements are structured around tangible asset development and market creation. This progression reflects a maturing strategy to secure specific capabilities, share capital costs, and establish clear routes to market.

Table: Key Hydrogen-Related Partnerships for Phillips 66

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Uniper | 2024–2025 | A collaboration agreement to facilitate the supply of green hydrogen from Uniper’s Humber H₂ub® project to the Phillips 66 Humber Refinery, targeting first delivery in 2029. This secures a low-carbon feedstock source for a core asset. | Power-to-X |

| Linden Cogeneration | 2023 | An operational project where hydrogen-rich refinery off-gas from the Bayway Refinery is commercially supplied to the adjacent power plant for blending with natural gas, reducing CO 2 emissions from power generation. | JERA Americas |

| H 2 Energy Europe | 2022 | A 50-50 joint venture to build and operate a network of up to 250 hydrogen refueling stations in Germany, Austria, and Denmark by 2026. This is a strategic move to enter the downstream hydrogen mobility market. | Phillips 66 |

| Plug Power | 2021 | A memorandum of understanding to explore the development of low-carbon hydrogen business opportunities, leveraging Plug Power’s electrolyzer and fuel cell technology. This represented an early-stage technology exploration. | Phillips 66 |

Geographic Focus: Aligning Hydrogen Projects with Refinery Assets

Hydrogen project development is geographically concentrated in regions where industrial assets already exist, demonstrating a strategy driven by asset decarbonization rather than speculative market entry. The choice of the UK and the US West Coast is not arbitrary; it is dictated by the locations of major Phillips 66 refineries that can serve as anchor customers, providing the foundational demand needed to justify new hydrogen infrastructure.

Industrial Use Dominates Hydrogen Demand

This chart provides the rationale for the geographic strategy, showing that refining is the top consumer of hydrogen, justifying the co-location of new projects with existing refineries.

(Source: Nature)

- In the period from 2021 to 2024, the UK’s Humber region emerged as the primary hub for strategic planning, with initiatives like Humber Zero and Gigastack. This was driven by the region’s status as a major industrial cluster and the presence of the Phillips 66 Humber Refinery.

- The period from 2025 to today has seen this focus solidify, with the partnership with Uniper for the Humber H₂ub® becoming the cornerstone UK project. Simultaneously, activity in the US has become more concrete with the planned 2025 commissioning of the Ferndale, Washington, green hydrogen plant.

- The geographic strategy is one of co-location. By building hydrogen production facilities at or near its own refineries (Humber, Ferndale, Bayway), Phillips 66 minimizes transportation costs and infrastructure risk, creating closed-loop ecosystems for low-carbon energy.

Technology Maturity: From R&D Exploration to Commercial Integration

The focus of technology application has shifted from exploring the potential of green hydrogen production to the practical engineering challenge of integrating it at scale into complex industrial processes. While the core technology, such as electrolysis, is mature, the test of its commercial viability now lies in its successful deployment within existing refinery operations. This marks a transition from technology validation to systems integration.

- Between 2021 and 2024, efforts were centered on demonstrating the feasibility of large-scale electrolyzers, such as the planned 100 MW unit for the Gigastack project. This phase focused on proving that the technology could be produced at a significant scale.

- The period from 2025 onward has shifted focus to operational integration. The Ferndale plant and the planned Humber H₂ub® project (120 MW) are less about testing the electrolyzer itself and more about integrating its output into refinery heaters and processes to displace conventional hydrogen.

- The successful hydrogen blending at the Linden Cogen facility in 2023 provides a commercial proof point for using hydrogen-rich gas streams to decarbonize adjacent power assets, showing that maturity is also being reached in applying hydrogen blends in established technologies like gas turbines.

SWOT Analysis: Phillips 66’s Hydrogen Strategy

The strategic position of Phillips 66 in the hydrogen market is defined by its ability to leverage existing assets to de-risk investments, but this strength creates dependencies on the operational and economic realities of its core refining business. The evolution from 2021 to 2025 reveals a clear pattern of mitigating external risks by internalizing demand.

Table: SWOT Analysis for Phillips 66 Hydrogen Initiatives for 2025

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Large-scale industrial footprint with potential hydrogen demand. Established retail network (JET brand). | Using refinery assets (Humber, Ferndale) as anchor customers for new hydrogen projects. Leveraging refinery byproducts (Bayway) for adjacent decarbonization. | The strategy of using internal offtake to de-risk hydrogen projects was validated as a more robust model compared to purely speculative ventures. |

| Weaknesses | High capital dependency on partners for large-scale projects like Gigastack. Nascent hydrogen market with uncertain demand signals. | Continued reliance on partners (Uniper) for production expertise and shared CAPEX on major projects. Project timelines are long (Humber supply not until 2029). | The weakness of partnership dependency was confirmed by the Gigastack stall, leading to a focus on partnerships with clearer commercial terms and shared goals. |

| Opportunities | Broad exploration of green hydrogen applications via MOUs (Plug Power). Entry into European mobility market. | Creating a replicable model for on-site green hydrogen production at other refineries. Building a large-scale European hydrogen refueling network by 2026 via the H 2 Energy JV. | The opportunity shifted from general exploration to specific market creation in mobility and scalable, repeatable industrial decarbonization projects. |

| Threats | Project viability heavily reliant on government subsidies and partner commitment, as seen with the Gigastack project’s dependence on Ørsted. | Economic viability of green hydrogen remains dependent on renewable power costs. Delays in FID for major projects (Humber) can push out timelines and impact strategy. | The primary threat was validated: reliance on a single partner or policy can halt a major project. The new strategy mitigates this by focusing on projects with more direct control and clearer economics. |

2026 Scenario: FID for Humber H₂ub® Is the Key Market Signal

The most critical event to watch in the near term is the Final Investment Decision (FID) for the Humber H₂ub® (Green) Project, expected in early 2026. This decision will serve as the definitive validation of the industry’s pivot toward using large-scale, integrated projects to decarbonize its own assets. A positive FID will confirm that the economics of green hydrogen for industrial use are becoming viable with the right partnership and offtake structure, likely accelerating similar projects across other industrial clusters. Conversely, a delay or negative decision would signal that significant economic or regulatory hurdles persist, even for the most strategically sound projects.

- If the Humber FID is approved in early 2026: Watch for announcements of similar green hydrogen-to-refinery projects at other Phillips 66 sites or by competitors. This would confirm the “inside-out” model is the new standard for industrial decarbonization.

- A key signal gaining traction: The operational performance of the smaller-scale Ferndale green hydrogen plant in 2025 will provide crucial data on the real-world costs and challenges of integrating electrolytic hydrogen into live refinery operations. Its success would build confidence for the larger Humber investment.

- A signal losing steam: The model of developing massive green hydrogen projects without a committed, large-scale industrial anchor tenant is losing credibility. The stall of Gigastack demonstrated that reliance on future merchant markets or uncertain policy support is too high a risk for major capital deployment at this stage.

Frequently Asked Questions

What is the “internal offtake” model, and why is it now central to Phillips 66’s hydrogen strategy?

The internal offtake model is a strategy where a company builds new hydrogen production capacity primarily to supply its own facilities, such as refineries. It is central to Phillips 66’s strategy because it solves the biggest challenge for new hydrogen projects: securing a guaranteed buyer. By acting as its own anchor customer, Phillips 66 de-risks the massive capital investment, ensures the project is financially viable, and avoids the uncertainty of building for a speculative merchant market.

Why was the Gigastack project stalled while the Humber H₂ub® project is moving forward?

The Gigastack project was highly dependent on an external partner (Ørsted) and government policy without a firm, locked-in offtake commitment from Phillips 66. When the partner put the project on hold, it stalled. In contrast, the Humber H₂ub® project is specifically designed with Phillips 66 as the guaranteed internal customer for the hydrogen. This commercial certainty makes the project more resilient and bankable, allowing it to proceed toward a Final Investment Decision (FID).

What is the most significant event to watch for in Phillips 66’s hydrogen strategy by 2026?

The most critical event is the Final Investment Decision (FID) for the Humber H₂ub® (Green) Project, expected in early 2026. A positive FID would be a major validation of the strategy to decarbonize industrial assets with integrated green hydrogen projects, proving the economic model works. It would likely trigger similar investments at other industrial sites. The operational success of the smaller Ferndale plant in 2025 is a key precursor that will provide data to support this larger decision.

Is Phillips 66 only focused on producing green hydrogen for its own refineries?

No, while decarbonizing its refineries is the core of its current strategy, Phillips 66 is also active in other parts of the hydrogen value chain. Through a joint venture with H2 Energy Europe, it is building a network of up to 250 hydrogen refueling stations in Europe by 2026 to enter the mobility market. Additionally, its Bayway Refinery commercially supplies hydrogen-rich gas to an adjacent power plant, demonstrating a model for using byproducts to reduce emissions in the power sector.

What changed in Phillips 66’s hydrogen approach between the 2021-2024 period and the post-2025 plan?

The primary change is a strategic pivot from broad, speculative exploration to focused, commercially secure projects. Between 2021 and 2024, the focus included ambitious but uncertain projects like Gigastack, which relied heavily on external partners. From 2025 onward, the strategy has consolidated around projects with guaranteed internal demand, such as the Ferndale refinery plant and the Humber H₂ub® project, which are directly integrated with existing operations to ensure project viability and an immediate path to decarbonization.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.