Hydrogen Hub Risk 2026: Why Oil Majors Are Abandoning Billions in Subsidies

The Strategic Pivot from Hydrogen Hubs to Captive Consumption

The hydrogen strategy for major U.S. refiners is undergoing a significant de-risking, shifting from speculative, large-scale clean hydrogen hub development to a conservative, integrated model focused on internal consumption. Between 2021 and 2024, the primary approach involved forming alliances to pursue billions in federal subsidies for regional hubs. This trend has reversed course in the 2025–2026 period, with companies now prioritizing capital discipline and leveraging hydrogen as an operational feedstock for their profitable renewable fuels businesses, signaling a retreat from the merchant hydrogen market.

- In the 2021–2024 timeframe, Marathon Petroleum’s strategy was aligned with the industry trend of pursuing large-scale, federally-backed projects. This was demonstrated by its participation in the Heartland Hydrogen Hub (HH 2 H) and the Appalachian Regional Clean Hydrogen Hub (ARCH 2), both of which aimed to produce blue hydrogen for broad regional use.

- A definitive strategic reversal occurred in August 2024 when Marathon Petroleum and its partner TC Energy withdrew from the Heartland Hydrogen Hub. This move canceled their participation in a project that had been selected to receive up to $925 million in U.S. Department of Energy funding.

- From 2025 onward, the focus has shifted to foundational capability building. Instead of large project announcements, activity is centered on enhancing existing operations through technology partnerships, such as the February 2026 deal with Baker Hughes for digital solutions, and workforce training via the International Board of Oil & Gas Professionals (IBOGP).

- This new strategy prioritizes using hydrogen as a critical, captive feedstock for the company’s renewable diesel facilities, like the Martinez Renewables joint venture. This creates a predictable, internal demand for hydrogen, avoiding the market and price volatility of selling it as a commodity.

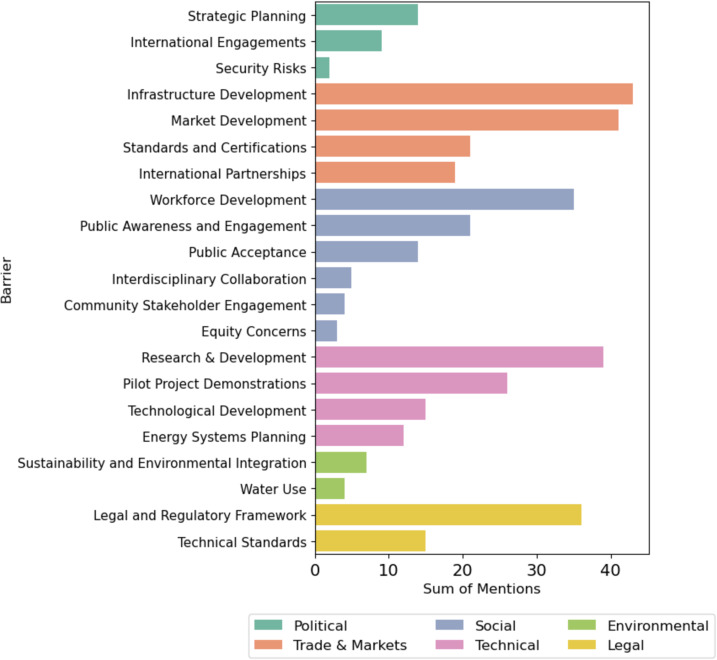

Key Barriers Drive Hydrogen Strategy Pivot

The significant challenges in infrastructure and market development, identified as top barriers in the chart, explain why companies are pivoting from large-scale hubs to internal consumption models.

(Source: ScienceDirect.com)

Investment Cancellations Signal a Retreat from Market Creation

Recent investment decisions show a clear preference for capital discipline and risk mitigation over speculative, first-mover ventures in the clean hydrogen economy. The cancellation of a multi-billion-dollar blue hydrogen project, despite significant available subsidies, in favor of a smaller, diversified low-carbon portfolio, marks a fundamental change in capital allocation strategy. This move indicates that refiners see more immediate and predictable value in optimizing existing assets for decarbonization rather than building new energy markets from the ground up.

Non-Economic Barriers Halt Market Creation

High-impact, non-economic barriers like regulatory uncertainty and public perception, as shown in the chart, provide a clear rationale for cancelling speculative multi-billion-dollar hydrogen projects.

(Source: ScienceDirect.com)

- The most significant financial signal was Marathon Petroleum’s decision in August 2024 to halt a planned $2 billion investment in the Prairie Horizon Hydrogen Project. This cancellation occurred despite the project’s central role in the Heartland Hub, which was backed by a potential $925 million federal grant.

- In contrast, the company’s forward-looking investment is a more measured $163 million capital allocation announced for projects beginning in 2026. This capital is earmarked for a diversified portfolio including blue hydrogen, CCUS, and renewable fuels, spreading risk across multiple technologies instead of concentrating it in a single large-scale hydrogen plant.

- This portfolio approach contrasts sharply with competitors like Phillips 66, which pursued a complete facility conversion at its Rodeo, California, refinery for renewable fuels, a more concentrated strategic direction. Marathon’s approach allows for optionality without exposing the company to the high upfront costs and regulatory uncertainties, such as the final rules for the 45 V tax credit, that currently impact the hydrogen sector.

Table: Strategic Investment and Cancellation Analysis (2024-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Low-Carbon Technologies Portfolio | 2026 | A $163 million allocation for a mix of low-carbon liquid fuels, blue hydrogen, and carbon capture. This represents a cautious, diversified entry into low-carbon technologies. | Marathon Petroleum Corporation (MPC): history, ownership, mission … |

| Prairie Horizon Hydrogen Project | 2024 (Canceled) | A $2 billion blue hydrogen project was halted. The cancellation signaled a strategic retreat from large-scale hydrogen production for external markets, prioritizing capital discipline. | Marathon Petroleum withdraws from $925 million Prairie Horizon … |

Partnership Strategy Shifts from Project Alliances to Capability Building

The nature of strategic partnerships has evolved from forming large consortia for hub development to creating targeted collaborations aimed at building foundational technical and human capital. Before 2025, partnerships were primarily structured to secure federal funding and share the risks of massive infrastructure projects. The new model, evident in 2025 and 2026, focuses on securing the technology and talent needed to execute future decarbonization projects efficiently and safely within the company’s existing operational footprint.

- The pre-2025 strategy was defined by large-scale alliances, most notably the partnership with TC Energy and Xcel Energy for the Heartland Hydrogen Hub. This collaboration was designed to develop, build, and operate a regional hydrogen economy but was disbanded in 2024.

- In February 2026, Marathon Petroleum formed a technology and service agreement with Baker Hughes. This deal focuses on deploying specialized chemical treatments and digital solutions to optimize refinery operations, a critical precursor for integrating complex systems like CCUS and blue hydrogen production.

- A focus on human capital is evident in the November 2025 affiliate partnership with the International Board of Oil & Gas Professionals (IBOGP). This collaboration, centered on the “Executive Diploma in Hydrogen Economy & Future Fuels, ” signals a proactive effort to upskill the workforce for the energy transition.

- The enduring partnership is the Martinez Renewables joint venture with Neste. This 50/50 JV remains the core of the renewables strategy and serves as the primary internal consumer of hydrogen, making it the anchor of the company’s current hydrogen-related activities.

Table: Evolution of Marathon Petroleum’s Hydrogen-Related Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Baker Hughes | 2026 | Technology and service agreement to provide digital and chemical solutions to optimize refinery operations, building a foundation for future CCUS and blue hydrogen projects. | Fuel Archives | ESG News.earth |

| International Board of Oil & Gas Professionals (IBOGP) | 2025 | Affiliate partnership to upskill employees via a diploma in the hydrogen economy, preparing the workforce for future energy systems. | Affiliate Partners – International Board of Oil & Gas Professionals |

| TC Energy, Xcel Energy (Heartland Hydrogen Hub) | 2024 (Exited) | Exited a major alliance for a blue hydrogen hub. The withdrawal confirmed a strategic pivot away from building external hydrogen markets. | Marathon Petroleum, TC Energy no longer involved with Heartland … |

| Neste (Martinez Renewables) | 2022 – Active | Active 50/50 joint venture converting a refinery to produce renewable diesel, creating a significant and stable internal demand for hydrogen as a feedstock. | Marathon Petroleum implements Topsoe technology at Martinez … |

Geographic Focus Narrows to Existing Refinery Footprints

The geographic strategy for hydrogen development has contracted from ambitious, multi-state greenfield regions to the existing brownfield sites of its core refining assets. Between 2021 and 2024, the focus was on leveraging the unique resource advantages of specific regions, like the natural gas reserves of the Appalachian Basin or the geology of the Midwest for carbon sequestration. Post-2024, the strategy has become asset-centric, concentrating on decarbonization and efficiency upgrades at operational refineries in states like California and North Dakota.

Regional Gas Gluts Offer Feedstock Advantage

The deep price discount for natural gas in basins like the Permian illustrates the type of regional resource opportunity that companies are now moving away from as they narrow focus to existing assets.

(Source: Deloitte)

- The 2021–2024 period was marked by a broad geographic vision. The Heartland Hydrogen Hub spanned North Dakota, Minnesota, Montana, and Wisconsin, while the ARCH 2 hub targeted Ohio, Pennsylvania, and West Virginia. This approach was about creating new energy ecosystems in resource-rich areas.

- The withdrawal from the North Dakota-based Prairie Horizon project in 2024 effectively removed the Upper Midwest as a strategic priority for new hydrogen production. While Marathon remains a member of the ARCH 2 alliance, its lack of new capital commitments suggests its focus has shifted away from the Appalachian region as well.

- Current activities are centered on states where Marathon has major operational assets. The primary focus is the Martinez Renewables facility in California, which aims for a capacity of 730 million gallons per year and is a major hydrogen consumer.

- Other key locations include the Dickinson, North Dakota, renewable diesel plant and the Detroit, Michigan, refinery, where hydrogen is used for hydrotreating. The modernization of a cogeneration plant at an unspecified refinery in October 2025 further reinforces this strategy of upgrading existing infrastructure rather than expanding into new territories.

Technology Strategy Prioritizes Proven Processes Over Pioneering Production

The company’s technological focus has pivoted from exploring emerging clean hydrogen production methods to optimizing commercially mature technologies that support its core business. The earlier strategy involved planning for blue hydrogen production with Carbon Capture and Sequestration (CCS), a technologically complex and capital-intensive process. The current strategy relies on proven hydrotreating technologies and foundational digital tools that enhance the efficiency of existing operations, deferring large-scale investment in novel production technologies until the market matures.

Grey Hydrogen’s Dominance Justifies Caution

The chart’s illustration of grey hydrogen’s 77.5% market dominance in 2025 provides the commercial context for why a company would prioritize proven technologies over pioneering riskier, capital-intensive clean hydrogen production.

(Source: Mordor Intelligence)

- Between 2021 and 2024, the technological frontier was blue hydrogen. The now-canceled Prairie Horizon project was designed to use steam methane reforming coupled with CCS, indicating an exploration of technologies to produce low-carbon fuels for an external market.

- The current technology in active, large-scale deployment is Topsoe’s Hydro Flex™. This is a mature hydrotreating process used at the Martinez Renewables facility to convert bio-feedstocks into renewable diesel, a process that is well-understood and heavily reliant on hydrogen.

- The 2025–2026 period is characterized by the adoption of enabling technologies. The Baker Hughes partnership brings in digital and chemical processing solutions to make existing refinery operations more efficient and ready for future integrations, which is essential for any future CCUS or hydrogen project.

- This pragmatic approach indicates that while the company explored next-generation production technology, it has concluded that the current market and regulatory environment does not support the risk. The focus is now on mastering operational efficiency, a necessary step before undertaking more complex technological ventures like the large-scale integration of CCS. A poor understanding of the underlying factors in the DAC Market 2026: Uncover the New Investment Risks Now could lead to poor capital allocation.

SWOT Analysis of Marathon Petroleum’s Evolving Hydrogen Strategy

The strategic shift from hydrogen market creation to captive consumption has reshaped Marathon Petroleum’s competitive posture, strengthening its financial discipline while potentially ceding ground to more aggressive first-movers in the energy transition. This SWOT analysis examines how the company’s strengths, weaknesses, opportunities, and threats have evolved between the hub-focused era and the current integrated-use strategy.

Table: SWOT Analysis for Marathon Petroleum’s Hydrogen Initiatives

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Large-scale project development capabilities; partnerships with major energy players like TC Energy; access to federal funding initiatives. | Strong capital discipline; expertise in refinery operations and hydrotreating; existing infrastructure for renewable diesel production (Martinez). | The strategy shifted from leveraging project development skills for new markets to optimizing core operational competencies, validating a focus on shareholder returns and risk management. |

| Weaknesses | Exposure to high CAPEX and nascent market risk of hydrogen hubs; dependence on federal subsidies and regulatory clarity (45 V tax credits). | A “follower” posture in the hydrogen economy; slower pace in developing standalone clean energy business lines compared to some European majors or US peers. | The withdrawal from HH 2 H resolved the immediate weakness of high financial exposure but solidified a more conservative, less pioneering role in the energy transition. |

| Opportunities | Become a first-mover in the regional blue hydrogen market; build a new revenue stream from clean hydrogen sales. | Meet growing demand for renewable diesel; leverage the $163 M low-carbon fund for pilot projects; use existing assets to produce blue hydrogen when commercially viable. | The opportunity shifted from creating a new market to dominating a profitable niche (renewable diesel) while preparing for future low-carbon ventures on a smaller, more manageable scale. |

| Threats | Regulatory delays or unfavorable 45 V rules; competition from other hubs; project cancellations due to poor economics. | Competitors establishing dominant positions in green hydrogen supply chains; losing market share in future low-carbon fuels if the pivot to hydrogen accelerates faster than anticipated. | The primary threat transformed from project-specific failure (which materialized) to the long-term strategic risk of being outpaced by more aggressive competitors in the broader energy transition. |

Scenario Modelling: Watch for Pilot Projects and CAPEX Trends

Moving into the second half of the decade, the most critical indicator of Marathon’s hydrogen strategy will be the deployment of its $163 million low-carbon portfolio fund. If the company is serious about blue hydrogen as a future pillar, the next logical step is to sanction a small-scale, commercial pilot project at one of its existing refineries. This would translate its foundational work with partners like Baker Hughes into a tangible asset, testing the integration of hydrogen production and carbon capture in a controlled, de-risked environment.

Future Market Growth Justifies Pilot Projects

The projection of the hydrogen market exceeding $44 billion by 2031 provides the long-term strategic incentive for companies to invest in pilot projects and scenario planning.

(Source: Mordor Intelligence)

- If this happens: The company announces a final investment decision for a small-scale blue hydrogen and CCUS pilot project at a refinery like the one in Martinez, CA or Garyville, LA.

- Watch this: Look for new partnerships specifically for CO₂ transport and sequestration, as this is a critical missing link in their current public-facing strategy. Also, monitor the company’s annual reports for an increase in the percentage of growth capital allocated to low-carbon initiatives beyond the current levels.

- These could be happening: This would signal that Marathon is moving from a passive, capability-building phase to an active, asset-building phase. It validates the “pragmatic follower” strategy, where the company enters the game once technology and regulations are clearer, leveraging its operational expertise to execute more efficiently than early pioneers. The overall 2026 Energy Outlook: Why BESS Beats Offshore Wind Costs suggests a move toward more predictable and cost-effective technologies.

Frequently Asked Questions

Why are oil majors like Marathon Petroleum abandoning hydrogen hub projects despite large federal subsidies?

According to the analysis, oil majors are prioritizing capital discipline and risk mitigation. They are shifting from speculative, large-scale hydrogen hub projects, which face market and regulatory uncertainties, to a more conservative model. This new model focuses on using hydrogen internally (“captive consumption”) for their profitable renewable fuels businesses, which offers more predictable returns and avoids the volatility of building a new energy market from the ground up.

What is Marathon Petroleum’s new hydrogen strategy for 2025-2026?

Marathon’s strategy has shifted to focus on internal or “captive” consumption. Instead of building large plants to sell hydrogen as a commodity, the company is using it as a critical feedstock for its own renewable diesel facilities, like the Martinez Renewables joint venture. This is complemented by building foundational capabilities through targeted partnerships for technology (Baker Hughes) and workforce training (IBOGP), rather than forming large project alliances.

What does the cancellation of the $2 billion Prairie Horizon Hydrogen Project signify?

The cancellation of this project, despite its connection to a potential $925 million federal grant, marks a definitive strategic retreat from large-scale hydrogen production for external markets. It signals a clear preference for capital discipline over speculative, first-mover ventures. The company is instead allocating a smaller, more measured $163 million towards a diversified portfolio of low-carbon technologies, spreading risk rather than concentrating it in a single massive project.

How does Marathon’s current strategy compare to competitors like Phillips 66?

Marathon’s strategy is described as a more cautious, portfolio-based approach. While Phillips 66 pursued a complete facility conversion for renewable fuels at its Rodeo refinery (a concentrated strategy), Marathon is spreading its risk with a smaller, $163 million investment across a mix of technologies including blue hydrogen, CCUS, and renewable fuels. This allows Marathon to maintain optionality without the high upfront costs and regulatory exposure that a single, large-scale conversion entails.

What is the most important indicator to watch for regarding Marathon’s future hydrogen plans?

The most critical indicator will be the deployment of its $163 million low-carbon portfolio fund. Specifically, a final investment decision for a small-scale, commercial blue hydrogen and carbon capture (CCUS) pilot project at one of its existing refineries would be a key signal. This would indicate a move from a passive, capability-building phase to an active, asset-building phase, validating its “pragmatic follower” strategy.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.