Bank of England Monetary Policy, 3.75% Rate Hold, 19.5% Gas Surge, and 4% Inflation Forecast Divergence (2022 to 2026)

Systemic Risk, Bank of England Grapples with Energy Volatility

The Bank of England’s monetary policy is increasingly constrained by energy price volatility, a systemic risk that creates a direct conflict between its 2% inflation target and the need to support economic growth. This dilemma has moved from a crisis response footing seen in 2022 to a state of persistent strategic uncertainty in 2026, where the source of energy shocks has shifted but their economic impact remains a primary constraint on the central bank’s actions.

- In 2022, the initial energy shock following Russia’s invasion of Ukraine drove UK gas futures to extreme peaks above 600 pence per therm, prompting aggressive monetary tightening. In contrast, the period from 2025 to 2026 is defined by renewed, albeit more moderate, volatility. Geopolitical tensions in the Middle East caused the UK’s front-month gas contract to surge by 19.5% in March 2026, demonstrating the economy’s continued vulnerability.

- The transmission of these shocks to the UK economy is rapid. Wholesale price spikes directly feed into consumer costs, with regulator Ofgem announcing that the average price cap would rise to 26.1 pence/k Wh for electricity in July 2026.

- The Bank of England’s principal concern is the potential for these price hikes to trigger “second-round effects, ” where higher business costs and wage demands lead to a persistent wage-price spiral, embedding inflation into the domestic economy and de-anchoring expectations.

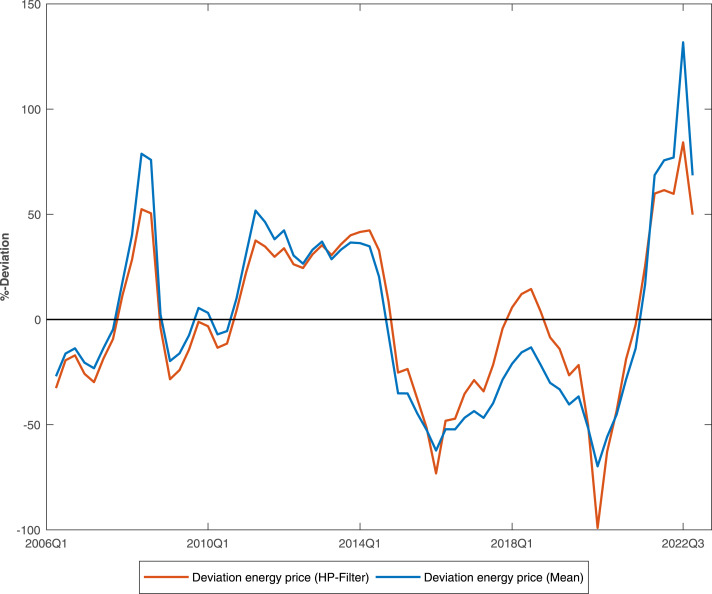

Chart Shows Extreme Energy Price Volatility Since 2006

The section heading’s focus on ‘Energy Volatility’ is directly and visually represented by this chart, providing the context for the systemic risk the Bank of England is grappling with.

(Source: ScienceDirect.com)

£10 B Tax Exposure, UK Government Fiscal Policy Interventions

The UK government has implemented a series of fiscal policies to mitigate the financial impact of energy price shocks, which both support and complicate the Bank of England’s monetary actions. These interventions directly alter the financial landscape for energy producers and consumers, creating a complex policy environment where monetary and fiscal levers can work at cross-purposes.

- To capture “excess profits” driven by gas-linked electricity prices, the government increased the Electricity Generator Levy, a windfall tax on older renewable and nuclear plants, from 45% to 55%, effective July 1, 2026.

- In a move that could affect decarbonization incentives, the Treasury scrapped the Carbon Price Support mechanism in April 2026. This UK-specific top-up to the EU Emissions Trading System price was designed to support investment in low-carbon generation.

- This decision creates new financial risks. Analysis from Energy UK warns that without a carbon price aligned with the EU, UK exporters could face an estimated £10 billion in extra taxes between 2026 and 2035 under the EU’s Carbon Border Adjustment Mechanism (CBAM).

- These fiscal measures, while intended to ease consumer burdens, add another layer of uncertainty to the Bank of England’s forecasting models, affecting assumptions about corporate profitability, investment, and headline inflation. The long-term impact of the stalled Wind Energy 2025 projects further complicates national energy independence goals.

Charts Model Welfare Impact of Fiscal Policy

The section discusses the financial impacts (‘Tax Exposure’) of ‘Fiscal Policy Interventions.’ The chart models the ‘Welfare Impact of Fiscal Policy,’ which is a direct conceptual match for illustrating the consequences of the policies described.

(Source: ScienceDirect.com)

Table: UK Government Energy Policy Interventions and Financial Impacts (2026)

| Policy / Finding | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Electricity Generator Levy | Jul 2026 | Increased the windfall tax on certain low-carbon electricity generators from 45% to 55% to capture profits linked to high gas prices. | BBC |

| CBAM Tax Exposure | May 2026 | Energy UK analysis warns that the lack of an aligned carbon price could expose UK exporters to £10 billion in EU carbon taxes by 2035. | [PDF] Energy UK |

| Carbon Price Support (CPS) | Apr 2026 | The UK Treasury decided to scrap the CPS, a domestic carbon tax floor, altering the financial incentives for power generation. | Gravis Capital |

| Fossil Fuel Subsidies | Feb 2026 | A report from the Coalition of Finance Ministers for Climate Action highlighted that eliminating fossil fuel subsidies could free significant fiscal space for clean energy investment. | [PDF] Finance Ministers for Climate |

European Electricity Prices Show Volatility in 2026

The section focuses on UK energy policy impacts in the specific year ‘2026.’ The chart provides crucial context by showing energy price volatility in ‘2026’ for the broader European market, which heavily influences the UK situation.

(Source: European Central Bank – European Union)

UK vs Europe, Bank of England Policy Amid Global Shocks

The UK’s structural position as a net importer of natural gas makes its economy, and by extension its monetary policy, highly sensitive to geopolitical events and supply chain disruptions originating far beyond its borders. This external vulnerability, a key feature of the 2022 crisis, was starkly demonstrated again in early 2026, confirming that geographic diversification of risk sources does not insulate the UK from price shocks.

- The 2021 to 2024 period was dominated by the fallout from the Russia-Ukraine war, which drove European gas prices to record highs and established the primary inflationary threat. This solidified the link between continental geopolitics and UK household bills.

- By 2026, the focus of risk shifted geographically but the impact remained. Renewed tensions in the Middle East, not Europe, triggered the 19.5% spike in the UK’s front-month gas contract, which immediately lifted European power prices and complicated the inflation outlook. This reflects the interconnectedness of global LNG markets, where a disruption in one region, like that affecting Qatar Energy LNG 2026, affects prices globally.

- The UK’s reliance on natural gas for 30-40% of its electricity generation creates a powerful and direct transmission mechanism from global wholesale markets to the domestic economy, leaving the Bank of England to manage the inflationary consequences of events it cannot control.

UK & EZ Output Prices Track Energy Volatility

This is a perfect match. The section heading explicitly states ‘UK vs Europe,’ and the chart compares ‘UK & EZ (Eurozone)’ output prices, linking them to the ‘Global Shocks’ theme via energy volatility.

(Source: LinkedIn)

Bank of England’s Policy Tools, A Supply-Side Dilemma (2022 to 2026)

The persistent energy crisis has exposed the fundamental limitations of the Bank of England’s primary demand-side policy tool, the Bank Rate, when confronted with a severe and recurring supply-side shock. The shift from decisive tightening in 2022 to deep division in 2026 reflects a growing recognition of the high economic cost and questionable precision of using interest rates to fight this type of inflation.

- In 2022, faced with soaring inflation, the Monetary Policy Committee (MPC) embarked on a path of aggressive and conventional monetary tightening, raising rates to cool aggregate demand.

- By early 2026, this confidence has been replaced by profound uncertainty. The MPC’s decision to hold the Bank Rate at 3.75% passed on a narrow 5-4 vote, with four members favoring a hike to combat persistent inflation. This split reveals a committee grappling with the classic stagflationary dilemma.

- The core problem is that raising interest rates to combat an external supply shock punishes domestic households and businesses already facing a real income squeeze from high energy bills. This risks triggering a sharp economic downturn for a problem originating in international commodity markets.

- The Bank’s increasing reliance on scenario analysis, such as modeling the impact of oil prices remaining above $130 per barrel, signals a move toward contingency planning. It underscores the reduced effectiveness of its traditional policy levers in an environment dominated by external, unpredictable shocks. This uncertainty is compounded by new demand sources, such as those driven by Dominion AI & Data Center Energy 2025, which further complicate long-term energy planning.

Charts Model Monetary Policy’s Role in Taming Inflation

The section is about the effectiveness and challenges of the Bank of England’s ‘Policy Tools.’ The chart, which ‘Models Monetary Policy’s Role in Taming Inflation,’ directly visualizes the mechanisms and outcomes of using these tools.

(Source: Bank for International Settlements)

SWOT Analysis, Bank of England’s Monetary Policy Response

The Bank of England’s response to energy-driven inflation highlights a core strength in its institutional credibility and clear mandate, but it also exposes significant weaknesses in its policy toolset, persistent external threats from global markets, and critical opportunities in coordinating with fiscal and industrial strategy.

Table: SWOT Analysis for UK Monetary Policy

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | Clear 2% inflation target provided a firm mandate for action. The Bo E acted decisively with rate hikes to anchor inflation expectations. | Maintains credibility through transparent communication, publishing MPC minutes and detailed scenario analyses (e.g., April 2026 oil shock models). | The Bank’s transparency about policy trade-offs has become a key strength, managing market expectations amid deep uncertainty. |

| Weaknesses | The blunt nature of the Bank Rate as a demand-side tool became apparent, as it could not address the root supply-side cause of inflation. | The 5-4 MPC vote split in Feb 2026 highlights profound internal division on the correct policy path, revealing the lack of a clear, painless option. | The weakness was validated; the tool is effective at cooling demand but at a high risk of triggering a recession when the problem is external. |

| Opportunities | Government support packages (e.g., Energy Price Guarantee) provided temporary fiscal support, alleviating some pressure on the Bo E. | Coordination with fiscal policy (e.g., Electricity Generator Levy) offers a more targeted way to address windfall profits and consumer pain. Long-term energy strategy to accelerate renewables offers a structural solution. | The opportunity for deeper fiscal-monetary coordination has become more apparent, as monetary policy alone is insufficient. |

| Threats | The primary threat was a single, massive geopolitical shock (Russia-Ukraine war) leading to unprecedented gas price spikes. | The threat has diversified to include broader geopolitical instability (e.g., Middle East tensions in Mar 2026), making shocks less predictable but still potent. The risk of a wage-price spiral remains central. | The threat of energy volatility is validated as a persistent, not transient, feature of the economic environment, constraining policy indefinitely. |

5.25% Peak Rate? Bank of England’s High-Stakes Scenario

The Bank of England’s future policy path hinges critically on whether the early 2026 energy price spike proves temporary, with a hawkish pivot to a Bank Rate as high as 5.25% remaining a tangible risk if second-round inflationary effects become embedded in the economy.

- If this happens: Global energy markets remain volatile due to sustained geopolitical instability, and wholesale prices do not recede as baseline forecasts predict.

- Watch this: The evolution of “second-round effects” will be the decisive factor. The MPC is intensely focused on UK wage growth data and core inflation metrics, which strip out volatile energy and food prices, as the key indicators for whether to tighten policy further.

- These could be happening: The Bank of England could be forced to abandon its cautious hold and implement a series of aggressive rate hikes, aligning with its own stress-test scenario where a prolonged energy shock pushes inflation to 6.2% and requires a peak Bank Rate of 5.25%. The narrow 5-4 vote to hold rates in February 2026 shows the committee is already on a knife’s edge, with a substantial minority believing the conditions for tighter policy have already been met.

UK Bank Rate History Shows Recent Spike

The section questions a potential ‘Peak Rate’ for the Bank of England. The chart showing the ‘UK Bank Rate History’ and its ‘Recent Spike’ provides the essential historical context and visual data to frame this high-stakes scenario discussion.

(Source: LinkedIn)

The questions your competitors are already asking

This report covers one angle of how energy price volatility shapes UK monetary policy. The questions that matter most depend on your work.

- What is actually happening with the Bank of England’s strategy for managing energy price shocks and their ‘second-round effects’?

- What is the outlook for UK inflation and interest rates given the persistent volatility in gas prices?

- How does the Bank of England’s monetary policy (rate changes) compare to the UK government’s fiscal policy for mitigating the impact of energy price shocks?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.