ISO-NE Grid Vulnerability, 4.4 GW Generation Loss, 33, 900 MW Queue Backlog, and FCA 19 Delay (2021 to 2026)

Grid Reliability Risks: ISO-NE 4.4 GW Generation Loss and 33, 900 MW Queue

The retirement of dispatchable thermal generation in New England has structurally outpaced the integration of reliable replacement capacity, shifting grid vulnerability from a forecast risk to an operational reality. Between 2021 and 2024, the grid absorbed the planned closure of major assets, including the Mystic Generating Station in May 2024, culminating a trend that saw over 4, 400 MW of conventional power plants shut down since 2013. This systematic erosion of firm capacity set the stage for the acute reliability challenges that materialized from 2025 onward.

- In the period from 2021 to 2024, the primary concern was the planned loss of firm capacity, with 2, 690 MW retiring in 2022 and another 2, 500 MW in 2023. This was viewed as a future challenge to be managed through market mechanisms and a growing pipeline of clean energy projects.

- From 2025 to today, the risk became acute and immediate. The temporary shutdown of 4.4 GW of gas-fired generation due to fuel supply constraints demonstrated a critical dependency, while a Spring 2026 heatwave forced ISO-NE to rely on up to 8 GW of oil-fired generation, confirming that the new resource mix cannot yet handle system stress.

- The problem is compounded by a severe mismatch in resource attributes. The retiring fleet provided on-demand, weather-resilient power, whereas the 33, 900 MW of generation in the current interconnection queue is dominated by intermittent wind, solar, and short-duration battery storage, which do not offer the same multi-day reliability.

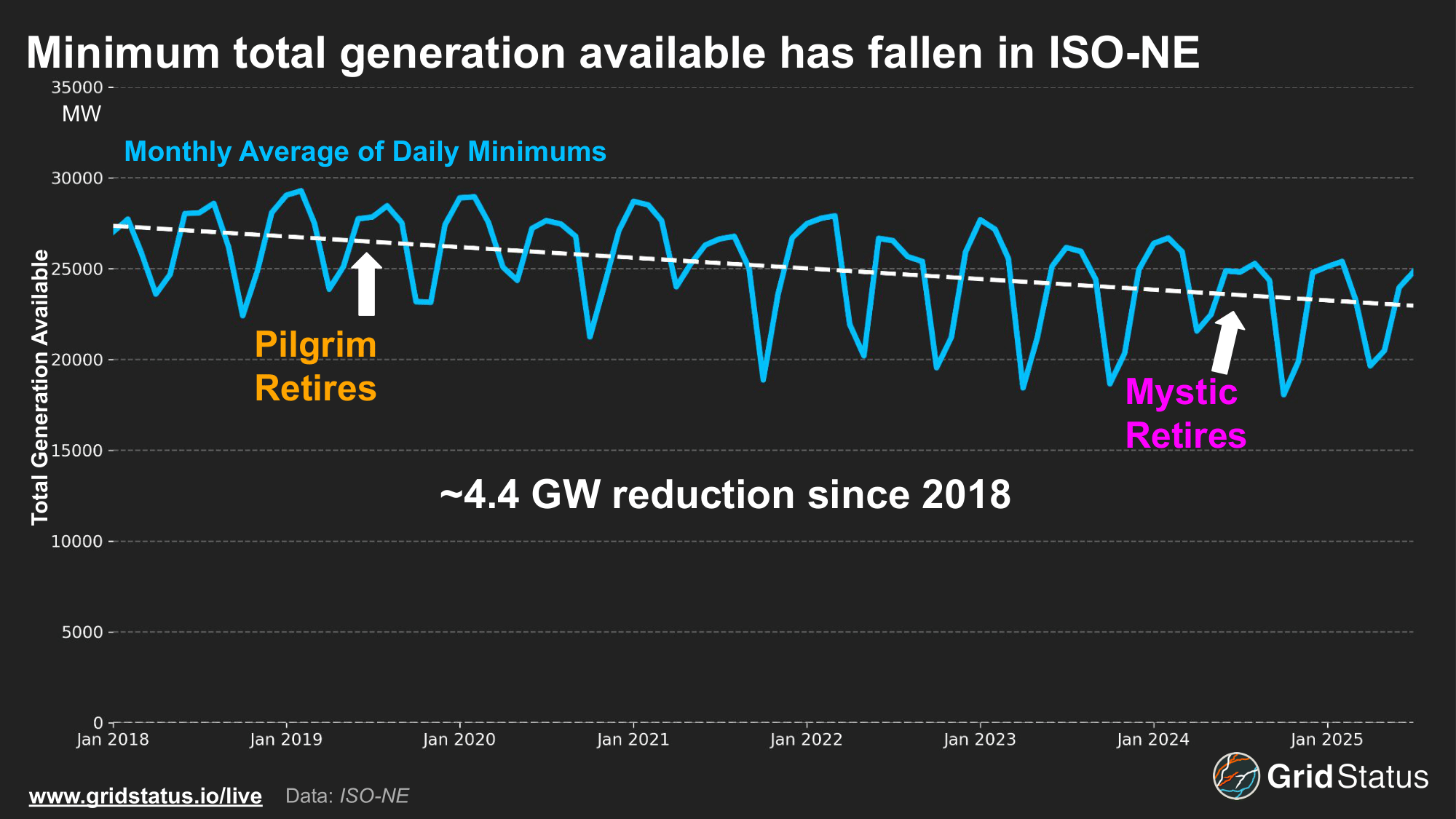

ISO-NE Available Generation Capacity Declines 4.4 GW

The chart directly visualizes the 4.4 GW decline in generation capacity, which is the specific data point and central theme of the section on grid reliability risks.

(Source: Grid Status Exports)

Wholesale Market Volatility: ISO-NE $15 B Market and $441/MWh Price Spikes

Shrinking capacity margins have directly translated into extreme price volatility and significant increases in wholesale electricity costs, exposing consumers and businesses to severe financial risk. While price sensitivity was evident before 2025, the tightening supply-demand balance has since amplified market swings to unsustainable levels, turning weather events and fuel logistics into primary drivers of energy costs.

- The 2022 wholesale electricity market was valued at $16.7 billion, establishing a high baseline for energy costs in the region driven by post-pandemic recovery and global fuel price pressures.

- In January 2025, the consequences of thinning capacity margins became clear as average real-time prices hit $135.08/MWh, a 112% increase compared to the previous year, reflecting the high cost of securing power during winter peak demand.

- The situation escalated further during a February 2026 cold snap, when wholesale prices soared to $441.8/MWh, demonstrating the grid’s extreme vulnerability to fuel constraints. The total wholesale electricity cost for 2025 was $15.0 billion, underscoring that even with slightly lower total costs, periods of extreme pricing are becoming more frequent.

- This volatility was further highlighted on June 24, 2025, when extreme heat triggered a capacity deficiency and forced ISO-NE to declare a “Power Caution, ” dispatching demand response resources to maintain grid stability and avoid more severe outcomes.

Real-Time Prices Show Extreme Market Volatility

This chart’s headline and visual data on price volatility directly correspond to the section’s focus on “Wholesale Market Volatility” and “Price Spikes,” serving as a perfect illustration.

(Source: Grid Status Exports)

Table: ISO-NE Market Volatility Events and Costs

| Event or Period | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Cold Snap Price Spike | Feb, 2026 | Wholesale electricity prices soared to $441.8/MWh during a cold snap, highlighting severe winter fuel security risks and their impact on market costs. | U.S. News & World Report |

| Annual Market Cost | 2025 | The total wholesale cost of electricity in 2025 was $15.0 billion, with an average price of $127/MWh, reflecting sustained high prices due to tight capacity. | ISO Newswire |

| January Price Surge | Jan, 2025 | Average real-time wholesale power prices reached $135.08/MWh, a 112% year-over-year increase, signaling a structural shift in winter supply risk. | ISO Newswire |

| Capacity Deficiency Event | Jun 24, 2025 | Extreme heat triggered a capacity deficiency, forcing ISO-NE into emergency operations and the dispatch of demand response to maintain grid stability. | RTO Insider |

| Annual Market Cost | 2022 | The total value of New England’s wholesale electricity markets was $16.7 billion, setting a high-cost precedent prior to the most recent capacity retirements. | [PDF] ISO New England |

ISO-NE Market Redesign, FCA 19 Delay, and Capacity Auction Reforms

In response to the escalating reliability crisis, ISO-NE has accelerated its shift from incremental adjustments to fundamental market redesigns aimed at properly valuing and procuring firm capacity. The initial, more measured actions of the 2021-2024 period have given way to more urgent and sweeping reforms from 2025 onward, signaling the operator’s recognition that the existing market structure is insufficient for the challenges ahead.

- The first major signal of reform was the decision to seek and receive FERC approval in January 2024 to delay the 19 th Forward Capacity Auction (FCA 19). This was done to implement a new “resource capacity accreditation” process designed to more accurately value the reliability contribution of different resource types.

- By 2025, with reliability risks mounting, ISO-NE escalated its reform efforts by formally proposing a major overhaul known as Capacity Auction Reforms (CAR). This initiative aims to replace the three-year forward auction with a “prompt” seasonal auction held closer to the delivery period, improving forecast accuracy and sending more effective price signals.

- Signaling the urgency of this transition, ISO-NE announced it would pause the Forward Capacity Auction for one full year (for the 2028/2029 period) to implement the new framework. This decisive action underscores the consensus that the old system could not secure the grid’s future.

- Complementing market reforms, physical infrastructure projects like the 1, 200 MW New England Clean Energy Connect (NECEC) transmission line, which was completed and energized in January 2026, represent tangible progress in diversifying the region’s energy supply.

Table: ISO-NE Market Reform Milestones

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Capacity Auction Reforms (CAR) Proposal | Jan, 2026 | ISO-NE proposed a fundamental market overhaul to shift from a three-year forward auction to a “prompt” seasonal auction to improve forecast accuracy and incentivize reliable capacity. | Utility Dive |

| New England Clean Energy Connect (NECEC) Energization | Jan, 2026 | Avangrid completed and energized the 1, 200 MW transmission line, providing a new path for clean energy from Québec to enter the New England grid. | Avangrid |

| Forward Capacity Auction Pause | Mar, 2026 | ISO-NE confirmed its plan to pause the Forward Capacity Auction for one year for the 2028/2029 period to implement the new market framework, signaling the urgency of the reforms. | Competitive Energy Services |

| FERC Approval for FCA 19 Delay | Jan, 2024 | FERC approved a one-year delay to FCA 19, allowing ISO-NE time to develop and implement a more accurate resource capacity accreditation methodology. | Utility Dive |

New England Hotspots: ISO-NE Demand Growth and Generation Retirements

The grid crisis is a region-wide phenomenon, but its drivers and impacts are geographically concentrated, stemming from aggressive state-level electrification policies that are creating new demand centers while localized thermal plant retirements remove critical supply. The collision of these trends has reversed a decade of flat energy use, with forecasts now consistently showing sustained growth that adds another layer of stress to the system.

- During the 2021-2024 period, long-term forecasts began to quantify the impact of electrification. The 2024 CELT report projected a 17% rise in annual energy use by 2033, driven primarily by state policies promoting electric vehicles and heat pumps. This established the expectation of a fundamental shift from a summer-peaking to a winter-peaking system.

- From 2025, the demand-side risk became more complex and uncertain with the formal recognition of a new, high-intensity load from data centers and artificial intelligence (AI) workloads. In May 2026, ISO-NE established a new forecasting framework for these “large loads, ” acknowledging their potential to significantly alter demand projections. The rise of AI compute, supported by companies like NVIDIA, is a factor that organizations like Oklo are planning to power.

- Demand growth varies by state, with forecasts projecting peak demand in Massachusetts to exceed 12, 500 MW, while Maine and Vermont show the highest growth rates. This uneven growth puts localized stress on transmission infrastructure.

- The retirement of the Mystic Generating Station near Boston in 2024 is a key example of geographic vulnerability, removing a major source of local capacity and increasing the area’s reliance on transmission to import power, a dependency that advanced gas turbine technology from firms like Baker Hughes could help mitigate.

Technology Mismatch: ISO-NE Reliance on Short-Duration BESS and Intermittent Renewables

While New England’s pipeline of new generation projects is substantial, its composition reveals a critical mismatch between the attributes of incoming resources and the reliability needs of the evolving grid. The system is swapping thermal assets capable of multi-day operation for a portfolio of intermittent renewables and short-duration energy storage, creating a new form of vulnerability during prolonged periods of challenging weather.

- Between 2021 and 2024, the composition of the interconnection queue shifted dramatically toward energy storage. As of August 2021, storage represented just 15% of proposed capacity. By March 2024, this figure had surged to 46%, reflecting developer response to market signals and policy incentives.

- This trend continued into 2026, with the queue dominated by wind, solar, and battery storage. As of January 2026, battery storage accounted for 46% (17, 700 MW) and wind for 44% (16, 928 MW) of the 38.5 GW of proposed capacity.

- The problem is that the vast majority of this proposed storage is lithium-ion technology with 1- to 4-hour discharge durations. While effective for daily peak shaving and managing solar intermittency, these systems cannot replace the multi-day energy security provided by a retiring coal or nuclear plant with on-site fuel, a gap exposed during winter cold snaps or low-wind periods.

- The operational impact of this mismatch was seen in Spring 2026, when pipeline maintenance on natural gas systems forced ISO-NE to call on oil-fired generation to meet demand during a heatwave. This event demonstrated that despite the massive queue of renewables and storage, the system still lacks sufficient non-gas, dispatchable capacity for all conditions.

Energy Prices Spike As Solar Generation Drops

This chart provides a specific example of the “Technology Mismatch” described in the section by showing how price spikes are linked to the intermittency of renewable sources like solar.

(Source: Grid Status Exports)

SWOT Analysis: ISO-NE Grid Vulnerability and Market Reforms

ISO-NE’s proactive planning and detailed market monitoring provide a strong foundation for managing the energy transition, but these strengths are being severely tested by the accelerating pace of thermal plant retirements and rapid, policy-driven demand growth. The resulting vulnerability has created a critical opportunity for new technologies and market participants that can provide firm, dispatchable capacity, but their success hinges on the timely implementation and effectiveness of ambitious market reforms.

Table: SWOT Analysis for ISO-NE Grid Vulnerability

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Proactive long-term planning (2050 Transmission Study); detailed market monitoring and reporting; established processes for stakeholder engagement. | Demonstrated ability to execute complex market changes (FCA 19 delay); maintaining system reliability through initial stress events (June 2025 capacity caution). | The crisis validated the need for the proactive planning ISO-NE was already doing, forcing regulators and stakeholders to accelerate their acceptance of proposed reforms. |

| Weaknesses | Heavy reliance on natural gas with known pipeline constraints; a slow, “first-come, first-served” interconnection process creating backlogs. | Inability of the existing resource mix to handle stress without relying on oil; insufficient firm capacity to manage fuel supply disruptions (4.4 GW gas shutdown). | The weakness of gas dependency, long a theoretical risk, was validated as an acute operational vulnerability with real-world consequences and price spikes. |

| Opportunities | Growing queue of renewables and storage; state-level clean energy mandates creating demand for new projects; development of resource accreditation reforms. | Fundamental capacity market redesign (CAR) to properly value reliability; new transmission (NECEC) coming online; falling costs of battery storage. | The opportunity shifted from accommodating renewables to actively procuring reliability. The market redesign (CAR) is a direct attempt to create a robust market for this attribute. |

| Threats | Pace of thermal retirements outpacing replacements; forecasted demand growth from electrification; potential for winter fuel shortages. | Extreme price volatility ($441/MWh spikes); delays to critical projects (Revolution Wind); new, uncertain load from data centers and AI. | Threats moved from being long-term and forecast-based to being immediate and operational. The risk of project delays became a direct threat to near-term grid reliability. |

ISO-NE 2026 Outlook: Winter Reliability and Capacity Auction Reform

The single most critical factor for ISO-NE over the next 12 to 18 months is whether its capacity market reforms can be implemented swiftly and effectively enough to incentivize the required investment in firm capacity to navigate a severe winter without a major reliability event. The success or failure of the first “prompt” seasonal auction will be a determinative signal for the region’s energy future.

- If this happens: The new seasonal capacity auction, part of the CAR framework, clears at a price that is high enough to spur investment in new firm resources, such as long-duration storage, flexible gas peakers, or hybrid renewable-plus-storage projects. This would signal that the market-based solution is working.

- Watch this: The rate of new interconnection requests specifically for firm, dispatchable capacity following the finalization of the CAR design. Also, monitor the clearing price and procured volumes in the first prompt auction as the most direct indicator of market confidence.

- These could be happening: A mild 2026-2027 winter could mask the underlying structural deficit and reduce the urgency for action, creating a false sense of security. Conversely, a severe winter could force ISO-NE into emergency actions, potentially leading to political intervention that prioritizes short-term price suppression over long-term reliability investment.

The questions your competitors are already asking

This report covers one angle of New England’s growing grid reliability crisis. The questions that matter most depend on your work.

- What is actually happening with ISO-NE’s Forward Capacity Auction 19 (FCA 19) since the delay?

- What is the outlook for deploying dispatchable capacity in New England to replace the 4.4 GW of retired thermal generation?

- What are the market opportunities for energy storage and other firm, low-carbon technologies to solve ISO-NE’s reliability gap?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.