Data Center Power 2026: PEM Fuel Cells Face a Two-Front War

The convergence of artificial intelligence power demands and grid instability is forcing a strategic reassessment of data center energy infrastructure. While Proton Exchange Membrane (PEM) fuel cells have been validated for zero-emission backup power, they face a two-front challenge for market dominance. The first is the entrenched position of Solid Oxide Fuel Cell (SOFC) technology for prime power, and the second is a critical dependency on a nascent and politically vulnerable green hydrogen supply chain. The market is consequently splitting into two distinct segments: SOFCs for baseload power and PEMs for diesel generator replacement.

Industry Adoption: PEM Fuel Cell Projects Pivot to Backup Power

Commercial activity shows a clear divergence in fuel cell application, with PEM technology solidifying its role as a diesel generator replacement while SOFC technology captures the larger-scale prime power market. This split reflects the distinct technical and economic strengths of each system, shaping investment and deployment strategies across the data center sector.

- Between 2021 and 2024, PEM adoption was characterized by foundational, megawatt-scale pilot projects. Key demonstrations included a 3 MW system from Plug Power and a 1.5 MW system from Caterpillar and Ballard Power Systems, both with Microsoft. These tests successfully validated PEM technology for long-duration backup, meeting the critical 48-hour runtime requirement.

- The period from 2025 to today reveals a strategic pivot. While PEM developers focus on the backup niche, Bloom Energy, an SOFC provider, secured a monumental $5 billion partnership with Brookfield in October 2025 to provide primary power for AI data centers. This deal underscores the market’s confidence in SOFCs for continuous, baseload electricity.

- In response, PEM companies are optimizing their strategy. In February 2026, Plug Power executed a $132.5 million sale of a hydrogen site to Stream Data Centers. This move signals a deliberate focus on supplying the data center backup market and leveraging its hydrogen production capabilities to support that specific application.

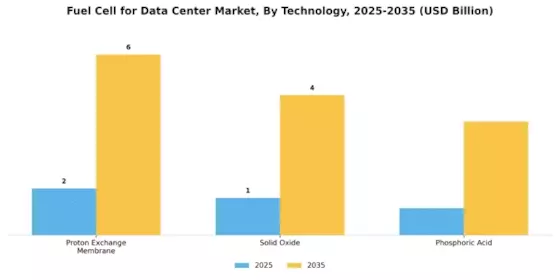

PEM to Lead Data Center Market

This chart shows the projected market growth for both PEM and SOFC technologies, directly illustrating the divergence in adoption within the data center sector.

(Source: Market Research Future)

Investment: Billions Flow into Both Fuel Cell Tech and Hydrogen Supply

Recent major investments highlight the dual tracks of market development, with significant capital flowing into both mature, fuel-flexible SOFC technology for immediate deployment and the enabling green hydrogen infrastructure required for PEM fuel cells to scale. This bifurcated investment pattern confirms that investors see separate, viable markets for prime and backup power solutions.

Data Center Fuel Cell Market Soars

This forecast for the data center fuel cell market to exceed $13 billion visually supports the section’s theme of major capital investment flowing into the ecosystem.

(Source: Market Research Future)

- The largest single investment is the October 2025 strategic partnership between Bloom Energy and Brookfield, valued at up to $5 billion. This capital is dedicated to deploying SOFC systems for primary data center power, leveraging their ability to run on natural gas today and hydrogen in the future.

- In contrast, the most significant funding for the PEM ecosystem is the $1.66 billion conditional loan guarantee issued by the U.S. Department of Energy to Plug Power in July 2025. This funding is not for fuel cell manufacturing but for building up to six green hydrogen production facilities, directly addressing the primary bottleneck for PEM adoption.

- European investment is also materializing, though at a smaller scale. The Mi Na Mi Project, with a €7 million budget, was launched in October 2025 to develop Europe’s first megawatt-scale stationary PEM fuel cell, with participation from companies like Power Cell Group.

Table: Major Investments in Data Center Fuel Cell Ecosystem (2025-2026)

| Company / Funder | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Plug Power | Feb 2026 | Executed a $132.5 million asset sale to Stream Data Centers as part of a larger $275 million infrastructure optimization initiative to sharpen its focus on the data center market. | Fuel Cells Works |

| Bloom Energy / Brookfield | Oct 2025 | Announced a strategic partnership valued at up to $5 billion to deploy Bloom Energy’s SOFC technology to provide primary power for global AI-focused data centers. | Fuel Cells Works |

| Power Cell Group / EU | Oct 2025 | Participating in the €7 million Mi Na Mi Project, an EU-funded initiative to develop and validate the first European MW-scale stationary PEM fuel cell. | Fuel Cells Works |

| Plug Power / U.S. DOE | Jul 2025 | Secured a $1.66 billion conditional loan guarantee to develop up to six green hydrogen production facilities, crucial for fueling its stationary PEM systems. | Carbon Credits |

Geography: United States Emerges as the Primary Arena for PEM Fuel Cell Adoption

The United States is the clear epicenter of PEM fuel cell development and deployment for data centers, driven by a combination of hyperscale operator demand, federal policy support, and a concentration of key technology providers. While activity is present elsewhere, the scale of U.S. projects and investments positions it as the definitive market leader.

North America Dominates Market

This chart directly validates the section’s claim by showing North America as the dominant regional market for data center fuel cells.

(Source: Market Research Future)

- From 2021 to 2024, foundational U.S.-based projects set the stage, such as the Microsoft and Caterpillar demonstration in Wyoming. These early-phase pilots were instrumental in proving the technology’s viability in a real-world data center environment.

- The period from 2025 to 2026 has solidified U.S. leadership through massive federal backing. The $1.66 billion DOE loan guarantee for Plug Power aims to build a domestic green hydrogen network, directly addressing the fuel supply challenge for PEMs within the U.S.

- Europe is an emerging secondary market, indicated by the Mi Na Mi project. However, its scale remains significantly smaller than the multi-billion-dollar initiatives underway in the U.S., which are shaped by major corporate actors and substantial public funding programs like the Inflation Reduction Act. The energy crisis spurred by geopolitical events like a potential US-Iran conflict could accelerate European adoption of alternative power sources.

Technology Maturity: PEM Fuel Cells Validated for Megawatt Backup Power

PEM fuel cell technology has successfully transitioned from small-scale applications to being validated for megawatt-class data center backup, a critical step toward commercialization. However, SOFC technology remains the more mature and preferred option for prime power, establishing a clear technological divide based on application.

Stationary PEM Market to Triple

The projected tripling of the stationary PEM market visually represents the technology’s maturation and successful validation for commercial backup power applications.

(Source: Fortune Business Insights)

- The 2021-2024 period was defined by proving technical feasibility at scale. Until then, PEMs were primarily used in smaller applications. The successful tests of 1.5 MW and 3 MW systems by companies like Ballard and Plug Power with Microsoft marked a major validation point, demonstrating they could replace diesel generators for mission-critical backup.

- From 2025 onward, the focus has shifted to commercial readiness and market positioning. Ballard’s partnership with Vertiv aims to create a cost-effective, integrated backup power product. This signals a move from one-off demonstrations to developing standardized, sellable solutions.

- In contrast, SOFC technology, exemplified by Bloom Energy’s over 400 MW of existing data center installations, is already commercially mature for prime power. Its key advantage is fuel flexibility, allowing it to use the existing natural gas grid while offering a path to hydrogen. This gives it an incumbency advantage that PEM technology, reliant solely on hydrogen, struggles to overcome for baseload applications.

SWOT Analysis: PEM Fuel Cells Poised for Backup but Face Hydrogen Headwinds

The strategic position of PEM fuel cells is defined by their technical suitability for backup power, which is both an opportunity and a constraint. While they offer a zero-emission alternative to diesel, their dependence on hydrogen and competition from mature SOFCs for prime power creates significant market challenges. The viability of the entire PEM data center business model hinges on political support for hydrogen subsidies.

SOFC Leads Stationary Power Market

This chart visualizes the competitive landscape mentioned in the SWOT analysis, showing SOFC’s current market leadership over PEM in stationary power.

(Source: EnkiAI)

Table: SWOT Analysis for PEM Fuel Cells in Data Centers

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Demonstrated rapid start-up capability in pilot projects; zero on-site emissions. | Validated rapid start-up and long-duration (48-hour) performance in MW-scale tests (Microsoft/Ballard). Modular nature offers deployment flexibility. | The technology’s suitability as a direct, zero-emission replacement for diesel backup generators was validated at hyperscale, moving from concept to proven application. |

| Weaknesses | High LCOE; dependency on non-existent high-purity hydrogen infrastructure; lower electrical efficiency (~50-60%) than SOFCs. | Hydrogen infrastructure remains a primary bottleneck. High CAPEX (~$1, 800/k W for backup) is still a barrier compared to incumbent diesel. | The weakness was not resolved but instead circumvented by focusing on the backup market where start-up time is more critical than efficiency, and by seeking subsidies to offset hydrogen costs. |

| Opportunities | Growing demand for clean backup power to meet corporate ESG goals; replacement of aging diesel generator fleets. | The Inflation Reduction Act’s 45 V tax credit (up to $3.00/kg) makes green hydrogen economically feasible. AI-driven power demand creates urgency for grid-independent power sources. | The 45 V tax credit became the central economic enabler for the entire PEM-for-data-center business case, transforming it from a niche solution to a potentially cost-competitive one. |

| Threats | Competition from established SOFC providers like Bloom Energy for prime power; low cost of diesel generators. | SOFC dominance solidified by Bloom Energy’s $5 billion partnership. Political risk to the 45 V tax credit, with proposed legislation threatening to repeal it and jeopardize 75% of the U.S. green hydrogen pipeline. | The threat from SOFCs intensified from competition to market dominance in the prime power segment. The economic viability of PEMs became directly tied to a politically contentious subsidy. This highlights how political shifts redefine investment risk. |

Scenario Modelling: 45 V Tax Credit is the Single Point of Failure for PEM Data Center Strategy

The future of PEM fuel cells in the data center market is almost entirely dependent on the continuation of the Section 45 V clean hydrogen production tax credit. If this subsidy is repealed or significantly reduced, the economic foundation for using PEMs in data centers will collapse, as the cost of green hydrogen would become prohibitive compared to alternatives.

PEM Market’s $16B Potential

This forecast highlights the significant multi-billion dollar market at stake, effectively illustrating the scale of the risk discussed in the scenario modeling.

(Source: Precedence Research)

- If this happens: If the 45 V tax credit is rescinded, as proposed in some legislation, the LCOE for PEM systems will become uncompetitive against both natural gas-powered SOFCs and traditional diesel generators.

- Watch this: The primary signal to monitor is any legislative action in the U.S. Congress concerning the Inflation Reduction Act and specifically the 45 V tax credit. The outcome of upcoming elections will be a leading indicator of this policy’s stability.

- These could be happening: In a scenario where the 45 V credit is lost, expect PEM-focused companies like Plug Power and Ballard to pivot their stationary power strategy away from the U.S. data center market toward regions with more stable and favorable subsidy regimes, such as the EU. Alternatively, they would be forced to double down on their traditional mobility markets, largely abandoning the stationary power segment until hydrogen costs fall organically, a distant prospect. This could be a significant shock to the global energy transition narrative.

Frequently Asked Questions

What is the main difference between how PEM and SOFC fuel cells are being used in data centers?

The market is splitting into two segments. Solid Oxide Fuel Cells (SOFCs), like those from Bloom Energy, are being adopted for continuous prime or baseload power due to their maturity and fuel flexibility (they can run on natural gas now). Proton Exchange Membrane (PEM) fuel cells are solidifying their role as a zero-emission replacement for diesel backup generators, valued for their rapid start-up times.

What is the biggest risk to the adoption of PEM fuel cells for data center backup power?

The biggest risk is the dependency on a nascent green hydrogen supply chain. The economic viability of this supply chain currently hinges almost entirely on the U.S. Inflation Reduction Act’s 45V tax credit. If this subsidy is repealed or reduced, the cost of green hydrogen would become prohibitive, collapsing the business case for PEMs in data centers.

Which companies are mentioned as leaders in this market?

For SOFCs, Bloom Energy is identified as the dominant leader for prime power, highlighted by a $5 billion partnership with Brookfield. For PEMs, Plug Power and Ballard Power Systems are the key players, having conducted major pilot projects with Microsoft and now focusing on the backup power market.

Why is the United States the primary market for this technology?

The U.S. is the epicenter due to a combination of factors: high demand from hyperscale data center operators like Microsoft, a concentration of key technology providers (Plug Power, Bloom Energy), and significant federal support. This support includes the $1.66 billion DOE loan to Plug Power to build hydrogen production facilities and the crucial 45V tax credit for green hydrogen.

Have PEM fuel cells been proven to work for data center backup?

Yes, the article states that PEM technology has been validated for megawatt-scale, long-duration backup. Pilot projects between 2021 and 2024, such as the 3 MW Plug Power system and the 1.5 MW Caterpillar/Ballard system with Microsoft, successfully demonstrated their ability to meet critical 48-hour runtime requirements, proving them a viable replacement for diesel generators.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.