PEM Fuel Cells for Rail 2026: From Pilot to Procurement, Tracking Commercial Scale-Up

Rail Decarbonization: PEM Fuel Cell Adoption Shifts from Pilots to Commercial Fleet Orders

The adoption of Proton Exchange Membrane (PEM) fuel cells in the railroad sector has decisively transitioned from small-scale pilots between 2021-2024 to significant, commercial-scale procurement since early 2025. This shift is driven by major orders that validate the technology for both passenger transport and demanding heavy-haul freight applications, confirming its role as a primary solution for decarbonizing non-electrified rail lines.

- Prior to 2024, the market was defined by pioneering but limited demonstrations, such as Alstom’s Coradia i Lint passenger trains in Germany and the FCH 2 Rail project in Spain, which focused on proving technical feasibility.

- A definitive turning point occurred in late 2024 and 2025, marked by substantial fleet orders. The Canadian Pacific Kansas City (CPKC) order for 98 PEM fuel cell engines from Ballard Power Systems represents the first major commercial commitment to decarbonizing heavy-haul freight in North America.

- In the passenger segment, Siemens Mobility’s initial order for modules to power 7 Mireo Plus H trains, along with a Letter of Intent for up to 200 additional modules, signals a long-term strategic shift by a major Original Equipment Manufacturer (OEM).

- Since 2025, the market has diversified beyond a single application. Projects now span shunting locomotives (PESA SM 42-6 Dn in Sweden), regional passenger service (Siemens in Germany), and high-power freight retrofits (Sierra Northern Railway in California), demonstrating the technology’s flexibility and broad market acceptance.

Hydrogen Train Market Poised for Major Growth

This forecast validates the shift from pilots to commercial orders, projecting the global hydrogen train market will reach over $26 billion by 2035.

(Source: Allied Market Research)

Hydrogen Rail Investment: Multi-Unit Orders Signal Long-Term Financial Commitment

Financial commitment in the hydrogen rail sector has evolved from funding for single-unit demonstrations before 2024 to multi-million dollar procurement contracts for fleet expansions. This change indicates a de-risking of the technology and a move towards long-term capital allocation by major railway operators, driven by confidence in the operational and economic case for PEM fuel cells.

- The CPKC order for 98 fuel cell engines represents a substantial private capital investment in decarbonizing its freight operations, moving the sector beyond reliance on government-funded pilots.

- Siemens Mobility’s framework agreement with Ballard, including an LOI for 200 modules, establishes a predictable, long-term revenue pipeline that justifies supplier-side investment in expanded manufacturing capacity.

- Projects launched since 2025, such as the SERA locomotive conversion in California (1.5 MW order) and the PESA passenger train launch in Poland, show a clear progression to commercial service, underscoring that operators are now purchasing assets for revenue-generating routes, not just for testing.

- Government incentives like the U.S. Inflation Reduction Act’s (IRA) 45 V tax credit, providing up to $3.00 per kilogram for clean hydrogen, directly improve the economic model and are a key enabler for these large-scale capital commitments.

Table: Key Commercial Commitments in PEMFC Rail (2022-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Canadian Pacific Kansas City (CPKC) | Dec 2024 | Order for 98 Ballard PEM fuel cell engines to significantly expand its hydrogen locomotive program, marking a major commercial-scale commitment for freight. | Fuel Cells Works |

| SERA (new company) | Jun 2025 | New order for 1.5 MW of fuel cell engines (12 units) from Ballard to convert three diesel locomotives for zero-emission operation in California. | Ballard Power Systems |

| PESA | Oct 2025 | Launched the first hydrogen-powered passenger train on regular routes in Poland, utilizing Ballard engines and moving from pilot to active service. | Ballard Power Systems |

| Siemens Mobility | Sep 2022 | Initial order for 14 fuel cell modules for 7 trains, plus a Letter of Intent for up to 200 additional modules, securing a long-term supply chain for its Mireo Plus H platform. | Newswire |

Strategic Alliances Solidify PEM Fuel Cell Supply Chains for Rail

Strategic partnerships have matured from technology co-development before 2024 to solidified supplier-integrator relationships post-2025. Rolling stock OEMs and operators are now locking in their PEMFC supply chains to secure proven technology, mitigate supply risk, and accelerate their entry into the hydrogen rail market.

- The alliance between Ballard and Siemens Mobility for the Mireo Plus H platform is a definitive example, where a global OEM leverages a specialist’s proven fuel cell modules to fast-track a flagship hydrogen product line and offer it to the market at scale.

- In the U.S., the partnership between Wabtec and General Motors establishes a powerful domestic competitor. This collaboration combines GM’s HYDROTEC fuel cell technology with Wabtec’s deep expertise in locomotive manufacturing to develop a fully integrated American solution.

- Ballard’s ongoing work with PESA in Poland demonstrates how technology suppliers are enabling regional manufacturers to develop and launch their own hydrogen-powered rolling stock, fostering a competitive and diverse European market.

- The memorandum of understanding between Ballard and India’s Adani Group, announced in 2022, shows a strategic intent to establish local manufacturing in emerging high-growth markets, localizing the supply chain for future demand.

Table: Notable PEMFC Rail Partnerships and Alliances

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Ballard / PESA | 2023 – 2025 | Supplier-OEM partnership. Ballard provides PEM fuel cells (e.g., 2 x 85 k W modules) for PESA’s new-build shunter and passenger locomotives in Poland and Sweden. | Ballard Power Systems |

| Ballard / Siemens Mobility | 2022 | Long-term supply agreement for Ballard to provide fuel cell modules for the Siemens Mireo Plus H train platform, locking in a key technology for a major OEM. | Newswire |

| Wabtec / General Motors | 2021 | Development partnership to commercialize GM’s HYDROTEC fuel cell systems and Ultium batteries for Wabtec’s locomotive platforms in North America. | Federal Railroad Administration |

| Ballard / Adani Group | 2022 | Mo U to evaluate a collaboration for fuel cell manufacturing in India, aiming to serve the Indian market for rail and other heavy-duty transport. | Adani Group |

Global Hydrogen Rail Market: North America and Europe Lead Commercial Deployments

While Europe pioneered early passenger train pilots between 2021 and 2024, North America has since emerged as the clear leader in large-scale, heavy-haul freight applications. This geographical divergence highlights different regional priorities, with Europe focusing on replacing diesel on regional passenger lines and North America targeting the more challenging decarbonization of its core freight corridors.

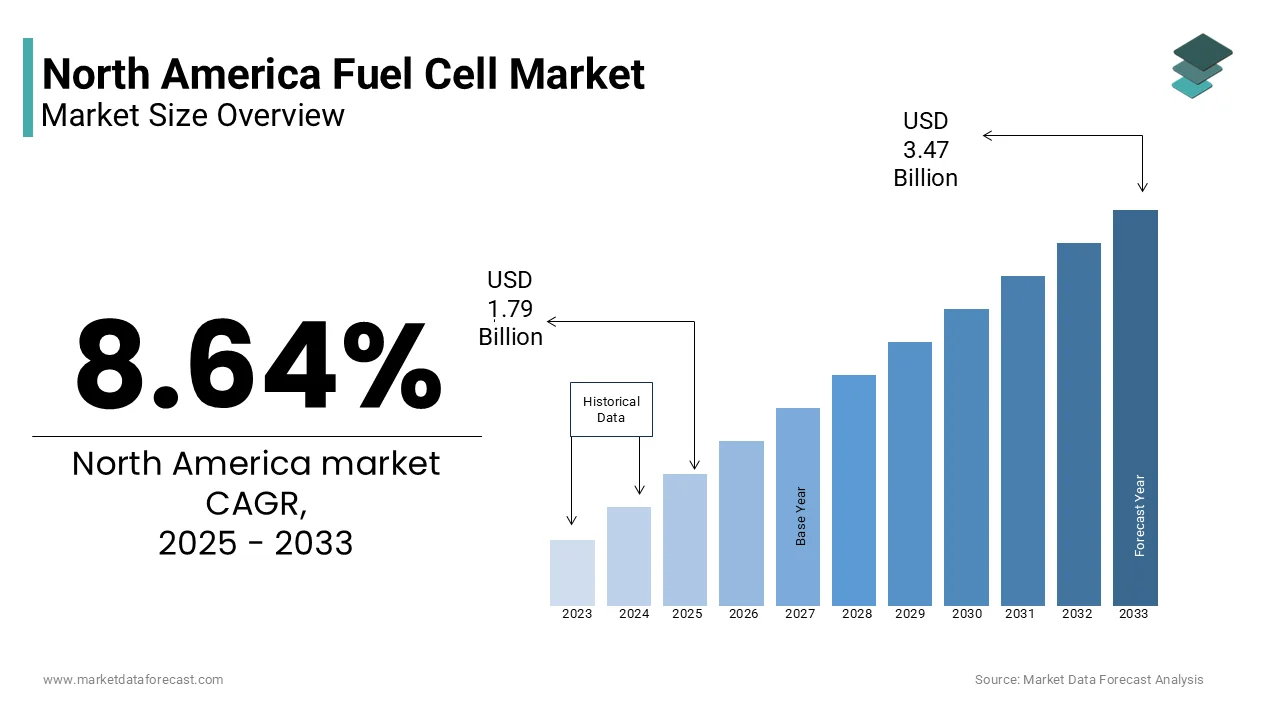

North American Market Drives Fuel Cell Expansion

This chart quantifies North America’s market leadership discussed in the section, forecasting regional growth to nearly $3.5 billion by 2033.

(Source: Market Data Forecast)

- Europe (Germany, Poland): Led early adoption with projects like the Alstom Coradia i Lint and continues to scale passenger services with the Siemens Mireo Plus H fleet in Brandenburg, set for operation in late 2024. The region’s strategy centers on deploying zero-emission solutions on non-electrified secondary lines.

- North America (USA, Canada): Has taken the lead in the freight sector, which has a larger emissions footprint. The CPKC program in Canada and the Sierra Northern Railway project in California, both using Ballard technology, represent the world’s most significant commitments to hydrogen-powered freight.

- Asia (India, China): India is a critical emerging market, rapidly advancing from announcing pilot projects to commencing trials in April 2025 of a powerful domestically manufactured 1200 HP hydrogen train. China’s inclusion of PEMFC transport in its national pilot projects also signals strong state-level support for future deployments.

PEM Fuel Cell Technology: Validated for Rail and Shifting to Industrial Scale

PEM fuel cell technology for rail applications has advanced from a state of technical validation in pre-2024 pilots to a commercially mature solution. The industry’s focus has now shifted from proving basic performance to demonstrating the long-term durability, reliability, and total cost of ownership required for full-scale industrial deployment.

How a PEM Fuel Cell Generates Electricity

This diagram illustrates the core electrochemical process, supporting the section’s discussion of the technology’s validation for rail applications.

(Source: Urban Transport Magazine –)

- Between 2021-2024, projects like the FCH 2 Rail demonstrator using Toyota fuel cells were critical for proving the feasibility of retrofitting existing train fleets with hybrid hydrogen-electric systems.

- Since 2025, deployments like the PESA shunter and passenger trains have moved into regular commercial service, validating the technology’s operational readiness in real-world conditions with fare-paying passengers and industrial customers.

- The primary challenge is no longer if the technology works, but scaling production of proven modules like Ballard’s FCmove®-HD+ and ensuring they meet the demanding 20, 000-30, 000 hour operational lifetimes required by rail operators with minimal degradation.

- The power output per locomotive is scaling significantly to meet different operational needs. Systems have progressed from 170 k W configurations in shunters to powerful 400 k W systems for freight and multi-megawatt configurations required for line-haul locomotives.

SWOT Analysis: PEM Fuel Cells for Rail in 2026

The primary strength of PEM fuel cells in rail is their proven zero-emission performance in demanding, heavy-duty applications. However, the market’s key challenge is shifting from resolving technology risk to addressing the systemic weaknesses of hydrogen infrastructure and manufacturing scale needed to support widespread adoption.

- Strengths have been validated as the technology’s high power density and operational flexibility are now proven in commercial freight and passenger projects.

- The main Weakness has shifted from technology risk to the logistical bottleneck of an undeveloped hydrogen production and refueling infrastructure.

- Opportunities have been amplified by strong government incentives like the IRA, which directly improve the economic viability of large-scale projects.

- Threats are evolving from competition with alternative technologies to intensified market competition from industrial giants entering the fuel cell space.

Table: SWOT Analysis for PEM Fuel Cells in Rail Applications

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | High power density and fast refueling were theoretical advantages over batteries. Focus on lower-power passenger train demos (e.g., Alstom Coradia i Lint). | Demonstrated high-power performance (400 k W+ systems) in heavy-haul freight (CPKC, Sierra Northern). Rapid start-up proven suitable for shunting (PESA). | The technology’s core advantages have been validated in real-world, revenue-generating heavy-duty applications, not just passenger pilots. |

| Weaknesses | Perceived technology risk and lack of long-term operational data were the primary barriers to adoption. High upfront cost of fuel cell systems. | The hydrogen production and refueling infrastructure gap is now the primary bottleneck holding back wider deployment. Total cost of ownership remains a key concern. | The risk has shifted from the fuel cell technology itself to the external ecosystem (i.e., hydrogen supply chain and cost). |

| Opportunities | General decarbonization mandates and climate targets created market interest. Most projects were government-funded pilots. | Specific, high-value government incentives like the U.S. IRA’s 45 V credit (up to $3/kg H 2) make green hydrogen cost-competitive and directly enable commercial projects. | The opportunity moved from policy-driven exploration to economically-driven procurement, creating a tangible business case. |

| Threats | Competition primarily from battery-electric trains on routes where catenary expansion was feasible. | Industrial giants like Cummins and the Wabtec/GM partnership are entering the market, intensifying competition for early movers like Ballard. | The primary competitive threat is evolving from alternative technologies (battery vs. hydrogen) to increased competition within the fuel cell market itself as it matures. |

2026 Outlook: Scaling Manufacturing and Infrastructure is the Next Hurdle

With PEM fuel cell technology now commercially validated for diverse rail applications, the critical growth trajectory for 2026 and beyond depends on the supply chain’s ability to scale manufacturing and the parallel build-out of reliable, cost-effective green hydrogen infrastructure.

Key Components Underpin Fuel Cell Manufacturing Scale-Up

This diagram aligns with the outlook on manufacturing by showing the critical components, like Bipolar Plates and MEAs, that form the basis of the supply chain.

(Source: PR Newswire)

- If this happens: Major fuel cell suppliers like Ballard, Cummins, and the Wabtec/GM venture announce new, dedicated high-volume manufacturing facilities for heavy-duty modules. This would be a strong signal that the supply side is ready to meet projected fleet-scale demand.

- Watch this: The operational data (uptime, reliability, total cost of ownership) from the first large fleets, particularly the CPKC freight locomotives and Siemens passenger trains. Positive results will trigger follow-on orders and accelerate wider industry adoption.

- These could be happening: Energy majors and infrastructure funds announcing large-scale green hydrogen production hubs co-located with major rail freight corridors or maintenance depots. This would solve the “chicken-and-egg” problem and de-risk fuel supply for operators.

- Gaining Traction: The retrofit market for existing diesel locomotives is a key trend to watch. Projects by SERA and CPKC show this is a capital-efficient pathway to decarbonization, allowing operators to leverage existing assets rather than procuring entirely new rolling stock.

Frequently Asked Questions

What is the biggest change in the hydrogen rail market since 2024?

The market has decisively shifted from small, experimental pilot projects to significant, commercial-scale procurement by major rail operators. This is highlighted by large fleet orders like Canadian Pacific Kansas City’s (CPKC) order for 98 fuel cell engines and Siemens Mobility’s long-term agreement for its passenger trains, indicating that the technology is now being purchased for revenue-generating services.

Is PEM fuel cell technology proven for different types of trains?

Yes, the technology’s flexibility has been validated across a diverse range of rail applications. As of 2025, successful commercial projects include high-power heavy-haul freight (CPKC), regional passenger service (Siemens Mireo Plus H), and shunting locomotives (PESA), proving its suitability for the industry’s varied operational demands.

If the technology is ready, what is the main challenge holding back wider adoption of hydrogen trains?

The primary barrier has shifted from the fuel cell technology itself to the surrounding ecosystem. The main bottleneck is the lack of a widespread green hydrogen production and refueling infrastructure along rail corridors. The industry’s next major hurdle is solving this ‘chicken-and-egg’ problem to ensure a reliable and cost-effective fuel supply for operators.

Who are the key companies leading the development of PEM fuel cell trains?

The market is defined by strategic partnerships. Ballard Power Systems is a leading fuel cell supplier, partnering with train manufacturers (OEMs) like Siemens Mobility (Mireo Plus H) and PESA. A major competing alliance in North America is between locomotive giant Wabtec and General Motors, which are collaborating to integrate GM’s HYDROTEC fuel cells into Wabtec platforms.

How are governments making hydrogen trains more economically viable?

Governments are creating powerful financial incentives that improve the business case. The article highlights the U.S. Inflation Reduction Act (IRA), which provides a tax credit of up to $3.00 per kilogram for clean hydrogen. This directly lowers fuel operating costs, making large-scale capital investments by private operators more economically attractive and accelerating the shift from pilots to commercial procurement.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.