Sinopec’s Hydrogen Pipeline Strategy: Building China’s 2026 Energy Backbone

Sinopec’s Hydrogen Projects: Shifting from Production Pilots to Full-Scale Infrastructure by 2026

Sinopec’s strategy has evolved from establishing large-scale green hydrogen production capabilities between 2021-2024 to an aggressive build-out of critical midstream and downstream infrastructure in 2025 and beyond, a move designed to de-risk the entire value chain. This shift indicates a transition from proving production capacity to actively creating a functional, integrated hydrogen economy.

- During the 2021–2024 period, Sinopec focused on demonstrating its capacity for large-scale green hydrogen production. This was defined by flagship projects like the $417 million, 20, 000 tons per annum (tpa) Xinjiang Kuqa solar-to-hydrogen plant commissioned in August 2023, and the launch of the even larger $828 million, 30, 000 tpa Ordos project in February 2023. These initiatives were backed by a comprehensive $4.6 billion investment plan aimed at establishing Sinopec as a leading producer.

- The period from 2025 onward marks a strategic pivot to solving logistical bottlenecks and building out the demand side. The most significant development is the plan for a nearly 400-kilometer green hydrogen pipeline from Ulanqab, Inner Mongolia, to the Beijing-Tianjin-Hebei region. This project, announced in September 2025, directly addresses the challenge of connecting remote, resource-rich production zones with eastern industrial demand centers.

- Downstream market creation accelerated significantly. The corporate goal to establish 1, 000 hydrogen refueling stations (HRS) by the end of 2025 gained momentum with the launch of the first public HRS in Hong Kong in December 2024. This was followed by a February 2026 memorandum with Towngas to expand the HRS network and develop a green methanol market in the Greater Bay Area, creating a captive market for its hydrogen production.

- To complement its domestic focus, Sinopec secured a role in the Front-End Engineering Design (FEED) for ACWA Power’s $8.5 billion Yanbu green hydrogen project in Saudi Arabia in August 2025. This provides invaluable experience in world-scale, export-oriented clean energy projects, diversifying its expertise beyond the Chinese domestic market.

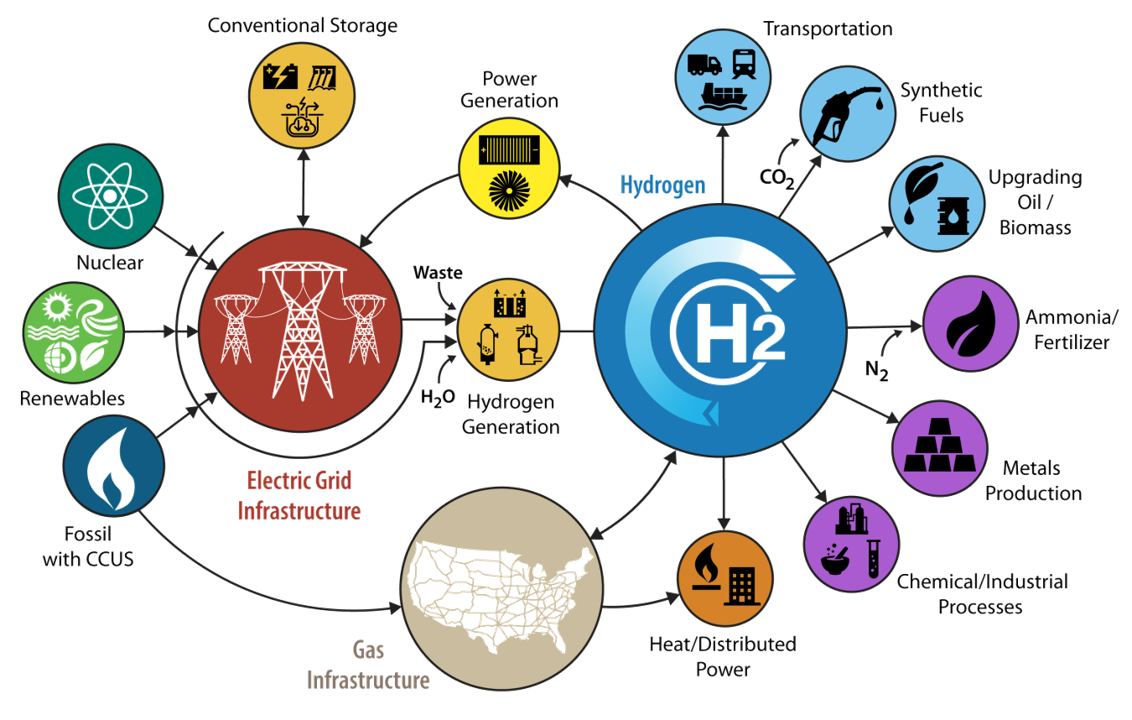

Visualizing the Integrated Hydrogen Economy

The section describes Sinopec building a “functional, integrated hydrogen economy” and de-risking the “entire value chain,” which this diagram directly illustrates.

(Source: Sandia National Laboratories)

Sinopec’s Capital Deployment: Over $5.8 Billion Earmarked for Hydrogen Dominance

Sinopec has substantiated its strategic hydrogen ambitions with over $5.8 billion in publicly announced capital commitments, directing funds toward large-scale production facilities designed to achieve economies of scale and establish a low-cost national supply base. The investment pattern shows a clear focus on securing upstream production capacity as a foundational step before expanding into midstream and downstream infrastructure.

- The company’s overarching commitment was signaled in August 2021 with a plan to invest $4.6 billion (30 billion yuan) into its hydrogen business through 2025. This capital was allocated across the value chain, from green hydrogen production to refueling networks and storage solutions.

- The largest project-specific investments were directed at two world-scale production facilities in China’s interior. The Ordos green hydrogen project in Inner Mongolia received an $828 million investment, and the Xinjiang Kuqa project was constructed with $417 million in capital.

- Beyond massive production plants, Sinopec also made smaller, targeted investments to stimulate downstream demand. A $7.35 million investment in a fuel cell supply demonstration project in Guangdong province in February 2022 highlights a strategy of nurturing local mobility markets alongside its larger infrastructure plays.

Table: Sinopec’s Key Hydrogen Investments (2021-2025)

| Project / Investment | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Ordos Green Hydrogen Project | 2023-02-22 | Invested $828 Million to build a 30, 000 tonnes/year green hydrogen facility in Inner Mongolia to decarbonize a local coal chemical plant. | Mercom India |

| Xinjiang Kuqa Green Hydrogen Project | 2023-07-05 | Invested $417 Million to construct a 20, 000 tonnes/year solar-to-hydrogen plant to supply its Tahe refinery, replacing grey hydrogen. | Upstream |

| Fuel Cell Supply Demonstration Project | 2022-02-03 | Invested $7.35 Million in a Guangdong province project to help develop the local hydrogen mobility market and supply chain. | CSIS |

| Hydrogen Development Fund | 2021-08-30 | Announced a $4.6 Billion investment plan through 2025 to fund green H 2 production, refueling stations, and storage infrastructure. | South China Morning Post |

Strategic Alliances: Sinopec’s Hydrogen Partnerships Expand from Technology Supply to Market Access

Sinopec’s partnership strategy has matured from securing electrolyzer technology for its initial projects (2022-2023) to forming strategic alliances for international project development and downstream market creation (2024-2026). This evolution reflects a growing confidence in its production capabilities and a sharpened focus on building commercially viable markets.

Benchmarking Clean Hydrogen Project Costs

This chart provides visual context for the projects listed in the section’s table, comparing their production capacity and cost against industry benchmarks.

(Source: Enverus)

- In its initial phase (2022-2023), partnerships were primarily transactional and technology-focused. For its flagship Kuqa project, Sinopec awarded supply contracts to electrolyzer manufacturers LONGi Hydrogen, Cummins, and Cockerill Jingli Hydrogen to mitigate supply chain risks and secure the necessary production hardware.

- Starting in 2024, the focus shifted toward strategic co-development and international expansion. A June 2024 collaboration with Saudi Arabia’s ACWA Power and a consortium with Técnicas Reunidas for the Yanbu project (August 2025) demonstrate a new emphasis on participating in global green energy projects and gaining expertise outside of China. These moves are complemented by broader energy partnerships, such as the April 2023 agreement with Qatar Energy for the North Field East LNG project, which solidifies its financial and strategic position in the global energy market.

- By 2026, partnerships became centered on downstream market access. The February 2026 Memorandum of Understanding with Towngas subsidiaries in Hong Kong focuses explicitly on building hydrogen refueling stations and developing a green methanol market, signaling a strategic push to create and control the end-user ecosystem.

Table: Sinopec’s Strategic Hydrogen Partnerships (2023-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Towngas | 2026-02-05 | Mo U to collaborate on hydrogen business development, HRS construction, and liquid hydrogen solutions in Hong Kong to build a local ecosystem. | Manifold Times |

| ACWA Power, Técnicas Reunidas | 2025-08-04 | Awarded FEED contract for the $8.5 B Yanbu green hydrogen project in Saudi Arabia, gaining experience in world-scale export projects. | EPC Intel |

| ACWA Power | 2024-06-26 | Formed a collaboration to jointly explore and develop global green hydrogen and ammonia projects, leveraging respective technical and portfolio strengths. | Offshore Energy |

| LONGi Hydrogen, Cummins, Cockerill Jingli | 2023-04-18 | Engaged as technology suppliers providing alkaline water electrolysis systems for the 20, 000 tpa Xinjiang Kuqa project. | LONGi |

Geographic Strategy: Connecting China’s Western Production Hubs to Eastern Demand Centers

Sinopec’s geographic strategy is deliberately bifurcated, concentrating massive green hydrogen production in the resource-rich western provinces of Xinjiang and Inner Mongolia while simultaneously building transport and refueling infrastructure to serve the high-demand industrial and urban hubs in the east and the Greater Bay Area. This “west-to-east” model is fundamental to its plan for a national hydrogen economy.

China’s 2020 Hydrogen Production Mix

This chart shows China’s historical reliance on coal for hydrogen, providing crucial context for Sinopec’s strategy to deploy green hydrogen from the west to decarbonize eastern industry.

(Source: Center on Global Energy Policy – Columbia University)

- Production Hubs (West): Between 2021 and 2024, capital was heavily concentrated in Western China to leverage its abundant solar and wind resources. The commissioning of the Kuqa project in Xinjiang and the construction of the Ordos project in Inner Mongolia established this region as the heart of Sinopec’s green hydrogen supply chain.

- Demand Centers (East): From 2025 onward, activity has intensified in China’s eastern economic zones. The Ulanqab-Beijing pipeline is the physical manifestation of this strategy, designed to function as a hydrogen artery. Concurrently, the build-out of refueling infrastructure in high-density areas like the Guangdong-Hong Kong-Macao Greater Bay Area aims to create reliable, localized demand.

- International Footprint (Middle East): The company’s engagement in Saudi Arabia’s Yanbu project since 2025 serves a distinct strategic purpose. It provides a foothold in the future global hydrogen export market and allows Sinopec to gain experience in international project structures and standards, which can be reapplied to its domestic operations.

Hydrogen Technology Maturation: From Seawater Electrolysis Pilots to Scaling Challenges

While Sinopec has successfully deployed commercial-scale alkaline electrolysis, operational challenges at its largest facility and ongoing pilots in novel technologies like direct seawater electrolysis show that the technology is still maturing and facing hurdles in reliability and cost-efficiency at scale. The company is simultaneously pushing the boundaries of established technology while investing in R&D to solve future cost and resource constraints.

Pathways for Green Hydrogen Production

The section discusses the maturation of various electrolysis technologies and pilots, and this diagram clearly illustrates the different technical pathways for green hydrogen production.

(Source: Nature)

- Commercial Scale Deployment: The commissioning of the Kuqa project in August 2023 was a major validation point, proving the viability of constructing a large-scale solar-to-hydrogen plant. The project uses established alkaline electrolysis technology sourced from commercial partners, confirming its readiness for industrial application.

- Operational Scaling Hurdles: Post-commissioning, the Kuqa project has highlighted the difficulties of at-scale operation. Reports from early 2024 revealed the plant was running significantly below its nameplate capacity, with Sinopec acknowledging that resolving issues related to intermittent renewable power integration could take until late 2025. This exposes a critical gap between building a plant and running it reliably and cost-effectively.

- Next-Generation R&D: Sinopec is actively exploring technologies that could resolve future bottlenecks. The successful completion of a 100 k W pilot project in December 2024 for direct seawater electrolysis without desalination is a significant R&D milestone. While still at an early stage, this technology could dramatically reduce the cost and freshwater dependency of green hydrogen production in coastal industrial regions.

SWOT Analysis: Sinopec’s Hydrogen Strategy for 2026

Sinopec’s primary strength lies in its state backing and integrated infrastructure strategy, which allows it to build out the full value chain. However, it faces significant weaknesses in managing the operational complexities of scaled green hydrogen and threats from the high cost of the fuel relative to incumbent energy sources.

- Strengths: The company’s ability to mobilize massive capital and leverage its existing energy infrastructure network is unmatched. Its strategy of building production, transport, and distribution in parallel is a key advantage.

- Weaknesses: The operational issues at the Kuqa project reveal a learning curve in managing large-scale, renewables-powered electrolysis. This suggests that technical expertise and reliability may lag behind construction speed.

- Opportunities: By aligning with China’s national decarbonization goals, Sinopec has strong policy support. Its infrastructure build-out creates new, captive markets for hydrogen in transport and industry.

- Threats: The ultimate economic viability of its network is the primary threat. The high price of green hydrogen must fall to compete without subsidies, which depends on both technological maturity and the rapid adoption of hydrogen fuel cell vehicles to ensure high utilization of its new infrastructure.

Table: SWOT Analysis for Sinopec’s Hydrogen Initiatives

| SWOT Category | 2021 – 2023 | 2024 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Massive capital commitment ($4.6 B fund); existing energy infrastructure network; strong state backing. | Aggressive execution of infrastructure (~400 km pipeline, 1, 000 HRS goal); gaining international project experience (Yanbu). | The strategy shifted from financial commitment to physical execution, validating its ability to construct large-scale projects and infrastructure. |

| Weaknesses | Heavy reliance on existing grey hydrogen production (3.5 M tpa); limited operational experience with green hydrogen at scale. | Operational challenges at the Kuqa plant (running below capacity); dependence on third-party electrolyzer technology that is still maturing. | The challenge evolved from building the plants to making them run reliably and efficiently, revealing a critical operational learning curve. |

| Opportunities | Alignment with China’s national carbon neutrality goals; captive demand from decarbonizing its own refining operations. | Creating new end-markets (Hong Kong HRS, green methanol); pioneering new tech (direct seawater electrolysis); building a captive mobility market. | The focus broadened from internal decarbonization to actively building and shaping new external markets for hydrogen fuel and derivatives. |

| Threats | High cost of green hydrogen production; competition from other low-carbon energy carriers and EVs. | Economic viability of the HRS network is dependent on rapid HFCV adoption; hydrogen prices (e.g., $4.86/kg) remain high without subsidies. | The threat became more concrete: will the massive infrastructure investment be profitable, or will it become a network of stranded assets? |

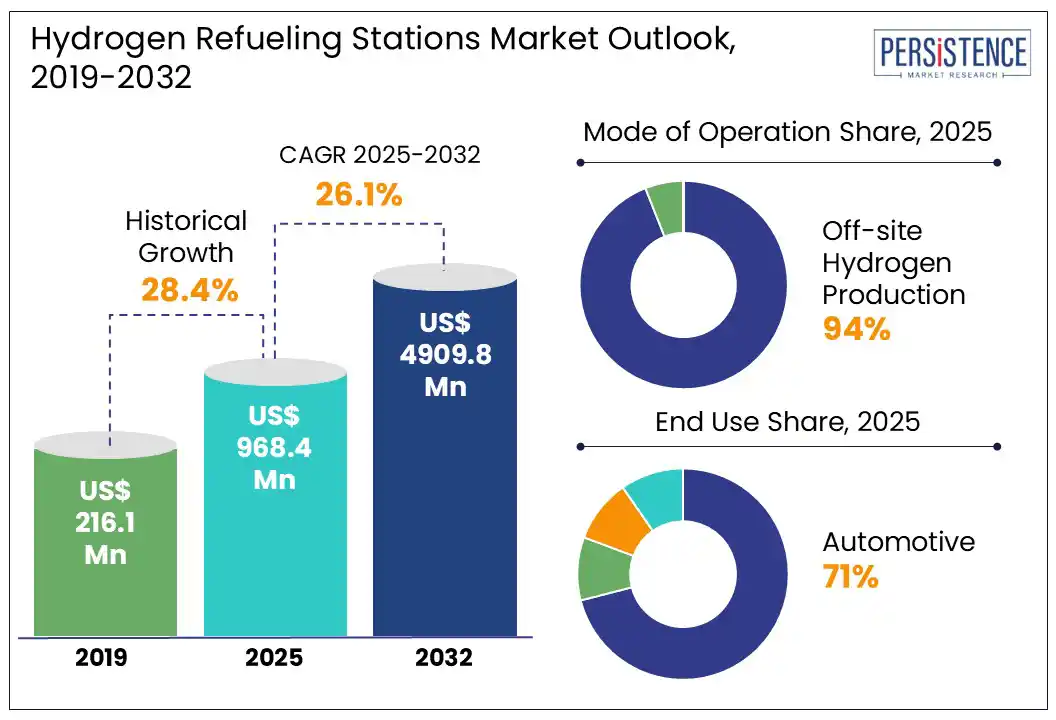

2026 Outlook: Watching Sinopec’s Pipeline Progress and Hydrogen Pricing

If Sinopec meets its 2025 construction milestones for the Ulanqab-Beijing pipeline and its refueling network, the key signal to watch in 2026 will be the utilization rates of this new infrastructure and the at-the-pump retail price of hydrogen, which will together determine the economic success of its entire strategy.

Hydrogen Refueling Market Set for Growth

As the section focuses on the outlook for Sinopec’s refueling network and hydrogen pricing, this chart directly quantifies the significant growth and value of that target market.

(Source: Persistence Market Research)

- If the pipeline progresses on schedule, watch its utilization rate. The Ulanqab-Beijing pipeline is the most critical piece of infrastructure in Sinopec’s plan. Its completion and subsequent transport volumes will be the first real-world test of the economics of long-distance hydrogen transport in China and will validate the company’s entire west-to-east supply strategy.

- If the HRS network expands, watch vehicle adoption rates. As Sinopec pushes towards its 1, 000 HRS target, the key metric will be the growth in the hydrogen fuel cell vehicle fleet. The success of partnerships like the one with Towngas in Hong Kong will signal whether demand can keep pace with supply infrastructure.

- These events could signal a shift in pricing strategy. As its large-scale production plants ramp up and the pipeline comes online, watch for any change in the retail price of hydrogen at Sinopec’s stations. A move to lower the price from current levels (around $4.86/kg) toward its long-term target would indicate growing confidence in its production costs and a serious attempt to make hydrogen competitive with conventional fuels.

Frequently Asked Questions

What is the core of Sinopec’s hydrogen strategy?

Sinopec’s strategy is to build a fully integrated national hydrogen economy in China. This involves a “west-to-east” model: concentrating large-scale green hydrogen production in the resource-rich western provinces (like Xinjiang and Inner Mongolia) and building critical transport infrastructure, like the 400-km pipeline to Beijing, to connect this supply with high-demand industrial and urban centers in the east.

What are Sinopec’s most significant hydrogen projects?

The most significant projects include two world-scale green hydrogen production facilities: the 20,000 tons per annum (tpa) Xinjiang Kuqa project and the larger 30,000 tpa Ordos project. Critically, Sinopec is also building a nearly 400-kilometer green hydrogen pipeline from Ulanqab to the Beijing-Tianjin-Hebei region and aims to establish 1,000 hydrogen refueling stations (HRS) by the end of 2025.

How has Sinopec’s strategy evolved over time?

Sinopec’s strategy has shifted from proving production to building a functional market. In the 2021–2024 period, the focus was on establishing large-scale green hydrogen production capabilities with projects like Kuqa and Ordos. From 2025 onward, the strategy pivoted to an aggressive build-out of midstream (pipelines) and downstream (refueling stations) infrastructure to solve logistical bottlenecks and create demand.

What are the main challenges Sinopec is facing in its hydrogen ambitions?

Sinopec faces two primary challenges. First, there are operational hurdles, as highlighted by its Kuqa plant running significantly below capacity due to difficulties in integrating intermittent renewable power. Second, the economic viability of its entire network is a major threat, as the current high price of green hydrogen (around $4.86/kg) must decrease to compete with conventional fuels and ensure its new infrastructure is profitable.

Is Sinopec’s hydrogen strategy only focused on China?

No, Sinopec is also expanding its expertise internationally. It secured a role in the Front-End Engineering Design (FEED) for ACWA Power’s $8.5 billion Yanbu green hydrogen project in Saudi Arabia. This move allows Sinopec to gain invaluable experience in world-scale, export-oriented clean energy projects, diversifying its knowledge beyond the Chinese domestic market.