SOFC Rail Adoption 2026: Why Auxiliary Power Is the New Gateway to Freight

SOFC Commercial Projects Signal Shift from Niche Trials to Heavy-Duty Viability

Solid Oxide Fuel Cell (SOFC) adoption is shifting from niche, experimental rail projects to commercially-driven deployments in adjacent heavy-duty transport, signaling a viable, albeit indirect, pathway to decarbonizing freight locomotives. The period between 2021 and 2024 was defined by small-scale, grant-funded demonstrations focused on auxiliary power units (APUs) and stationary signaling. Since 2025, the strategy has evolved, with major SOFC players validating the technology in demanding maritime applications, which serve as a direct proxy for the high-power, high-vibration environment of rail freight.

- Between 2021 and 2024, market entry was limited to proving baseline functionality in low-power rail applications. The most significant activity was the UK-based project led by Adelan to demonstrate an SOFC APU on a Class 37 locomotive, and Adaptive Energy securing orders for wayside signaling power. These projects established a foothold but did not address the core challenge of motive power.

- Starting in 2025, the commercial focus expanded to adjacent heavy transport sectors, a critical step for scaling technology and proving durability. Bloom Energy partnered with GTT and PONANT to develop an LNG-powered SOFC for ships, while Delta Electronics initiated a 120 k W pilot on an FPSO vessel. These projects tackle similar durability and power density challenges as rail freight, building the commercial and technical track record necessary for future locomotive systems.

- The application focus has broadened from simply replacing diesel generators to creating integrated, high-efficiency hybrid systems. Research into ammonia-fed SOFC hybrids showing 69.55% efficiency and Star Lite Engineering’s work on a diesel-reforming SOFC-turbine system highlight a move towards solutions that can transition with future fuel availability, a key advantage over fuel-specific technologies.

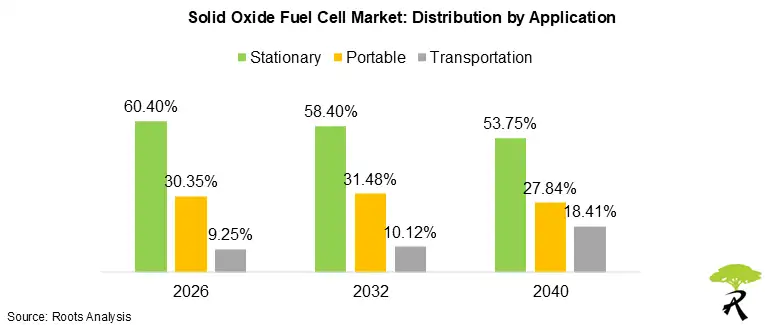

SOFCs Gain Traction in Heavy Transport

This forecast shows transportation’s market share nearly doubling by 2040, validating the article’s point about a strategic shift from niche trials to heavy-duty commercial viability.

(Source: Roots Analysis)

Investment in SOFC Manufacturing Scales for Heavy-Duty Applications

Strategic investments have pivoted from early-stage technology validation to securing manufacturing scale and vertical integration, a necessary prerequisite for entering the cost-sensitive rail and heavy-duty transport markets. Early funding focused on proving concepts, while recent capital injections from major industrial partners like Bosch and Delta Electronics are aimed squarely at mass production, which is essential for driving down the high capital costs that have historically limited SOFC adoption.

Investment Fuels Massive SOFC Market Growth

Projected to grow nearly tenfold to over $34 billion by 2034, the market’s expansion reflects the significant capital injections aimed at achieving manufacturing scale for heavy-duty applications.

(Source: Fortune Business Insights)

- In January 2024, Ceres Power and Delta Electronics finalized a manufacturing and license agreement, with Delta committing £43 million ($54.5 million) for technology transfer to produce SOFC stacks. This move is designed to leverage Delta’s mass-manufacturing expertise to reduce unit costs.

- Doosan Fuel Cell, using Ceres technology, is executing a 9.0 MW SOFC power project valued at approximately $170 million as of September 2025. While for stationary power, this project demonstrates the ability to deploy SOFCs at a megawatt scale and cost basis relevant to locomotive power requirements.

- The consistent financial backing from industrial giants underscores confidence in SOFCs for demanding applications. In March 2022, Ceres Power raised £181 million ($248 million) from its strategic partners Bosch and Weichai Power, providing the capital to expand its licensing model into new high-volume markets.

Table: Key Strategic Investments in SOFC Technology (2022-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Doosan Fuel Cell / Ceres Power | Sep 2025 | A 9.0 MW stationary SOFC project valued at 234.9 billion KRW (~$170 M), demonstrating scaled deployment of Ceres’ licensed technology. | FN News |

| Delta Electronics / Ceres Power | Jan 2024 | Manufacturing and license agreement including £43 M ($54.5 M) to Ceres for technology transfer, aimed at mass-producing SOFC stacks to lower costs. | PV Magazine |

| Bosch & Weichai Power / Ceres Power | Mar 2022 | Raised £181 M ($248 M) from existing strategic investors to fund technology expansion into high-volume markets, validating the asset-light licensing model. | ERM |

SOFC Rail Partnerships Target Auxiliary Power and Maritime Proxies

Partnerships in the SOFC space reveal a clear, pragmatic strategy: dominate niche rail applications first while using the maritime sector as a development ground for future high-power locomotive systems. Before 2025, collaborations were small and focused on rail-specific APU trials. Now, major SOFC developers are forming alliances with global shipping and energy leaders to solve the exact durability and fuel-flexibility challenges that rail freight presents, creating a de-risked path for technology transfer.

Strategic Alliances Shape SOFC Ecosystem

This ecosystem map identifies the key system integrators and component suppliers who are forming the strategic partnerships necessary to commercialize SOFCs for rail and maritime.

(Source: MarketsandMarkets)

- The Adelan, G-Volution, and Colas Rail UK partnership, active in early 2024, represented the first wave of rail-specific collaboration, focusing on a biofuel SOFC to power auxiliary systems on a freight locomotive. This targeted a clear commercial need by reducing idling emissions.

- A significant strategic shift occurred in late 2025 when Bloom Energy, a leader in stationary SOFCs, partnered with maritime specialists GTT and PONANT. Their goal is to develop an LNG-fueled SOFC system for cruise ships, proving the technology’s robustness in a mobile, high-vibration environment directly analogous to a locomotive.

- The collaboration between Delta Electronics, MODEC, and Eld Energy, announced in January 2026, further validates this maritime-first strategy. Their pilot project to deploy a 120 k W SOFC on an FPSO vessel by 2027 is a critical test of long-term operational reliability in a demanding industrial setting, a key requirement for rail operators.

Table: Strategic Partnerships Advancing SOFCs for Heavy Transport

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Delta Electronics, MODEC, Eld Energy | Jan 2026 | To deploy a 120 k W SOFC pilot on an FPSO vessel, validating the technology for heavy industrial, mobile use cases with a 2027 target. | Fuel Cells Works |

| Bloom Energy, GTT, PONANT | Oct 2025 | Joint innovation project to develop an LNG-powered SOFC and carbon capture system for ships, using maritime as a proxy for mobile, high-vibration applications. | Fuel Cells Works |

| Adelan, G-Volution, Colas Rail UK | Mar 2024 | Demonstrated a biofuel-powered SOFC APU on a Class 37 locomotive to reduce diesel use for auxiliary systems, proving the initial rail business case. | Rail Business Daily |

Geographic Focus Expands from UK Niche to Asian Industrial Scale

The geographic center of gravity for SOFC development is shifting from early-stage demonstrations in the UK and North America to large-scale manufacturing and deployment in Asia, particularly South Korea and China. While the UK initiated the first tangible rail projects and the US established a market for wayside signaling, Asia is now the hub for the industrial-scale production and capital investment required to make SOFCs viable for heavy-duty transport, including future rail applications.

Asia-Pacific to Lead Global SOFC Market

This forecast shows the Asia-Pacific region becoming the dominant market by 2030, which directly supports the section’s argument about the geographic shift toward Asian industrial scale.

(Source: MarketsandMarkets)

- Between 2021-2024, activity was concentrated in the West. The UK led with the Adelan-led APU project for freight locomotives, while in the US, Adaptive Energy secured significant orders for SOFC-powered rail signaling systems, establishing early commercial traction.

- From 2025 onwards, Asia has emerged as the leader in manufacturing and scaled deployment. Doosan Fuel Cell began mass production of Ceres Power’s SOFC technology in South Korea and is deploying it in a $170 million domestic power project. This demonstrates a commitment to industrialization that is absent in Europe and North America.

- China’s SOFC market is projected to reach USD 8.9 billion by 2031, growing at a 22.1% CAGR. This aggressive growth, coupled with manufacturers like Elcogen expanding their footprint in Asia, indicates the region will be the primary driver of cost reductions and supply chain development for the global SOFC industry.

Technology Maturity: SOFCs Move from Lab to High-Stakes Commercial Pilots

SOFC technology for mobile applications has progressed from a low Technology Readiness Level (TRL) characterized by lab-based research and small-scale rail APU demos to a medium TRL validated by commercial-scale pilots in demanding, real-world environments. Before 2025, the key challenges were material durability and slow dynamic response, confining SOFCs to constant-load auxiliary roles. Post-2025 projects, particularly in the maritime sector, are actively addressing these issues and proving the technology’s fitness for the variable loads and harsh conditions of heavy transport.

SOFC Deployments Signal Increasing Technology Maturity

The significant growth in annual installed capacity (MW) directly visualizes the technology’s progression from lab research and small demos to larger, real-world commercial pilots.

(Source: IDTechEx)

- The 2021-2024 period was defined by technological constraints. High operating temperatures (500-1000°C) and sensitivity to thermal cycling made SOFCs unsuitable for primary traction, while high costs limited deployments to grant-funded trials like the Adelan APU project.

- Since 2025, technology has advanced to meet commercial demands. Metal-Supported SOFCs (MS-SOFCs) offer faster start-up times and greater mechanical strength. This progress is reflected in the ambitious maritime pilots by Bloom Energy and Delta Electronics, which would not be feasible without significant improvements in durability and system integration.

- The narrative has shifted from overcoming fundamental flaws to proving economic viability at scale. While a 70% cost reduction is still needed for rail traction, projects like Doosan’s 9.0 MW deployment and Bosch’s move to volume production in 2023 are concrete steps toward achieving the economies of scale required for cost-competitiveness. This signals a clear path in the global energy transition for heavy transport.

SWOT Analysis: SOFCs Shift from Niche Weakness to Strategic Strength in Fuel Flexibility

The strategic position of SOFCs in the rail sector has fundamentally changed, moving from a technology with theoretical strengths but practical weaknesses to one whose core advantages are now being validated in commercially relevant projects. The most critical shift is the validation of its fuel flexibility, once a talking point, now a key enabler for pragmatic decarbonization strategies in heavy transport.

SOFCs Emerge as Strategic Growth Technology

This diagram illustrates the strategic shift where SOFCs enable new revenue in key markets like transportation, aligning with the SWOT analysis of its evolution into a strategic strength.

(Source: MarketsandMarkets)

- Strengths: SOFCs’ primary strength, fuel flexibility, has been validated through projects and research involving biofuels (Adelan), LNG (Bloom Energy), and future fuels like ammonia.

- Weaknesses: The historical weakness of high cost is now being directly addressed through scaled manufacturing partnerships (Ceres/Doosan, Ceres/Delta).

- Opportunities: The market opportunity has expanded from niche APUs to a clear, transitional pathway for decarbonizing heavy freight, starting with existing fuels like diesel and LNG and shifting to zero-carbon fuels later.

- Threats: The primary threat remains competition from more mature PEMFCs, which have solidified their lead in passenger rail with deployments by Siemens.

Table: SWOT Analysis for SOFCs in Railroad Applications (2021-2025)

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | High theoretical efficiency; Lab-proven fuel flexibility. | Proven efficiency >60% in commercial settings; Multi-fuel capability demonstrated in projects using LNG (Bloom Energy), biofuels (Adelan), and diesel/ammonia (research). | Fuel flexibility and efficiency have been validated in real-world, heavy-duty pilot projects, moving from a theoretical benefit to a proven strategic advantage. |

| Weaknesses | High capital cost ($5, 750+/k W); Slow start-up and poor dynamic response; Concerns over durability and thermal cycling. | Cost remains a barrier, but large-scale manufacturing (Doosan, Bosch) is beginning to address it. MS-SOFC development improves durability. | While cost is still high, the industry is now actively pursuing economies of scale through mass production, representing a concrete strategy to resolve a primary weakness. |

| Opportunities | Niche applications in rail APUs (Adelan) and wayside signaling power (Adaptive Energy). | Heavy-duty freight on non-electrified lines; Transitional fuel strategy (diesel/LNG to ammonia); Growth in proxy markets like maritime (Bloom, Delta). | The market opportunity has expanded from small rail niches to a credible, multi-fuel decarbonization pathway for the entire heavy-duty freight sector. |

| Threats | Competition from more mature PEMFCs (Alstom, Siemens) and battery-electric systems. | PEMFCs have entered commercial passenger service (Siemens), solidifying their lead in that segment. Batteries are a strong competitor for shunting and last-mile. | The competitive threat has become more defined. PEMFCs are winning the passenger rail market, forcing SOFCs to focus on the distinct advantages they hold for heavy freight. |

2026 Scenario: Maritime Success Will Trigger First SOFC Locomotive Traction Pilots

The most critical strategic development for SOFCs in rail by 2026 will be the successful operation of megawatt-scale systems in maritime applications, which will directly trigger the first well-funded locomotive traction pilot projects. If a company like Bloom Energy or Delta Electronics demonstrates reliable, high-efficiency operation on a ship for over 12 months, rail operators and OEMs will gain the confidence to invest in adapting the now-proven powertrain for freight locomotives. The key signal to watch is the transition from maritime project announcements to public data on performance, durability, and cost.

Transport Sector Drives Future SOFC Growth

This forecast’s emphasis on consistent, significant growth in the transportation sector directly supports the 2026 scenario where success in maritime triggers new locomotive pilots.

(Source: Market Research Reports & Consulting)

- If this happens: Delta Electronics‘ 120 k W FPSO pilot, scheduled for 2027, reports successful initial operation with over 60% efficiency and minimal degradation.

- Watch this: Major rail freight operators (e.g., BNSF, Union Pacific) or locomotive OEMs (e.g., Wabtec, Progress Rail) will announce a joint development agreement with an established SOFC manufacturer like Bloom Energy or a technology licensor like Ceres Power.

- These could be happening: The first RFPs will be issued for an SOFC-hybrid APU or a full traction system testbed, likely designed to run on reformed diesel or LNG as a transitional fuel, mirroring the approach being tested by Star Lite Engineering.

Frequently Asked Questions

Why is auxiliary power considered the ‘new gateway’ for SOFCs in freight rail?

Auxiliary power is considered a gateway because it allows SOFC technology to gain a commercial foothold in rail by first targeting a smaller, less demanding application. By replacing diesel generators for onboard power (APUs), SOFCs can prove their reliability and reduce idling emissions. This success, combined with parallel developments in the more demanding maritime sector, de-risks the technology and builds a viable pathway toward its eventual use for full locomotive traction.

How has the strategy for SOFC adoption in heavy transport changed since 2025?

Before 2025, the strategy focused on small, grant-funded rail demonstrations to prove basic functionality, such as the Adelan APU project. Since 2025, the strategy has evolved to target large-scale, commercial deployments in adjacent heavy-duty sectors, particularly maritime. Companies like Bloom Energy and Delta Electronics are developing high-power SOFC systems for ships, which serve as a proxy to validate the technology’s durability and performance for future freight locomotive applications.

Why is the maritime sector so important for the future of SOFCs in rail?

The maritime sector is crucial because it serves as a real-world, high-stakes testbed for SOFCs in an environment with challenges similar to freight rail: high vibrations, the need for continuous high power, and long-term operational reliability. Success in maritime projects, like those by Bloom Energy and Delta Electronics, demonstrates the technology’s robustness and builds the technical and commercial track record necessary to give rail operators the confidence to invest in SOFCs for their locomotives.

What has been the biggest barrier to SOFC adoption, and how is it being addressed?

Historically, the biggest barrier has been the high capital cost of SOFC systems. The article highlights that this is now being directly addressed through strategic investments focused on achieving mass production. Major industrial partnerships, such as Ceres Power’s agreements with Delta Electronics and Doosan Fuel Cell, are designed to leverage mass-manufacturing expertise to drive down unit costs and achieve the economies of scale needed for the cost-sensitive heavy transport market.

What is the main advantage of SOFCs for freight rail compared to other technologies?

The main advantage of SOFCs for freight rail is their fuel flexibility. Unlike other technologies like PEM fuel cells that typically require pure hydrogen, SOFCs can operate on a variety of fuels, including LNG, biofuels, ammonia, and even reformed diesel. This allows rail operators to begin decarbonizing using existing fuel infrastructure and transition to zero-carbon fuels like green ammonia in the future without a complete overhaul of the powertrain, offering a more pragmatic, transitional pathway.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.