Maritime SOFCs 2026: From Pilot to Propulsion, How Shipbuilders Are Scaling Up

SOFC Projects Shift from R&D to Commercial Scale-Up

The adoption of Solid Oxide Fuel Cells (SOFCs) in the maritime industry has decisively shifted from research-focused pilots to commercially-driven, large-scale deployment projects. The period from 2025 onwards is marked by major shipbuilders and industrial firms moving to validate megawatt-class systems on commercial vessels, a clear indicator that the technology is advancing toward becoming a standard for decarbonization.

- Between 2021 and 2024, maritime SOFC projects were primarily small-scale demonstrations focused on technology validation, such as the 500 k W Bloom Energy system trialed on the MSC World Europa and the 60 k W NAUTILUS project. These initiatives proved the technical feasibility of SOFCs in a marine environment.

- Starting in 2025, the focus pivoted to commercial readiness and operational validation. In April 2025, Doosan Fuel Cell and Samchully signed an MOU for a one-year sea trial on a commercial route, a critical step to gather long-term performance data.

- By June 2025, shipbuilding giant HD Hyundai announced an acceleration of its efforts to commercialize SOFCs for both vessels and port power, signaling a strategic integration of the technology into its core business.

- The LNGame Changer consortium, announced in March 2025, is designing a hybrid powertrain combining SOFCs with turbines fueled by LNG, a pragmatic approach that leverages existing infrastructure to facilitate near-term adoption.

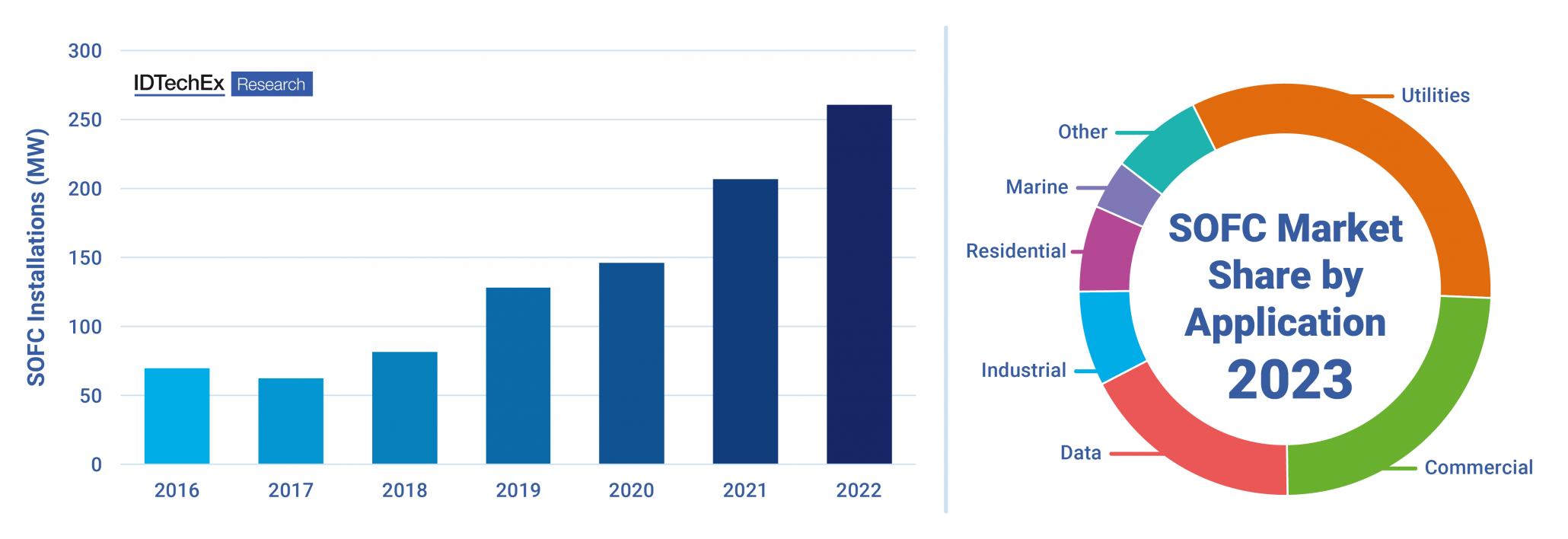

Marine Sector Emerges in SOFC Market

This chart shows the growth of SOFC installations and highlights the marine sector as a new, distinct application, visually confirming the section’s focus on commercial scale-up in maritime.

(Source: IDTechEx)

Strategic Investments Target Manufacturing Scale and Supply Chain Control

Direct strategic investment has become the primary financial mechanism for accelerating SOFC commercialization in the maritime sector, shifting away from grant-funded research. Industrial leaders are now acquiring stakes in core technology providers to secure their supply chains and co-develop systems optimized for mass production and integration into new vessel designs.

- This trend is exemplified by HD Hyundai’s €45 million strategic investment in Elcogen in October 2023. The explicit goal is to establish a European manufacturing facility and jointly develop SOFC systems, ensuring HD Hyundai controls a critical part of its future energy technology supply chain.

- The investment strategy aims to scale SOFC systems from auxiliary power units (APUs) to primary propulsion, directly addressing the industry’s need for high-power, zero-emission solutions.

- By funding cell and stack manufacturing directly, shipbuilders like HD Hyundai are working to drive down the high capital expenditure (CAPEX) that has historically been a major barrier to adoption.

Table: Key Strategic Investments in Maritime SOFCs

| Investor | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| HD Hyundai | Oct 2023 | A €45 million strategic investment in Elcogen to secure SOFC technology, establish a manufacturing base, and co-develop systems for marine applications, starting with APUs and scaling to propulsion. | Elcogen |

Maritime SOFCs Advance Through Targeted Ecosystem Partnerships

The maritime SOFC market is coalescing around strategic ecosystems that pair technology specialists with industrial powerhouses, shipbuilders, and energy majors. These collaborations are designed to de-risk development, share expertise, and build a complete value chain from fuel supply to on-board integration, accelerating the path to commercial viability.

Mapping the SOFC Value Chain Ecosystem

This map illustrates the SOFC ecosystem by player role, directly supporting the section’s discussion of strategic partnerships building a complete value chain from suppliers to integrators.

(Source: MarketsandMarkets)

- In April 2025, the partnership between Doosan Fuel Cell and energy provider Samchully was formed to operate a demonstration ship on an actual route, a collaboration aimed at proving operational reliability and securing market acceptance.

- The LNGame Changer consortium, formed in March 2025, brings together multiple partners to design a hybrid LNG-SOFC powertrain. This collaborative approach pools expertise in fuel systems, turbine technology, and naval architecture.

- The partnership between UK-based Ceres Power and Norway’s Alma Clean Power, announced in October 2023, combines Ceres’ core cell technology with Alma’s marine system integration expertise to bring a dedicated maritime SOFC product to market.

- Earlier, in October 2022, a consortium led by Shell, including KSOE (a Hyundai company), Doosan Fuel Cell, and Ceres, was established to explore using SOFCs as the main power source on a Shell-chartered vessel, linking an energy major directly with shipbuilders and tech developers.

Table: Key Maritime SOFC Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Genevos | Feb 2026 | Launched development of a next-generation SOFC solution specifically for commercial and cruise shipping, targeting high-power applications. | Fuel Cell China |

| Doosan Fuel Cell & Samchully | Apr 2025 | Signed an MOU for a one-year sea trial to demonstrate a domestically produced SOFC system on a commercial shipping route, aiming for commercialization in H 2 2025. | Fuel Cells Works |

| LNGame Changer Consortium | Mar 2025 | A consortium project to design a hybrid powertrain combining SOFCs with gas and steam turbines, leveraging existing LNG infrastructure for a transitional decarbonization pathway. | HAV Group |

| Alma Clean Power & Ceres | Oct 2023 | Partnership to demonstrate a complete SOFC system for the marine market, leveraging Ceres’ cell technology and Alma’s marine system design. | Offshore Energy |

| Shell-led Consortium | Oct 2022 | Partnership between Shell, KSOE, Doosan Fuel Cell, and Ceres to develop and install a 600 k W SOFC auxiliary power unit on a tanker. | Shell |

South Korea and Europe Emerge as Dual Hubs for Maritime SOFC Development

The global development of maritime SOFCs is concentrated in two key regions: South Korea and Europe. South Korea leverages its shipbuilding dominance to drive manufacturing and commercialization, while Europe provides deep technology expertise and hosts critical pilot projects, creating a complementary relationship that accelerates market-wide progress.

Asia-Pacific Region to Dominate SOFC Market

This forecast identifies the Asia-Pacific region as the dominant and fastest-growing market, directly supporting the section’s claim that South Korea is a central hub for commercialization.

(Source: MarketsandMarkets)

- South Korea has become the center for industrial-scale commercialization. Giants like HD Hyundai and Doosan Fuel Cell are integrating SOFCs into their shipbuilding and power system businesses, with clear timelines for market entry announced in 2025.

- Europe, particularly Scandinavia and the UK, serves as the technology and innovation hub. Norway’s Alma Clean Power, the UK’s Ceres Power, and Estonia’s Elcogen are key technology developers. European consortiums like Ship FC (ammonia SOFC) and NAUTILUS (LNG hybrid) are pushing the boundaries of fuel flexibility and system integration.

- The partnership between South Korea’s HD Hyundai and Europe’s Elcogen, solidified in 2023, exemplifies the inter-regional collaboration required to bring maritime SOFCs to market at scale.

SOFC Technology Reaches Commercial System Qualification

Maritime SOFC technology has matured from component-level testing to full-system qualification for on-vessel operations. While the 2021-2024 period focused on proving the viability of cells and small stacks in a marine environment, the post-2025 era is defined by the certification and deployment of complete, megawatt-scale power blocks, signaling readiness for commercial adoption.

SOFCs Identified as Disruptive Marine Technology

This chart positions SOFCs as a key disruptive technology for the marine market, reinforcing the section’s point that the technology has matured to the point of commercial qualification.

(Source: MarketsandMarkets)

- Between 2021 and 2024, key milestones included component-level validation. In March 2024, Doosan Fuel Cell and Hy Axiom became the first to pass environmental tests for SOFC components for maritime use, a foundational step.

- In April 2023, Alma Clean Power received an Approval in Principle (Ai P) from DNV for its 1 MW SOFC module design, validating the safety and feasibility of a large-scale, containerized system.

- The period from 2025 onwards focuses on full-system, long-duration sea trials. Doosan’s plan to commercialize its SOFC product in H 2 2025 and immediately begin a one-year demonstration on a commercial vessel represents the final stage of qualification before widespread commercial orders.

- The launch of development by Genevos in February 2026 for a next-generation SOFC solution for large commercial and cruise ships further indicates the technology is advancing to meet the most demanding power requirements in the shipping industry.

SWOT Analysis: Maritime Solid Oxide Fuel Cells

The strategic outlook for maritime SOFCs is shaped by their high efficiency and fuel flexibility, which present a clear opportunity to meet decarbonization mandates. However, high capital costs and unresolved fuel logistics remain significant hurdles that ongoing commercialization efforts aim to overcome.

SOFCs Demonstrate Competitive Energy Density

This chart provides technical data on the competitive energy density of ammonia-SOFC systems, substantiating the ‘Strengths’ like fuel flexibility identified in the section’s SWOT analysis.

(Source: IDTechEx)

- Strengths: The core advantages of high electrical efficiency and fuel flexibility have been consistently validated and are now being proven at a larger scale.

- Weaknesses: High CAPEX continues to be the primary barrier, though strategic investments and manufacturing scale-up are actively addressing this issue.

- Opportunities: The IMO 2050 net-zero target provides a powerful regulatory driver, creating a multi-billion dollar market opportunity for effective decarbonization technologies like SOFCs.

- Threats: Competition from alternative technologies and uncertainty around the future cost and availability of green fuels like ammonia pose external risks to adoption.

Table: SWOT Analysis for Maritime SOFC Adoption

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | High electrical efficiency (50-65%) and fuel flexibility (LNG, ammonia) demonstrated in research and small pilots like the Ship FC project. | Efficiency over 60% confirmed. Fuel flexibility is now a central feature of commercialization strategies, as seen in the hybrid LNG-SOFC LNGame Changer project. | The technology’s core strengths have been validated in larger, commercially-backed projects, moving from theoretical advantage to a proven value proposition for shipowners. |

| Weaknesses | High capital expenditure (CAPEX) compared to traditional Internal Combustion Engines (ICEs). Limited manufacturing scale and supply chain for marine-grade systems. | CAPEX remains a significant barrier, acknowledged in a May 2025 study. Related industrial ROI is benchmarked at 12.8 years, indicating a long payback period. | The weakness is now being directly addressed by industrial-scale manufacturing pushes from HD Hyundai and Doosan, aiming to drive down costs through volume production. |

| Opportunities | IMO decarbonization targets created a potential future market. The marine TAM was estimated by Bloom Energy at $15-20 billion. | The IMO’s net-zero by 2050 goal has become an urgent driver. Market forecasts show the overall SOFC market growing at over 30% CAGR, with transportation’s share doubling by 2040. | The market opportunity has transitioned from a forecast to an active driver of corporate strategy, with major shipbuilders making SOFCs a core part of their decarbonization roadmaps. |

| Threats | Uncertainty over the future availability and cost of green fuels like ammonia and hydrogen. Competition from alternative technologies (e.g., batteries, PEMFCs). | Fuel logistics remain a challenge. Competing technologies like onshore electrification for offshore platforms show a competitive LCOE of $50–110/MWh. | The threat has become more defined. SOFCs are being positioned as a fuel-flexible bridge technology (e.g., LNG-to-ammonia) to mitigate fuel risk, a key advantage over less flexible alternatives. |

Scenario Modelling: 2026 Sea Trials to Trigger First Commercial Orders

The success of the large-scale sea trials planned for 2025 and 2026 is the single most critical variable determining the commercial adoption curve for maritime SOFCs. If these demonstrations validate system durability, reliability, and safety in real-world operations, the first significant wave of commercial newbuild orders featuring integrated SOFC power systems is likely to occur by late 2026 or early 2027.

Transportation’s SOFC Market Share to Double

This forecast, showing the transportation segment’s market share doubling, quantifies the commercial adoption curve that the section’s scenario modelling predicts will be triggered by successful sea trials.

(Source: Roots Analysis)

- If this happens: The one-year commercial sea trial announced by Doosan Fuel Cell and Samchully successfully concludes, providing a full set of operational data that confirms the economic and technical case for SOFCs.

- Watch this: HD Hyundai’s progress towards its 2025 commercialization goal. Any announcements of newbuild designs that incorporate SOFCs as a standard or optional power source will be a strong signal of market readiness.

- These could be happening: Classification societies like DNV and Lloyd’s Register may publish finalized rules for SOFC system integration based on the trial data, removing regulatory uncertainty. Simultaneously, port authorities and energy majors may announce initial investments in ammonia or hydrogen bunkering infrastructure to support the first generation of SOFC-powered vessels.

Frequently Asked Questions

What is the biggest change happening with maritime SOFCs starting in 2025?

The main change is the shift from small-scale, research-focused pilot projects (2021-2024) to large, commercially-driven deployments. Starting in 2025, major shipbuilders and industrial firms are launching megawatt-class systems on commercial vessels to validate long-term performance and prepare for mass-market adoption, moving the technology from a concept to a standard for decarbonization.

Why are shipbuilders like HD Hyundai investing millions in SOFC technology companies?

Shipbuilders are making large strategic investments to secure their supply chains and control the development of critical decarbonization technology. By investing in SOFC specialists like Elcogen, companies like HD Hyundai aim to establish manufacturing facilities, co-develop systems for mass production, and drive down the high capital costs (CAPEX) that have been a major barrier to adoption.

What are the biggest challenges still facing SOFC adoption in the shipping industry?

The two primary challenges are the high capital expenditure (CAPEX) compared to traditional engines and the uncertainty around the future cost and availability of green fuels like ammonia and hydrogen. While strategic investments are aimed at lowering manufacturing costs, the high initial investment and fuel logistics remain significant hurdles.

Which regions are leading the development of maritime SOFCs?

South Korea and Europe have emerged as the two key hubs. South Korea, home to shipbuilding giants like HD Hyundai and Doosan Fuel Cell, is leading the industrial-scale manufacturing and commercialization. Europe, particularly Scandinavia and the UK, serves as the technology and innovation hub with key developers like Elcogen, Ceres Power, and Alma Clean Power.

When are the first commercial orders for SOFC-powered ships expected?

The first significant wave of commercial newbuild orders featuring integrated SOFC power systems is likely to occur by late 2026 or early 2027. This timeline is dependent on the success of the large-scale sea trials planned for 2025 and 2026, which are designed to validate the technology’s durability and reliability in real-world commercial operations.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.