Grid-First Hydrogen: Why Southern Company’s Infrastructure Strategy is Winning in 2026

From Pilots to Power Plants: Hydrogen’s Shift to Commercial Scale

The energy industry’s approach to hydrogen adoption has pivoted from exploratory research to a focused, infrastructure-led strategy, with major utilities like Southern Company demonstrating large-scale co-firing in existing assets as the most viable near-term path to commercialization. This model prioritizes leveraging billions of dollars in current infrastructure to de-risk the energy transition, a stark contrast to the high-capital, greenfield projects that characterized the sector’s earlier ambitions.

- Between 2021 and 2024, the focus was on validating foundational concepts through smaller-scale pilots. Southern Company’s successful test of a 20% hydrogen blend in a gas turbine in 2022 was a critical proof-of-concept, but it remained a demonstration. During this period, many competitors like Plug Power pursued a different strategy, announcing plans for pure-play green hydrogen production facilities.

- Starting in 2025, the strategy scaled dramatically from pilot to pre-commercial validation. The landmark achievement was Southern Company’s successful test of a 50% hydrogen blend in an advanced-class turbine at Plant Mc Donough-Atkinson in June 2025, proving that significant decarbonization, an approximate 22% reduction in carbon emissions, is achievable with existing commercial power plants.

- This infrastructure-first approach is validated by market dynamics, as a Wood Mackenzie report noted a lack of giga-scale green hydrogen project Final Investment Decisions (FIDs) in the U.S. during 2025. By focusing on co-firing, utilities can achieve tangible emissions reductions without waiting for the entire green hydrogen value chain to mature, offering a more pragmatic and scalable deployment model.

Investment Strategy Shifts from R&D to Systemic Grid Modernization

Capital deployment for hydrogen has matured from funding discrete R&D projects to securing massive, long-term financing for modernizing the core power generation infrastructure designed to use hydrogen. This shift underscores a systemic commitment to a natural gas and hydrogen-centric future, backed by significant federal validation and private capital.

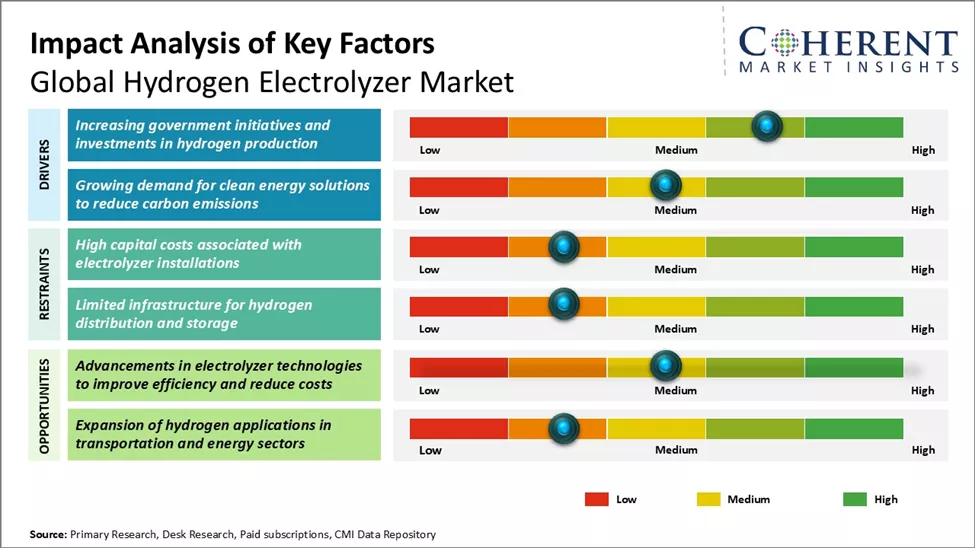

Investment and Costs Shape Market

The chart identifies government investment as a high-impact driver and high capital costs as a restraint, which aligns with the section’s focus on the shifting investment strategy for hydrogen infrastructure.

(Source: Coherent Market Insights)

- In the 2021-2024 period, investments were targeted and project-specific. For example, Southern Company announced a $65 million investment in December 2024 to create a hydrogen-powered worksite and fuel-cell truck ecosystem, a project designed to test a specific end-use application.

- The investment landscape transformed in 2025 and 2026, moving from the project level to the system level. Southern Company announced a five-year capital plan exceeding $80 billion to strengthen its grid and deploy cleaner technologies, creating the foundation for hydrogen integration.

- This strategy was cemented in February 2026 when the U.S. Department of Energy issued a monumental $26.5 billion, 30-year loan to Southern Company. This capital is designated for financing 5 GW of new natural gas generation and modernizing the very assets intended to co-fire hydrogen, directly underwriting the company’s blending strategy.

Table: Strategic Hydrogen-Related Investments and Capital Plans (2024-2026)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Southern Company (DOE Loan) | Feb 2026 | Secured a $26.5 billion federal loan to finance 5 GW of new natural gas generation and modernize the power assets that will be used for hydrogen co-firing. This de-risks the capital-intensive fleet transition. | POLITICO Pro |

| Southern Company (Capital Plan) | Sep 2025 | Announced a five-year capital plan of over $80 billion aimed at grid modernization and deploying advanced technologies, including hydrogen-ready infrastructure. | Southern Company |

| Unnamed Developer (Competitor Project) | Jun 2025 | A $1.85 billion project for a large-scale solar-powered green hydrogen manufacturing facility in California, representing a greenfield production-focused strategy. | POWER Magazine |

| Southern Company (Worksite Ecosystem) | Dec 2024 | A $65 million project to demonstrate hydrogen as a diesel alternative in fuel-cell medium-duty trucks, focused on a specific mobility application. | Southern Company |

Partnerships Solidify Southern Company’s Infrastructure-Led Hydrogen Strategy

Strategic alliances have evolved from broad, exploratory R&D consortiums into concrete technology and fuel supply agreements that anchor the infrastructure-led hydrogen strategy for the long term. This transition from exploration to execution demonstrates a clear commitment to a specific decarbonization pathway.

Hydrogen Corridors Model Strategic Partnerships

This diagram of a ‘Green Hydrogen Corridor’ illustrates a large-scale, infrastructure-led strategy, visually representing the type of concrete supply and technology partnerships the section describes.

(Source: TRENDS Research & Advisory)

- Between 2021 and 2024, partnerships were primarily focused on research and ecosystem building. Key examples include Southern Company’s membership in the DOE-backed Hy Velocity Hub and its collaboration with the Electric Power Research Institute (EPRI) and Mitsubishi Power on the initial 20% blend test.

- In 2025, partnerships became highly focused and operational. The renewed collaboration with Mitsubishi Power to execute the successful 50% hydrogen blend test at a commercial scale in June 2025 was a critical technology validation that moved the concept toward commercial reality.

- Most strategically, Southern Company signed a 10-year natural gas supply agreement with producer EQT in June 2025. This agreement secures the foundational fuel for its power plants, directly underpinning the hydrogen blending strategy by ensuring a stable, long-term supply of the base fuel to be mixed with hydrogen.

Table: Evolution of Strategic Hydrogen Partnerships (2022-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Mitsubishi Power | Jun 2025 | Technology demonstration partner for the successful 50% hydrogen blend test in an advanced-class M 501 GAC gas turbine, a global milestone for a turbine of its class. | PR Newswire |

| EQT Corporation | Jun 2025 | Signed a 10-year natural gas supply agreement, securing the primary fuel source for power plants now being validated for high-percentage hydrogen blending. | Argus Media |

| Hy Velocity Hub | Oct 2023 | As a key member, Southern Company gained access to a share of $7 billion in federal funding and a collaborative ecosystem to scale hydrogen technologies in the Gulf Coast. | Southern Company |

| Mitsubishi Power & EPRI | Jun 2022 | Collaborated on the initial 20% hydrogen blend demonstration, providing the foundational data and confidence to pursue higher blend ratios. | EPRI |

U.S. Southeast Emerges as the Epicenter of Utility-Scale Hydrogen Blending

While global hydrogen activity is geographically diverse, Southern Company has concentrated its efforts in the U.S. Southeast, establishing its service territory as the primary proving ground for utility-scale hydrogen blending in existing power generation infrastructure.

Natural Gas Dominates Southern Co. Mix

This chart shows that natural gas is 52% of Southern Company’s energy mix, providing crucial context for why the U.S. Southeast has become an epicenter for hydrogen blending in existing gas infrastructure.

(Source: 3BL Media)

- Between 2021 and 2024, hydrogen activities were more geographically dispersed. Southern Company was active in the multi-state Hy Velocity Hub covering the Gulf Coast, and competitors like Plug Power announced green hydrogen production projects in Georgia, indicating broad regional interest.

- The focus sharpened significantly in 2025, centering on Southern Company’s own operational footprint in Georgia. Plant Mc Donough-Atkinson in Smyrna and the Plant Yates modernization project in Coweta County became the epicenters of the company’s hydrogen strategy, moving from regional consortiums to asset-specific execution.

- This regional concentration in the Southeast contrasts with other market strategies. For example, So Cal Gas is focused on developing dedicated hydrogen pipeline infrastructure in California, while HDF Energy’s partnership in Vietnam targets decentralized green hydrogen solutions for remote islands, highlighting different market-driven approaches.

Technology Maturity: Co-Firing Leaps from Concept to Commercial-Ready

Hydrogen co-firing technology for power generation has rapidly matured from a small-scale, experimental concept into a validated, large-scale application, with demonstrated blend percentages more than doubling in a single year. This acceleration validates the technical feasibility of retrofitting existing assets for a lower-carbon future.

How Grid-Integrated Hydrogen Production Works

The diagram illustrates the technical pathways for producing hydrogen for power generation, visually explaining the technology that enables the co-firing applications discussed in the section.

(Source: Nature)

- The 2021-2024 period was defined by foundational validation. The key milestone was the successful test of a 20% hydrogen blend in a natural gas turbine in 2022, which proved the basic concept was sound but left questions about the viability and performance of higher concentrations.

- A major technological leap occurred in June 2025 with the successful demonstration of a 50% hydrogen blend in an M 501 GAC advanced-class turbine. This achievement proved that existing assets can achieve significant decarbonization without immediate replacement and without compromising operational stability.

- The delivery of new, advanced natural gas turbines to Plant Yates in August 2025 signals the next phase of technology deployment. These modern turbines are designed with greater fuel flexibility, providing the technological foundation for future hydrogen co-firing capabilities and a pathway to even higher blend percentages.

SWOT Analysis: Southern Company’s Infrastructure-Led Hydrogen Strategy

Southern Company’s hydrogen strategy successfully transitioned from an R&D-heavy phase with uncertain commercial viability to a validated, infrastructure-focused model. This pivot has de-risked the technology but introduces new dependencies on hydrogen supply costs and the stability of regulatory incentives like the Inflation Reduction Act.

- The company leveraged its core strengths in asset management to prove out a scalable decarbonization technology.

- A key weakness remains the entrenchment of natural gas infrastructure, making long-term net-zero goals dependent on a low-cost, low-carbon hydrogen supply that is not yet mature.

- The primary opportunity was the capitalization of federal support, transforming general incentives into a concrete $26.5 billion loan.

- The main external threat has shifted from technological competition to the market and policy volatility surrounding hydrogen feedstock pricing and tax credit implementation.

Table: SWOT Analysis for Southern Company’s Hydrogen Strategy Evolution

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Extensive existing natural gas asset base and operational expertise. Participation in R&D consortiums like the Hy Velocity Hub. | Proven 50% hydrogen blend capability in advanced-class turbines. Massive federal financial backing via a $26.5 billion DOE loan. | The strategy transitioned from leveraging assets for R&D to securing capital to deploy a validated, asset-led decarbonization technology at scale. |

| Weakness | Dependency on unproven high-blend combustion technologies and the natural gas supply chain. Blue hydrogen pathway dependent on CCUS development. | Deepened long-term dependency on natural gas infrastructure. Success now hinges on the future availability and cost of low-carbon hydrogen. | The primary risk shifted from internal technology development (Can we do it?) to external market dependency (Can we afford the fuel?). |

| Opportunity | Potential for federal funding through DOE Hydrogen Hubs and the Inflation Reduction Act (IRA). Growing utility decarbonization pressure. | Secured a monumental $26.5 billion DOE loan. A clear, asset-based path to leverage IRA 45 V clean hydrogen production tax credits. | The company successfully converted broad policy opportunities into tangible, large-scale financial and strategic advantages. |

| Threat | Competition from pure-play green hydrogen infrastructure projects (e.g., So Cal Gas’s “Angeles Link”). Uncertainty over final IRA 45 V rules. | Continued regulatory uncertainty on 45 V credit implementation could delay hydrogen supply investments. Potential for volatile hydrogen and natural gas prices. | The threat evolved from competition over technology pathways to a market-based risk centered on feedstock cost and policy stability. |

2026 Scenario: From Demonstration to Commercial Deployment

For 2026, the critical variable for Southern Company’s hydrogen strategy is the translation of successful demonstrations into a commercially scalable, fleet-wide deployment plan. This next step is entirely contingent on stable policy support and the emergence of a reliable, low-cost hydrogen supply chain.

Future Scenarios Point to Hydrogen Growth

This forecast shows dramatic growth in low-carbon hydrogen production through 2050, illustrating the scale of the reliable supply chain needed to make the section’s 2026 commercial deployment scenario a reality.

(Source: Natural Gas Intelligence)

- If federal support via the Inflation Reduction Act’s 45 V tax credits is finalized with clear, favorable guidance, watch for Southern Company to announce its first large-scale, long-term hydrogen offtake agreements. This action would signal a definitive move from testing to commercial operation.

- If the cost of low-carbon hydrogen begins a sustained decline, these could be happening: concrete announcements of retrofitting plans for other natural gas plants in the company’s fleet, expanding the program beyond the initial test sites at Plant Mc Donough-Atkinson and Plant Yates.

- If regulatory uncertainty persists or natural gas price volatility impacts the economics of blending, watch for a potential slowdown in the pace of fleet-wide conversion. The company would instead leverage its $80 billion capital plan to focus on efficiency upgrades for its gas fleet, maintaining hydrogen as a future option rather than an immediate priority. This highlights the value of the flexible, infrastructure-led approach.

Frequently Asked Questions

What is Southern Company’s “Grid-First” hydrogen strategy?

The “Grid-First” strategy prioritizes leveraging existing natural gas power plant infrastructure to co-fire hydrogen, rather than building entirely new, capital-intensive hydrogen production facilities. This approach allows for scalable, near-term emissions reductions by modifying assets already in place, as demonstrated by the successful 50% hydrogen blend test at Plant McDonough-Atkinson in 2025.

How is Southern Company financing this large-scale infrastructure strategy?

The strategy is backed by significant public and private capital. The company announced a five-year capital plan of over $80 billion for grid modernization. Crucially, in February 2026, it secured a monumental $26.5 billion, 30-year loan from the U.S. Department of Energy, which is designated to finance new natural gas generation and modernize the very assets intended for hydrogen co-firing.

What was the significance of the 50% hydrogen blend test in 2025?

The successful test of a 50% hydrogen blend was a global milestone that validated the entire infrastructure-led strategy. It moved hydrogen co-firing from a small-scale pilot (like the 20% test in 2022) to a pre-commercial reality in an advanced-class turbine. It proved that significant decarbonization—approximately a 22% reduction in carbon emissions—is achievable with existing commercial power plants without compromising operational stability.

How does Southern Company’s approach differ from competitors like Plug Power or the developer in California?

Southern Company’s strategy focuses on creating hydrogen *demand* by retrofitting existing power plants. This contrasts with competitors who are focused on the *supply* side by building “greenfield” projects, like pure-play green hydrogen production facilities. By focusing on co-firing, Southern Company can achieve tangible emissions reductions now, without waiting for the entire green hydrogen value chain to mature.

What are the biggest risks or challenges to Southern Company’s hydrogen strategy?

The main risk has shifted from technology to market and policy. While the company has proven the technical viability of high-percentage blending, its success now depends on external factors. The key challenges are securing a reliable, low-cost supply of low-carbon hydrogen and the need for stable, favorable government policy, particularly the final implementation of the Inflation Reduction Act’s (IRA) 45V tax credits, which are crucial to making hydrogen fuel economically competitive.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.