DAC Strategy 2026: Why Cautious Regional Hubs Outmaneuver Megaproject Risk

From Megaprojects to Regional Pilots: A Strategic Split in DAC Commercialization

By 2025, the Direct Air Capture industry fractured into two distinct commercialization models: capital-intensive, megaton-scale standalone plants and smaller, regionally integrated, partnership-driven pilot projects. This divergence reflects differing appetites for financial risk and strategic priorities, with utilities and industrial players favoring a more cautious, learning-oriented approach over the high-stakes rush to scale.

- Between 2021 and 2024, the market was defined by ambitious announcements for large-scale development. For instance, Occidental’s subsidiary 1 Point Five began constructing its Stratos facility in Texas, a project with a budget exceeding $1 billion, and vertically integrated by acquiring its technology provider, Carbon Engineering, for $1.1 billion in August 2023. In contrast, Southern Company pursued a low-risk entry, securing a $3 million Department of Energy (DOE) grant for a Front-End Engineering and Design (FEED) study for the Southeast DAC (SEDAC) Hub.

- The strategic split widened in 2025 as projects moved toward execution. Southern Company and its subsidiary Georgia Power confirmed their cautious strategy by launching an on-site DAC pilot with technology provider Aircapture and partnering with Monroe Sequestration Partners for a planned biofuels facility in Louisiana. This approach focuses on building complete, localized carbon management value chains with specialized partners, directly contrasting with Occidental’s continued pursuit of the massive South Texas DAC Hub.

- This strategic variety demonstrates that industry adoption is not monolithic. The regional hub model, favored by utilities like Southern Company, offers a more resilient, capital-light path to de-risk technology and build operational expertise. The megaproject model chases economies of scale but faces greater exposure to financial and policy risks, particularly around the stability of large-scale federal subsidies.

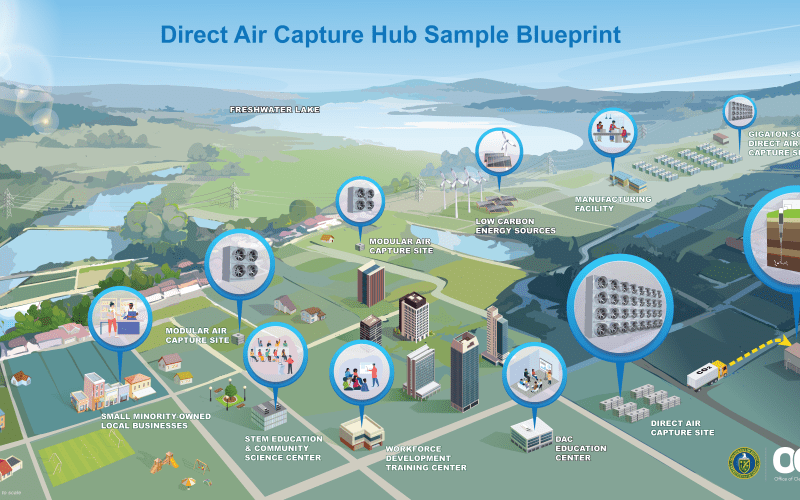

Blueprint for Integrated Direct Air Capture Hubs

This blueprint visualizes the integrated, regional DAC hub model discussed in the section, showing how capture, energy, and manufacturing components are combined in newer commercialization strategies.

(Source: Carbon Herald)

Federal Funding Volatility Reshapes DAC Investment Calculus

Significant federal funding uncertainty in 2025 exposed the financial fragility of capital-intensive DAC megaprojects, making smaller, partnership-funded initiatives with access to state-level cost recovery mechanisms appear more durable. The market’s initial reliance on massive federal grants was tested, revealing the strategic advantage of a diversified funding and project development approach.

- In 2023, the DOE signaled strong support for large-scale hubs, selecting projects like Project Cypress in Louisiana for up to $603 million and 1 Point Five’s South Texas DAC Hub for up to $500 million. This drove a narrative that large federal grants were the primary pathway to commercialization, encouraging the development of megaprojects.

- This narrative was challenged in October 2025, when reports emerged that the DOE was considering terminating awards for the two largest DAC hubs as part of a potential $7.5 billion grant review. Although a later bill preserved $800 million for the DAC Hubs program, the volatility created significant uncertainty for projects wholly dependent on this capital.

- In this context, Southern Company’s strategy appears more resilient. By focusing on smaller pilots funded through partnerships and foundational studies supported by modest federal grants, and leveraging state policies that allow for cost recovery on technology investments, the company insulated its DAC program from the turbulence of federal funding cycles.

Table: Comparative Analysis of DAC Project Funding Strategies

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Occidental / ADNOC (South Texas DAC Hub) | May 2025 | Received an award of up to $650 million from the DOE for the South Texas DAC Hub. ADNOC also agreed to evaluate a potential investment of up to $500 million, underscoring a strategy reliant on massive federal and international partner capital for a single large-scale project. | Carbon Credits.com |

| Southern Company / SSEB (SEDAC Hub) | August 2023 | The SSEB-led consortium, including Southern Company, was awarded $3 million from the DOE for a FEED study. This represents a minimal-risk approach to gain a foothold, understand technology, and de-risk future investment without major capital outlay. | RMI |

Partnerships Evolve from Grant-Seeking to Functional Execution

In the DAC sector, strategic partnerships have matured from broad, multi-stakeholder consortiums designed to secure federal grants (pre-2025) to focused, functional alliances aimed at executing specific projects and completing the carbon management value chain (2025 and beyond). This shift signals the market is moving from planning and fundraising to tangible project delivery and operational problem-solving.

Captured CO2 as a Valuable Commercial Feedstock

This infographic illustrates the end-products of the carbon management value chain, providing context for why partnerships are evolving towards functional execution to create valuable commodities.

(Source: ClearPath)

- The period between 2021 and 2024 was characterized by the formation of large consortiums for funding applications. The SEDAC Hub, established in August 2023, exemplifies this, bringing together the Southern States Energy Board (SSEB), Southern Company, technology provider 8 Rivers, and academic institutions primarily to secure a DOE grant for a feasibility study.

- By 2025, partnerships became more tactical and execution-oriented. Southern Energy’s selection of Monroe Sequestration Partners in June 2025 for its Louisiana biofuels plant is a prime example. This alliance was not for a study but to provide a critical, functional service: CO 2 storage, demonstrating a clear focus on building an operational, end-to-end industrial process.

- This trend highlights a strategic divergence in building capabilities. While Southern Company pursues a model of “renting” expertise through partnerships with specialists like Aircapture and Monroe Sequestration, competitors like Occidental have opted to “buy” capabilities, as seen in its $1.1 billion acquisition of Carbon Engineering. The partnership model is more capital-efficient but creates dependencies, whereas vertical integration offers greater control at a much higher cost.

Table: Evolution of Southern Company’s DAC Partnership Model

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Monroe Sequestration Partners | June 2025 | Selected as the CO 2 storage partner for Southern Energy’s planned Louisiana biofuels plant. This is a functional partnership to create a complete CCS value chain for an industrial asset. | Carbon Herald |

| Aircapture & SSEB | February 2025 | Georgia Power initiated a pilot project to test on-site DAC technology in collaboration with technology provider Aircapture. The purpose is technology validation and performance assessment in a real-world setting. | Georgia Power |

| SSEB & 8 Rivers (SEDAC Hub) | August 2023 | Southern Company joined a consortium to conduct a FEED study for a DAC hub. The purpose was to pool resources and expertise to secure a federal grant and explore the feasibility of a regional hub. | SSEB |

US Gulf Coast Solidifies as DAC Epicenter with Diverging Regional Strategies

DAC development is firmly concentrating in the U.S. Gulf Coast, a region favored for its unique combination of favorable sequestration geology, extensive industrial infrastructure, and supportive state-level policies. However, within this geographic hotspot, two distinct development strategies have emerged: the Texas model of building large-scale, standalone DAC factories and the Alabama/Louisiana model of integrating smaller DAC facilities with existing industrial and utility assets.

Texas Power Grid Shifts Towards Renewable Energy

This chart shows the changing energy mix in Texas, a key factor supporting the development of large, energy-intensive DAC facilities as described in the section’s regional analysis.

(Source: Energy Central)

- Before 2025, the U.S. Gulf Coast was broadly identified as a prime location for DAC development, largely driven by the DOE’s DAC Hubs program, which targeted the region for major investment announcements in Texas and Louisiana in 2023.

- Activity in 2025 solidified this concentration while clarifying the sub-regional strategies. Occidental reinforced the Texas-centric megaproject model by advancing its South Texas DAC Hub. In parallel, Southern Company’s activities demonstrated a different approach, focusing on Alabama with the SEDAC Hub in Mobile County and Louisiana with its integrated biofuels and CCS project.

- This geographic split in strategy is significant. Texas is becoming the global center for building massive, centralized carbon removal facilities designed to operate at utility scale. In contrast, Alabama and Louisiana are emerging as crucial testbeds for a more distributed and integrated model, where DAC technology is co-located with and provides decarbonization services for specific industrial facilities like power plants and biofuel refineries.

DAC Technology Focus Shifts from Scale to Validation of Diverse Pathways

The DAC market is undergoing a crucial technological maturation, shifting from a primary focus on scaling first-generation liquid-solvent systems to a broader effort to validate diverse, next-generation technologies like solid sorbents and calcium-looping processes. The year 2025 marks a key inflection point, with the first large-scale commercial plant providing cost benchmarks while smaller pilots generate critical operational data on emerging alternatives.

Solid-DAC Technologies to Drive Future Market Growth

This forecast supports the section’s claim that the market is validating diverse pathways, projecting that next-generation solid-sorbent technologies (Solid-DAC) will become a dominant component.

(Source: IMARC Group)

- The 2021-2024 period was dominated by the push to scale established technologies, primarily potassium hydroxide-based liquid solvent systems developed by companies like Carbon Engineering. Occidental adopted this technology for its Stratos plant, which is scheduled to begin operations in mid-2025 and serve as the first major commercial-scale benchmark for the technology’s cost and performance.

- In 2025, the market’s focus broadened to include real-world testing of alternative pathways. Southern Company’s strategy exemplifies this trend. Its involvement in the SEDAC Hub is centered on validating 8 Rivers’ Calcite technology, a thermal-swing calcium-looping process. Concurrently, its subsidiary Georgia Power launched a pilot with Aircapture, a solid-sorbent technology provider.

- This diversification is a sign of a healthy, maturing technology sector. While the Stratos plant will provide invaluable data on the economics of at-scale liquid systems, the concurrent pilots of solid-sorbent and calcium-looping technologies will inform the industry’s next wave of investment decisions. This de-risks the sector from over-reliance on a single technology pathway and fosters competition on cost and efficiency.

SWOT Analysis: Strategic Divergence in DAC Deployment Models

Southern Company’s cautious, partnership-based DAC strategy successfully leverages its regional strengths and minimizes direct financial risk, particularly in a volatile funding environment. However, this prudent approach results in a deliberate lag in operational scale and creates a dependency on the technological success of its partners when compared to more aggressive, vertically integrated first-movers.

- The company’s primary strength is its risk-averse, capital-light model, which shifted from planning to execution in 2025, proving resilient to federal funding uncertainty.

- Its key weakness remains a lack of large-scale operational capacity, confirming a slower path to market but one that is mitigated by the significant financial pressures now facing competitors with massive sunk costs.

- The main opportunity has evolved from chasing large federal grants to leveraging state-level policies and integrating DAC with economically viable industrial assets, creating a more sustainable business model.

- The primary threat has shifted from being outpaced by competitors to the systemic instability of the megaproject funding model, a market-wide risk that ironically validates a more cautious strategy.

Table: SWOT Analysis for Southern Company’s DAC Strategy

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Low-risk entry via partnerships and small-scale federal grants ($3 M FEED study for SEDAC Hub). Strong regional presence. | Execution of a resilient, capital-light strategy through targeted pilots (Aircapture) and functional partnerships (Monroe Sequestration). | The cautious strategy was validated as a strength when the federal funding environment for megaprojects became highly uncertain in late 2025. |

| Weakness | No large-scale projects initiated. Lagging behind first-movers like Occidental in deployed capacity and operational timelines. | Still no commercial-scale capacity online. Dependent on the technological and execution success of partners like 8 Rivers and Aircapture. | The weakness of being a “fast follower” was confirmed, but the associated risk was reduced as first-movers faced significant funding threats. |

| Opportunity | Secure a portion of the DOE’s $1.2 B+ DAC Hubs program for large-scale construction of the SEDAC Hub. | Leverage state-level cost recovery mechanisms to fund projects. Integrate DAC with economically viable assets like biofuels plants to create new revenue streams. | The strategic focus shifted from relying on singular, large federal grants to building more resilient, integrated business models independent of federal funding volatility. |

| Threat | Competitors like Occidental and Climeworks were building at a scale and pace that threatened to make them the market-dominant players. | The entire megaproject funding model became a systemic risk, with the DOE’s review of $7.5 B in grants threatening the viability of the largest DAC hubs. | The primary external threat shifted from direct competitors to market-wide policy and funding instability, which disproportionately impacts capital-intensive projects. |

2026 Outlook: From Feasibility Studies to Final Investment Decisions

The most critical strategic action for the DAC sector in 2026 will be the transition from feasibility studies and pilots to final investment decisions (FIDs) on commercial-scale projects, particularly for cautious players like Southern Company. The results from 2025 pilots will determine whether these companies commit significant capital and move from a “watch and learn” posture to active construction, reshaping the competitive environment.

DAC Market Set for Strong Post-2025 Growth

This market forecast quantifies the significant growth expected from 2026 onward, reinforcing the section’s focus on the importance of upcoming final investment decisions.

(Source: The Business Research Company)

- If the Georgia Power pilot with Aircapture and the SEDAC Hub FEED study yield positive results on cost and performance, watch for an FID announcement from Southern Company in late 2026 for its first commercial-scale DAC facility. This would likely be an integrated project, such as with the planned Louisiana biofuels plant, rather than a standalone facility.

- The allocation of the DOE’s remaining $800 million in DAC Hub funding is a key external catalyst. An award to the SEDAC Hub for Phase 2 construction would significantly accelerate Southern Company’s timeline and validate the regional, partnership-based hub model on a national level.

- Conversely, if the 2025 pilot results are disappointing or federal support is withdrawn entirely, expect players like Southern Company to remain in a holding pattern. This would leave the market to first-movers like Occidental, which would face immense pressure to prove the economic viability of their megaprojects without broad market participation and with uncertain long-term policy support.

Frequently Asked Questions

What are the two main commercialization strategies for Direct Air Capture (DAC) discussed in the article?

The article identifies two distinct strategies. The first is the capital-intensive “megaproject model,” which involves building massive, standalone, megaton-scale plants, exemplified by Occidental’s Stratos facility. The second is the “cautious regional hub model,” which focuses on smaller, regionally integrated pilot projects driven by partnerships with specialized companies, as demonstrated by Southern Company’s approach.

Why is the regional hub model considered more resilient than the megaproject model?

The regional hub model is considered more resilient primarily because it is a capital-light, lower-risk approach. It relies on smaller, diversified funding sources like partnerships, modest federal grants for studies, and state-level cost recovery mechanisms. This insulates it from the volatility of large-scale federal funding, which has become a significant risk for megaprojects that are wholly dependent on massive grants, as highlighted by the potential termination of major DOE awards in late 2025.

How has the role of partnerships in the DAC sector evolved?

Before 2025, partnerships were typically broad consortiums formed to secure large federal grants for feasibility studies, like the initial SEDAC Hub group. By 2025, they evolved into more focused, functional alliances designed for project execution. Examples include Southern Energy partnering with Monroe Sequestration Partners for CO2 storage and Georgia Power collaborating with Aircapture to test a specific technology, demonstrating a shift from fundraising to building operational value chains.

Which companies are leading these different DAC strategies?

Occidental, through its subsidiary 1 Point Five, is leading the megaproject strategy. It is constructing the billion-dollar Stratos facility in Texas and vertically integrated by acquiring its technology provider, Carbon Engineering. Southern Company is the primary example of the cautious, regional hub strategy, pursuing smaller pilots with partners like Aircapture and engaging in FEED studies for projects like the SEDAC Hub.

What is the critical next step for the DAC industry in 2026?

According to the outlook, the most critical step for the DAC sector in 2026 is the transition from feasibility studies and pilots to making Final Investment Decisions (FIDs) on commercial-scale projects. The performance and cost data from the 2025 pilots will determine whether cautious players like Southern Company commit significant capital to move from a ‘watch and learn’ phase into active construction, which would significantly reshape the competitive landscape.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.