Alberta’s Carbon Strategy 2026: Why Near-Term CCUS Hubs Are Eclipsing DAC Projects

CCUS vs. DAC Adoption: How Alberta’s Carbon Capture Projects Are Diverging

Analysis of 2025 market activity reveals a strategic split in carbon capture adoption, with capital and government support prioritizing commercially ready point-source Carbon Capture, Utilization, and Storage (CCUS) projects for immediate industrial decarbonization, while Direct Air Capture (DAC) initiatives focus on technology validation in parallel innovation hubs.

- In 2025, the market clarified its approach, moving from the broad hub concepts of 2021-2024, such as the proposed Pathways Alliance, to funding specific, executable projects like the Bow Valley Carbon Hub. This project, a joint venture between Inter Pipeline Ltd. and Entropy Inc., exemplifies the focus on point-source capture from existing industrial facilities like the Cochrane Gas Plant.

- The primary risk for investors and strategists is misinterpreting this trend and conflating point-source CCUS with DAC. While both are forms of carbon management, Bow Valley Carbon’s model is about mitigating existing emissions at their source, a fundamentally different and more economically viable near-term strategy than removing diffuse CO 2 from the atmosphere.

- The emergence of dedicated DAC facilities in 2025, such as Deep Sky’s new innovation center in Innisfail, Alberta, confirms this strategic divergence. Instead of large-scale removal, its purpose is to test and commercialize multiple DAC technologies side-by-side, signaling that DAC is still in a pre-commercial, technology-proving phase, unlike the deployment-ready modular CCUS technology used by Entropy Inc.

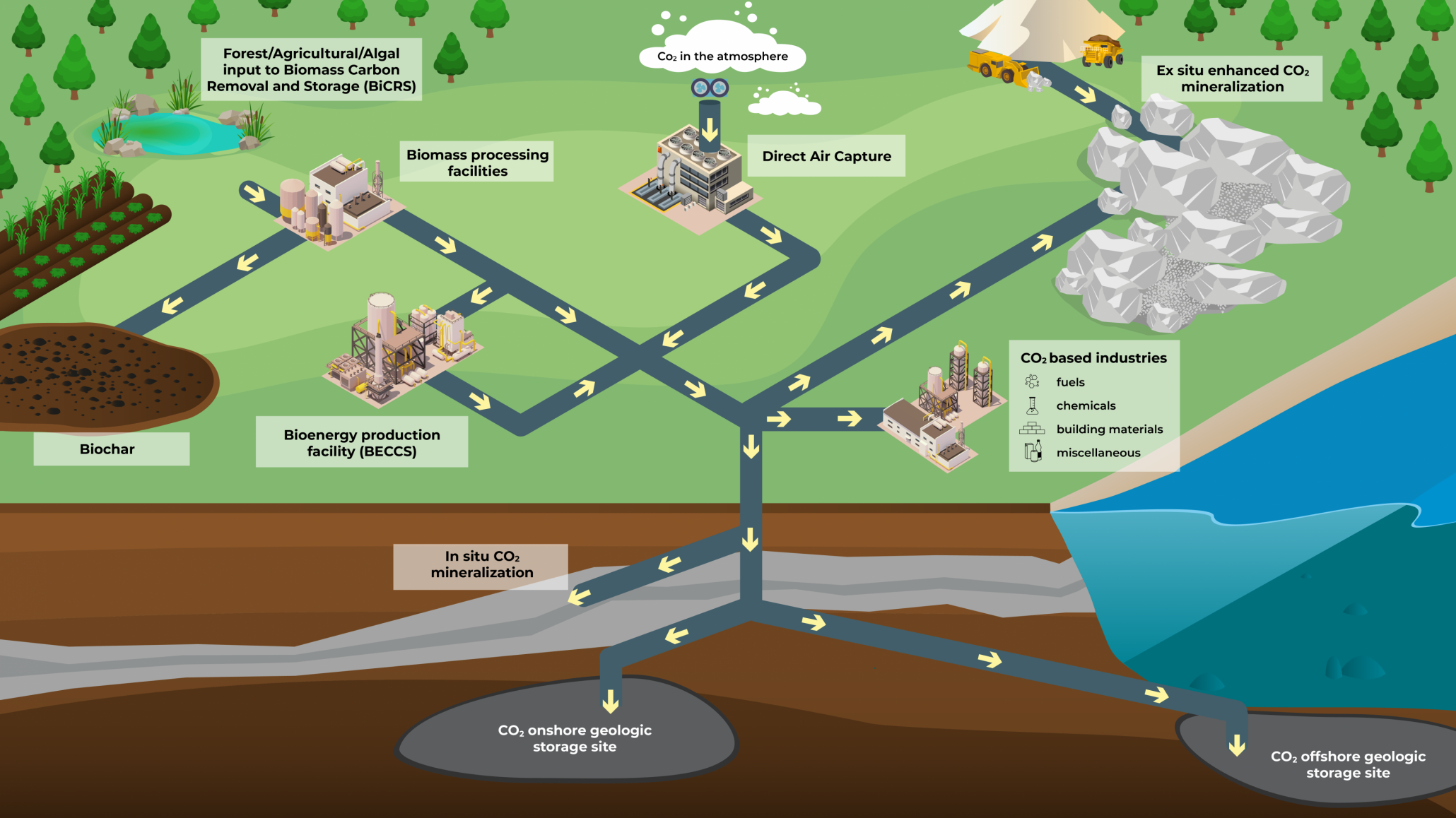

Canada’s Carbon Management Pathways Visualized

This diagram illustrates the different technological paths for carbon management, including Direct Air Capture and geologic storage (CCUS), providing high-level context for the article’s focus on the strategic split between them.

(Source: Natural Resources Canada – Canada.ca)

Carbon Capture Investment Analysis: Federal Funding Backs Point-Source Projects

Canadian government investment in 2025 decisively favors de-risking tangible, near-term point-source CCUS projects through direct funding and substantial tax credits, establishing a clear financial pathway for industrial decarbonization over speculative DAC ventures.

- The Government of Canada allocated a $21.5-million funding pool in July 2025 across five Alberta-based CCUS projects, including the Bow Valley Carbon initiative. This direct investment is targeted at front-end engineering and design (FEED) studies, a critical step to move projects toward a final investment decision.

- The financial viability of projects like the Bow Valley Carbon Hub is further secured by Canada’s national CCUS Investment Tax Credit (ITC). This policy provides a 50% refundable credit on capital for capture equipment and 37.5% for transportation and storage, significantly lowering the financial barrier for industrial players.

- This focused public funding contrasts with the broader, more volatile venture capital trends seen in the DAC space. While DAC saw peak VC funding in 2022, projections for 2025 showed a significant downturn, indicating that government-backed industrial partnerships are currently the more stable investment pathway in carbon management. Similar to how large energy players like Shell’s Top 10 AI Projects for 2025 Unveiled leverage technology, these CCUS projects rely on proven engineering.

Table: Canadian Carbon Capture Investments and Incentives (2025)

| Recipient / Program | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Federal Green Tax Credits | 2025-2026 | A $93 Billion pool of federal tax credits, including the CCUS ITC, designed to reduce costs for green initiatives by 30-75% and drive private investment. | Bomcas |

| Bow Valley Carbon & 4 Others | July 4, 2025 | Selected as a recipient from a $21.5 Million shared pool from Natural Resources Canada to support engineering and development of carbon capture projects in Alberta. | The Globe and Mail |

| Bow Valley Carbon | July 4, 2025 | Received a portion of the federal funding pool specifically to finance the design of a CO 2 compression system, pipeline, and sequestration well for its demonstration project. | Natural Resources Canada |

Strategic Alliances in Alberta: The Bow Valley Carbon Partnership Model

The Bow Valley Carbon project’s success is built on a vertically integrated partnership model that combines an emissions source, technology provider, and infrastructure operator, a pragmatic structure designed for near-term execution that stands in contrast to the open, multi-technology platform model used by emerging DAC hubs.

Visualizing the Direct Air Capture Value Chain

This chart illustrates the multi-partner DAC hub model, providing a direct visual contrast to the vertically integrated CCUS partnership structure used by the Bow Valley project as described in the text.

(Source: MarketsandMarkets)

- The core of the initiative is the Bow Valley Carbon Cochrane Limited Partnership, a strategic joint venture formed between midstream operator Inter Pipeline Ltd. and technology firm Entropy Inc. This structure internalizes the value chain: Inter Pipeline provides the CO 2 source from its Cochrane Gas Plant and operational expertise, while Entropy Inc. supplies its proven modular capture technology.

- Crucial public-private partnerships underpin the project’s viability. The Government of Alberta granted the partnership exclusive rights to develop an 853 km² pore space for sequestration, while the Government of Canada provided funding to de-risk the initial engineering and design phases in July 2025.

- This closed-loop, full-chain partnership model differs significantly from that of Deep Sky’s DAC innovation center, which partners with multiple competing technology vendors simultaneously. Deep Sky’s approach is designed for technology discovery and validation, whereas the Bow Valley Carbon model is structured for immediate commercial deployment and risk mitigation.

Table: Key Carbon Capture Partnerships in Alberta (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Bow Valley Carbon & Inter Pipeline Ltd. / Entropy Inc. | Active in 2025 | A joint venture where Inter Pipeline provides the source CO 2 and midstream expertise, and Entropy Inc. provides the modular capture technology for a full-chain CCUS project. | Entropy Inc. |

| Deep Sky & Multiple Technology Vendors | September 29, 2025 | Deep Sky launched a cross-technology innovation hub, partnering with various DAC companies to host and test their technologies side-by-side in real-world conditions. | CTV News |

| Bow Valley Carbon & Government of Canada | July 4, 2025 | A funding partnership where the federal government provides capital to support the front-end engineering and design (FEED) study, de-risking the project for private investors. | Government of Canada |

| Bow Valley Carbon & Government of Alberta | Active in 2025 | A regulatory partnership where the provincial government awarded the rights to an 853 km² pore space, granting the legal authority to develop a carbon sequestration hub. | Cochrane Eagle |

Alberta’s Carbon Capture Geography: Hubs Emerge Around Industrial Clusters

Alberta solidified its position as North America’s central geography for carbon capture development in 2025, with project locations strategically concentrated around existing industrial infrastructure in areas like Cochrane and Innisfail, demonstrating a pragmatic focus on leveraging established assets.

Map Shows Alberta’s Carbon Project Concentration

This map directly supports the section’s focus on geography by showing the location of Canada’s carbon projects and visually confirming the heavy concentration of activity in Alberta’s industrial clusters.

(Source: Natural Resources Canada – Canada.ca)

- The Bow Valley Carbon Hub is centered around the Cochrane Gas Extraction Plant, northwest of Calgary. This location was chosen to minimize transportation costs and leverage Inter Pipeline’s existing industrial footprint, a strategy reflecting a shift from the geographically vast but conceptual proposals of 2021-2024 to specific, asset-centric projects.

- Similarly, Deep Sky chose Innisfail, Alberta, for its DAC innovation center, a location that provides access to the necessary energy infrastructure and a supportive regulatory environment for testing new carbon removal technologies under real-world Canadian climate conditions.

- The Government of Alberta is the key enabler of this geographic concentration, awarding pore space tenure for carbon sequestration. The 853 km² grant to the Bow Valley Carbon partnership is a prime example of the province actively curating the development of sequestration hubs in geologically suitable areas close to emission sources.

CCUS Technology Maturity: Modular Deployment vs. DAC Experimentation in 2026

The 2025 carbon capture landscape reveals a clear divide in technology maturity: point-source CCUS has advanced to scalable, modular deployment, while Direct Air Capture remains in a technology validation phase, with projects focused on testing and de-risking multiple unproven methods.

- The technology at the heart of the Bow Valley Carbon Hub is Entropy Inc.’s modular CCUS system. This approach uses pre-engineered, skid-mounted units, which signifies a mature technology ready for rapid and repeatable deployment at industrial sites, moving beyond the large, bespoke projects that characterized the sector in the early 2020 s.

- In sharp contrast, the most significant DAC development in 2025 was the launch of the Deep Sky Alpha facility. Its purpose is not mass capture but to serve as a “cross-technology innovation center, ” concurrently testing various DAC approaches like solid sorbent and liquid solvent systems to determine their real-world performance and commercial viability.

- This technological divergence confirms that point-source capture is a commercially ready solution for near-term industrial decarbonization, leveraging decades of development in technologies like amine scrubbing. Meanwhile, DAC is still in a necessary but earlier stage of its lifecycle, focused on innovation and cost reduction before it can be deployed at a climate-relevant scale, a challenge not unlike the one faced in Methanol Bunkering 2026: An Uphill Battle Against LNG.

SWOT Analysis: Bow Valley Carbon’s Position in the 2026 Energy Market

The Bow Valley Carbon initiative’s strengths lie in its de-risked commercial model and strong partnerships, but its identity as a point-source CCUS project creates a potential weakness in a market often captivated by DAC, while its greatest opportunity is to become a foundational sequestration service provider for the broader carbon economy.

Chart Details CO2 Utilization Pathways

This chart details the various commercial uses for captured CO2, which visually explains the ‘Opportunity’ for the Bow Valley project to serve a broader carbon economy as identified in the SWOT analysis.

(Source: Natural Resources Canada – Canada.ca)

- Strengths: The project’s structure, which combines an existing emissions source (Inter Pipeline’s plant), proven modular technology (Entropy Inc.), and government financial backing, represents a low-risk, executable model.

- Weaknesses: Its classification as a point-source CCUS project, while pragmatic, may cause it to be overlooked by investors and policymakers focused on the more aspirational narrative of atmospheric carbon removal via DAC.

- Opportunities: The vast 853 km² sequestration hub offers a significant opportunity to evolve into a multi-user “sequestration-as-a-service” platform, potentially serving third-party emitters and future DAC facilities.

- Threats: The project’s timeline is critically dependent on securing a final Carbon Sequestration Agreement from the Alberta government, and any delay poses a significant risk.

Table: SWOT Analysis for Alberta’s Carbon Hub Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Broad industrial alignment (e.g., Pathways Alliance). Strong political will for CCS. | Vertically integrated partnerships (Inter Pipeline & Entropy). Federal funding confirmed. Proven modular CCUS technology. | Strategy shifted from broad conceptual alliances to tangible, funded projects with specific technology partners and emission sources, validating a more de-risked approach. |

| Weaknesses | High capital cost of shared infrastructure. Vague project timelines and financial commitments. | Focus on point-source CCUS, which lacks the carbon removal narrative of DAC. Project success is tied to a single industrial asset initially. | The market is bifurcating. While point-source is more mature, it may struggle to attract “pure-play” climate tech investors focused on atmospheric removal. |

| Opportunities | Potential to create large, multi-user sequestration hubs serving entire industrial regions. | Commercialize a sequestration hub (853 km²) as a service for third parties. Become foundational infrastructure for future DAC projects needing storage. | The “hub” concept was validated by the award of pore space rights. The opportunity now is to monetize that asset beyond the anchor tenant, creating a new business model. |

| Threats | Regulatory uncertainty around long-term liability for stored CO 2. Public and Indigenous community opposition. | Delays in securing the final Carbon Sequestration Agreement (expected Q 4 2025). Competition from other hubs. Policy shifts favoring DAC. | The critical path has narrowed to a specific regulatory milestone. The main threat is no longer conceptual but administrative, revolving around final government sign-off. |

2026 Outlook: Sequestration Agreements as the Critical Milestone for Carbon Hubs

The primary trajectory for Alberta’s carbon capture sector in 2026 hinges on the execution of formal Carbon Sequestration Agreements; if these agreements are finalized, it will trigger final investment decisions and construction, solidifying the province’s hub-based infrastructure model.

Pathways Project Highlights Alberta CCUS Scale

This chart illustrates the massive potential sequestration capacity of Alberta’s major hub projects, reinforcing the significance of the Final Investment Decisions and future infrastructure scale discussed in the 2026 outlook.

(Source: Chinook Consulting Services)

- If the Bow Valley Carbon partnership secures its final Carbon Sequestration Agreement from the Alberta government, as anticipated in late 2025, watch for a Final Investment Decision (FID) in early 2026. This would signal the start of construction for the compression system, pipeline, and injection well.

- This could be happening because both federal and provincial governments are aligning policy and funding to fast-track shovel-ready industrial decarbonization projects. The success of Bow Valley Carbon would validate this pragmatic approach and likely accelerate similar point-source projects across Canada.

- Conversely, if regulatory approvals are delayed, watch for a potential cooling of investor interest in the hub model, as it would signal persistent administrative risk. This could shift momentum back toward smaller, standalone projects or different technology pathways. The long-term vision of a broad energy transition, similar to the challenges faced in Battery Storage 2026: The #1 Energy Investment Choice, depends on clearing these regulatory hurdles.

- The key signal gaining traction is the evolution of CCUS projects from single-user emission mitigation to multi-user infrastructure platforms. Monitor announcements from Bow Valley Carbon regarding third-party service agreements, as this will confirm its transition into a true sequestration hub operator.

Frequently Asked Questions

What is the main difference between the CCUS and DAC projects mentioned in the article?

The article explains that point-source CCUS projects, like the Bow Valley Carbon Hub, capture CO₂ directly from an industrial source (e.g., a gas plant) to mitigate existing emissions. This technology is described as commercially ready and deployment-ready. In contrast, Direct Air Capture (DAC) projects, such as Deep Sky’s innovation center, focus on removing diffuse CO₂ directly from the atmosphere and are still in a pre-commercial, technology-proving phase.

Why is the Canadian government prioritizing funding for point-source CCUS?

The Canadian government is prioritizing point-source CCUS because it is a mature, tangible technology that offers an immediate pathway for industrial decarbonization. The article highlights that direct funding, like the $21.5-million pool, and incentives like the CCUS Investment Tax Credit are designed to de-risk these shovel-ready projects and secure a stable investment pathway for reducing emissions from existing industrial facilities.

What is the Bow Valley Carbon Hub?

The Bow Valley Carbon Hub is a point-source carbon capture project in Alberta, formed as a joint venture between Inter Pipeline Ltd. and technology provider Entropy Inc. The project captures CO₂ from Inter Pipeline’s Cochrane Gas Plant using Entropy’s modular technology and plans to store it in an 853 km² underground pore space granted by the Alberta government.

What is the most significant hurdle for projects like Bow Valley Carbon in 2026?

According to the article’s outlook, the most critical hurdle is securing a final Carbon Sequestration Agreement from the Alberta government. Finalizing this agreement is expected to trigger a Final Investment Decision (FID) and the start of construction. Any delay in this regulatory step is identified as a significant threat to the project’s timeline and investor confidence.

How does the partnership model for the Bow Valley Carbon Hub differ from Deep Sky’s DAC hub?

The Bow Valley Carbon Hub uses a vertically integrated, closed-loop partnership model between an emissions source (Inter Pipeline) and a single technology provider (Entropy Inc.), a structure designed for immediate commercial deployment. In contrast, Deep Sky’s DAC hub uses an open, multi-technology platform model, partnering with multiple competing vendors to test and validate their different technologies side-by-side, which is suited for technology discovery rather than commercial operation.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.