Woodside Energy CCUS, $5.7 B Stonepeak Deal, $200/Tonne Cost Gap, and 4 Key Projects (2021 to 2025)

CCUS Project Risk, Woodside $200/Tonne Cost Gap

Woodside Energy’s 2025 strategy exposes a fundamental economic constraint for large-scale carbon capture projects, where development costs vastly exceed current policy incentives, making widespread adoption dependent on future financial or technological shifts. While the company advanced major carbon capture and storage (CCS) initiatives, its leadership openly acknowledged a significant viability gap that defines the primary risk for its decarbonization pathway. This marks a strategic shift from the planning and smaller-scale offset activities seen between 2021 and 2024 to a direct confrontation with the economic realities of deploying CCS at a commercial scale.

- In April 2025, Woodside CEO Meg O’Neill stated that the cost of carbon capture for LNG plants is between $US 200 and $US 500 per tonne. This figure is more than double the company’s internal carbon price of US$80 per tonne and well above the leading U.S. 45 Q tax credit, which offers up to $85 per tonne for stored CO 2.

- Despite the stated high costs, Woodside advanced major projects contingent on future CCS deployment. The company submitted its proposal for the Browse CCS project in Western Australia, which aims to capture over 4 Mtpa, and completed the appraisal campaign for the Bonaparte CCS project in Northern Australia.

- This economic gap forces Woodside to pursue a dual strategy. It relies on more immediate and cost-effective measures like carbon credits to meet near-term targets, such as its goal of a 15% reduction in Scope 1 and 2 emissions by 2025, while positioning its large CCS projects as long-term options that require a different economic environment to proceed.

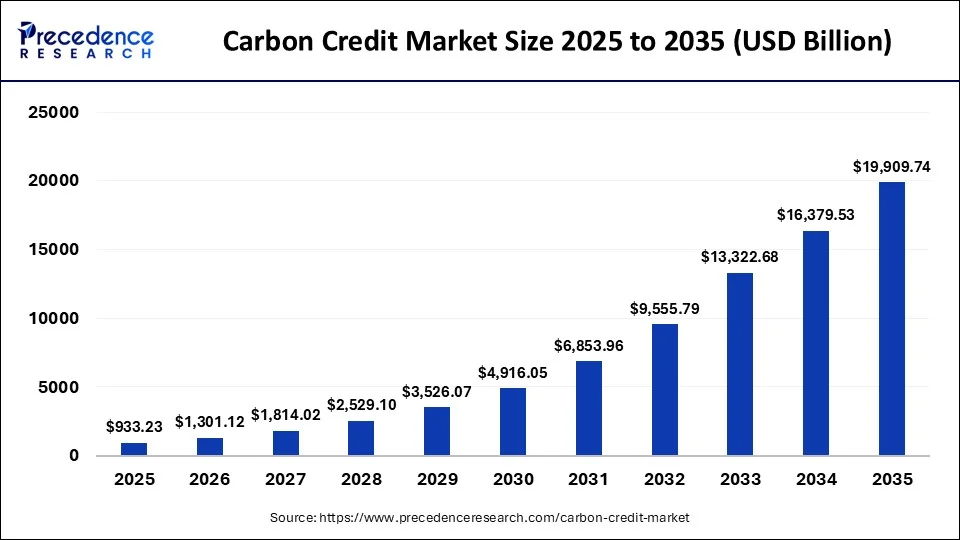

Carbon Credit Market to Near $20 Trillion by 2035

This chart’s projection of a multi-trillion dollar carbon credit market provides the strategic context for Woodside’s CCUS investments, suggesting that the long-term value of carbon credits could offset and eventually overcome the current ‘$200/Tonne Cost Gap’ associated with the technology.

(Source: Precedence Research)

$15.9 B in LNG, Woodside Capital Allocation Strategy

In 2025, Woodside’s capital allocation strategy demonstrated a clear prioritization of its core LNG business, with new energy investments representing a comparatively small portion of its overall spending. This approach underscores a strategy where CCS and lower-carbon initiatives primarily serve as enablers for new and existing fossil fuel assets rather than a wholesale replacement of the company’s business model. The scale of investment in traditional projects dwarfs the capital targeted for the energy transition.

- The most significant financial commitment made in 2025 was the Final Investment Decision (FID) for the $18 billion Louisiana LNG project. This single investment in new fossil fuel infrastructure is more than three times the company’s entire 2030 target for new energy spending.

- Woodside has a stated target to invest US$5 billion in new energy products and lower-carbon services by 2030. This figure, spread over several years, highlights a cautious approach to the energy transition, especially when compared to its broader project pipeline.

- The company’s overall capital discipline is oriented around a $39 billion project pipeline announced in August 2025, which is heavily weighted towards traditional oil and gas developments. This focus confirms that shareholder returns are expected to be driven primarily by the core business for the foreseeable future.

Fossil Fuels Retain Dominance in Global Energy Mix

This chart supports Woodside’s significant capital allocation to LNG by illustrating the continued dominance of fossil fuels in the global energy mix, justifying major investments in core assets while simultaneously pursuing decarbonization strategies like CCUS.

(Source: REN21)

Table: Woodside Energy Major Capital Investments (2025)

| Project / Initiative | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| New Energy & Lower-Carbon Services | Target by 2030 | Company-wide target to invest $5 billion in new energy products, including CCUS and hydrogen, to support long-term transition. | Woodside Energy |

| Total Project Pipeline | Announced Aug 2025 | Focus on a $39 billion project pipeline, scaling back new exploration to strengthen the balance sheet and focus on prioritized assets. | Reuters |

| Louisiana LNG Development | FID Apr 2025 | Final investment decision for the $18 billion, 16.5 Mtpa LNG project. Investment partners significantly reduced Woodside‘s direct capital exposure. | The Guardian |

Woodside 4 Key Partnerships, Stonepeak and Aramco

To de-risk the immense capital requirements of its LNG expansion and new energy ventures, Woodside aggressively secured strategic partnerships in 2025. These alliances served not only to offload billions in capital expenditure but also to secure technical expertise and market access, validating the projects for the broader market. This collaborative model is central to advancing projects that would be too financially burdensome for Woodside to undertake alone.

- For its Louisiana LNG project, Woodside brought in financial partners to shoulder a significant portion of the cost. Stonepeak contributed $5.7 billion for a 40% interest, while Williams invested $1.9 billion, reducing Woodside‘s net capital expenditure from $17.5 billion to under $10 billion.

- In May 2025, Woodside signed a collaboration agreement with Aramco. The deal explores a potential equity investment by Aramco in the Louisiana LNG project and includes provisions for LNG offtake, securing a key potential customer.

- To support its new energy ambitions, Woodside partnered with Linde to secure a supply of low-carbon hydrogen for its Beaumont New Ammonia plant in Texas. For technology development, it partnered with Baker Hughes to explore commercializing an industrial-scale low-carbon power plant.

- For foundational research, Woodside continued its partnership with Monash University, focusing on advancing Direct Air Capture (DAC) and Carbon Capture and Utilisation (CCU) technologies toward industrial deployment.

Aramco Ranked World’s Top Corporate Emitter

This chart provides critical context for Woodside’s partnership with Aramco, highlighting the partner’s significant emissions profile and underscoring the strategic imperative and scale of joint decarbonization efforts through technologies like CCUS.

(Source: InfluenceMap)

US vs Australia, Woodside Geographic Project Focus

In 2025, Woodside Energy‘s decarbonization strategy became geographically concentrated in two key jurisdictions: Australia for developing large-scale CCS hubs and the U.S. Gulf Coast for producing new lower-carbon commodities. This dual-region focus allows the company to leverage specific local advantages, including favorable geological storage formations in Australia and powerful policy incentives like the Inflation Reduction Act in the United States. This represents a consolidation from more exploratory activities between 2021 and 2024 into two strategic hubs for execution.

- In Australia, Woodside is focused on creating CCS hubs to decarbonize its extensive natural gas operations. Key projects include the proposed Browse CCS project offshore Western Australia and the Bonaparte CCS project in the Timor Sea, both of which leverage depleted gas reservoirs for CO 2 storage.

- In the United States, Woodside is capitalizing on mature infrastructure and strong policy support. Its Louisiana LNG project and the Beaumont New Ammonia facility in Texas are strategically located to benefit from the $85/tonne 45 Q tax credit, skilled labor, and access to global export markets.

CCUS Commercial Scale, Woodside Technology Maturity

Woodside’s 2025 portfolio reveals a clear separation between technically mature CCS applications for its own facilities and earlier-stage technologies for new markets, with economics being the primary barrier to commercial scale. Although the technology to capture CO 2 from LNG and ammonia plants is well-understood, its deployment at the scale required for projects like Browse is constrained by the significant cost-incentive gap. This is a crucial shift from the 2021-2024 period, where the focus was on technical feasibility; the challenge in 2025 is economic viability at scale.

- Commercially Ready but Economically Challenged: The technology for the proposed Browse CCS project and the Beaumont New Ammonia plant (designed for 95% CO 2 capture) is considered commercially ready. However, the high costs cited by the company make these projects difficult to sanction without higher carbon prices or subsidies.

- Commercialization Stage: The partnership with Baker Hughes to explore the Net Power cycle for a low-carbon industrial power plant is in the commercialization phase. This aims to create a business case for a technology that has been demonstrated but not yet widely deployed.

- Pilot and Research Stage: Technologies like Direct Air Capture (DAC) remain at a much earlier stage. Woodside‘s partnership with Monash University aims to move DAC from the lab toward pilot-scale operations, indicating it is not yet considered a near-term solution for the company’s emissions.

Chart Models Technology Adoption S-Curve for CCUS

This chart directly visualizes the theme of technology maturity, placing CCUS on a typical adoption S-curve. This helps illustrate its current stage of development and its trajectory towards becoming a commercially scaled solution, as discussed in the section.

(Source: Nature)

SWOT Analysis, Woodside Strengths and Economic Risks

In 2025, Woodside‘s primary strength was its ability to fund its transition strategy from a profitable LNG business, while its main weakness was the unfavorable economics of its flagship decarbonization technology, CCS. The changing policy landscape presented both opportunities and threats, with new incentives unable to bridge the gap exposed by the high costs of large-scale projects.

Decarbonization Imperatives Drive Industrial Client Demand

This chart frames a key external factor for the SWOT analysis, illustrating how decarbonization pressures create strong client demand. This trend represents a significant ‘Opportunity’ for Woodside’s CCUS business and a ‘Threat’ to its traditional operations if unaddressed.

(Source: MarketsandMarkets)

Table: SWOT Analysis for Woodside CCUS Strategy (2021-2025)

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Strong balance sheet from legacy oil and gas assets. Established technical expertise in large-scale offshore projects. | Secured major partnerships (Stonepeak, Williams) to de-risk $18 B Louisiana LNG project. Advanced large CCS projects (Browse, Bonaparte) to appraisal stage. | The company validated its ability to leverage its financial strength and project expertise to attract partners and advance a multi-billion-dollar pipeline, even in new energy sectors. |

| Weaknesses | Rising Scope 1 & 2 emissions from expanded operations post-BHP merger. Reliance on carbon offsets for compliance. | CEO publicly stated CCS costs of $200-$500/tonne, confirming a major economic viability gap and making it “too expensive” for shareholders. | The economic weakness of CCS as a primary decarbonization tool was validated. The strategy’s dependence on factors outside the company’s control (carbon price, subsidies) became explicit. |

| Opportunities | Potential to leverage Australian geology for CCS hubs. Growing global demand for lower-carbon products like ammonia and hydrogen. | U.S. 45 Q tax credits (up to $85/tonne) directly support the business case for the Beaumont New Ammonia plant. Public comment period opened for Browse, a key step toward regulatory approval. | The opportunity presented by U.S. policy became concrete, driving investment in the Gulf Coast. However, the 45 Q credit was also shown to be insufficient for abating LNG emissions. |

| Threats | Regulatory uncertainty and opposition from environmental groups for new fossil fuel projects and CCS. Volatility in global energy markets. | Passage of the “One Big Beautiful Bill Act” (OBBBA) in the US introduced a future phase-out of 45 Q credits, creating timeline pressure. Continued opposition to the Browse project. | The threat of changing policy became a tangible risk with the OBBBA, highlighting that even the most favorable policy environments are not permanent. Regulatory and social license hurdles remain a constant threat. |

Woodside Scenario, Carbon Price Impact on CCS FID

The single most critical variable for Woodside‘s large-scale CCS strategy is the future carbon price. If prices and incentives fail to rise substantially to close the $200+/tonne viability gap, the company will likely delay Final Investment Decisions on major CCS hubs like Browse and lean more heavily on carbon credits and smaller-scale abatement projects to meet its near-term climate targets.

- If This Happens: A significant increase in the global carbon price or a major enhancement of Australian CCS policy incentives occurs.

- Watch This: Woodside fast-tracks a Final Investment Decision for the Browse CCS or Bonaparte CCS projects, signaling that the economic hurdles have been cleared.

- This Could Be Happening: Announcements of breakthroughs from the Baker Hughes partnership that dramatically lower the cost of capture technology could also trigger an FID, even without a major policy shift.

- If This Happens: The carbon price remains stagnant, and CCS costs do not fall.

- Watch This: Woodside continues to advance CCS projects to key engineering gates but repeatedly delays FIDs, citing unfavorable market conditions. The company’s reliance on purchasing carbon offsets (ACCUs) will likely increase to meet compliance obligations.

- This Could Be Happening: The company pivots capital toward projects with more direct economic returns, such as expanding its lower-carbon ammonia business, while its largest CCS ambitions remain on hold.

High Prices for Carbon Removal Credits Revealed

This chart provides the essential data for the scenario analysis in this section. It shows that high prices for carbon credits are a market reality, directly influencing the financial modeling that determines whether a carbon capture project achieves a positive Final Investment Decision (FID).

(Source: CarbonCredits.com)

The questions your competitors are already asking

This report covers one angle of Woodside Energy’s path to commercial-scale carbon capture. The questions that matter most depend on your work.

- What is actually happening with Woodside’s Browse and Bonaparte CCS projects since their appraisal campaigns?

- What is the outlook for CCS deployment in the LNG sector, given the $200/tonne viability gap highlighted by Woodside?

- What is the cost breakdown of a CCS system for an LNG plant that results in a cost of over $200 per tonne?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.