Advanced Reactor Supply Chain Risk, 300 GW Gap, 7-Year Vogtle Delay, and 4-Year NRC Permits (2021-2026)

US Nuclear Supply Chain Constraints Inhibit 400 GW Target

The U.S. national goal to quadruple nuclear capacity to 400 GW by 2050 is not constrained by technology or market demand, but by a severely atrophied domestic industrial base. Decades of limited new construction have eroded manufacturing capabilities, creating a “chicken-and-egg” paralysis where suppliers are unwilling to invest in new factories without a firm pipeline of reactor orders, and utilities are hesitant to place orders that cannot be fulfilled on time or budget. This supply chain gap, not technological readiness, is the primary impediment to bridging the 300 GW clean energy deficit needed to meet decarbonization and AI-driven electricity demand.

- Between 2021 and 2024, the completion of the Plant Vogtle expansion served as a stark reminder of supply chain risk. The 2.2 GW project was seven years late and $17 billion over budget, with an average construction cost overrun of 102.5% for nuclear plants, deterring investment in new large-scale reactors and keeping manufacturing capabilities dormant.

- The shift from 2025 to today has been defined by a surge in demand from data centers and a new federal policy targeting 400 GW, which has exposed profound weaknesses in the industrial base. The U.S. lacks sufficient domestic capacity for large forgings and other critical components, forcing reliance on a limited number of foreign suppliers.

- Advanced reactors, particularly SMRs, face a critical fuel bottleneck. These designs largely depend on High-Assay, Low-Enriched Uranium (HALEU), for which no commercial-scale production capacity currently exists in the U.S., potentially delaying the deployment of next-generation designs.

- The regulatory process remains a significant time constraint. New reactor designs can take up to four years to receive certification from the Nuclear Regulatory Commission (NRC), creating a lengthy and costly barrier before any supply chain mobilization can formally begin.

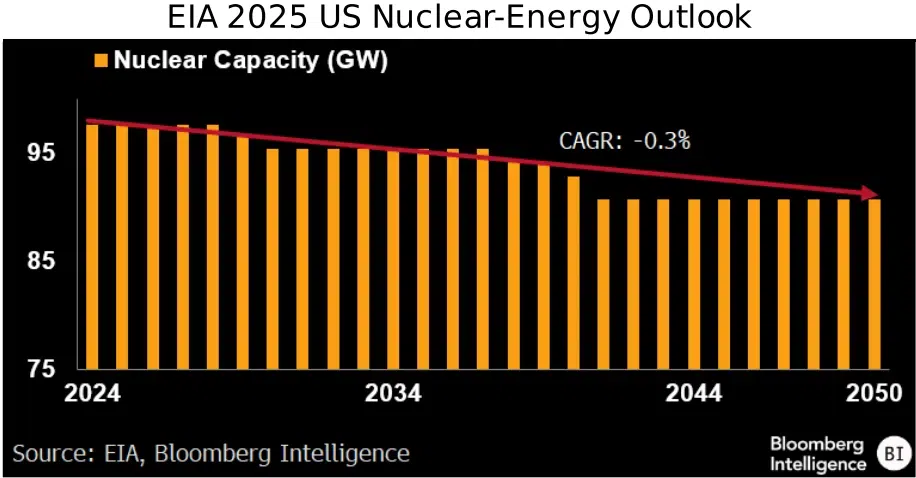

EIA Projects US Nuclear Capacity Decline

This section discusses the supply chain constraints inhibiting an ambitious 400 GW nuclear target in the US. The chart powerfully illustrates this challenge by showing that the current official projection is not for growth, but for a decline in capacity, highlighting the significant gap between the target and the current trajectory.

(Source: Bloomberg)

Investment in SMR Developers Surges, But Manufacturing Capacity Lags

While private capital is flowing into advanced nuclear development companies, this investment is directed at reactor design and commercialization, not the foundational, multi-billion-dollar re-industrialization of the manufacturing supply chain. The legislative uncertainty created by the 2025 “One Big Beautiful Bill Act” (OBBBA), which modifies or repeals certain Inflation Reduction Act (IRA) incentives, further complicates the long-term capital planning required for new component factories and forging facilities.

- Significant venture funding has validated the market potential of SMR developers. Terra Power raised $750 million to advance its projects, and X-energy secured $700 million in a November 2025 Series D funding round to support its Xe-100 SMR.

- Federal support through the Department of Energy’s Loan Programs Office (LPO) remains a critical instrument for de-risking first-of-a-kind projects. The UPRISE program, announced in March 2026, aims to add 5 GW of capacity from the existing fleet through low-cost financing for uprates and restarts, backed by $289 billion in loan authority.

- The OBBBA legislation introduced in 2025 alters the financial landscape. While it aims to support nuclear by restricting fuel sourcing from certain nations after 2027, its accelerated expiration of the Section 45 Y and 48 E tax credits for some renewables introduces instability that affects the economic calculus for all long-term energy investments, including nuclear.

Nuclear Lags as Solar and Wind Dominate Capacity Growth

The section describes a surge in investment for SMR developers that is not matched by manufacturing capacity. This chart visually depicts the ‘lag’ by showing how new nuclear capacity additions are dwarfed by solar and wind, underscoring the gap between investment/design and actual deployment.

(Source: pv magazine USA)

Table: Advanced Reactor Private and Public Investment (2025-2026)

| Company / Entity | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| U.S. Department of Energy (DOE) | Mar 2026 | Launched the UPRISE initiative to add 5 GW of capacity by 2029 from existing plants via uprates and restarts, supported by $289 billion in federal loan authority. | Power Magazine |

| X-energy | Nov 2025 | Secured $700 million in a Series D funding round to accelerate development and deployment of its Xe-100 SMR technology. | Neutron Bytes |

| Terra Power | Jun 2025 | Raised $750 million from private investors to fund the development and commercialization of its Natrium advanced reactor and other projects. | FTI Consulting |

Hyperscaler Partnerships Provide Demand Signal for New Nuclear Builds

A new commercial model is emerging where large technology companies, facing immense power demands from AI, are acting as anchor customers and strategic partners for nuclear projects. These agreements provide the long-term revenue certainty required to de-risk capital-intensive construction and send a crucial demand signal to the beleaguered supply chain. This marks a shift from the traditional model where utilities were the sole customers for new reactors.

- In August 2025, the Tennessee Valley Authority (TVA) signed the first U.S. utility Power Purchase Agreement (PPA) for Gen IV nuclear power, part of a three-way deal with Google and Kairos Power for output from the Hermes 2 reactor.

- X-energy and Amazon announced a strategic collaboration in August 2025 to develop a standardized deployment and financing model for SMRs, aiming to accelerate the delivery of clean power for AI infrastructure.

- Elementl Power and Google signed a development agreement in May 2025 to establish three project sites for advanced reactors, directly linking new nuclear development to data center energy needs.

- Meta has also been an active offtaker, with multiple agreements announced in 2025 to secure firm, carbon-free power from new nuclear projects for its growing data center fleet.

Nuclear Power Demonstrates Highest Capacity Factor

This section covers how partnerships with hyperscalers (data centers) are creating a demand signal for new nuclear builds. The chart provides the core rationale for this trend, as nuclear’s industry-leading capacity factor represents the 24/7 reliability that is critical for data center operations.

(Source: TSCS – Substack)

Table: Key Nuclear Offtake and Development Partnerships (2025-2026)

| Key Partner | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| X-energy, Amazon, KHNP, Doosan | Aug 2025 | Strategic partnership to accelerate and scale deployment of Xe-100 SMRs specifically for powering AI data centers and infrastructure. | X-energy |

| TVA, Google, Kairos Power | Aug 2025 | First-of-its-kind utility PPA for Gen IV nuclear power from the Hermes 2 reactor, directly connecting advanced nuclear output to a major tech offtaker. | Power Magazine |

| Elementl Power, Google | May 2025 | Development agreement to establish three project sites for advanced reactors to directly power data centers. | Nuclear Energy Institute |

U.S. Nuclear Expansion Concentrates in Pro-Nuclear States

While the 400 GW goal is a national ambition, practical deployment and supply chain development are concentrating in states with supportive regulatory environments, existing nuclear workforces, and significant industrial power needs. Activity prior to 2025 was almost exclusively centered on the Vogtle site in Georgia, but the new policy landscape is spurring development in a handful of other proactive states.

- Before 2025, Georgia was the sole focal point for new U.S. nuclear construction with the completion of Plant Vogtle units 3 & 4, demonstrating the immense challenge of executing a single, state-level project.

- From 2025 onward, activity has expanded to other regions. Terra Power selected Kemmerer, Wyoming, for its first Natrium reactor, while X-energy is developing a project with Dow in Seadrift, Texas, capitalizing on industrial decarbonization demand.

- The Southeast remains a critical hub, led by the TVA’s exploration of SMRs at its Clinch River site in Tennessee. In South Carolina, discussions have revived around restarting construction at the canceled V.C. Summer site, indicating renewed interest from utilities in established nuclear regions.

- States are taking proactive roles, exemplified by the Texas Advanced Nuclear Reactor Working Group. Its November 2024 report outlined a strategic plan to develop a robust in-state supply chain and streamline regulations to attract advanced reactor projects.

SMRs Are Commercially Unproven Despite Technological Advancement

Large-scale reactor technology is commercially mature but economically challenging for rapid deployment, while SMRs and advanced reactors remain commercially unproven at scale despite reaching key technological milestones. The period from 2021 to 2024 was marked by the high-profile failure of Nu Scale’s Carbon Free Power Project, a setback for SMR commercialization. Since 2025, specific designs are advancing through the regulatory pipeline, but no SMR has yet completed construction in the U.S., and the first commercial units are not expected until the late 2020 s or early 2030 s.

- The completion of Vogtle’s AP 1000 reactors confirmed the viability of Gen III+ technology but also its prohibitive cost and schedule overruns, effectively closing the door on a wave of similar large-scale, bespoke projects.

- Key enabling technologies for SMRs are maturing. In 2026, Fe Cr Al alloy cladding, which improves fuel performance and safety, reached Technology Readiness Level 7, with commercial deployment anticipated between 2027 and 2029.

- Despite this progress, SMRs have not yet overcome commercial hurdles. The four-year NRC certification process for new designs, coupled with supply chain immaturity, means that even the most advanced projects from companies like Rolls-Royce SMR and Terra Power are years from generating revenue.

- The primary value proposition of SMRs—cost reduction through factory-based modular construction and economies of scale—has not been validated. Projections of a 40% CAPEX reduction compared to large reactors remain theoretical until multiple units are built and deployed.

Chart Shows Decades-Long Hiatus in US Nuclear Construction

The section argues that SMRs, despite technological advances, remain commercially unproven. This chart provides direct historical evidence for this claim by illustrating the multi-decade pause in new U.S. nuclear construction, highlighting the lack of recent commercial deployment experience in the industry.

(Source: Yes Energy)

Table: SWOT Analysis for U.S. Nuclear Supply Chain Expansion

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Existing 100 GW fleet provided reliable baseload power. Established operational expertise. | Fleet continues to be the largest source of U.S. clean energy (18-20%). Bipartisan political support for nuclear grows. | The value of firm, 24/7 carbon-free power is validated by surging AI demand, making nuclear’s primary strength more valuable. |

| Weaknesses | Vogtle cost overruns and delays highlighted project execution risk. Supply chain was largely dormant. | Acute shortages in skilled labor and domestic forging capacity are exposed. HALEU fuel bottleneck becomes a critical path issue for SMRs. | The “chicken-and-egg” problem of supply chain investment is validated as the central barrier to scaling, with no resolution in sight. |

| Opportunities | Decarbonization goals created a theoretical market for new nuclear. SMR designs were in development. | AI data center demand creates a massive, immediate need for firm power. Tech giants like Google and Meta sign offtake agreements. | Market demand has shifted from theoretical (climate policy) to tangible and urgent (powering data centers), creating real commercial pull. |

| Threats | Competition from cheap natural gas and renewables. Public opposition and waste disposal issues. | Policy uncertainty from the OBBBA’s changes to IRA credits creates financial risk. High interest rates increase CAPEX sensitivity. | Political and financial risk is amplified. The potential for policy reversal every election cycle deters the long-term investment needed for factories. |

A Firm Order Book is the Critical Path to Nuclear Expansion

The single most critical action required to enable significant nuclear expansion is the materialization of a consistent, multi-unit order book for standardized SMR designs. Without a clear and bankable pipeline of firm reactor orders, manufacturers will not make the multi-billion-dollar, long-term capital investments required to build new factories, and the U.S. nuclear industrial base will remain incapable of supporting a large-scale build-out.

- The key signal to monitor is a shift from one-off project announcements to large, consolidated orders, such as a major utility or a consortium of buyers committing to ten or more standardized SMRs like the GE-Hitachi BWRX-300.

- Currently, a “self-reinforcing market paralysis” persists. Without a firm order book, component suppliers cannot secure financing to expand capacity, which in turn makes new reactor projects appear too risky for utilities to order.

- If a large, firm order is placed, watch for subsequent announcements of new domestic manufacturing facilities for heavy forgings, reactor pressure vessels, and other critical components, as well as new workforce training programs.

- If these orders do not materialize by 2027, the supply chain will not be able to ramp up in time. In this scenario, the 400 GW target will remain an aspiration, and actual new capacity additions by 2050 will likely be limited to a fraction of the 300 GW goal.

Global Nuclear Capacity Stagnates Below 400 GW

This section claims that a ‘firm order book’ is the critical path to expanding nuclear power. The chart illustrates the very problem that a firm order book would solve: global nuclear capacity has been stagnant for two decades, indicating new builds are barely keeping pace with retirements. New orders are required to break this trend.

(Source: Silvercrest Asset Management Group)

The questions your competitors are already asking

This report covers one angle of the supply chain bottlenecks hindering the US nuclear build-out. The questions that matter most depend on your work.

- What is the outlook for deploying 300 GW of new nuclear capacity by 2050, considering supply chain and permitting delays?

- Who are the key global suppliers for large forgings and other critical nuclear components, and what is their available capacity?

- What is the status of commercial-scale HALEU fuel production for advanced reactors?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.