AI Chip Shortage 2025: How Hardware Constraints Reshape Global Technology Deployment

Industry Risks 2025: How the AI Chip Shortage Creates Project Delays and Concentrates Market Power

The global surge in Artificial Intelligence has shifted the semiconductor shortage from a transient supply disruption into a structural market crisis, directly throttling AI adoption by inflating costs, delaying projects, and concentrating advanced capabilities within a few dominant technology firms.

- Between 2021 and 2024, the market grappled with broad chip shortages affecting industries like automotive, but the AI-specific hardware crunch was still nascent. Since January 1, 2025, the insatiable demand from AI data centers for advanced GPUs and High-Bandwidth Memory (HBM) has overwhelmed manufacturing capacity, creating a distinct and persistent bottleneck that defines the current market.

- The scarcity of critical components is now severe, with lead times for Nvidia‘s H 100 and A 100 GPUs extending up to six months. This is not a simple supply issue; major producers are completely sold out. SK Hynix has already sold its entire 2026 HBM chip output, and Micron Technology reports its AI-focused memory products are fully booked for the current year.

- This hardware deficit directly translates into significant economic drag, risking the delay of hundreds of billions of dollars in digital transformation projects. Businesses report that the inability to secure semiconductors has hindered the scalability of their AI initiatives, creating a clear chasm between the few hyperscalers with secured supply and the broader market facing costly delays.

- The prohibitive cost and limited availability of AI hardware concentrates power among large corporations that can afford to secure the limited supply. This dynamic creates a market of “haves” and “have-nots, ” stifling innovation from smaller enterprises and startups that are priced out of accessing the necessary computational resources.

Semiconductor Investment 2025: A Trillion-Dollar Response to the AI Hardware Bottleneck

The semiconductor industry is responding to the supply crisis with unprecedented capital expenditure aimed at expanding global fabrication capacity, though the long lead times for new facilities mean market relief is not expected before 2027.

- The scale of investment is staggering, with Mc Kinsey estimating that total investment in fabrication plants (fabs) will accumulate to $1 trillion by 2030. This level of spending reflects a strategic shift to address the structural deficit in AI-related chip production.

- Specific commitments highlight the urgency, including SK Hynix spending $13 billion to expand its AI memory production capacity. On a national scale, Taiwanese companies plan to invest $250 billion in the U.S. for semiconductors and AI, while total announced investments across the United States have surpassed $630 billion to revitalize its domestic supply chain.

- While investments were significant before 2025, the focus has now sharpened from general manufacturing capacity to building out production lines specifically for AI accelerators and advanced memory like HBM, a direct response to the market’s most acute bottleneck.

- Despite these massive financial commitments, the timeline for relief is extended. New factories for conventional chips are not expected to come online until 2027 or 2028, confirming analyst predictions that the memory and GPU shortage will persist well beyond 2026.

Table: Major Investments in Semiconductor Capacity

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Taiwanese Companies | Jan 20, 2026 | Investment of $250 Billion in the U.S. to boost production of semiconductors, energy, and AI as part of a ‘democratic’ high-tech supply chain initiative with the United States. | Reuters |

| United States | Jan 7, 2026 | Total announced investments surpassed $630 Billion across the U.S. to revitalize the domestic semiconductor supply chain and reduce reliance on foreign manufacturing. | Oreate AI |

| Global Semiconductor Industry | Aug 25, 2025 | Mc Kinsey estimates total investment in fabrication plants will reach $1 Trillion by 2030, driven by the explosive demand for AI and other advanced technologies. | Tech Mahindra |

Strategic Alliances 2025: Building Resilient Supply Chains Amid the AI Chip Shortage

In response to the hardware crisis, companies and governments are forming targeted strategic alliances to de-risk supply chains, improve manufacturing efficiency, and secure sovereign access to critical semiconductor technologies.

- At the corporate level, partnerships are focused on optimizing production. The collaboration between Siemens and Global Foundries aims to deploy AI-driven manufacturing solutions to enhance efficiency and strengthen the global semiconductor supply, a direct tactical response to output constraints.

- On a geopolitical scale, nations are forging alliances to build collective supply chain security. The partnership between Canada and the United Kingdom, announced in July 2025, is designed to create a stronger, more resilient semiconductor ecosystem to support their growing AI compute needs.

- The most significant geopolitical move is the strategic AI partnership between the United States and Taiwan. Announced in January 2026, this initiative aims to build a “democratic” high-tech supply chain, cementing a technology bloc to counter dependency on other regions and secure the flow of advanced components.

- This marks a clear evolution from the pre-2025 period, where international partnerships were primarily centered on commercial sales or R&D. The new alliances are explicitly defensive, focused on resilience and strategic autonomy in an era where access to chips is a national security imperative.

Table: Key Strategic Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Taiwan & United States | Jan 20, 2026 | Formation of a strategic partnership to lead a “democratic” high-tech supply chain, involving $250 billion in investment from Taiwanese companies in the U.S. | Reuters |

| Siemens & Global Foundries | Dec 11, 2025 | A strategic collaboration to deploy AI-driven manufacturing techniques, aiming to strengthen and increase the efficiency of the global semiconductor supply. | Siemens |

| Canada & United Kingdom | Jul 3, 2025 | A partnership to build a stronger and more resilient semiconductor supply chain between the two countries to support growing AI compute capacity needs. | Government of Canada |

Geopolitical Chokepoints: How the AI Chip Shortage Redraws the Global Tech Map

Access to advanced semiconductors has become a primary instrument of geopolitical power, with the current shortage concentrating manufacturing leverage in Asia and forcing Western nations to launch expensive, multi-hundred-billion-dollar onshoring initiatives to secure their technological futures.

- Between 2021 and 2024, the global economy was aware of its dependency on Taiwan for advanced chips, but the AI boom since 2025 has transformed this dependency into a critical strategic chokepoint. Taiwan Semiconductor Manufacturing Company (TSMC) and its fabrication capabilities now sit at the center of the global technology race.

- The United States has weaponized this chokepoint by intensifying export controls, effectively cutting off China’s access to the most advanced AI accelerators from companies like Nvidia and AMD. This policy is deliberately widening the technology gap and forcing China to accelerate its efforts to build a self-reliant domestic semiconductor ecosystem.

- In response, the U.S. and Europe have initiated massive state-sponsored investment programs. The U.S. is deploying funds from its $52.7 billion CHIPS Act, part of a wave of over $630 billion in announced private and public investments aimed at revitalizing domestic chip manufacturing and reducing reliance on Asia.

- This dynamic solidifies a new geopolitical map defined by technology blocs. Taiwan has formalized its alignment with the U.S. by announcing a “democratic” high-tech supply chain partnership, positioning itself and its manufacturing prowess as a cornerstone of Western technology strategy.

From GPU Scarcity to HBM Bottleneck: The Evolving Maturity of AI Hardware Constraints

The core of the AI hardware constraint has matured from a general shortage of GPUs to a more complex and persistent bottleneck in advanced packaging and High-Bandwidth Memory (HBM), confirming that AI workloads are pushing the limits of current manufacturing technology and creating a structural, not transient, crisis.

HBM to Dominate AI Chip Market

This forecast highlights High Bandwidth Memory (HBM) as the key growth driver, perfectly matching the section’s argument that the hardware constraint has evolved into an HBM bottleneck.

(Source: MarketsandMarkets)

- In the 2021-2024 period, the primary hardware limitation was the supply of leading-edge GPUs like Nvidia‘s A 100. Since 2025, the problem has evolved. The bottleneck is now increasingly centered on HBM, a technology that involves the difficult process of vertically stacking DRAM chips to feed data-hungry AI models.

- The technological challenge of HBM production is validated by market conditions. Major producers like Micron and SK Hynix are completely sold out for 2025 and well into 2026, with Micron calling the AI-driven memory shortage “unprecedented.”

- The constraint has also cascaded down the supply chain. Persistent shortages are now reported for downstream materials like substrate fiberglass and high-end glass fiber cloth, which are essential for the advanced chip packaging required by AI accelerators. This indicates the problem has expanded beyond silicon to the entire manufacturing ecosystem.

- This technological shift confirms that the market is no longer just grappling with high demand but is hitting fundamental manufacturing and material limits. The “insanely memory-hungry” nature of modern AI models has made HBM and advanced packaging the new chokepoints, solidifying the shortage as a long-term structural issue.

SWOT Analysis: Navigating the Semiconductor Supply Crisis in the AI Era

The AI-driven demand shock has created immense market growth opportunities and solidified the pricing power of key players, but it has also exposed severe structural weaknesses in manufacturing capacity and ignited geopolitical threats, forcing a global realignment toward supply chain sovereignty.

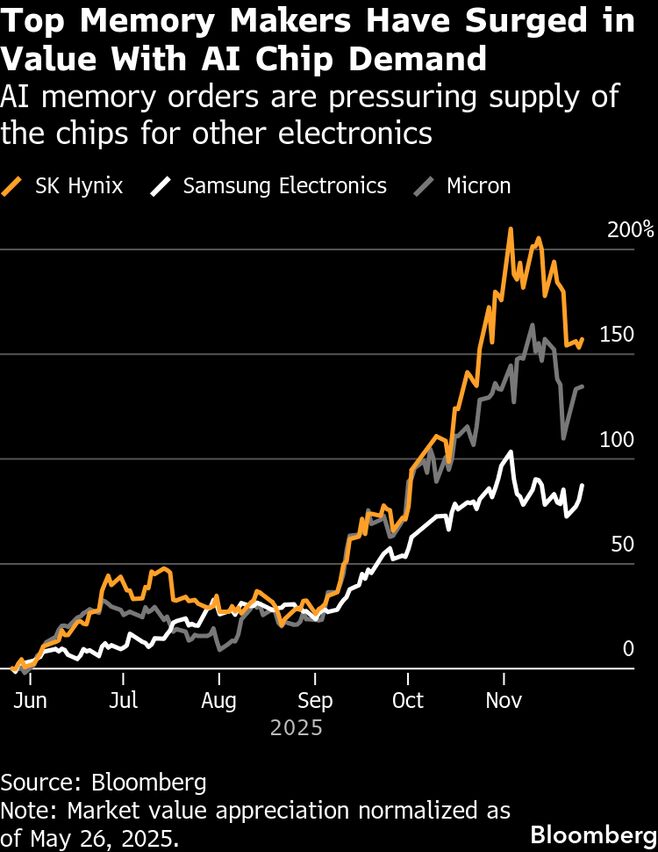

Memory Chip Makers’ Market Value Soars

This chart shows the surging value of top memory chip makers, which powerfully illustrates the ‘Strengths’ category of the SWOT analysis concerning the market dominance and pricing power of incumbents.

(Source: Bloomberg.com)

- Strengths: The crisis has cemented the market dominance and unprecedented pricing power of incumbents like Nvidia and memory makers, fueling massive capital investment in next-generation technology.

- Weaknesses: The industry’s primary weakness is its inability to meet demand for HBM and advanced packaging, a problem worsened by the cannibalization of conventional memory production, which creates collateral shortages.

- Opportunities: The shortage has created a vital opportunity for alternative foundries like Intel to gain market share, while massive government funding programs are accelerating domestic manufacturing and R&D.

- Threats: The most significant threats are the intensified U.S.-China tech war, the risk of AI adoption stalling for most businesses due to cost, and broad-based price inflation for consumer electronics.

Table: SWOT Analysis for the AI-Driven Semiconductor Shortage

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Market dominance of established players like Nvidia and TSMC. High-profit margins on advanced chips. | Unprecedented pricing power solidified. Massive capital influx ($1 T by 2030) for next-generation R&D and expansion. | Market dominance shifted from strong to near-monopolistic for key players. Investment scale became a matter of national strategic importance. |

| Weaknesses | Long lead times for new fabs. High geographical concentration of manufacturing in Taiwan. | Inability to meet acute demand for HBM and advanced packaging. Production capacity cannibalized from conventional memory, creating collateral shortages for PCs and smartphones. | The bottleneck matured from a general GPU shortage to a complex, multi-faceted manufacturing crisis (HBM, packaging), exposing deeper structural weaknesses in the supply chain. |

| Opportunities | Rise of custom silicon by hyperscalers. Early-stage government incentives (e.g., passage of the CHIPS Act). | Massive market opening for alternative foundries (Intel). Large-scale government funding deployment ($630 B+ in U.S. announced). Growth in AI-driven manufacturing (Siemens/Global Foundries). | The “opportunity” for alternative suppliers became a strategic necessity for supply chain resilience. Government funding shifted from proposal to massive, active deployment. |

| Threats | Geopolitical tensions over Taiwan. Initial U.S. export controls on China. | Intensified U.S.-China tech war, cutting China off from advanced chips. AI adoption stalling for non-hyperscalers. Price inflation for consumer electronics (projected up to 20%). | Geopolitical tension evolved into an active economic weapon. The threat of a slow AI rollout moved from a potential risk to a direct constraint on the global economy. |

Forward Outlook: Expect a Widening Gap Between AI ‘Haves’ and ‘Have-Nots’ Through 2027

The most critical strategic expectation for the next two years is the consolidation of AI power among a few hyperscalers that can secure scarce hardware, while the majority of the market faces significant project delays and prohibitive cost barriers, forcing a fundamental realignment of AI adoption strategies.

- If this happens: The current trajectory of severe GPU and HBM shortages continues without significant new fabrication capacity coming online before the 2027-2028 timeframe.

- Watch this: Monitor the price of server memory, with DDR 5 RDIMM costs projected to surge by 100% by 2026. Track the success of alternative foundries like Intel in securing large-scale advanced packaging and fabrication orders. Follow the allocation of CHIPS Act funding to see which projects are prioritized for accelerating domestic supply.

- These could be happening: Smaller enterprises and startups will increasingly pivot from building proprietary AI models to consuming APIs from major cloud providers, trading control for access. Geopolitical technology blocs will harden, with the U.S.-Taiwan alliance defining one sphere of influence. The hardware bottleneck will delay widespread productivity gains from AI, as most of the economy waits for hardware costs and availability to normalize.

Frequently Asked Questions

What is the main cause of the 2025 AI chip shortage?

The shortage is caused by an insatiable demand from AI data centers for advanced hardware, specifically GPUs (like Nvidia’s H100) and High-Bandwidth Memory (HBM), which has overwhelmed global manufacturing capacity. This is a structural crisis driven by the specific, immense needs of modern AI models, distinct from the broader shortages seen in previous years.

When is the AI hardware shortage expected to end?

Significant relief from the shortage is not expected before 2027. Despite unprecedented investments in new fabrication plants (fabs), these facilities have long construction lead times. The analysis confirms that the memory and GPU shortage will persist well beyond 2026.

How does this shortage affect smaller businesses compared to large tech companies?

The shortage creates a market of “haves” and “have-nots.” Large corporations and hyperscalers can afford the prohibitive costs and secure the limited supply of advanced chips. This leaves smaller enterprises and startups priced out, delaying their AI projects, hindering their ability to scale, and stifling innovation.

What specific hardware components are the most difficult to get?

The primary bottlenecks are advanced GPUs, such as Nvidia’s H100 and A100, and High-Bandwidth Memory (HBM). The demand for HBM is so high that major producers like SK Hynix and Micron have already sold out their entire supply for 2025 and, in SK Hynix’s case, for all of 2026 as well.

What are governments and corporations doing in response to the crisis?

Governments and companies are responding with massive capital investment, strategic alliances, and onshoring initiatives. The semiconductor industry plans to invest nearly $1 trillion by 2030, while the U.S. has announced over $630 billion in investments to boost domestic production. Nations like the U.S., Taiwan, Canada, and the U.K. are also forming partnerships to build more resilient and secure supply chains.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.