AI Power Grid Constraints: Microsoft’s 2 GW Pullback, $22 B in Canceled Renewables, and 27 State-Level Bills (2025-2026)

AI Energy Risks, Microsoft 2 GW Pullback, $22 B Cancellations (2025-2026)

The primary risk to capitalizing on the AI-driven energy demand has shifted from a technology challenge to an execution crisis, defined by physical grid limitations and disruptive policy changes. While demand forecasts through 2024 pointed to a straightforward growth opportunity, the period from 2025 to 2026 revealed that inadequate grid infrastructure and political upheaval are now the dominant constraints on development, forcing major technology players to scale back plans.

- The most acute signal of this constraint was Microsoft‘s decision to cancel or defer over 2 GW of data center capacity agreements between late 2024 and March 2025. This was not due to a lack of demand for AI, but a direct consequence of insufficient power and grid capacity in planned regions.

- Grid interconnection backlogs have moved from a developer nuisance to a systemic barrier, causing the cancellation of over $22 billion in renewable energy projects in the first half of 2025 alone. These delays directly inhibit the “speed-to-power” strategy required to meet data center deployment timelines.

- The market narrative has pivoted from “Energy for AI, ” which focused on building generation, to navigating the “Grid for AI, ” which prioritizes overcoming interconnection bottlenecks, securing scarce transmission capacity, and managing policy risk.

- Public and regulatory opposition is now a material risk, with data center project cancellations quadrupling in 2025 due to sustained local resistance. This adds a new layer of complexity and uncertainty to project permitting and timelines.

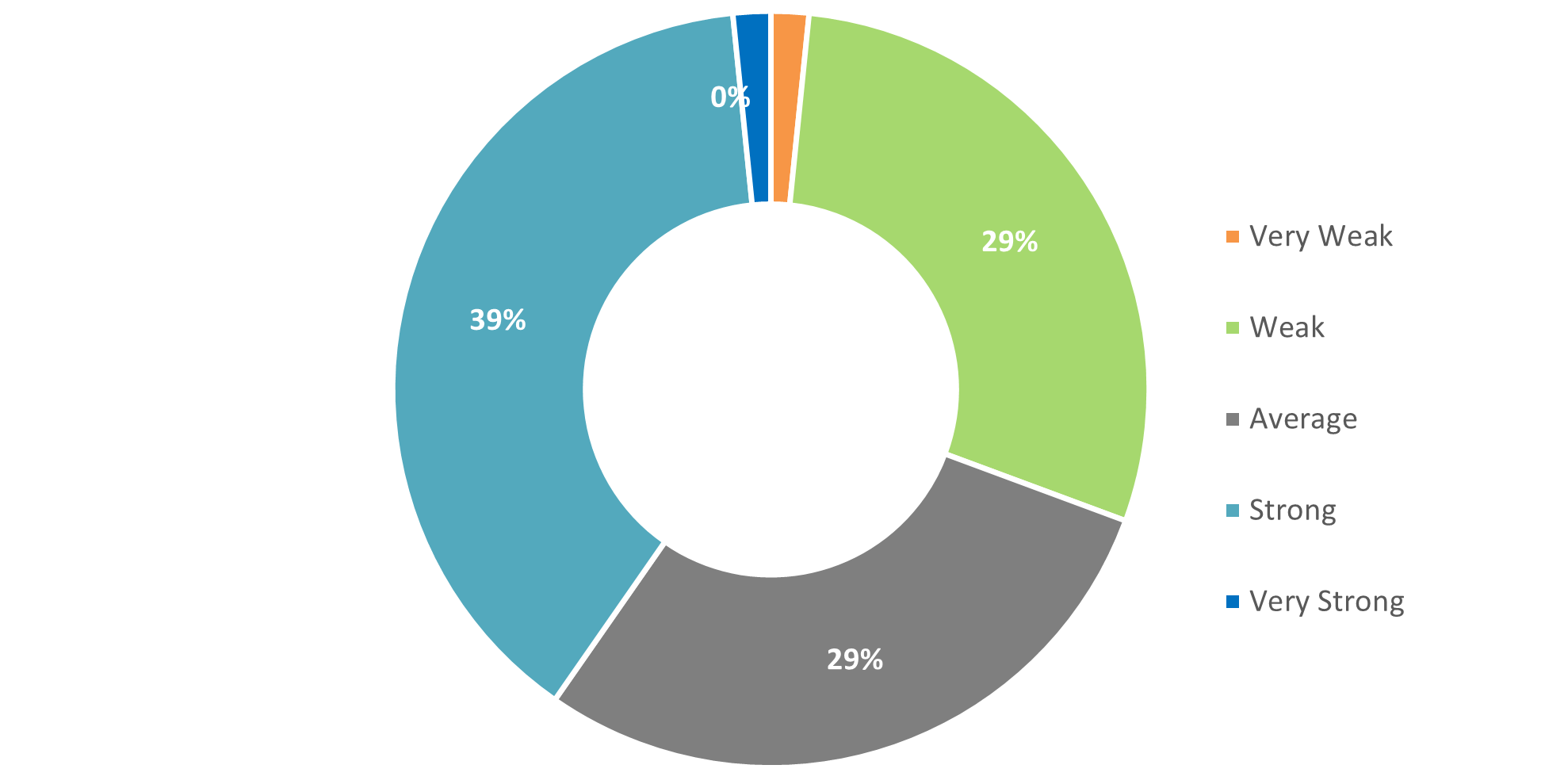

Utility Readiness for AI Demand is Fractured

This chart quantifies the ‘execution crisis’ by showing that a majority of utilities are not strongly prepared for AI’s energy demand, aligning with the section’s theme of grid limitations forcing project pullbacks.

(Source: Sustainalytics)

$22 B in Cancellations, AI Energy Projects Sidelined by Grid Delays

Project cancellations are no longer isolated incidents but a systemic trend driven by grid interconnection failures and mounting local opposition, directly impacting the ability of both energy developers and their hyperscale customers to execute growth plans. The data from 2025 and 2026 shows a dramatic increase in project failures, highlighting a critical market friction that financial investment alone cannot solve.

- In the first half of 2025, the financial impact of interconnection delays became starkly evident, with over $22 billion worth of renewable projects being officially canceled. This represents a significant loss of potential generation capacity intended to serve new industrial and computational load.

- Hyperscalers are now directly exposed to these infrastructure failures, as shown by Microsoft‘s strategic pullback of more than 2 GW of data center capacity. This indicates that even bankable offtake agreements are insufficient if the physical grid cannot support the new load.

- Local opposition has become a primary driver of project failure, with cancellations of data center projects increasing fourfold in 2025. This growing resistance complicates siting and permitting, adding significant time and cost to development.

Table: Significant AI Energy-Related Project Cancellations and Delays (2025-2026)

| Entity / Project Type | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Microsoft Data Centers | Late 2024 – Mar 2025 | Canceled or deferred over 2 GW of data center capacity agreements due to infrastructure and power availability constraints, signaling a major setback for a leading hyperscaler. | windowsforum.com |

| U.S. Renewable Energy Projects | H 1 2025 | Over $22 billion in planned projects were canceled due to extensive backlogs in grid interconnection queues, eliminating 16, 500 jobs and significant potential power capacity. | globaldatacenterhub.com |

| U.S. Data Center Projects | 2025 | The rate of data center project cancellations quadrupled compared to the previous year, driven primarily by sustained local opposition to new developments. | gizmodo.com |

US vs. State Policy, AI Energy Regulation Fragments Across 27 States

A significant conflict between federal ambitions and state-level legislative action has fragmented the U.S. regulatory environment, creating a complex and unpredictable patchwork for energy and data center developers. While federal policy in 2025 aimed to accelerate development, by 2026 a wave of state-level bills introduced new, often contradictory, requirements that challenge a unified national strategy.

- The passage of the “One Big Beautiful Bill Act” (OBBBA) on July 4, 2025, abruptly altered federal energy policy by eliminating or modifying many clean energy tax credits from the 2022 Inflation Reduction Act. This created immediate uncertainty for renewable projects and shifted economic incentives toward firm power sources like nuclear and natural gas.

- As of April 2026, at least 27 states are advancing their own legislation concerning data centers. These bills address energy costs, establish moratoriums on new construction, and impose unique clean energy or water usage requirements, directly countering federal efforts to streamline permitting.

- This state-level pushback creates a balkanized market where project viability depends not just on resource availability and grid access, but on navigating a diverse and shifting set of local political priorities.

- For developers, this means that a national rollout strategy is no longer feasible. Instead, a state-by-state or even county-by-county approach is required, significantly increasing regulatory overhead and project risk.

AI Energy System Maturity, Grid Integration is the Primary Constraint

The core challenge in powering AI is not a lack of viable generation technologies but the immaturity of the systems required to permit, connect, and regulate them at scale. The 2025-2026 period demonstrated that while a diverse portfolio of technologies exists, the grid’s structural and regulatory weaknesses are the true bottleneck, a sharp contrast to the pre-2025 focus on technology innovation alone.

Energy System Health Metrics Reveal Weaknesses

This chart illustrates the ‘immaturity’ of the energy system by comparing key metrics. The weaker scores for ‘Availability’ directly reflect the grid integration constraints and structural weaknesses described in the text.

(Source: Nature)

- The problem is not a shortage of generation options. A mix of fast-to-deploy renewables, reliable firm power from natural gas, advanced nuclear, and modular solutions like those from Bloom Energy are all technically ready. The constraint is getting them approved and physically connected to the grid.

- The interconnection queue itself is the clearest sign of system immaturity. The inability to process and approve new generation projects in a timely manner is a systemic failure that directly increases costs and delays the energy transition, regardless of which generation technology is used.

- Policy has amplified this issue. The OBBBA legislation in 2025 created an abrupt shift in economic signals, rewarding certain technologies like natural gas with carbon capture and penalizing others, adding volatility to a system that requires long-term stability for investment.

- The winning strategies are now those that can circumvent this systemic immaturity. This includes direct “behind-the-meter” power agreements, vertical integration as seen with Alphabet‘s acquisition of Intersect Power, and focusing on sites with pre-existing grid capacity and favorable local politics.

SWOT Analysis for AI Energy, Policy & Infrastructure Risks Mount

The strategic landscape for powering AI has been reshaped by the collision of massive demand with severe real-world constraints. The period from 2024 to 2025 exposed major weaknesses and threats that now define the primary challenge, shifting the focus from capturing growth to managing systemic risk.

AI Boom to More Than Double Energy Use

This forecast visualizes the ‘massive, structural’ demand described as the primary ‘Strength’ in the SWOT analysis, perfectly setting the context for the strategic challenges and opportunities discussed.

(Source: Statista)

- Strengths have been validated by durable, non-cyclical demand from hyperscalers, creating a bankable long-term revenue stream for energy producers who can deliver reliable power.

- Weaknesses in the physical grid and regulatory processes, once a known issue, have become the central limiting factor, actively destroying project value and delaying deployments.

- Opportunities are now greatest for strategies that bypass these weaknesses, such as direct power-of-take agreements and generation portfolios that prioritize reliability over any single technology.

- Threats have magnified, with policy instability and fragmented state-level regulation creating a volatile and unpredictable environment for long-term capital investment.

Table: SWOT Analysis for the AI Energy Market

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Hypothetical large-scale demand from the emerging AI sector was seen as a major future growth driver for electricity consumption. | AI data centers became the single largest driver of new load growth in the U.S., with hyperscalers seeking long-term, multi-GW power agreements. | The massive, structural nature of AI energy demand was validated, reversing two decades of flat U.S. power demand and creating a durable market for new generation. |

| Weakness | Grid interconnection queues were a known but manageable issue for developers, seen as a cost of doing business. | Interconnection queues became a primary cause of project failure, leading to $22 billion in canceled renewable projects in H 1 2025 alone. | The weakness of the U.S. grid and its regulatory processes was exposed as the primary bottleneck, unable to handle the speed and scale of new generation requests. |

| Opportunity | The focus was on “AI for Energy, ” using software to optimize the existing grid and integrate intermittent renewables. | The focus shifted to “Energy for AI, ” with direct offtake agreements (PPAs) and “behind-the-meter” solutions becoming the premium opportunity. | The opportunity shifted from grid software to direct infrastructure development. Alphabet‘s acquisition of Intersect Power validated the strategy of vertical integration to secure power. |

| Threat | The primary threat was seen as technological competition or the risk of AI energy efficiency improvements reducing future demand. | The primary threats became policy instability (OBBBA’s repeal of IRA credits) and fragmented regulation (27 states with conflicting data center laws). | Regulatory and political risk surpassed technological or market risk as the main threat to development, confirmed by the passage of the OBBBA on July 4, 2025. |

AI Energy 2026 Scenarios, ‘Behind-the-Meter’ Deals Signal Market Path

Looking ahead, the most critical indicator of success in the AI energy market will be the viability and scalability of projects that bypass traditional grid constraints. The strategic focus has shifted from building generation to securing a direct, reliable path to the customer, making “behind-the-meter” and dedicated infrastructure projects the key signal to watch in 2026.

AI Demand Crisis Spurs Future Pathway Scenarios

This infographic presents two distinct future scenarios for managing AI’s energy demand, directly aligning with the section’s focus on strategic paths forward, including those that bypass traditional grid infrastructure.

(Source: ScienceDirect.com)

- If hyperscalers and energy developers successfully execute more direct power agreements that circumvent public utility bottlenecks, expect an acceleration of vertical integration and M&A activity, mirroring Alphabet’s $4.75 billion acquisition of Intersect Power.

- Watch for the geographic clustering of new data center announcements in regions with favorable, stable regulations and available transmission capacity. This will signal which states are winning the AI infrastructure buildout.

- The price premium for 24/7 reliable power will become more explicit. If the cost differential between intermittent renewables and firm power sources (nuclear, geothermal, gas with CCS) widens, it validates the strategic pivot towards a reliability-focused generation portfolio.

- Conversely, if “behind-the-meter” projects face their own regulatory or execution challenges, it could signal a significant slowdown in data center growth, as hyperscalers will be unable to expand beyond the capacity of the existing strained public grid.

The questions your competitors are already asking

This report covers one angle of the execution crisis constraining the AI energy boom. The questions that matter most depend on your work.

- What is actually happening with Microsoft’s 2 GW of deferred data center capacity agreements since the pullbacks were announced?

- What is the outlook for new renewable energy projects to power data centers by 2026, considering the $22 billion in recent cancellations?

- What are the opportunities for transmission developers and grid-enhancing technologies in markets constrained by interconnection backlogs?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.