China DAC Infrastructure, 2.1 Gt/yr Demand, 55% Lower CAPEX, and China Huaneng’s 1.5 Mtpa Project (2025 to 2026)

From Policy to Pilots: China’s DAC Adoption Shifts to Physical Infrastructure

China’s Direct Air Capture adoption is shifting from a theoretical necessity to a practical industry focus in 2025-2026, driven by a massive long-term carbon removal demand that dwarfs current global capacity. Before 2025, China’s carbon capture efforts were concentrated on academic research and large-scale point-source CCUS pilots, while policy was being formulated to meet the nation’s 2060 carbon neutrality goal. The current period marks a strategic pivot toward validating DAC technology itself, creating a market for early-stage commercial applications that can generate revenue and de-risk the path to gigaton-scale carbon removal.

- The primary driver is a structural deficit in carbon removal. China’s industrial sector alone is projected to emit 2.1 billion metric tons of CO 2 in 2060, creating a non-negotiable demand for negative emissions technologies like DAC to achieve national climate targets.

- The operational playbook for DAC is being written by analogue point-source capture projects. The commissioning of China Huaneng Group’s 1.5 Mtpa post-combustion capture facility in 2025 provides critical domestic experience in CO 2 handling, transport, and storage, building the supply chains and expertise required for future DAC hubs.

- Initial commercialization is focused on utilization, not just storage. The leading applications for captured CO 2 are in producing high-value products like Sustainable Aviation Fuel (SAF) and e-methanol. This strategy creates an early revenue stream to offset high capital costs, making projects more attractive before a robust carbon price for pure sequestration exists.

- The global context highlights the scale of China’s opportunity. As of early 2026, total global operational DAC capacity is just 0.01 million tons per year, demonstrating the nascent state of the industry and creating a vacuum for a manufacturing-led power to emerge and define the market. This push mirrors global efforts in hard-to-abate sectors, where companies like U.S. Steel and Heidelberg Materials are also exploring large-scale capture solutions.

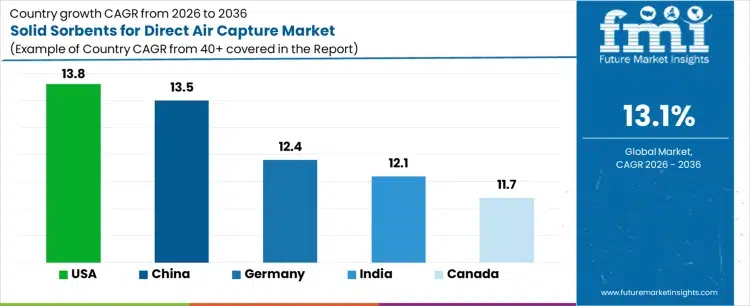

China’s DAC Sorbent Market to Grow Rapidly

This chart shows China’s projected growth in the DAC sorbent market, putting it nearly on par with the US. This directly supports the section’s theme of China shifting from policy to building physical DAC infrastructure.

(Source: Future Market Insights)

20% CAPEX Subsidy: How China is De-Risking Early DAC Investments

While direct private investment into Chinese DAC projects is still developing, the 2025-2026 period is defined by crucial state-led financial incentives designed to de-risk capital and catalyze the market. The government’s approach is not to wait for DAC costs to fall, but to create the market conditions that will actively drive down the cost curve through industrial policy and targeted financial support.

Government Regulations Drive Carbon Capture Growth

This chart identifies ‘Stringent government regulations’ as a primary driver for the carbon capture market. This perfectly illustrates the section’s core argument that state-led financial incentives are key to de-risking and catalyzing China’s early DAC market.

(Source: Coherent Market Insights)

- In October 2025, the National Development and Reform Commission (NDRC) introduced a subsidy covering up to 20% of capital expenditure for clean fuel projects, a measure that directly benefits the DAC-to-fuels pathway and provides a clear financial incentive for first-movers.

- China’s broader clean energy investment, which reached a record $213 billion in foreign direct investment programs in 2025, creates a massive pool of strategic capital that can be directed toward DAC as it gains status as a critical climate technology.

- The expansion of China’s national Emissions Trading Scheme (ETS) is the most significant long-term financial driver. Projections for the ETS to become a $56-84 billion market by 2030 signal the government’s intent to create a durable, compliance-driven carbon price that will eventually make DAC projects economically self-sufficient.

- The existing ETS framework already provides a foundational demand signal by allowing companies to offset up to 5% of their compliance obligations with domestic credits, including those from carbon capture projects, establishing an initial market for DAC-generated offsets.

China’s Manufacturing Edge: A Projected 55-70% Lower DAC CAPEX

China is positioned to shape the global DAC scale-up by leveraging its formidable manufacturing and supply chain capabilities, which are projected to yield a decisive capital expenditure advantage over Western projects. Before 2025, DAC technology development was concentrated in North America and Europe with companies like Climeworks and CO 280, which focused on validating technology but at a high cost. China’s entry into the market is expected to shift the focus from pure technology demonstration to mass production and cost reduction.

- Analysis suggests that Chinese carbon capture projects could achieve 55-70% lower capital expenditure per tonne compared to equivalent projects in the West. This potential for radical cost reduction is China’s most significant competitive advantage.

- This cost advantage is rooted in China’s proven ability to rapidly scale manufacturing of key industrial components, apply “learning-by-doing” to complex engineering projects, and optimize supply chains, a model successfully deployed in the solar PV and battery industries.

- While international firms lead in some proprietary DAC sorbent technologies, China is well-positioned to mass-produce the standardized modules, heat exchangers, pumps, and other balance-of-plant equipment that constitute a large portion of a DAC facility’s cost.

- The geographic focus is expected to be on co-locating DAC facilities with existing industrial hubs and regions rich in renewable energy resources to minimize costs for both energy input and CO 2 utilization or storage, creating integrated carbon management zones.

DAC Technology Readiness: TRL 6 Prototypes Confront Gigaton-Scale Demand

While core Direct Air Capture technologies have reached the large-scale prototype stage (TRL 6) and are ready for initial commercial deployment in 2025-2026, a significant gap remains between current capabilities and the engineering challenges of building and operating the gigaton-scale infrastructure China needs. The period before 2025 was about proving the science; the current period is about proving the engineering and economics at scale.

DAC Market Growth Shows Scale-Up Challenge

Projecting massive growth from a tiny 2025 base, this chart visualizes the gap between current prototype technology and future gigaton-scale demand. The breakdown by L-DAC and S-DAC technologies also matches the specific types mentioned in the text.

(Source: Market Research Future)

- Globally, both liquid solvent and solid sorbent DAC technologies are considered to be at Technology Readiness Level (TRL) 6, meaning they have been demonstrated at a pilot scale in a relevant environment. China’s domestic technology development is largely aligned with this international benchmark.

- The primary technological barrier is not invention but integration and scale. Moving from kiloton-per-year pilots to megaton-scale plants introduces immense engineering challenges related to energy efficiency, thermal management, sorbent degradation, and operational reliability that are not yet solved at a competitive cost.

- A major technical hurdle is the high energy penalty. DAC’s process of separating CO 2 from air is energy-intensive, and projects must be paired with massive, dedicated renewable energy sources to ensure they are net-negative and avoid simply shifting emissions to the power sector.

- China’s strategy appears to be focused on rapid iteration and process optimization. By leveraging operational data from its large-scale CCUS projects, its innovation ecosystem is working to develop lower-cost designs, novel materials, and AI-driven operational controls tailored for its industrial environment.

SWOT Analysis for China’s DAC Market (2025-2026)

China’s Direct Air Capture market in 2025-2026 is defined by the strength of its state-led industrial policy and manufacturing base, which is offset by the weakness of high nascent costs and technological energy penalties. The expansion of its national carbon market and the global push for decarbonization present major opportunities, but these are tempered by the threat of policy volatility and competition for resources.

Table: SWOT Analysis for China’s DAC Market

| SWOT Category | 2021 – 2024 (Foundation Phase) | 2025 – 2026 (Initial Deployment) | What Changed / Validated |

|---|---|---|---|

| Strengths | Clear top-down government mandate for 2060 carbon neutrality; extensive experience in large-scale industrial projects. | Demonstrated ability to deliver massive CCUS projects (e.g., China Huaneng’s 1.5 Mtpa plant); established manufacturing base projected to lower CAPEX by 55-70%. | The state-led industrial model has been validated as effective for building precursor infrastructure, confirming China’s ability to execute complex carbon management projects. |

| Weaknesses | Extremely high estimated costs for DAC ($250+/ton); technology largely in R&D or small pilot stages; lack of specific policy support for DAC. | High energy consumption remains a key barrier; sorbent degradation impacts operational costs; dependence on policy incentives creates financial risk. | The shift from R&D to pilot deployment has confirmed that high energy requirements and operational costs are the most significant near-term weaknesses to be addressed. |

| Opportunities | Nascent national ETS; growing global awareness of the need for carbon removal; potential to lead a new climate technology sector. | Expansion of the national ETS to heavy industry; direct subsidies (e.g., 20% CAPEX for clean fuels); growing demand for SAF and other e-fuels. | Tangible policy mechanisms and subsidies introduced in 2025 have converted the general opportunity of carbon markets into a specific, bankable opportunity for DAC-to-fuels projects. |

| Threats | Energy security concerns prioritizing fossil fuels; potential for policy changes; competition for R&D funding from other green technologies. | Carbon price volatility in the ETS; competition for low-cost renewable energy from other sectors; potential for supply chain bottlenecks in specialized DAC components. | The threat has shifted from a lack of policy to the specifics of policy execution. Carbon price instability and resource competition for renewables are now the primary external risks. |

China’s DAC 2026 Outlook: Monitoring the 15 th Five-Year Plan for Targets

The trajectory of China’s DAC market beyond 2026 will be determined by the inclusion of specific, quantitative deployment targets and dedicated financial support mechanisms in the upcoming 15 th Five-Year Plan (2026-2030). This document will provide the clearest signal of whether DAC is being elevated to a national strategic priority on par with solar and electric vehicles.

DAC Market Poised for Explosive Growth

This forecast, showing the market hitting $17.5B by 2035 with a 61% CAGR, quantifies the aggressive growth discussed in the section. It provides a tangible vision for the market scale China could unlock with its 15th Five-Year Plan.

(Source: Research Nester)

- If the plan is aggressive: Watch for the announcement of multiple Final Investment Decisions (FIDs) on DAC plants with capacities exceeding 100, 000 tons per year. These projects would likely be led by state-owned enterprises like China Huaneng and co-located at existing industrial parks, leveraging the infrastructure and expertise built from precursor CCUS projects.

- If the plan is cautious: A continued focus on point-source CCUS with only vague language on DAC would signal that the technology is expected to remain in the small-scale pilot phase for several more years. In this scenario, growth would be constrained by unfavorable project economics, awaiting either a technology cost breakthrough or a much higher carbon price.

- The key market signal to monitor is the price of carbon: A rising and stable price within China’s national ETS is the most critical factor for long-term commercial viability. As the ETS price approaches the all-in cost of DAC (with emerging technologies targeting $80-$100 per ton), it will unlock private investment and reduce the market’s reliance on direct subsidies.

The questions your competitors are already asking

This report covers one angle of China’s transition from DAC policy to building commercial-scale carbon removal infrastructure. The questions that matter most depend on your work.

- Which companies are leading the development of China’s DAC pilot projects?

- What is the status of China Huaneng’s 1.5 Mtpa CCUS project and how does it support the build-out of DAC supply chains?

- What is the cost breakdown for a commercial-scale DAC plant in China, and how is the 55% lower CAPEX achieved?

- What are the opportunities for DAC-derived CO2 in China, specifically for producing Sustainable Aviation Fuel (SAF) and e-methanol?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.