Mitsubishi Heavy Industries Post-Combustion Capture, Worley 800 K Ton Deal, 1.2 M Ton KBR Project, and 8+ Partnerships (2021 to 2026)

Hard-to-Abate Sector Pilots, MHI Projects with Heidelberg and Arcelor Mittal

Mitsubishi Heavy Industries has systematically shifted its post-combustion capture strategy from pilot-scale validation to full commercial execution in the world’s most challenging industrial sectors, proving the adaptability of its core technology. Between 2021 and 2024, the company focused on de-risking its KM CDR Process™ for new flue gas streams through collaborative trials. By 2025, this foundational work translated into commercial-scale project execution, signaling market readiness and establishing MHI as the go-to technology licensor for decarbonizing cement, steel, and shipping.

- In the 2021-2024 period, MHI initiated critical trials, including a partnership with Arcelor Mittal and BHP to test capture technology on blast furnace gas and a pre-FEED contract for a UK cement plant in December 2022. This phase was essential for adapting its amine-based solvent technology to the unique chemical compositions and particulate loads found in industrial emissions beyond the power sector.

- The period from 2025 to today marks a definitive shift to commercial scale, headlined by the December 2025 start of execution for Europe’s first full-scale cement capture facility with Heidelberg Materials and Worley. This project, designed to capture 800, 000 tons of CO 2 per year, represents the culmination of earlier pilot efforts and validates the technology’s commercial viability for cement.

- MHI expanded its application to the maritime sector with a study awarded in April 2025 to design compact CO 2 capture modules for Floating Production Storage and Offloading (FPSO) vessels. This move from stationary land-based facilities to mobile offshore assets demonstrates the technology’s versatility and opens a significant new market vertical.

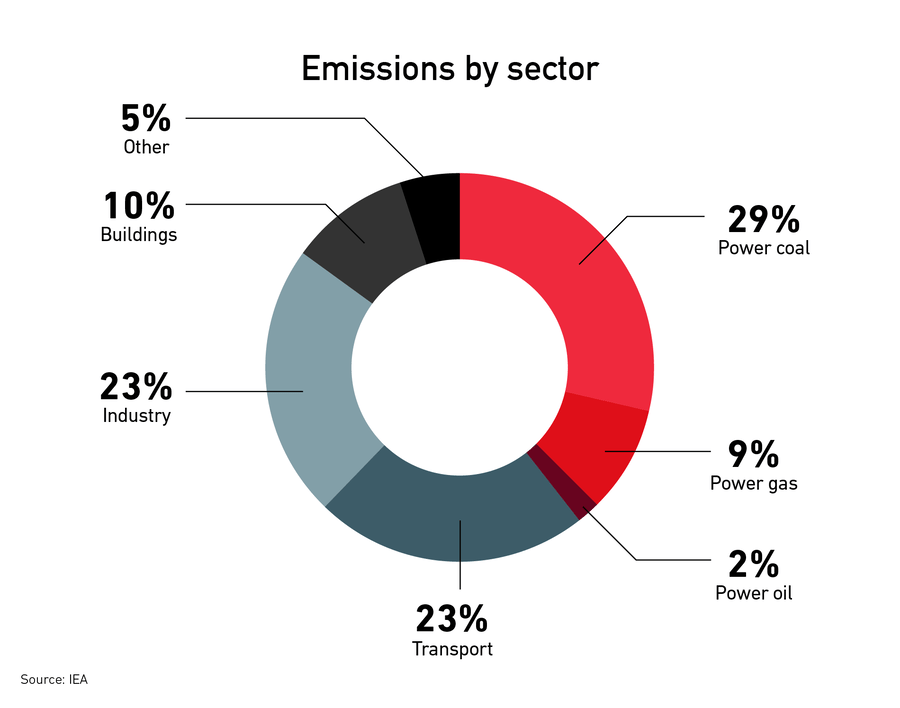

Industry a Major Global Emissions Source

This chart provides critical context for the section by showing that the industrial sector is a primary source of emissions, justifying MHI’s strategic focus on these hard-to-abate areas.

(Source: Bloomberg Media Studios)

MHI 8+ Strategic Alliances from Exxon Mobil to Saipem (2021 to 2026)

Mitsubishi Heavy Industries’ market penetration strategy is defined by a capital-light, scalable partnership model that leverages the domain expertise of global energy leaders, EPC firms, and industrial end-users to de-risk and accelerate project deployment. By licensing its proprietary KM CDR Process™, MHI avoids the financial burden of direct project ownership and instead positions itself as a critical technology enabler across the CCUS value chain. This collaborative framework allows for rapid scaling in key regions and sectors.

Chart Details MHI’s CCS Alliance Role

This diagram provides a concrete example of the strategic partnership model discussed in the text, illustrating how MHI collaborates with other firms within the CCS value chain.

(Source: Mitsubishi Heavy Industries)

- The alliance with Exxon Mobil, announced in November 2022, integrates MHI’s technology into Exxon Mobil’s end-to-end CCUS service offering, providing MHI with unparalleled global reach and access to large-scale industrial customers.

- To target regional markets, MHI partnered with Italian EPC firm Saipem in April 2023 to pursue projects in Europe and the Middle East, combining MHI’s capture technology with Saipem’s project execution capabilities.

- For domestic expansion in Japan, MHI granted a license to Chiyoda Corporation in May 2024, leveraging Chiyoda’s local EPC strength to accelerate CCUS deployment in its home market.

- Direct engagement with industrial emitters is demonstrated through partnerships with Heidelberg Materials for cement and Arcelor Mittal for steel, ensuring the technology is tailored and proven for specific hard-to-abate applications.

Table: Mitsubishi Heavy Industries Strategic Carbon Capture Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Worley & Heidelberg Materials | Dec 2025 | Began execution of a full-scale cement CCS facility in the UK designed to capture 800, 000 tons/year, pairing MHI’s technology with Worley’s EPC expertise for a major industrial emitter. | Carbon Herald |

| Chiyoda Corporation | May 2024 | Licensing agreement for KM CDR Process™ to expand CCUS business within Japan, leveraging Chiyoda’s domestic EPC experience. | MHI |

| Kellogg Brown & Root (KBR) | Mar 2024 | Licensing agreement to supply CO₂ capture technology for a low-carbon hydrogen project in the US, capturing approximately 1.2 million tonnes of CO₂ per year. | Carbon Herald |

| Saipem | Apr 2023 | Collaboration to develop carbon capture projects in Europe and the Middle East, combining MHI’s technology with Saipem’s project delivery expertise. | Carbon Herald |

| Exxon Mobil | Nov 2022 | Strategic alliance for Exxon Mobil to use MHI’s technology in its end-to-end CCUS solutions, expanding MHI’s global market access. | MHI |

| Arcelor Mittal, BHP, Mitsubishi Development | Oct 2022 | Collaboration to trial MHI’s technology at an Arcelor Mittal steel plant, targeting difficult-to-capture emissions from blast furnaces. | MHI |

Europe vs. North America, MHI Cement and Steel Project Deployments

MHI’s commercial activities are geographically concentrated in Europe and North America, regions with robust regulatory frameworks and financial incentives that provide the bankability required for large-scale carbon capture projects. While its technological roots are in Japan, the most significant commercial deployments and market-making partnerships are focused on Western economies where policies like the US 45 Q tax credit and the EU’s carbon pricing mechanisms create a viable business case for industrial decarbonization.

North America to Lead CCS Market

This chart supports the section’s focus on North America as a key deployment region by identifying it as the largest market, reinforcing the article’s point about regional concentration.

(Source: maximize market research)

- In Europe, the United Kingdom is a key market, hosting the landmark Heidelberg Materials Padeswood cement plant project, which began execution in late 2025. This project, along with the earlier partnership with Drax for a major BECCS facility, underscores the UK’s role as a primary proving ground for MHI’s technology at scale.

- North America represents a major growth market, demonstrated by the planned full-scale CCUS project at Heidelberg Materials’ Edmonton cement plant in Canada and the licensing agreement with KBR for a large-scale blue hydrogen facility in the U.S. These projects are directly enabled by supportive carbon pricing and tax credit policies.

- In its home market of Japan, MHI’s focus has been on building the foundational CCUS value chain, including the development of liquefied CO₂ carriers and forging domestic licensing partnerships like the one with Chiyoda. This activity aims to create the necessary infrastructure to support future domestic capture projects in sectors like steel, involving partners such as JFE Steel.

16 Commercial Plants, MHI’s KM CDR Process and KS-21 Solvent Validation

MHI’s carbon capture technology has achieved commercial maturity (TRL 7-9), backed by a portfolio of 16 operational plants and a strategic focus on continuous innovation to reduce costs and expand applications. The period between 2021 and 2024 was characterized by the adaptation of its proven KM CDR Process™ to new, challenging industrial environments. The subsequent period, from 2025 to today, is defined by the deployment of enhanced technologies like the Advanced KM CDR Process™ with the KS-21™ solvent, solidifying its performance and economic advantages.

- The technology’s foundation is built on decades of operational experience in the power and chemical sectors, providing a robust and de-risked starting point for entering harder-to-abate industries. This established track record is a key competitive differentiator.

- Between 2021-2024, MHI focused on validating its technology for new flue gas compositions, undertaking trials in steel with Arcelor Mittal and initiating design studies for cement plants. This work proved the solvent’s resilience and the process’s adaptability.

- From 2025 onwards, MHI has deployed its next-generation technology. The Heidelberg Materials Padeswood project utilizes the Advanced KM CDR Process™ with the proprietary KS-21™ solvent, which offers lower energy consumption and operational stability, directly addressing the high operating costs that have historically challenged CCUS economics.

- The company is also innovating for new form factors, evidenced by the April 2025 study for compact capture modules for FPSOs and the renewal of its “CO₂MPACT™” series. This demonstrates a clear product strategy to address both massive, centralized emitters and smaller, distributed sources.

SWOT Analysis, MHI Strengths in Technology Licensing and Market Risks

MHI’s market position is defined by its mature technology and scalable partnership model, but its growth remains tightly coupled to external policy and infrastructure development. The company’s strategy successfully leverages its core strengths to capitalize on growing market opportunities, yet it faces significant threats related to project economics and the build-out of a complete CCUS value chain. The evolution from 2021 to 2026 shows a validation of its strengths and an intensification of its external dependencies.

- Strengths have been validated as MHI’s technology-licensing model proved effective in securing major partners like Exxon Mobil and Heidelberg Materials, confirming the market’s confidence in its proprietary technology.

- Weaknesses remain centered on the high capital and operational costs of CCUS, a persistent industry-wide challenge that MHI’s advanced solvents aim to mitigate but cannot eliminate.

- Opportunities have grown substantially with the strengthening of policy incentives like the US 45 Q tax credit and the EU’s CBAM, which create a stronger business case for MHI’s customers.

- Threats have become more acute as projects move to execution, highlighting the critical dependency on the timely development of third-party CO₂ transport and storage infrastructure, which remains a major bottleneck.

Table: SWOT Analysis for MHI’s Post-Combustion Capture Strategy

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Established KM CDR Process™ technology with a history of operational plants. Initial partnerships forming with industrial players (Drax, Arcelor Mittal). | Proven ability to secure major licensing deals (Exxon Mobil, KBR, Chiyoda). Advanced KS-21™ solvent deployed at commercial scale (Heidelberg). | The technology licensing and partnership model was validated as the primary growth engine, attracting top-tier global partners and de-risking market entry. |

| Weaknesses | High energy penalty and operational cost of amine-based capture, posing an economic barrier for industrial customers. | Capture costs ($40-$120/ton) still often exceed policy incentives, particularly for dilute flue gas streams in cement and steel. | While advanced solvents reduce costs, the fundamental economic challenge of high opex and capex remains the primary adoption barrier for customers. |

| Opportunities | Emerging net-zero targets and initial policy discussions (e.g., enhanced 45 Q) creating interest in CCUS solutions. | Concrete policies like the full implementation of the EU’s CBAM (Jan 2026) and robust 45 Q credits create tangible financial drivers for capture investment. | The market opportunity shifted from theoretical (net-zero pledges) to tangible (carbon pricing and tax credits), creating a clearer business case for MHI’s offerings. |

| Threats | Lack of large-scale CO₂ transportation and storage infrastructure. Uncertainty over long-term stability of government policy support. | As large projects (Heidelberg) move to execution, the reliance on nascent CO₂ pipeline and storage networks becomes a critical path risk. | The primary threat evolved from policy uncertainty to logistical and infrastructural bottlenecks, as real projects now depend on a complete value chain to operate. |

MHI 2026 Outlook, Shipping Sector Deployments and Policy Dependencies

The most critical indicator to watch for MHI in the near term is the successful conversion of its technology development for the maritime sector into a commercial victory. A first-of-a-kind commercial order for an onboard capture system on a large vessel or FPSO would validate a new billion-dollar market vertical and confirm MHI’s leadership in decarbonizing mobile emission sources. This, combined with the progression of its large-scale terrestrial projects, will determine its growth trajectory.

Diagram Outlines Ship-Based CO2 Transport

This diagram illustrates the role of ship transportation in the CCS value chain, directly connecting to the section’s forward-looking analysis of the shipping sector as a new market.

(Source: Mitsubishi Heavy Industries)

- If MHI secures a commercial contract for its onboard CO₂ capture system following the 2025 FPSO study, watch for other major shipping lines and offshore operators to accelerate their own decarbonization plans, potentially creating a rapid new sales pipeline for MHI’s “CO₂MPACT™” technology.

- If major projects like the Heidelberg Materials facilities in the UK and Canada reach Final Investment Decision (FID), this signals that supportive policies are sufficient to close the economic gap for hard-to-abate sectors, likely triggering a new wave of similar projects across the cement and steel industries.

- If the build-out of CO₂ transport and storage hubs in North America and Europe accelerates, these could be happening: MHI may expand its licensing partnerships to include midstream companies, further integrating its technology into full-chain service offerings and solidifying its market position.

The questions your competitors are already asking

This report covers one angle of Mitsubishi Heavy Industries’ commercial execution in the carbon capture market. The questions that matter most depend on your work.

- Mitsubishi Heavy Industries activities in steel and cement. Are partnerships like ArcelorMittal and Heidelberg Materials progressing from pilot to commercial deployment?

- What is the outlook for MHI’s carbon capture deployment in the maritime shipping sector by 2026?

- Which cement and steel operators are adopting MHI’s KM CDR Process™ technology?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.