MCFC Grid Solutions: Fuel Cell Energy $160 M Eversource PPA, 7.4 MW Plant, and 4 Commercial Agreements (2021-2026)

MCFC Utility-Scale Projects, Fuel Cell Energy’s 7.4 MW Hartford Plant

Molten carbonate fuel cell (MCFC) technology is moving from niche industrial applications to a validated solution for utility-scale baseload power, primarily because severe grid interconnection bottlenecks create a premium for reliable, on-site generation. Prior to 2025, MCFC projects were often smaller in scale, focused on demonstrating reliability and building a project pipeline. The market dynamic has shifted, with fuel cells now positioned as a critical enabler for power-intensive industries like data centers that cannot afford the multi-year delays associated with traditional grid upgrades.

- Between 2021 and 2024, the primary focus was on securing a backlog of service and generation agreements and executing smaller-scale projects, which established a foundation for future growth but did not yet prove utility-scale bankability in the United States.

- A significant inflection point occurred in January 2022 with the announcement of Fuel Cell Energy’s $160 million, 20-year Power Purchase Agreement (PPA) with utilities Eversource and United Illuminating for the 7.4 MW Hartford plant. This long-term contract with investment-grade utilities provides the commercial validation required for larger projects.

- The market opportunity is defined by grid constraints, with interconnection wait times for new projects extending five to seven years. This gridlock makes on-site, distributed generation a highly attractive alternative for customers requiring reliable power.

- In response, Fuel Cell Energy announced in March 2026 the launch of a new 12.5 MW system specifically designed for the data center market, signaling a strategic pivot to larger, standardized power blocks to meet this urgent demand.

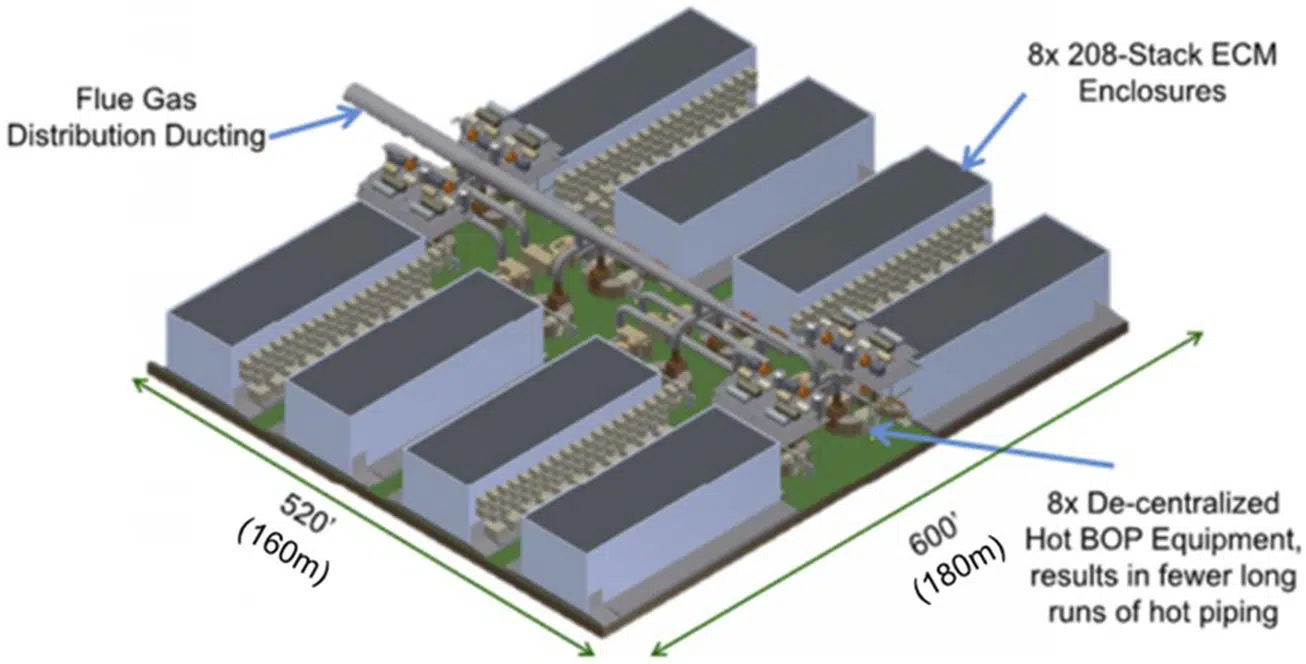

Diagram Details Utility-Scale MCFC Plant Layout

The section discusses MCFC technology’s move to utility-scale projects like the Hartford plant, and the chart provides a detailed technical layout of such a plant, making it a perfect match.

(Source: Frontiers)

$1.19 Billion Backlog, Fuel Cell Energy Investment in Production

Fuel Cell Energy’s financial and investment strategy has matured from securing one-off project contracts to funding a systematic manufacturing expansion aimed at capturing the recurring, high-demand data center market. This shift is supported by a substantial backlog of contracted revenue that provides the financial stability needed for capital-intensive investments in production capacity.

- As of late 2025, the company reported a total project backlog of $1.19 billion, a key indicator of secured future revenue from committed generation, service, and advanced technology agreements.

- In March 2026, the company announced a strategic investment in production expansion to support its newly launched 12.5 MW systems, a direct response to the growing pipeline of data center and industrial power projects.

- The PPA for the $160 million Hartford project, along with a separate $160 million module supply agreement with Gyeonggi Green Energy (GGE) in South Korea, represent major capital inflows that de-risk and enable this manufacturing scale-up.

Table: Fuel Cell Energy Major Contracts and Backlog (2025 – 2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Data Center Production Expansion | Mar 2026 | Announced manufacturing expansion to support new 12.5 MW systems targeting the data center market, addressing grid capacity limitations and long permitting delays. | Renewable Energy Industry |

| Annual Report Backlog | Feb 2026 | Reported a total backlog of $1.19 billion as of October 31, 2025, representing a significant pipeline of future revenue from committed projects. | Stock Titan |

| Hartford Power Plant PPA | Jan 2025 | Secured a $160 million, 20-year PPA with Eversource and United Illuminating for a 7.4 MW fuel cell plant, validating the technology for utility-scale baseload power. | Hartford Business Journal |

| Gyeonggi Green Energy (GGE) | Jan 2025 | Agreement to supply 1.4 MW carbonate fuel cell modules, adding approximately $160 million to the company’s product backlog for the South Korean market. | [PDF] Company Presentation |

Fuel Cell Energy 4 Strategic Alliances (2025 to 2026)

Recent partnerships confirm a three-pronged strategy: locking in long-term revenue with domestic utilities, expanding market share in established international territories, and creating new markets by targeting off-grid data centers with waste-fuel-to-power solutions. These alliances are crucial for de-risking market entry and scaling deployment across different segments. While Fuel Cell Energy builds its portfolio, competitors like Bloom Energy continue to announce larger-scale projects, underscoring the competitive intensity of the stationary fuel cell market.

- The PPA with utilities Eversource and United Illuminating for the Hartford plant establishes a bankable, long-term revenue model for utility-scale deployment in the regulated U.S. market, serving as a blueprint for future projects.

- In July 2025, an agreement with China General Nuclear Power Group (CGN) for a 10 MW repowering project demonstrated the value of upgrading existing infrastructure with modern, low-carbon carbonate fuel cell systems.

- A January 2025 agreement with Gyeonggi Green Energy (GGE) to supply modules for an industrial complex reinforced Fuel Cell Energy’s strong market position in the mature South Korean industrial power sector.

- The March 2025 collaboration with Diversified Energy and TESIAC to form an acquisition and development company is a strategic move to serve the high-value off-grid data center market by leveraging undervalued fuel sources like coal mine methane.

Table: Fuel Cell Energy Strategic Partnerships (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| CGN | Jul 2025 | Agreement for a 10 MW repowering project in China, replacing older modules and signaling momentum in international utility markets. | Fuel Cell Energy |

| Diversified Energy, TESIAC | Mar 2025 | Formation of a development company to deliver off-grid, net-zero power for data centers using coal mine methane and natural gas as fuel. | Fuel Cell Energy |

| Eversource, United Illuminating | Jan 2025 | 20-year, $160 million PPA for 7.4 MW of baseload power from the Hartford plant, providing revenue certainty and validating the utility-scale model. | Globe Newswire |

| Gyeonggi Green Energy (GGE) | Jan 2025 | Module supply agreement for the Hwaseong Baran Industrial Complex in South Korea, adding approximately $160 million to the company’s product sales backlog. | [PDF] Company Presentation |

US vs. South Korea, Fuel Cell Energy Geographic Focus

While South Korea has historically been a primary market for Fuel Cell Energy’s industrial and power generation modules, the United States is rapidly emerging as a key growth region for larger, utility-scale projects driven by grid constraints and the massive power demands of data centers. The company’s geographic strategy now appears to be a dual focus: maintaining its stronghold in the mature Korean market while aggressively pursuing new, high-value opportunities in North America.

- Between 2021 and 2024, a significant portion of commercial activity and backlog was tied to the South Korean market, which has strong government support for hydrogen and fuel cell technologies for industrial decarbonization.

- The January 2025 announcement of the 7.4 MW Hartford, CT project marked a pivotal moment, establishing a firm commercial anchor for utility-scale deployments in the U.S. This market is driven by the need for grid resilience and alternatives to congested transmission systems.

- The company has maintained its focus on Asia, as evidenced by the $160 million GGE module supply agreement in January 2025 and the 10 MW CGN repowering project in July 2025, confirming the continued importance of these markets.

- The strategic pivot towards the data center market with the new 12.5 MW system is primarily targeted at the North American market, where the concentration of hyperscale data centers and grid limitations is most acute.

MCFC Commercial Viability, Fuel Cell Energy Efficiency Gains

Molten carbonate fuel cell technology has reached commercial maturity for providing utility-scale baseload power, a status validated by long-term power purchase agreements and steady advancements in core technical performance that enhance its economic competitiveness against other power sources. While earlier deployments focused on proving long-term reliability, recent developments confirm its readiness for larger and more critical applications.

Stationary Power Dominates 2025 Fuel Cell Market

The section argues for the commercial viability of MCFCs in utility-scale baseload power, and the chart confirms this by showing stationary power is the dominant application in the fuel cell market.

(Source: IMARC Group)

- The period between 2021 and 2024 was characterized by the operation of sub-10 MW projects that demonstrated the technology’s high availability and capacity factors, building an operational track record.

- The 20-year PPA for the Hartford plant, announced in January 2025, serves as the definitive validation point for the commercial and financial viability of MCFC technology at the multi-megawatt grid-support scale.

- In its 2025 annual report, Fuel Cell Energy announced a critical technical milestone: an improvement in its carbonate fuel cells’ electrical efficiency from 47% to 50%. This directly improves the levelized cost of energy (LCOE) by reducing fuel consumption per megawatt-hour generated.

- The launch of a scalable 12.5 MW system in March 2026, a significant increase from legacy 1.4 MW and 2.5 MW platforms, shows the technology’s platform is mature enough to be scaled to meet the much larger power demands of data centers and industrial users.

SWOT Analysis, Fuel Cell Energy’s Market Position and Risks

Fuel Cell Energy’s core technology strengths in providing continuous, fuel-flexible power are directly aligned with pressing market needs for grid stability and distributed generation, creating significant opportunities. However, the company faces intense competition from more efficient technologies and must flawlessly execute on its growing backlog to convert commercial traction into market leadership.

Fuel Cell Market Forecasted to Exceed $45B

This section provides a SWOT analysis, and the chart contextualizes the ‘Opportunities’ by showing significant market growth and the ‘Threats’ by listing competing technologies.

(Source: IMARC Group)

Table: SWOT Analysis for MCFC Utility-Scale Deployment

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Demonstrated high reliability in industrial settings; fuel flexibility (natural gas, biogas). | Validated as Class 1 renewable baseload power (Hartford PPA); inherent suitability for carbon capture. | The Hartford PPA with Eversource validated the technology’s bankability for long-term, utility-scale contracts, moving it beyond niche industrial use cases. |

| Weaknesses | Lower electrical efficiency compared to SOFC competitors; perceived as higher cost. | Efficiency improved from 47% to 50%, but still faces a competitive gap. Project execution timelines are critical. | The efficiency gain helps close the gap with competitors, but the primary validation came from demonstrating that the total value proposition (baseload, on-site) commands a premium LCOE. |

| Opportunities | Growing need for grid stability and distributed power. | Explosive data center power demand; 5-7 year grid interconnection queues creating a market for on-site power; carbon capture incentives. | The acute power crisis in the data center industry has become the primary market driver, turning the high cost of fuel cells into a viable alternative to years-long grid upgrade delays. |

| Threats | Competition from Bloom Energy and other stationary power solutions; natural gas price volatility. | Bloom announced a much larger 80 MW project in South Korea; continued dependence on natural gas feedstock; policy risk around tax incentives. | The scale of competitor projects has increased, raising the stakes for execution. The formation of a venture to use waste methane is a direct attempt to mitigate natural gas price risk. |

Fuel Cell Energy 2026 Outlook: Hartford Plant Performance

The single most critical factor for Fuel Cell Energy’s success over the next 18 months is the operational performance of the Hartford plant. Its real-world reliability and efficiency data will serve as the definitive benchmark for securing future utility and data center contracts. Flawless execution is required, as this project is the linchpin for the company’s strategic pivot to larger-scale deployments.

Diagram Shows MCFC Use for CO2 Capture

The section’s SWOT analysis explicitly mentions ‘inherent suitability for carbon capture’ as a strength, and this process flow diagram perfectly illustrates that specific technical application.

(Source: Frontiers)

- If this happens: The 7.4 MW Hartford plant consistently operates with a capacity factor above 95% while maintaining its stated 50% electrical efficiency throughout its initial 12-24 months of operation.

- Watch this: The announcement of the first commercial deployment of the new 12.5 MW system, ideally with a hyperscale data center operator or large industrial client, which would validate the company’s new product strategy.

- These could be happening: Other utilities and private customers gain confidence in the technology’s bankability for mission-critical loads, accelerating the conversion of the $1.19 billion backlog and leading to new, larger PPA announcements that compete more directly on scale with rivals like Bloom Energy.

The questions your competitors are already asking

This report covers one angle of FuelCell Energy’s transition to utility-scale MCFC deployment. The questions that matter most depend on your work.

- What is the operational performance of FuelCell Energy’s 7.4 MW Hartford plant since the PPA was announced?

- What is the outlook for utility-scale MCFC deployment in grid-constrained markets by 2030?

- FuelCell Energy activities in new platforms. Is the 12.5 MW platform progressing from announcement to commercial deployment?

- Which utilities and data center operators are adopting carbonate fuel cells for baseload grid support?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.