Grid Bottlenecks Threaten AI Growth: How 2026 Capital Flows Target Power-First Infrastructure

AI Power Demand Creates Grid Bypass: How 2026 Projects Prioritize Speed-to-Power

Capital is increasingly bypassing traditional grid upgrade timelines by funding on-site and direct power solutions to meet the immediate, high-density energy needs of AI data centers. This strategic shift addresses the critical bottleneck of slow grid interconnection and insufficient capacity, prioritizing speed-to-power over reliance on public infrastructure development.

- Between 2021 and 2024, corporate clean energy procurement focused on grid-connected Power Purchase Agreements (PPAs) for wind and solar. The period from 2025 to today shows a definitive shift toward behind-the-meter and dedicated generation, a strategy designed to circumvent multi-year interconnection queues and secure reliable power for gigawatt-scale AI campuses.

- On-site fuel cells have emerged as a key solution to this problem, exemplified by the $5 billion Brookfield and Bloom Energy financing partnership announced in October 2025. This deal provides capital for grid-independent deployments at data centers, establishing a commercially scalable model that was not prevalent prior to 2025.

- A new co-location model that integrates power generation directly with data centers is gaining traction, validated by the initiative from Google, Intersect Power, and TPG in December 2024. The plan aims to catalyze $20 billion in new clean energy projects built alongside data centers, effectively internalizing the power supply chain.

- Modular, off-grid solutions are also attracting capital, as shown by the January 2026 launch of Exowatt’s arm to provide modular, always-on clean energy for data centers. This signals growing investor confidence in private, self-contained energy systems as a direct response to public grid limitations.

Billions Redirected: Analyzing 2026 Investment in Off-Grid and Dedicated AI Power Solutions

Investment patterns in 2025 and 2026 reveal a strategic redirection of capital away from generalized grid decarbonization and toward targeted, high-reliability power infrastructure that directly serves AI data centers. This flow of private capital is outpacing and outmaneuvering public funding initiatives, focusing on immediate, project-specific deployment.

- The largest capital commitments are now tied directly to data center build-outs, including their dedicated power infrastructure. Google’s plan to invest $40 billion in three new Texas data centers through 2027 is a primary example, where capex covers the entire power delivery and cooling system, not just the IT hardware.

- Private equity has identified this convergence as a central investment theme for the coming decade. Blackstone anticipates $1 trillion in capital spending to power the AI-driven energy transition, while KKR and Energy Capital Partners have entered an agreement to invest up to $50 billion in AI data centers, a significant increase in focus from the 2021-2024 period.

- The $5 billion financing partnership between Brookfield and Bloom Energy in October 2025 for on-site fuel cells is a key signal. It validates that immediately deployable, grid-independent technologies are now considered bankable assets for institutional investors seeking to capitalize on AI’s power demand.

- While governments are responding, their actions are slower and smaller in scale than direct corporate investment. For instance, Canada’s proposed $15 billion fund to support green data centers contrasts with the faster, more targeted multi-billion-dollar commitments from individual corporations.

Table: Key Investments in Dedicated Power for AI Data Centers (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Google (Alphabet) | 2026-2027 | $40 Billion capital expenditure for three new Texas data centers. The investment includes all associated power and cooling infrastructure, demonstrating a model of integrated power system development. | AI’s Explosive Energy Demand May Unexpectedly Strengthen … |

| Brookfield & Bloom Energy | Oct 2025 | $5 Billion financing partnership to deploy Bloom Energy’s solid oxide fuel cells. The goal is to provide grid-independent, on-site power for data centers, bypassing grid constraints. | Brookfield and Bloom Energy Launch $5 Billion Partnership to … |

| Google, Intersect Power, & TPG | Dec 2024 | Plan to catalyze $20 Billion in renewable energy projects co-located with new data centers. This strategic alliance aims to build gigawatts of dedicated clean power capacity. | Google, Intersect Power, TPG Launch $20 Billion Data Center Clean … |

| Meta & Entergy | Dec 2024 | $10 Billion AI-optimized data center in Louisiana. The partnership requires utility Entergy to develop new renewable resources to ensure the facility is matched with 100% clean power. | Meta Selects Northeast Louisiana as Site of $10 Billion Artificial … |

Strategic Alliances Forge New Energy Models: How Tech and Energy Partnerships Are Reshaping Grid Decarbonization

Strategic partnerships formed between 2024 and 2026 among tech giants, energy producers, and private capital represent a fundamental evolution from simple procurement to active co-development of energy infrastructure. These alliances are purpose-built to solve the grid bottleneck and secure the reliable, large-scale power that AI requires.

Tech Sector Dominates Clean Energy Procurement

This chart shows the technology sector is responsible for two-thirds of all contracted carbon-free energy in the US. This data quantifies the massive impact of the strategic tech and energy partnerships discussed in the section.

(Source: S&P Global)

- The partnership between Google, Intersect Power, and TPG in December 2024 establishes a new model for the industry. By linking $20 billion in renewable project development directly to new data center capacity, the alliance creates a template for bypassing public grid limitations entirely.

- Microsoft’s partnerships to secure nuclear power, highlighted by the September 2024 deal supporting the reopening of the Three Mile Island plant, demonstrate a strategic move toward 24/7 carbon-free baseload power. This directly addresses the reliability standard that the intermittent renewable PPAs common in 2021-2024 could not meet.

- The December 2024 agreement between Meta and utility Entergy for a $10 billion data center is another key signal. It commits the utility to developing new renewable resources specifically for one industrial customer, tying grid development directly to a private company’s needs.

- Collaborations are also forming to make the existing grid more efficient, such as the June 2024 partnership between Deloitte and Utilidata. Their work to deploy AI-enabled smart meters aims to help grid operators better manage the rising demand, offering a different approach to solving the bottleneck from within the system.

Power Plays: Regional Hotspots Emerge for AI Data Centers and Dedicated Clean Energy Investment

The geographic deployment of AI data centers and their associated energy infrastructure has consolidated in regions offering favorable regulations, land availability, and access to scalable power. This marks a shift from traditional tech hubs toward areas that can support massive, energy-intensive industrial development.

Regional Hotspot Shows Exponential Demand Growth

This chart provides a direct example of a regional hotspot, detailing the exponential rise in data center energy demand within a single utility’s territory. This visualizes the concentrated industrial-scale load growth described in the section.

(Source: Bloomberg.com)

- While data center growth was more dispersed between 2021-2024, regions with permissive energy markets have become central from 2025 onward. Texas is a prime example, attracting Google’s $40 billion investment in three new data centers, driven by its deregulated energy market and abundant land.

- The U.S. Midwest, particularly Ohio, has become a key destination due to its strong renewable energy potential and established industrial infrastructure. Google’s 15-year solar PPA with Total Energies to power its Ohio data centers confirms this trend.

- Canada is actively positioning itself as a major hub, led by Alberta’s $100 billion AI Data Centres Strategy announced in late 2024, which leverages its natural gas resources for power generation with carbon capture. A proposed $15 billion federal fund further signals the country’s national ambition to attract investment.

- Internationally, specific European markets with strong renewable policies are attracting targeted investment. Germany is a key site for offshore wind development tied to AI, validated by Google’s 15-year PPA announced in February 2026.

Beyond Solar and Wind: How AI Power Demand Is Accelerating Commercialization of Firm, Clean Energy Technologies

The 24/7 reliability requirement of AI data centers is forcing the rapid maturation of firm, dispatchable, low-carbon technologies, including nuclear, fuel cells, and energy storage. This demand is moving these technologies from pilot stages to commercially viable solutions much faster than previous climate-driven timelines.

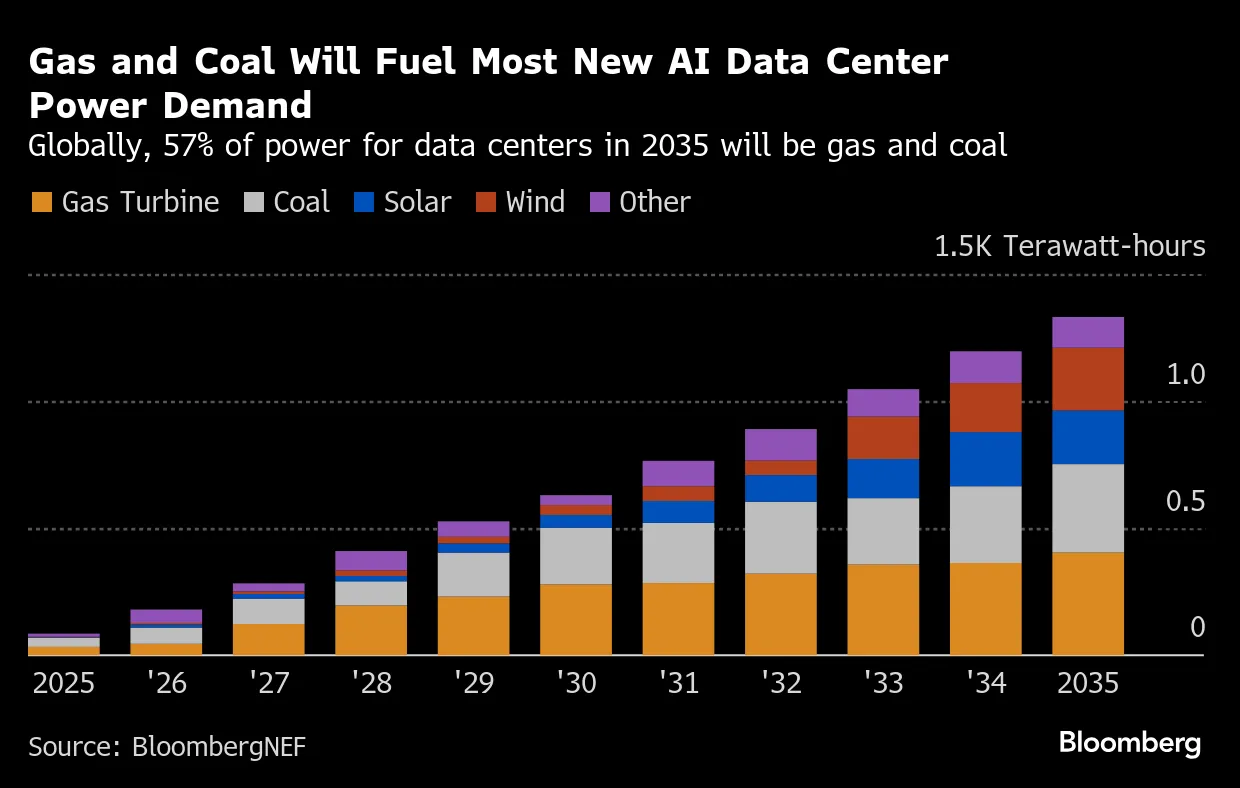

AI’s Firm Power Gap Filled by Fossil Fuels

This forecast shows that natural gas and coal are projected to meet over half of AI’s power demand by 2035. This highlights the critical need to accelerate the commercialization of firm, clean technologies to avoid reliance on fossil fuels.

(Source: Bloomberg.com)

- During the 2021-2024 period, corporate procurement was overwhelmingly focused on mature solar and wind PPAs. The period from 2025 onward is defined by significant commercial validation for alternative technologies that can provide the continuous baseload power AI demands.

- Solid oxide fuel cells from providers like Bloom Energy have achieved commercial scale for data center applications. This is validated by the $5 billion Brookfield financing partnership of October 2025, which treats the technology as a bankable, deployable asset.

- Nuclear power is transitioning from a legacy asset into a strategic component for Big Tech’s energy strategy. Microsoft’s support for the Three Mile Island reopening and Amazon’s commitment to invest in Small Modular Reactors (SMRs) signal a corporate-led revival of the technology for its carbon-free, firm power attributes.

- Natural gas with carbon capture (CCUS) is now being positioned as a commercially viable, low-carbon bridging solution. Companies like Shell and KALi NA announced projects in 2024 to develop natural gas-powered data centers with integrated CCS, a solution tailored to meet both power and climate targets.

SWOT Analysis: Navigating Risks and Opportunities in AI-Driven Grid Decarbonization

The convergence of AI and energy creates immense opportunities for rapid clean energy deployment but also introduces significant threats related to grid fragmentation and equity if not managed holistically. Corporate capital is the primary strength, while the inertia of public infrastructure remains the core weakness.

AI to Drive 31-Fold Power Demand

This chart quantifies the scale of the opportunity and risk, showing US power demand from AI alone is projected to skyrocket 31-fold by 2035. This massive growth underpins the strategic strengths and weaknesses outlined in the SWOT analysis.

(Source: PR Newswire)

- Strengths are rooted in the massive, fast-moving capital from tech companies and private equity, which can underwrite new projects without relying on public subsidies.

- Weaknesses stem from the slow pace of public grid modernization and regulatory delays for transmission, which is the primary driver for capital to seek bypass solutions.

- Opportunities lie in the AI-driven acceleration of next-generation technologies like SMRs, long-duration storage, and hydrogen, creating the first scaled commercial market for these solutions.

- Threats include the creation of private “energy islands” that could leave the public grid less stable and more expensive for all other users, exacerbating energy inequity.

Table: SWOT Analysis for AI-Driven Grid Decarbonization

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Corporate climate goals and PPA-driven renewable procurement. Capital flow was significant but followed traditional project finance models. | Massive, direct corporate capex (Google’s $40 B) and private equity funds (Blackstone’s $1 T theme) for integrated power and data center projects. | The scale and speed of private capital has become the primary driver of new clean energy deployment, dwarfing previous investment levels and bypassing traditional financing. |

| Weaknesses | Grid interconnection queues and permitting delays were recognized problems but not yet at a crisis point for tech growth. | Grid capacity is a hard physical and regulatory limit to AI expansion, with the U.S. grid projected to add only 25 GW of capacity in the next 3 years, far short of demand. | The grid bottleneck has been validated as the single greatest constraint on AI growth, forcing a strategic shift toward on-site and dedicated power generation. |

| Opportunities | Focus on cost reduction and scaling of mature technologies like solar, wind, and lithium-ion batteries. | Accelerated commercialization of firm, clean power: nuclear (Microsoft), fuel cells (Bloom Energy), and natural gas with CCUS (Shell). | AI’s demand for 24/7 reliable power created the first scaled commercial market for advanced clean technologies, shortening their path to widespread adoption. |

| Threats | Risk of greenwashing and reliance on renewable energy credits without adding new generation capacity. | Emergence of privately funded “energy islands” that bypass the public grid, potentially increasing costs and instability for other users. | The solution to the grid bottleneck is creating a new risk: a bifurcated energy system where well-capitalized tech firms have resilient, clean power while the public grid lags. |

2026 Outlook: Watching for Grid Fragmentation as Private Capital Builds ‘AI Energy Islands’

If corporate capital continues to prioritize speed-to-power through dedicated, off-grid, or behind-the-meter solutions, the primary trajectory for 2026 is the emergence of privately-funded, decarbonized “energy islands, ” which risk exacerbating public grid instability. The critical action for stakeholders is to monitor the scale and regulatory treatment of these private energy systems.

Public Grid Investment Hits Record High

This chart provides essential context, showing that investment in the traditional public grid is at a record high. This sets up the central conflict between strengthening public infrastructure and the private development of ‘energy islands’ that could lead to grid fragmentation.

(Source: Forbes)

- Watch for an increase in partnerships that mirror the Google-Intersect Power-TPG model, where power generation and data center load are co-developed as a single, integrated asset. This signals a formalization of the grid-bypass strategy.

- Monitor the deal flow for on-site power providers like Bloom Energy and modular solutions like Exowatt. A continued surge in large-volume orders from data center operators will validate that the market is choosing to bypass grid interconnection queues altogether.

- Track regulatory responses from state and federal bodies. New rules designed to either fast-track transmission projects or regulate these private energy systems could significantly alter the current trajectory and the economics of these bypass solutions.

- Observe the technology mix in new project announcements. A growing number of deals involving nuclear SMRs or natural gas with CCUS will confirm that reliability and firm power have become non-negotiable requirements, overriding the low levelized cost of intermittent renewables.

Frequently Asked Questions

Why are companies building their own power sources for AI instead of just connecting to the public grid?

Companies are bypassing the public grid because it cannot meet the immediate and massive power demands of new AI data centers. The primary bottlenecks are multi-year delays for grid interconnection and insufficient existing capacity. This new strategy allows companies to achieve ‘speed-to-power’ by funding their own on-site or dedicated generation, rather than waiting for slow public infrastructure upgrades.

What is the main difference in how AI power projects were funded before 2025 compared to now?

Before 2025 (from 2021-2024), corporate clean energy funding focused on purchasing power from large, grid-connected wind and solar projects through Power Purchase Agreements (PPAs). Starting in 2025, capital has shifted decisively toward funding on-site, behind-the-meter, and dedicated power generation that is built specifically for and often co-located with the data centers, as seen in the Google, Intersect Power, and TPG initiative.

Besides solar and wind, what other energy technologies are being used to meet AI’s 24/7 power demand?

To ensure the 24/7 reliability that AI requires, which intermittent renewables alone cannot provide, companies are investing in ‘firm’ and dispatchable low-carbon technologies. Key examples highlighted in the text include on-site solid oxide fuel cells (like the Brookfield and Bloom Energy partnership), nuclear power (supported by Microsoft), and natural gas with carbon capture and storage (CCUS).

Who are the main financial and corporate players driving this shift to dedicated AI power?

The shift is being driven by a combination of tech giants, private equity firms, and energy companies. Key players mentioned include Google (investing $40 billion in Texas data centers with integrated power), private equity like Blackstone (anticipating a $1 trillion investment theme) and KKR, and strategic partnerships such as the $5 billion deal between Brookfield and Bloom Energy for on-site fuel cells.

What is the biggest risk associated with this trend of building private ‘energy islands’ for AI?

The primary threat, as identified in the SWOT analysis, is the creation of a two-tiered energy system. As large corporations build their own resilient, private power infrastructure, the public grid that serves everyone else could become less stable and more expensive. This trend risks ‘grid fragmentation’ and could worsen energy inequity by leaving the public with a less reliable and more costly power supply.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.