Fuel Cell Energy MCFC Grid Constraints, 450 MW SDCL Plan, 275% Pipeline Surge, and 2 Strategic MOUs (2021 to 2026)

Grid Interconnection Delays, Fuel Cell Energy Data Center Adoption (2021-2026)

The primary driver shifting the energy market for data centers is the failure of traditional grid infrastructure to meet the speed and scale of AI power demand, creating a significant commercial opportunity for on-site fuel cell solutions. Before 2025, fuel cell adoption was characterized by smaller, bespoke projects focused on reliability and combined heat and power benefits. The AI-driven power demand has since turned multi-year grid interconnection queues from an inconvenience into a critical business failure point, forcing technology providers and data center operators to pivot to rapidly deployable, behind-the-meter generation.

- Between 2021 and 2024, fuel cell deployments were often niche, such as Fuel Cell Energy‘s 1.4 MW plant for Hartford Hospital, which highlighted reliability but was not driven by the urgent speed-to-power needs of the AI sector. Grid delays were a known issue but had not yet catalyzed a market-wide shift to on-site generation for hyperscalers.

- Beginning in 2025, the AI “demand shock” made grid availability the central constraint to growth. Modern AI facilities require up to 200 MW, exposing the inadequacy of grid infrastructure and creating a massive opening for companies that can bypass interconnection queues.

- In response, technology providers now compete on speed and standardization. Fuel Cell Energy launched a standardized 12.5 MW power block designed for quick deployment, while competitor Bloom Energy demonstrated its ability to deliver power for Oracle‘s data centers within 90 days.

- This shift is validated by commercial data, with Fuel Cell Energy‘s business development pipeline surging by 275% since February 2025, an increase attributed almost entirely to data center customers who cannot afford to wait for grid upgrades.

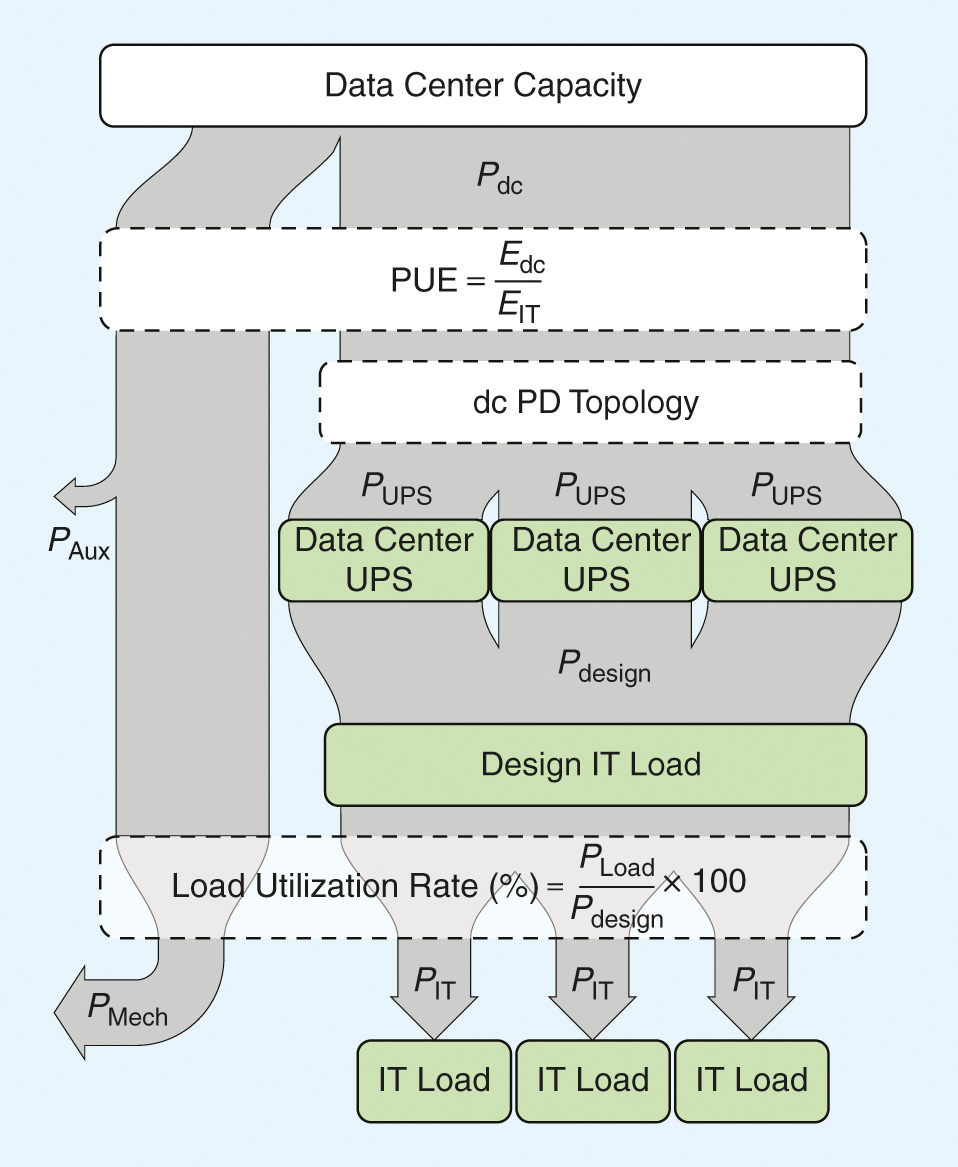

Visualizing Data Center Power Inefficiency

This Sankey diagram illustrates the energy losses within a typical data center’s power infrastructure, providing crucial context for the grid-level challenges and the need for more efficient on-site power solutions discussed in the section.

(Source: Nxtbook)

$150 M Hy Axiom Investment, Fuel Cell Energy’s $275 M Pivot (2022-2025)

Capital is increasingly flowing to fuel cell companies that demonstrate a clear strategy to capture the lucrative AI data center market, rewarding those with scalable technology and established strategic partnerships. The contrast in financing activities before and after the AI power demand surge highlights this trend, with recent investments directly tied to servicing data center clients.

- In July 2023, Hy Axiom, a subsidiary of Doosan, secured approximately $150 million in a private investment round specifically to accelerate its growth and fund capital expenditures, positioning it to compete for large-scale projects before the AI demand fully intensified.

- Bloom Energy‘s strategic focus on data centers resulted in a 1, 000% stock price increase in the year leading up to October 2025, demonstrating strong investor confidence in its ability to execute on the AI power opportunity.

- In November 2025, Plug Power announced plans to unlock $275 million to pivot its business toward the data center market, signaling a reactive move to catch up with competitors who had already established a foothold.

- Large infrastructure investors are now driving demand for technology suppliers. Black Rock acquired Aligned Data Centers in October 2025 and secured agreements with GE Vernova and Next Era to scale energy solutions for AI.

Table: Strategic Fuel Cell Investments and Financing

| Company / Funder | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Plug Power | Nov. 2025 | Announced plans to unlock $275 million in capital to pivot its strategy toward supplying the data center power market, indicating a strategic shift to capture this high-growth segment. | Reuters |

| Black Rock (Global Infrastructure Partners) | Oct. 2025 | Acquired Aligned Data Centers and entered partnerships with GE Vernova and Next Era Energy to fund and develop power infrastructure at the scale required for AI. | Global Infrastructure Partners |

| Hy Axiom (Doosan) | Jul. 2023 | Secured approximately $150 million from investors to fund R&D and capital expenditures, accelerating its ability to manufacture and deploy its fuel cell technology. | Hartford Business Journal |

Fuel Cell Energy 450 MW SDCL Plan, Bloom Energy 1 GW AEP Deal (2024-2026)

Strategic partnerships have evolved from small-scale technology demonstrations into massive, multi-megawatt development agreements with energy financiers and utilities, validating fuel cells as a primary solution for the AI power challenge. This progression from technology-focused collaborations to large-scale deployment frameworks marks a significant maturation of the market.

Bloom Energy Highlights Data Center Dominance

This infographic directly validates the section’s mention of large-scale deals by competitors, quantifying Bloom Energy’s ~1.5 GW deployed capacity and its stated focus on the data center market.

(Source: Arya’s Substack)

- Before 2024, partnerships were often focused on technology development and integration. For instance, Ballard Power Systems partnered with Vertiv in June 2024 to develop hydrogen-powered backup solutions, and Hy Axiom worked with Ceres to advance SOFC technology.

- A market turning point occurred in November 2024 when Bloom Energy announced a landmark agreement with utility American Electric Power (AEP) to supply up to 1 GW of fuel cells for data centers, signaling that utilities now view fuel cells as a core solution for serving their largest customers.

- In January 2026, Fuel Cell Energy followed with a similar large-scale strategy, signing a letter of intent with financier Sustainable Development Capital LLP (SDCL) to develop up to 450 MW of on-site power projects for data center customers globally.

- The trend extends to the broader energy infrastructure space, with data center developer Vantage partnering with Liberty Energy in January 2026 to develop and operate 1 GW of power solutions.

Table: Data Center Power Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Fuel Cell Energy & SDCL | Jan. 2026 | Signed a letter of intent to develop up to 450 MW of on-site fuel cell power projects for data centers, providing a financing and deployment framework to capture global demand. | Stock Titan |

| Vantage Data Centers & Liberty Energy | Jan. 2026 | Formed a strategic partnership to develop and operate 1 GW of power solutions for next-generation data centers, creating a dedicated energy supply chain for hyperscale needs. | Vantage Data Centers |

| Bloom Energy & AEP | Nov. 2024 | Announced a major agreement for AEP to procure up to 1 GW of Bloom Energy‘s fuel cells as a behind-the-meter solution for its large industrial and data center customers. | Yahoo Finance |

| Fuel Cell Energy & Inuverse | Jul. 2025 | Signed an MOU to develop data centers in South Korea using Fuel Cell Energy‘s platforms, targeting a key international market with high power density needs. | Fuel Cell Energy Investors |

| Ballard Power Systems & Vertiv | Jun. 2024 | Formed a technology partnership to develop hydrogen fuel cell backup power solutions for data centers, ranging from 200 k W to multiple megawatts. | Ballard Power Systems |

US vs South Korea, Fuel Cell Energy Global Data Center Push

While the United States is the epicenter of the AI power demand and initial large-scale fuel cell deployments, strategic activity in power-constrained Asian markets like South Korea indicates a global expansion strategy is underway for key players. The geographic focus has sharpened significantly since 2024, concentrating on regions where grid limitations and high-density power needs intersect.

Mapping AI Power Demand Hotspots

This map visually supports the section’s focus on geography by pinpointing AI data center power hotspots in the US, directly corresponding to the text’s claim that the United States is the epicenter of demand.

(Source: Leyline Renewable Capital)

- Between 2021 and 2024, international activity was more fragmented. For example, in November 2022, Hy Axiom entered the China market with a 105 MW supply agreement and separately pursued maritime demonstrations with Shell, reflecting a broader, less targeted global approach.

- From 2025 onward, the United States has become the primary market for large-scale deployments, driven by its hyperscale data center boom and severe grid bottlenecks. Landmark deals like Bloom Energy‘s 1 GW agreement with AEP and Crusoe‘s 1.8 GW development plan in Wyoming confirm the U.S. as the core battleground.

- Fuel Cell Energy‘s July 2025 MOU with Inuverse to develop data centers in South Korea is a key strategic signal. It shows a deliberate move to replicate the U.S. on-site power model in other mature economies facing similar grid constraints and high energy costs.

- This targeted geographic expansion is a direct response to where AI infrastructure is being built. Companies are no longer just exporting technology; they are deploying solutions tailored to the specific energy challenges of high-growth data center hubs.

SOFC & MCFC Commercial Scale, Fuel Cell Energy’s 12.5 MW Block

Fuel cell technology has transitioned from niche applications to commercially validated, modular, multi-megawatt power blocks, with speed of deployment and fuel flexibility emerging as the key metrics of maturity for the AI data center market. The primary technological shift has been from customized, project-specific engineering to standardized, scalable products designed to meet urgent customer timelines.

- In the 2021-2024 period, fuel cells were proven but often deployed in smaller, bespoke projects like Fuel Cell Energy‘s 1.4 MW hospital plant. Technology partnerships, such as Hy Axiom’s collaboration with Ceres on SOFCs, focused on advancing core technical capabilities rather than rapid commercial scaling.

- Starting in 2025, the market demanded standardization to achieve scale. Fuel Cell Energy‘s launch of a 12.5 MW packaged power block and Hy Axiom‘s unveiling of a 10 MW power block at CES 2026 directly address this need for rapid, repeatable deployments.

- The metric of success shifted from pure electrical efficiency to “speed-to-power.” Bloom Energy‘s ability to deliver operational power to an Oracle data center within 90 days set a new competitive benchmark that highlights this change.

- Future-proofing for decarbonization has become a critical feature. While natural gas is the dominant fuel source today, the forward-looking technological development is focused on hydrogen. Caterpillar‘s successful demonstration of a 3 MW hydrogen fuel cell system with Microsoft validates this transition pathway.

SWOT Analysis, Fuel Cell Energy Execution Risks and Market Opportunity

Fuel Cell Energy’s primary strength is its established carbonate and solid oxide technology, which it has recently repackaged to target the high-growth data center market. Its greatest opportunity lies in converting its surging sales pipeline into firm contracts. However, its main weakness is a demonstrated lag in securing the gigawatt-scale commercial deals already won by competitors, posing a significant execution risk.

FuelCell Energy Financials Underscore Execution Risk

This chart’s data on negative gross margins and fluctuating revenue provides a clear financial illustration of the weaknesses and execution risks discussed in FuelCell Energy’s SWOT analysis.

(Source: Seeking Alpha)

Table: SWOT Analysis for Fuel Cell Energy’s Data Center Strategy

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strength | Diverse fuel cell technology portfolio (MCFC, SOFC) and experience in utility-scale projects and carbon capture. | Launched a standardized 12.5 MW power block for data centers and announced plans to triple manufacturing capacity. | The company successfully pivoted its existing technology to a specific, high-demand market with a tailored product offering. |

| Weakness | History of financial losses and a lack of focus on the emerging data center market, resulting in smaller, one-off projects. | Despite a 450 MW development plan, has not yet announced a firm, binding contract on the scale of Bloom Energy‘s 1 GW AEP deal. | The gap between announced ambition and contracted revenue remains a key weakness, as competitors secure market-defining deals. |

| Opportunity | General market growth for clean, distributed energy and potential for hydrogen and carbon capture applications. | Massive, immediate demand from AI data centers for grid-independent power, validated by a 275% surge in its business pipeline. | The market opportunity became tangible and urgent, shifting from a long-term energy transition theme to an immediate infrastructure need. |

| Threat | Broad competition from other fuel cell manufacturers (Bloom Energy, Hy Axiom) and traditional power generation. | Direct, validated competition from Bloom Energy (1 GW deal) and Hy Axiom (10 MW block for AI), who have clear first-mover advantages in the large-scale data center segment. | Competitors have successfully translated their technology into large-scale commercial wins, setting a high bar for market entry and share capture. |

Scenario Modelling: Will Fuel Cell Energy Convert its 275% Pipeline into GW-Scale Deals?

The critical scenario for Fuel Cell Energy in the next 12-18 months is whether it can convert its rapidly growing 275% business development pipeline into firm, multi-hundred-megawatt contracts that rival the scale of its competitors. Success hinges on executing its 450 MW plan with SDCL and demonstrating an ability to compete on speed, scale, and bankability.

- If the SDCL partnership translates into the first 100 MW–200 MW of projects being financed and deployed quickly in 2026, watch for an acceleration in market validation and investor confidence similar to what Bloom Energy experienced in 2025.

- If Fuel Cell Energy fails to announce a major binding contract from this pipeline within the next year, this could mean its commercial offering or manufacturing capacity is struggling to compete on price or speed against established players for large-scale data center deployments.

- A key leading indicator of success would be an announcement of manufacturing capacity expansion beyond the currently planned tripling, as this would signal that firm, large-volume orders are materializing.

- The most important signal to track is the conversion of the 450 MW letter of intent with SDCL into definitive, binding purchase orders, which would validate the company’s strategy and its ability to execute in the competitive AI power market.

The questions your competitors are already asking

This report covers one angle of the commercial race between fuel cell providers to power AI data centers. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the on-site data center power market, from FuelCell Energy to HyAxiom?

- What is actually happening with FuelCell Energy’s 450 MW data center plan with SDCL since it was announced?

- How does FuelCell Energy’s MCFC technology compare to competing solutions for bypassing grid interconnection delays?

- Which hyperscale data center operators are adopting on-site fuel cells to meet AI power demand?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.