X-energy SMR Funding for Data Centers, $1.4 B Raised, $500 M Amazon Investment, and 4 Key Projects (2021 to 2026)

X-energy SMR Commercial Scale, 2 Major Projects, and Big Tech Adoption (2021-2026)

The period from 2025 to 2026 marks a definitive shift from government-led demonstration projects to corporate-funded commercial execution for Small Modular Reactors (SMRs), driven by the urgent need for clean, firm power to support Artificial Intelligence. Whereas the 2021-2024 period was defined by technology validation and public funding, the market has now transitioned to a model where technology giants are directly underwriting the path to commercialization to secure their future energy supply.

- Before 2025, the SMR market was characterized by reliance on government support, such as the U.S. Department of Energy’s Advanced Reactor Demonstration Program (ARDP). The economic viability remained a significant question, underscored by the November 2023 cancellation of the Nu Scale Power project with UAMPS after projected costs soared nearly 55%, making it too expensive for its municipal utility partners.

- Starting in 2025, a wave of private capital, led by corporate venture arms of major technology companies, began to de-risk commercialization. Amazon committed over $500 million to SMR development and is a key investor in X-energy’s recent funding rounds. This mirrors moves by Google and Microsoft, which have also entered into major nuclear power agreements to fuel their data centers.

- This strategic shift is best exemplified by the types of projects gaining traction. While the utility-led Nu Scale project failed, new projects are being structured around guaranteed corporate offtake. An example is the planned X-energy SMR deployment to power a Dow chemical facility in Texas, a model of co-locating generation with industrial demand that is directly applicable to data center campuses.

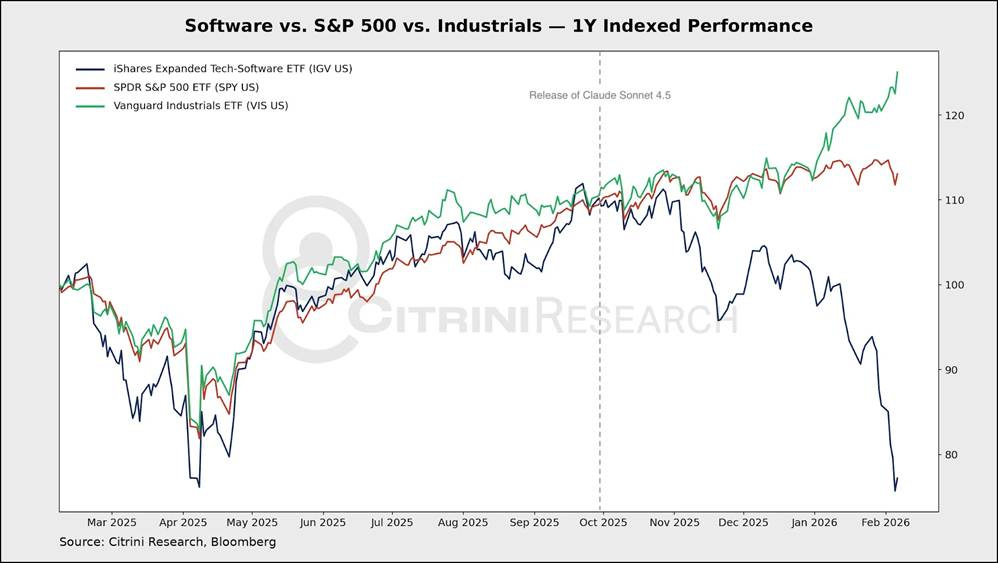

Industrials Outperform Software Amid AI Power Demand

This chart visualizes the market transition described in the section, where capital rotates from the tech/software sector (IGV) to the industrials sector (VIS) to fund the clean, firm power needed for AI.

(Source: Citrini Research)

$3.7 B in Capital, Advanced Nuclear Funding for X-energy and Competitors

Late-stage venture funding for advanced nuclear developers accelerated dramatically in 2025, with over $3.7 billion raised by key players, signaling strong investor conviction in the technology’s critical role for powering AI infrastructure. This influx of execution-focused capital is intended to bridge the gap from demonstration to commercial-scale manufacturing and deployment, a sharp contrast to the earlier-stage, R&D-focused funding rounds seen prior to 2024.

- X-energy secured $1.4 billion across two funding rounds in 2025 alone, a $700 million Series C-1 in February and another $700 million Series D in November. This level of late-stage funding demonstrates a clear market signal that investors believe the company is ready to transition from technology development to building and deploying its reactors.

- The investment trend extends across the advanced nuclear sector. Competitors also secured significant capital, including Terra Power’s $650 million round with participation from NVentures (Nvidia’s venture arm), Radiant Nuclear’s $300 million+ Series D, and Commonwealth Fusion Systems’ $863 million round, showing broad market appetite.

- This corporate-led investment cycle represents a fundamental change in the financing model for new nuclear. In the past, developers relied heavily on government grants and fickle public markets. Now, tech companies with immense balance sheets are acting as strategic investors to guarantee a future customer base for their own power-hungry operations.

Table: Key Advanced Nuclear Investments (2025 to 2026)

| Company | Time Frame | Funding Details and Strategic Purpose | Source |

|---|---|---|---|

| Starring Energy | Apr 2026 | Raised ~$138 M (1 B yuan) in a Series A round led by China General Nuclear to advance its fusion technology. | 36 Kr |

| Radiant Nuclear | Dec 2025 | Raised over $300 M in a Series D round to advance mass production of its Kaleidos microreactor for remote and military applications. | Radiant Nuclear |

| X-energy | Nov 2025 | Secured $700 M in Series D funding, with Amazon as a key strategic investor, to accelerate commercial deployment for industrial and data center use. | Neutron Bytes |

| Commonwealth Fusion Systems | Sep 2025 | Announced $863 M in new funding alongside a major partnership with Italian energy giant Eni. Investors include Bill Gates, Google, and Khosla Ventures. | MIT Technology Review |

| Terra Power | Aug 2025 | Raised $650 M in a funding round joined by NVentures, Nvidia’s venture capital arm, explicitly linking nuclear development to powering AI. | Remio.ai |

| X-energy | Feb 2025 | Closed an upsized $700 M Series C-1 financing round to accelerate development and deployment of its advanced SMR technology. | X-energy |

Big Tech Partnerships, X-energy, Amazon, and 4 Major Nuclear Power Deals

Strategic partnerships have evolved from government-developer collaborations to direct alliances between SMR developers and technology companies, creating a new offtake model that guarantees demand and secures project financing. Before 2024, major partnerships involved entities like the DOE providing R&D funding. Now, tech giants are structuring multi-billion dollar deals to procure nuclear power directly, effectively becoming the anchor customers that make new projects bankable.

- Amazon set a precedent in March 2024 by acquiring a data center campus directly connected to the Susquehanna nuclear plant for $650 million from Talen Energy. This was followed by its direct investments in X-energy’s development in 2025, signaling a clear strategy to co-locate its AI infrastructure with reliable, carbon-free power sources.

- Microsoft followed a similar playbook by entering an agreement to help restart the Three Mile Island nuclear plant and signing PPAs to power its data centers. This move focuses on leveraging existing nuclear assets for immediate power needs, complementing the long-term strategy of funding new SMRs.

- Google has also entered the space, signing a deal in October 2024 to back the development of new nuclear plants and committing to a 1.8 GW agreement with Elementl Power in 2025. This shows that across the board, hyperscalers see nuclear power as a mandatory component of their energy strategy.

- These corporate PPAs and direct investments mirror the playbook used a decade ago to scale the solar and wind industries. By acting as a guaranteed first customer with a massive balance sheet, Big Tech provides the revenue certainty needed to unlock project financing for high-capital-expenditure SMR projects. Other major cloud players, such as Oracle, are also exploring SMRs to meet their AI power needs.

United States Focus, X-energy SMR Projects and Favorable Policy Shifts

The United States has firmly established itself as the epicenter for SMR commercialization, driven by a combination of surging domestic data center power demand and a sharp, favorable pivot in federal energy policy in 2025. While the 2022 Inflation Reduction Act provided foundational tax credits, policy enacted in 2025 created direct mandates and incentives that strongly favor domestic nuclear deployment over other regions.

- A major policy catalyst was the “One Big Beautiful Bill Act” (OBBBA), signed into law on July 4, 2025. This legislation established a comprehensive nuclear energy policy by enhancing production tax credits and reversing parts of the IRA to favor an “energy dominance” agenda centered on nuclear power.

- In May 2025, Executive Orders were issued directing the Nuclear Regulatory Commission (NRC) to approve SMR applications in no more than 18 months. This directly addresses the regulatory delays that have historically plagued the industry and provides a clear signal of political will to accelerate deployment.

- This supportive environment has concentrated major projects within the U.S., including Terra Power’s Natrium reactor in Wyoming and X-energy’s project in Texas. While other countries are pursuing SMRs, such as the UK with Rolls-Royce and its SMR program and China with significant fusion investment, the combination of policy and private capital makes the U.S. the primary market for near-term commercial deployment.

X-energy SMR Technology, TRL 7.5 Status and Commercial Deployment Path (2025-2026)

Advanced reactor technology, particularly SMRs, has advanced from the demonstration phase (TRL 6-7) toward commercial readiness (TRL 8-9), with late-stage funding in 2025 aimed at overcoming the final manufacturing and supply chain hurdles for scaled deployment. The core scientific principles are well-established; the current challenge is one of industrialization, not invention.

- As of mid-2025, SMR technology is estimated to be at a Technology Readiness Level (TRL) of 7.5. This signifies that a system prototype has been demonstrated in an operational environment, moving beyond laboratory-scale tests. The capital flowing into the sector is now focused on the expensive leap to TRL 9, which is a full-scale commercial system proven through successful operation.

- A critical dependency for many advanced reactors is the supply of High-Assay Low-Enriched Uranium (HALEU) fuel. The U.S. currently has a structural supply gap, and scaling domestic production is a multi-year effort. This supply chain bottleneck, rather than reactor technology itself, is a primary risk to deployment timelines.

- X-energy’s Xe-100 reactor utilizes TRi-structural ISOtropic (TRISO) particle fuel, which is considered “meltdown-proof” due to its layered ceramic and carbon coating that traps radioactive byproducts. This inherent safety feature is a key technological advantage that can help accelerate regulatory approval and improve public acceptance. Advanced materials for these reactors are expected to be commercially deployed between 2027 and 2029.

SWOT Analysis, X-energy Nuclear-Powered Data Center Execution Risks

While surging AI-driven demand and powerful policy tailwinds create significant strengths and opportunities for SMRs, critical execution weaknesses related to cost and timelines, along with external threats from supply chains and competing technologies, remain substantial risks. The market’s enthusiasm, reflected in recent funding rounds, must be weighed against a history of project delays and cost overruns in the nuclear sector.

Table: SWOT Analysis for SMR Deployment for Data Centers

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | High capacity factor (>90%), carbon-free, baseload power. Small footprint suitable for co-location. | Same core strengths, but now valued as a unique solution for 24/7 AI power needs that intermittent renewables cannot meet. | The 2024-2025 AI boom validated the strategic importance of firm, clean power, elevating SMRs from a niche solution to a critical enabler of the tech economy. |

| Weaknesses | High First-of-a-Kind (FOAK) costs and economic uncertainty, as demonstrated by the Nu Scale/UAMPS project cancellation in 2023 due to an ~55% cost increase. | FOAK cost risk remains, but is now being underwritten by deep-pocketed tech companies (e.g., Amazon) rather than smaller municipal utilities. | The financing model shifted from public/utility-led to private/corporate-led, which provides more capital to absorb initial cost overruns but does not eliminate the underlying risk. |

| Opportunities | Decarbonization of industrial heat and electricity grids. Government funding through programs like the ARDP. | Explosive, non-negotiable power demand from AI and data centers created a massive new addressable market. Favorable policy (OBBBA) in 2025. | The market opportunity shifted from a gradual, policy-driven energy transition to an urgent, commercially-driven need to power AI, dramatically increasing the TAM and accelerating timelines. |

| Threats | Long regulatory approval timelines with the NRC. Competition from cheaper renewables and natural gas. Public opposition. | Supply chain bottlenecks (HALEU fuel, specialized components). Competition from fast-improving geothermal and existing nuclear plants. | While policy aims to shorten regulatory drag, supply chain constraints have emerged as a more immediate and tangible threat to meeting deployment targets in the late 2020 s. |

First FID Signal, X-energy, Amazon, and Nuclear Data Center Projects

The most critical signal to monitor in the next 12-18 months is the first Final Investment Decision (FID) for a commercial SMR project backed by a Big Tech Power Purchase Agreement (PPA). This milestone will validate the economic model for nuclear-powered data centers, prove that FOAK costs can be managed, and trigger a wave of project financing for subsequent deployments.

- If this happens: A company like Terra Power or X-energy announces FID on a multi-reactor plant for a data center campus.

- Watch this: How the project’s Levelized Cost of Electricity (LCOE) is structured in the PPA. An LCOE below $100/MWh would signal commercial competitiveness. Also, monitor the NRC’s processing time for the first SMR applications under the 2025 executive orders to see if the 18-month target is achievable.

- These could be happening: A surge of investment into the HALEU fuel supply chain to address the primary bottleneck. Competitors like HD Hyundai or specialized players like BWXT may accelerate their plans to capture a piece of the industrial and maritime markets. Utilities like TVA will likely fast-track their own advanced reactor programs to avoid being disintermediated by direct corporate PPAs.

The questions your competitors are already asking

This report covers one angle of the capital market signals for SMR commercialization. The questions that matter most depend on your work.

- Which SMR companies are gaining or losing ground in the race to power data centers?

- What is the outlook for SMR deployment in AI data centers by 2030?

- X-energy investments and funding. Is its path to commercialization on track following its $1.4B raise?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.