Equinor Blue Hydrogen Focus, $700 M CCS Project with Shell, $25.6 B Centrica Deal, and 3 Partnerships (2025)

Blue Hydrogen and CCS Infrastructure: Equinor’s Strategic Pivot in 2025

In 2025, Equinor executed a significant strategic recalibration, moving away from broad renewable targets to a pragmatic focus on blue hydrogen enabled by large-scale Carbon Capture and Storage (CCS) infrastructure. This deliberate pivot was a direct response to industry-wide economic headwinds and project cancellations that afflicted pure-play green hydrogen developers, allowing Equinor to de-risk its energy transition by building a market on more mature technologies.

- Faced with challenging market conditions, Equinor reduced its 2030 renewable capacity target from 12-16 GW to 10-12 GW and halved its investment in the sector, reallocating capital to projects with more immediate commercial viability.

- This shift was highlighted by the shelving of a major green hydrogen pipeline from Norway to Germany, a joint plan with Shell, signaling a retreat from large-scale green infrastructure in the near term.

- In its place, Equinor prioritized blue hydrogen by advancing the H 2 M Eemshaven project in the Netherlands with partner Linde to the Front-End Engineering Design (FEED) stage.

- This “blue-first” approach is designed to build market scale, develop supply chains, and establish a customer base for low-carbon hydrogen, while mitigating the financial and technological risks that caused other companies, like Statkraft, to cease new green hydrogen developments.

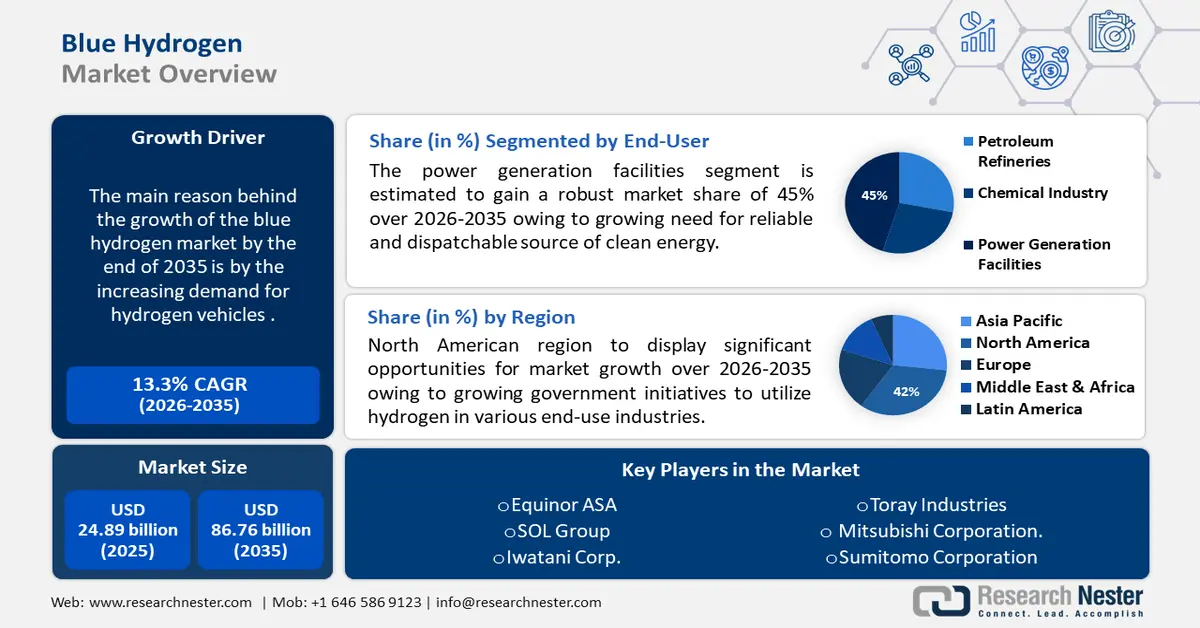

Blue Hydrogen Market to Reach $86.76B by 2035

The section discusses Equinor’s strategic pivot towards blue hydrogen. A chart forecasting the significant growth of the blue hydrogen market provides essential context for why a company would make such a strategic move.

(Source: Research Nester)

$700 M in CCS Funding, Equinor Prioritizes Enabling Infrastructure

Equinor’s investment pattern in 2025 clearly prioritized foundational infrastructure for the low-carbon economy over speculative, direct investments in green hydrogen production. The company’s capital allocation strategy focused on building the non-negotiable enablers for its blue hydrogen ambitions, demonstrating a disciplined, long-term approach to market creation.

- The cornerstone investment was a NOK 7.5 billion (approximately $700 million) commitment to expand the Northern Lights carbon capture and storage (CCS) project, a critical piece of infrastructure that makes large-scale blue hydrogen production commercially feasible.

- This major capital outlay for CCUS contrasts with a strategic scale-back in other areas, including the decision to discontinue certain power-from-shore electrification projects, thereby concentrating capital on core transition projects.

- While large-scale investments focused on blue hydrogen, Equinor Ventures maintained a long-term view on green hydrogen by participating in a €3 million equity funding round for Hysun and investing in Hy Si Labs, a company developing a novel liquid hydrogen carrier.

Clean Hydrogen Investment Surpasses $100B by 2025

This section details Equinor’s specific funding for CCS infrastructure. A chart showing the broader investment landscape in clean hydrogen provides a macro-level context for the capital being deployed in the sector, highlighting the trend Equinor is part of.

(Source: Precedence Research)

Table: Equinor Strategic Investments and Capital Reallocations (2025)

| Investment Target / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Hysun | Oct 2025 | Participation in a €3 million equity funding round to support emerging green hydrogen technology. | Equinor |

| Hy Si Labs | Sep 2025 | Strategic venture investment in a novel liquid hydrogen carrier technology to address storage and transport challenges. | Equinor |

| Northern Lights Project | Aug 2025 | $700 million (NOK 7.5 B) investment with partners Shell and Total Energies to expand CO₂ transport and storage capacity, enabling blue hydrogen production. | [PDF] Global CCS Institute |

| Renewable Energy Portfolio | May 2025 | Halved investment spending and reduced 2030 capacity targets to focus capital on core business and more mature low-carbon solutions. | REN 21 |

Value Chain Partnerships, Equinor Secures $25.6 B Centrica Deal

In 2025, Equinor structured its partnerships to construct a complete low-carbon hydrogen value chain, from production and transport to downstream markets. The alliances combined Equinor’s upstream and CCS capabilities with the industrial expertise and market access of its partners, ensuring demand and infrastructure were developed in parallel.

- A monumental gas supply agreement valued at over £20 billion ($25.6 billion) was signed with Centrica, which critically includes a framework for a future transition to hydrogen, securing a long-term offtake partner in the key UK market.

- The partnership with industrial gas leader Linde on the H 2 M Eemshaven blue hydrogen project in the Netherlands brings together production expertise and ensures the project is designed for industrial-scale offtake.

- Continued collaboration with SSE Thermal and Centrica focused on developing low-carbon hydrogen projects for the UK’s industrial clusters, building anchor demand in a core strategic region.

Captive Hydrogen Market to Reach $189.9B by 2030

The section discusses large-scale value chain partnerships, such as the Centrica deal. A chart on the ‘captive’ market, which refers to hydrogen produced for a specific end-use or industrial process, is highly relevant. These partnerships are designed to serve this captive demand.

(Source: MarketsandMarkets)

Table: Equinor Hydrogen-Related Partnerships (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Linde | Aug 2025 | Advanced the H 2 M Eemshaven low-carbon hydrogen project in the Netherlands to the Front-End Engineering Design (FEED) stage. | [PDF] Global CCS Institute |

| Centrica | Jun 2025 | Signed a $25.6 B (£20 B) long-term gas supply deal that includes provisions for a future transition to hydrogen, securing a major offtake pathway. | Fuel Cells Works |

| Shell | Nov 2025 | A previously planned joint project to develop a major hydrogen pipeline from Norway to Germany was shelved, reflecting a strategic pivot to phased, de-risked projects. | [PDF] DNV |

Northwest Europe, Equinor Focuses on a Core Geographic Hub

Equinor’s hydrogen activities in 2025 were geographically concentrated in Northwest Europe, a strategic decision to build a tightly integrated, cross-border system leveraging its existing North Sea assets and proximity to mature industrial markets in the UK, Netherlands, and Germany.

- Norway was established as the central hub for carbon storage infrastructure through the expansion of the Northern Lights CCS project, positioning the country to serve as a CO₂ depository for the continent.

- The Netherlands was designated as the primary site for blue hydrogen production, with the H 2 M Eemshaven project selected for its strategic port access and direct connections to industrial consumers.

- The United Kingdom served as a primary target for market creation and offtake, evidenced by the $25.6 billion supply and transition agreement with Centrica and collaborations with SSE Thermal to decarbonize industrial clusters.

Asia Pacific Leads 2025 Hydrogen Generation Market

The section focuses on Equinor’s strategy in Northwest Europe. A chart showing that Asia Pacific is the leading market provides important global context. It helps frame Equinor’s regional focus as a strategic choice, possibly to avoid a crowded market or to leverage unique advantages in Europe.

(Source: Precedence Research)

Technology Maturity: Commercial-Scale Blue Hydrogen vs. Venture-Stage Green

Equinor’s 2025 actions drew a clear line between the maturity of blue and green hydrogen pathways, confirming that it views blue hydrogen, supported by CCS, as an investable, commercial-scale technology today, while treating green hydrogen as an emerging field best addressed through targeted venture capital.

- The advancement of the H 2 M Eemshaven project to the FEED stage, coupled with the $700 million investment in Northern Lights, validates that the combination of steam methane reforming and CCS is considered a technically and commercially ready pathway for large-scale deployment.

- In contrast, Equinor’s engagement with green hydrogen technology remained at the venture level. Investments in startups like Hy Si Labs (hydrogen carriers) and Hysun were designed to gain exposure and knowledge without committing major capital, signaling these technologies are not yet deemed mature enough for large-scale projects.

- The decision to shelve the large-scale green hydrogen pipeline to Germany further underscores the view that the infrastructure and economics for transporting pure green hydrogen at scale remain significant hurdles compared to leveraging existing natural gas expertise and infrastructure.

Green Hydrogen Faces Major Implementation Gap

This section directly compares the commercial maturity of blue hydrogen against the venture-stage status of green hydrogen. The chart’s headline about a ‘Major Implementation Gap’ for green hydrogen perfectly visualizes and supports the core argument of this section.

(Source: Nature)

SWOT Analysis, Equinor Hydrogen Strategy and Market Position

Equinor’s recalibrated hydrogen strategy in 2025 leveraged its core competencies to secure a de-risked position in the low-carbon economy, but it also reinforced its dependence on fossil fuels and exposed it to long-term policy and technology risks.

- The company’s primary strength lies in its extensive experience with large offshore projects and natural gas, which it successfully translated into a first-mover advantage in European CCS infrastructure.

- However, this blue-hydrogen-first approach creates a potential weakness by tying its transition strategy to the future of natural gas and the public and regulatory acceptance of CCS.

- The key opportunity is to establish and dominate a “CCS-as-a-service” market, enabling decarbonization across Europe while creating a captive market for its own hydrogen production.

- The main threat remains the possibility of disruptive cost reductions in green hydrogen or unfavorable policy shifts that could render its significant investments in blue hydrogen infrastructure less competitive sooner than anticipated.

Low-Carbon Hydrogen Market Shows Strong Growth Potential

This section introduces a SWOT analysis of Equinor’s strategy. A high-level chart showing the ‘Strong Growth Potential’ of the market directly corresponds to the ‘Opportunities’ component of a SWOT analysis, setting a positive backdrop for the strategy.

(Source: maximize market research)

Table: SWOT Analysis for Equinor’s Hydrogen Strategy (2025)

| SWOT Category | 2021 – 2024 Evidence | 2025 Evidence | What Changed / Validated |

|---|---|---|---|

| Strength | Existing natural gas reserves and infrastructure; expertise in offshore projects and geology. | $700 M investment in Northern Lights CCS project; advancing H 2 M Eemshaven blue hydrogen project. | Theoretical advantages were converted into concrete, large-scale capital projects, validating its ability to execute complex integrated energy and CCS initiatives. |

| Weakness | Dependence on volatile natural gas prices and exposure to criticism for extending fossil fuel use. | Halved renewable investments while signing a $25.6 B gas deal with Centrica. | The strategic pivot away from renewables deepened the company’s reliance on its fossil fuel business as the engine for its low-carbon transition. |

| Opportunity | Early-stage Mo Us for hydrogen and CCS with European partners. | Secured partnerships with Linde and Centrica; moved H 2 M Eemshaven to FEED stage. | Abstract opportunities were translated into tangible, commercially structured projects with major industrial partners, solidifying a clear path to market. |

| Threat | General risk of competition from green hydrogen and changing regulations. | Shelved a major green hydrogen pipeline with Shell; competitors like Statkraft exited new green H 2 projects due to costs. | The market for large-scale green hydrogen projects proved economically unviable for now, validating Equinor’s more cautious, blue-focused approach but also highlighting the extreme volatility and uncertainty in the hydrogen sector. |

Scenario Modelling: Equinor’s H 2 M Eemshaven FID is the Signal to Watch

The single most critical validation of Equinor’s infrastructure-first hydrogen strategy will be a Final Investment Decision (FID) on a major blue hydrogen production facility in the next 12-18 months. This action would confirm that the entire value chain, from gas supply and CO₂ storage to final offtake, is commercially viable.

- If an FID is announced for the H 2 M Eemshaven project, it will signal that binding offtake agreements are in place and the project’s economics are robust, likely triggering a new wave of investment across the European hydrogen and CCS ecosystem.

- Watch for new commercial agreements for the Northern Lights project. Securing third-party industrial emitters as customers is a key leading indicator of demand for CO₂ storage and validates the “CCS-as-a-service” business model.

- Monitor the development of the “future hydrogen transition” clause within the Centrica agreement. The first concrete pilot or plan to blend hydrogen into the UK gas supply will provide a crucial timeline for large-scale market adoption.

- Conversely, a delay in the FID for H 2 M Eemshaven or a slowdown in new customers for Northern Lights would suggest that even this pragmatic blue hydrogen strategy is encountering significant commercial or regulatory hurdles, casting doubt on the near-term scalability of the European low-carbon hydrogen market.

Chart Compares 2050 Energy Mix Scenarios

The section’s title explicitly mentions ‘Scenario Modelling’. A chart that compares different 2050 energy mix scenarios is a direct and perfect match, illustrating the kind of long-term thinking and planning discussed in the text.

(Source: RFF.org)

The questions your competitors are already asking

This report covers one angle of Equinor’s low-carbon hydrogen commercialization strategy. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the European low-carbon hydrogen market?

- What is actually happening with the Equinor-Shell partnership since the green hydrogen pipeline was shelved?

- What is the outlook for blue hydrogen deployment in the Netherlands and Germany by 2030, given Equinor’s pivot?

- Equinor investments and funding. Is the H2M Eemshaven project with Linde progressing from FEED to a final investment decision?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.