Data 4 SMR Strategy, 1.92 GW AWS Deal, 34 Last Energy Units, and 5 Hyperscaler PPA Signals (2021 to 2026)

Data Center SMR Adoption, from Theory to Commercial Scale Projects

The relationship between data centers and nuclear power has evolved from a theoretical concept into a strategic necessity, driven by artificial intelligence’s exponential energy demand and the inadequacy of public grids. Data center operators have shifted from being passive electricity consumers to becoming active anchor clients for advanced nuclear projects, using long-term power agreements to underwrite the development of Small Modular Reactors (SMRs) and secure a stable, carbon-free power supply for future growth.

- Between 2021 and 2024, the industry focus was on policy and potential, with the EU’s Net-Zero Industry Act recognizing SMRs as a strategic technology and early U.S. projects like Talen Energy’s data center campus setting a conceptual precedent. However, commercial activity was limited to feasibility studies and early-stage agreements, such as Last Energy’s PPA for 34 SMR units in Poland.

- The period from 2025 to 2026 marked a definitive commercial shift, with major U.S. hyperscalers executing tangible, multi-gigawatt offtake agreements. These include Amazon‘s 1.92 GW PPA with Talen Energy and Microsoft‘s deal with Constellation Energy to secure 837 MW, establishing a bankable model for financing nuclear assets with private capital.

- This transition validates the role of data centers as “anchor customers” capable of de-risking the high upfront capital costs of first-of-a-kind (FOAK) SMRs. A long-term PPA from a creditworthy technology company provides the revenue certainty required for developers to secure financing, which can range from $1 billion to $3 billion per plant.

- The March 2026 unveiling of the European Commission’s comprehensive SMR strategy, including a €200 million guarantee, signals that Europe is now fostering the policy environment necessary for companies like Data 4 to replicate the U.S. model and secure private nuclear power.

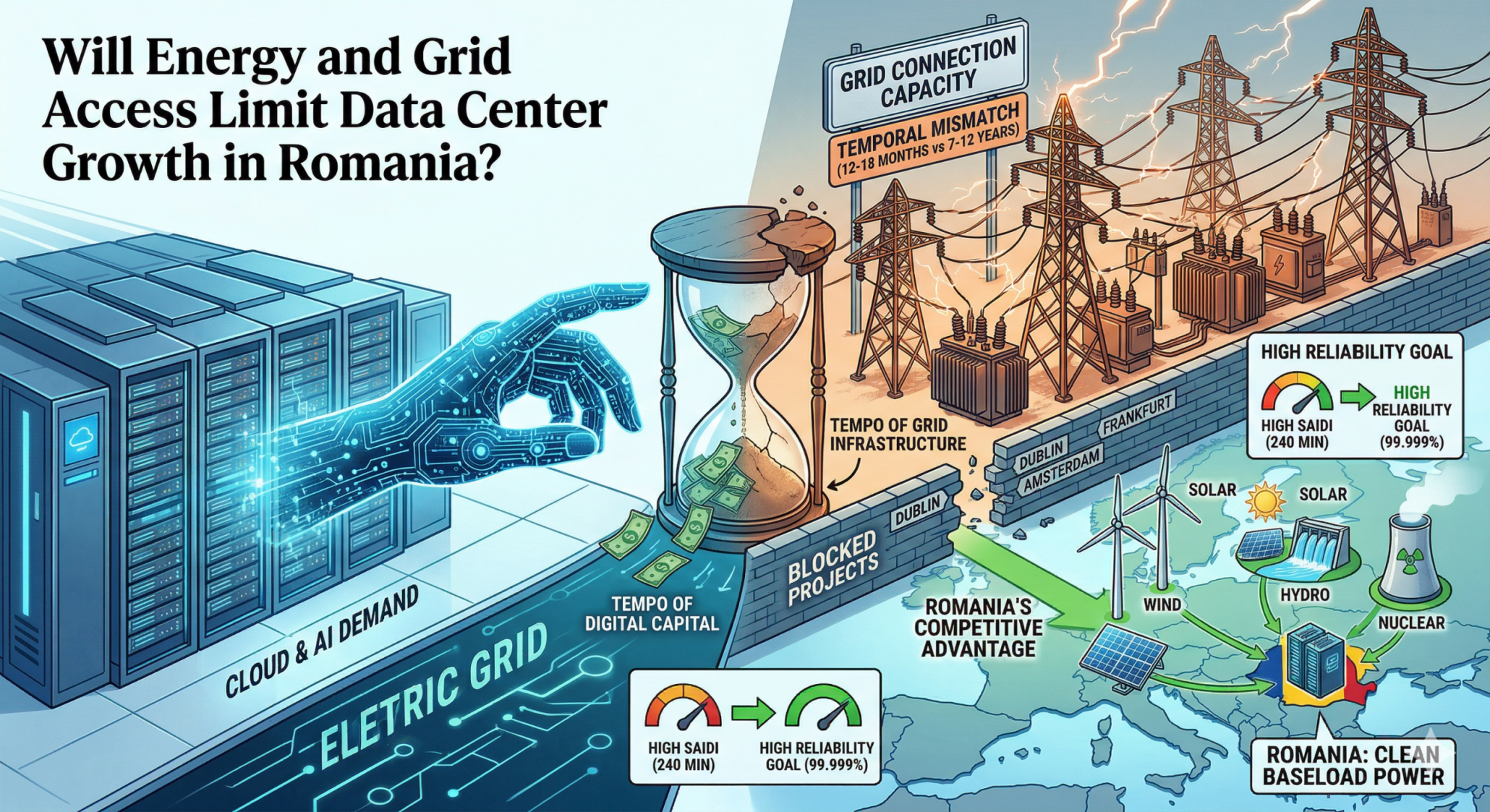

Grid Upgrades Lag Behind AI’s Demand

This chart perfectly visualizes the section’s core theme of ‘inadequacy of public grids’ driven by AI. It shows the temporal mismatch between rapid data center development and slow grid upgrades, explaining the strategic shift toward nuclear power.

(Source: DATACENTER FORUM 2026)

Data 4 SMR Partnerships, 5 Hyperscaler PPAs Signal Market Shift

Hyperscale cloud providers have created the commercial blueprint for securing nuclear power through long-term Power Purchase Agreements (PPAs), demonstrating a viable path for colocation providers like Data 4 to bypass grid constraints in Europe. These multi-decade contracts from creditworthy offtakers are the critical catalyst that makes capital-intensive SMR projects bankable for private investors.

- The PPA model, solidified between 2025 and 2026, involves a data center operator committing to purchase a significant portion or the entire output of a nuclear plant for 15-20 years. This provides the SMR developer with a guaranteed revenue stream, essential for securing the billions in construction financing.

- U.S. technology giants led this charge, with landmark deals that serve as a template. These include a 1.92 GW PPA between AWS and Talen Energy, a 1, 121 MW agreement between Meta and Constellation Energy, and a pact between Google and Kairos Power to develop 500 MW of SMRs.

- By siting SMRs “behind-the-meter” at or near data center campuses, operators can circumvent grid interconnection queues, which can take 5 to 10 years, while also avoiding transmission costs and market price volatility.

- These partnerships are symbiotic: data centers secure the vast, reliable, and clean power they need for AI workloads, while SMR developers gain the financial certainty required to build FOAK reactors and achieve commercial scale.

Table: Hyperscaler Nuclear Power Purchase Agreements (2025-2026)

| Buyer | Nuclear Developer/Provider | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|---|

| AWS (Amazon) | Talen Energy | May 2026 | A 17-year PPA for 1.92 GW of electricity from the Susquehanna nuclear plant to power data center operations, demonstrating a massive commitment to baseload nuclear power. | i Recruit.co |

| Meta | Terra Power | Feb 2026 | Agreement to develop eight Natrium reactors, securing a future supply of advanced nuclear power to support long-term data center growth. | Spencer Fane |

| Microsoft | Constellation Energy | Dec 2025 | PPA to restart Three Mile Island Unit 1, securing 837 MW of baseload power by 2028 to meet AI-driven energy demand. | Introl |

| Meta | Constellation Energy | Oct 2025 | A 20-year PPA for 1, 121 MW from the Clinton Nuclear Power Plant, one of the largest such deals to back data center operations with existing nuclear assets. | POWER Magazine |

| Kairos Power | Feb 2025 | Agreement to develop 500 MW of SMRs co-located near data centers starting in 2030, creating a direct power supply model. | Reuters |

US vs Europe, Data 4 SMR Strategy for EU Grid Constraints

While the United States pioneered data center-nuclear partnerships, Europe is rapidly becoming the next critical market, driven by more severe grid constraints, higher energy price volatility, and a unified policy push to accelerate SMR deployment. This creates a distinct opportunity for continental providers like Data 4 to secure a competitive advantage by locking in long-term, reliable power.

French Reactor Outages Underscore EU Grid Risk

This chart directly supports the section’s focus on Europe’s ‘severe grid constraints’ by providing a specific example. The significant downtime of France’s nuclear fleet highlights the unreliability that makes dedicated SMRs an attractive solution in the EU.

(Source: World Nuclear Industry Status Report)

- From 2021 to 2024, the U.S. was the center of commercial activity, with data center developers actively exploring co-location with nuclear assets. Europe, in contrast, was focused on developing a policy foundation, culminating in the Net-Zero Industry Act, which designated SMRs a strategic technology.

- The dynamic shifted in 2025-2026 as U.S. hyperscalers signed a series of multi-gigawatt PPAs, proving the commercial model. In parallel, Europe moved from policy to action. The European Commission’s March 2026 SMR strategy provides the regulatory certainty and financial incentives needed for private sector deals to materialize.

- Key European nations are leading this charge. The UK is supporting the Rolls-Royce SMR, France is advancing its NUWARD project, and Poland has seen early commercial interest with Last Energy’s agreements. These national efforts are now supported by the pan-EU Industrial Alliance on SMRs.

- The European context is defined by urgency. Grid modernization timelines of 5-10 years are too slow for the pace of AI-driven data center deployment. This makes the “behind-the-meter” SMR model not just an option but a strategic necessity for growth.

SMR Technology Maturity, Data 4 and the Path to Commercial Viability

Small Modular Reactor technology has progressed from design concepts toward commercial viability, with the primary challenge shifting from technical feasibility to overcoming the financial and regulatory hurdles of first-of-a-kind deployment. The entrance of data center operators as anchor customers provides a clear path to resolving these commercialization barriers.

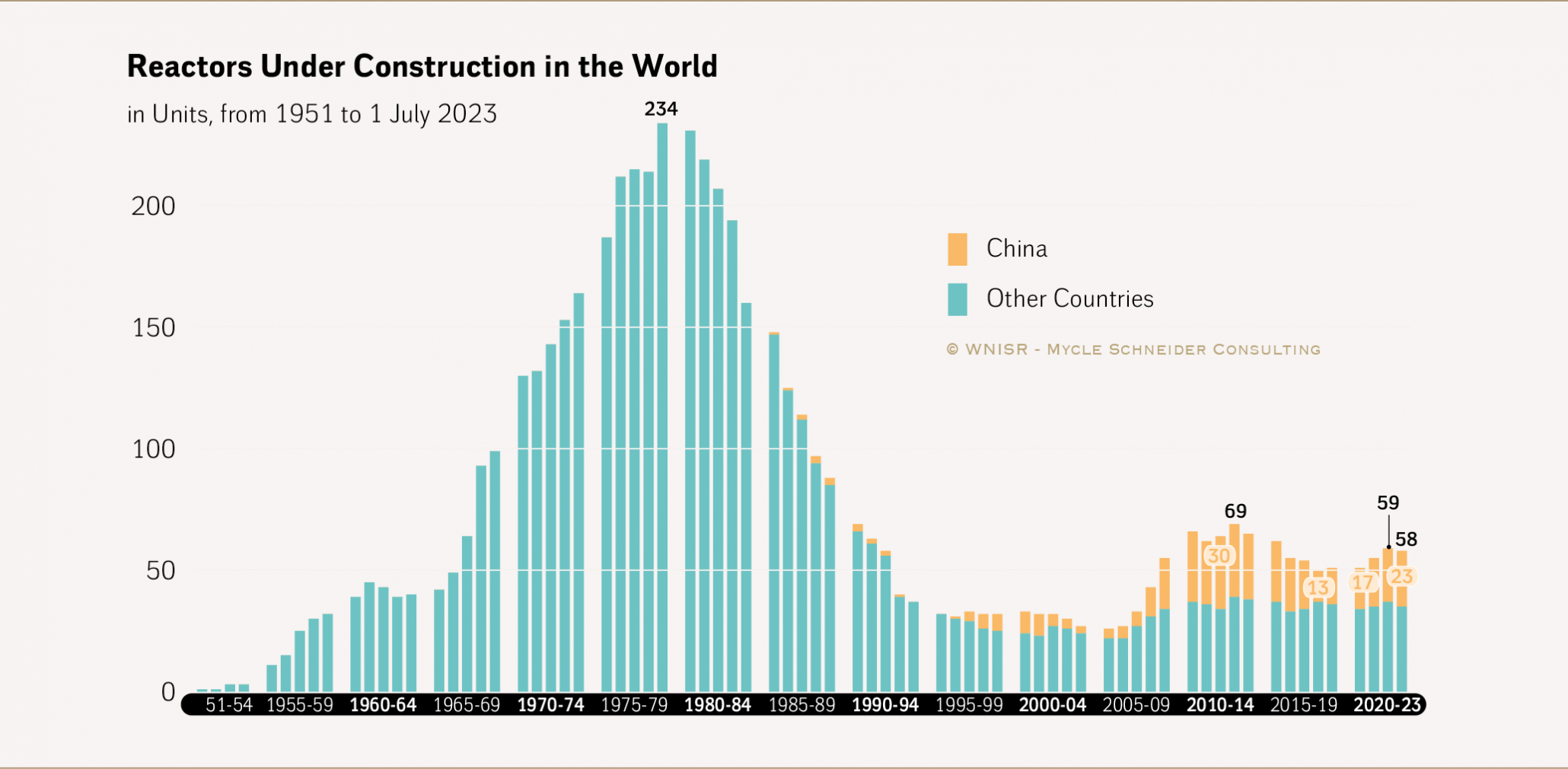

Renewed Growth in Global Nuclear Construction

This chart illustrates the section’s point about SMRs moving toward ‘commercial viability.’ The recent resurgence in reactor construction signals that the industry is progressing from design concepts to tangible projects, aligning with the path to commercialization.

(Source: World Nuclear Industry Status Report)

- In the 2021-2024 period, the SMR conversation was dominated by Technology Readiness Levels (TRLs) and projected Levelized Cost of Electricity (LCOE). Most designs were in development, and high cost estimates, such as Nu Scale Power’s revised target price of $89/MWh for its now-canceled project, raised investor concerns.

- By 2025-2026, the focus moved from LCOE in isolation to the total cost of inaction. With AI data centers requiring 80 MW or more per facility, the opportunity cost of being unable to secure power from a congested grid far outweighed the premium on FOAK SMRs.

- The industry now views the high initial cost of SMRs (estimated at $6, 000-$10, 000 per k W for early units) as a solvable problem. The IEA projects costs could fall to $4, 500/k W in Europe by 2040 through factory production and learning effects, but this requires an initial pipeline of projects underwritten by customers like data centers.

- A remaining technological hurdle is the supply chain for High-Assay Low-Enriched Uranium (HALEU) fuel, required by many advanced reactor designs. While a bottleneck in 2024, the clear demand signal from the tech industry is accelerating investment and development of a commercial fuel supply.

Data 4 2026 Outlook, 5 EU SMR Project Signals to Watch

In the year ahead, the critical signal for the European market will be the first firm SMR Power Purchase Agreement signed by a continental colocation provider, which would validate the EU’s new policy framework and officially replicate the successful U.S. model.

- If this happens: The European Industrial Alliance on SMRs announces its first round of supported projects or “SMR Valleys” before year-end 2026. Watch this: The specific locations and SMR technologies chosen, as they will indicate the regions and developers with the strongest political and financial backing for near-term deployment.

- If this happens: A major European colocation provider like Data 4 or a hyperscaler announces a binding PPA with an SMR developer such as Rolls-Royce SMR, EDF, or newcleo. Watch this: The contract structure, specifically whether it involves direct equity investment in the SMR project, which would signal a deeper, more integrated partnership model.

- These could be happening: Watch for announcements of new European-based facilities for HALEU fuel production or enrichment. This would be a crucial step in de-risking the fuel supply chain for advanced reactors and reducing dependence on non-EU sources. Progress on this front is a leading indicator of the SMR market’s long-term viability.

The questions your competitors are already asking

This report covers one angle of data center operators securing private nuclear power. The questions that matter most depend on your work.

- What is the outlook for SMR deployment in the European data center sector by 2030?

- Which hyperscalers and energy providers are gaining ground in the U.S. and EU nuclear data center market?

- Amazon’s 1.92 GW PPA with Talen Energy. Is this the bankable model for financing SMR projects with private capital?

- Which colocation providers are following Data4’s lead in securing SMRs to overcome EU grid constraints?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.