SOFC Data Center Deals, 2.8 GW Oracle Offtake, $2.65 B AEP Pact, and PAFC’s Military Foothold (2025 to 2026)

Stationary Fuel Cell Adoption, Bloom Energy’s Data Center Focus, and PAFC’s Critical Role

In 2026, the stationary fuel cell market is segmenting based on application-specific risk tolerance, creating a dual-track adoption model. Advanced Solid Oxide Fuel Cells (SOFCs) are being rapidly deployed in power-intensive data centers where electrical efficiency is paramount. Concurrently, legacy Phosphoric Acid Fuel Cell (PAFC) technology maintains its vital role in ultra-conservative sectors like military and healthcare, where a long history of proven reliability outweighs the benefits of higher efficiency.

- From 2021 to 2024, stationary fuel cell adoption was characterized by broad, incremental growth across various commercial and industrial applications. The technology was primarily seen as a clean and reliable alternative to traditional backup power.

- The period from 2025 to today has been defined by an explosion in demand from the data center sector, driven by the energy requirements of Artificial Intelligence. This has catalyzed massive, targeted deployments of high-efficiency SOFCs, exemplified by Bloom Energy‘s multi-gigawatt agreements with major technology firms.

- While SOFCs capture the high-growth data center market, PAFC technology persists due to its unmatched operational history. For military bases and hospitals, the “cost of failure” is catastrophic, making PAFC the rational, low-risk choice for mission-critical power resilience. Companies like Doosan and historically Fuel Cell Energy have established this technology’s reputation for durability.

- This bifurcation demonstrates a market maturing beyond a one-size-fits-all approach. End-users are now making sophisticated procurement decisions based on a trade-off between peak performance (SOFC) and established, long-term operational certainty (PAFC).

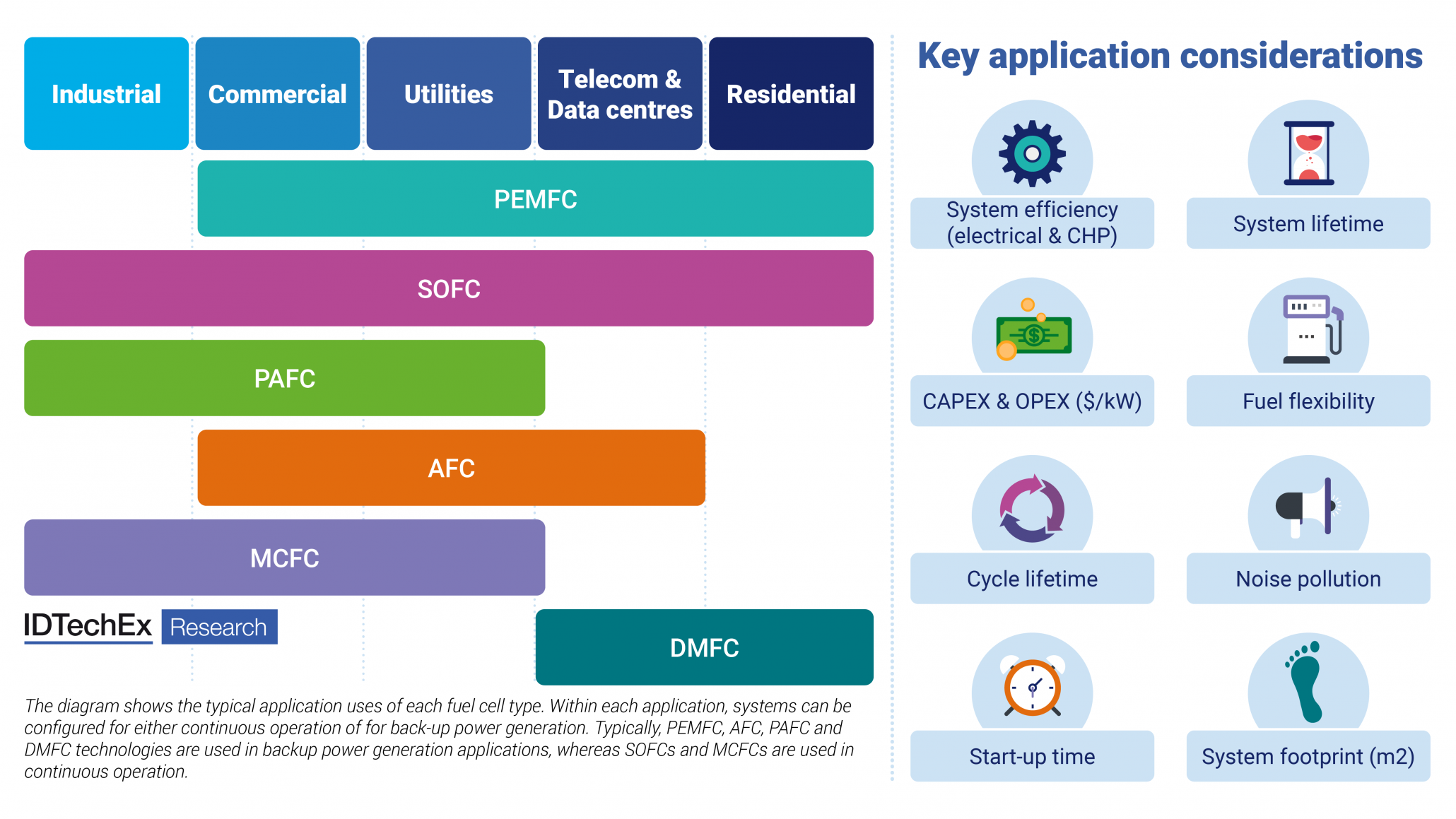

Mapping Fuel Cell Technologies to Applications

This chart illustrates the section’s main point about a dual-track market by mapping specific technologies like SOFC and PAFC to different applications such as data centers and backup power.

(Source: IDTechEx)

$2.65 B AEP Agreement, Bloom Energy’s SOFC Investment, and Market Forecasts

Capital investment in the stationary fuel cell market is heavily concentrated in SOFC technology, directly targeting the urgent power needs of the digital economy. The scale of recent financial commitments and market projections validates stationary fuel cells as a foundational component of modern critical infrastructure, with multiple analysts projecting the overall fuel cell market to exceed $50 billion by 2031.

Fuel Cell Market Forecast Exceeds $50B

This chart’s forecast of a $50.8 billion market in 2026 directly corroborates the section’s mention of analyst projections exceeding $50 billion, validating the market’s significant scale.

(Source: Transparency Market Research)

- A landmark $2.65 billion agreement between Bloom Energy and American Electric Power (AEP) to deploy up to 1 GW of SOFCs at data center sites signals deep financial confidence in the technology’s ability to provide continuous, utility-scale power.

- Market forecasts reflect this aggressive growth, with Technavio projecting the total fuel cell market to reach $59.51 billion by 2030, growing at a CAGR of 39.5%. The more specific SOFC segment is forecast by Verified Market Research to hit $12.5 billion by 2032.

- This investment surge is a direct response to grid instability and the inadequacy of traditional power sources to meet the demands of AI infrastructure. Fuel cells offer a scalable, on-site solution that enhances grid stability while meeting decarbonization goals.

Table: Stationary and Overall Fuel Cell Market Forecasts

| Forecast Provider | Market Segment | 2026 Forecast ($B) | 2030-2034 Forecast ($B) | CAGR (%) | Source |

|---|---|---|---|---|---|

| Technavio | Overall Fuel Cell | N/A | $59.51 (by 2030) | 39.5% | Technavio |

| Mordor Intelligence | Global Fuel Cell | $10.42 | $50.64 (by 2031) | 37.19% | Mordor Intelligence |

| Verified Market Research | Solid Oxide Fuel Cell (SOFC) | N/A | $12.5 (by 2032) | 21.1% | Verified Market Research |

| Fortune Business Insights | Stationary Fuel Cells | N/A | $5.97 (by 2034) | 13.94% | Fortune Business Insights |

Bloom Energy 2.8 GW Oracle Deal, and Other Critical Infrastructure Pacts (2026)

Strategic partnerships formed in 2026 are solidifying the market’s segmentation, with SOFC providers securing massive offtake agreements for data centers while other fuel cell technologies are chosen for specific resilience applications. These alliances are not just commercial transactions; they are long-term commitments that define the competitive positioning of different fuel cell technologies for the next decade.

Stationary Fuel Cell Market Growth Forecast

This chart from Fortune Business Insights provides the exact forecast value ($5.97B by 2034) that is cited in the section’s table, making it a perfect data visualization for the text.

(Source: Fortune Business Insights)

- The definitive partnership of 2026 is Bloom Energy‘s agreement to supply Oracle with 2.8 GW of its SOFC systems. This deal establishes SOFCs as the go-to solution for powering AI infrastructure at an unprecedented scale, providing reliable baseload power independent of the grid.

- In Europe, a strategic partnership between Centrica and Ceres aims to deploy multi-gigawatt SOFC systems for on-site, grid-independent power, future-proofing critical facilities across the UK and Europe and underscoring the technology’s growing international adoption.

- Illustrating the different focus of other technologies, India’s Defence Research and Development Organisation (DRDO) successfully developed a 270 kilowatt PAFC-based propulsion system for submarines. This application prioritizes absolute reliability and robustness over the raw electrical efficiency sought by data centers.

Table: Key Stationary Fuel Cell Partnerships and Deployments (2026)

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Bloom Energy / Oracle | April 2026 | Agreement for 2.8 GW of SOFC systems to power Oracle’s AI data centers, providing continuous baseload power. | Barchart |

| Centrica / Ceres | March 2026 | Strategic partnership to deploy multi-gigawatt on-site SOFC power generation to enhance grid independence for critical infrastructure in the UK and Europe. | Centrica |

| Fuel Cell Energy / SDCL | January 2026 | Collaboration to potentially deploy up to 450 MW of fuel cell systems for data centers and other decentralized applications globally. | Fuel Cell Energy |

| Bloom Energy / AEP | February 2026 | $2.65 billion agreement to deploy up to 1 GW of SOFC systems at data center sites, enhancing grid stability for digital infrastructure. | Climate Drift |

US vs. Global Adoption, Bloom Energy’s Focus on Data Center Power

While stationary fuel cell adoption is a global trend, North America, and particularly the United States, has become the undisputed epicenter for new, large-scale SOFC deployments in 2026. This is due to the concentration of power-hungry AI data centers and the urgent need for grid-independent energy solutions. Meanwhile, other regions like Europe and Asia are pursuing a more diversified strategy, integrating fuel cells for grid resilience and industrial CHP applications.

North America Dominates Stationary Fuel Cell Market

This chart’s headline and data, showing North America’s 46% market share, directly support the section’s central argument that the region is the ‘undisputed epicenter’ for adoption.

(Source: Grand View Research)

- The United States dominates new capacity additions, driven by landmark deals like Bloom Energy’s agreements with Oracle and AEP. This positions the US as the primary market for SOFCs aimed at digital infrastructure.

- In Europe, the focus is increasingly on grid resilience and industrial decarbonization. The partnership between Centrica and Ceres to provide on-site power across the UK exemplifies a strategy centered on fortifying existing infrastructure against grid vulnerabilities.

- Asian markets continue to show strong interest, particularly in South Korea and India. Hyundai‘s major investments in its home market and India’s development of PAFC systems for defense applications highlight a focus on energy security and specialized industrial use cases.

Technology Trade-Offs, SOFC Efficiency vs. PAFC’s Proven Durability

The bifurcation of the stationary fuel cell market is a direct consequence of the distinct maturity levels and technical trade-offs between SOFC and PAFC technologies. SOFCs lead on efficiency, making them ideal for new commercial builds with high energy costs, whereas PAFCs lead on proven, long-term reliability, making them the preferred choice for environments where failure is not an option.

SOFC Excels In Continuous Stationary Power

This chart details the high efficiency of SOFCs, which is the core technical advantage discussed in the section’s comparison of SOFC and PAFC technology trade-offs.

(Source: IDTechEx)

- Solid Oxide Fuel Cells (SOFC) represent the cutting edge, offering electrical efficiencies greater than 60% and superior fuel flexibility. Their primary challenge remains long-term material durability due to high operating temperatures (600-1000°C), a risk that large commercial customers are willing to accept for significant operational cost savings.

- Phosphoric Acid Fuel Cells (PAFC) are a mature, first-generation technology with a multi-decade track record of dependable performance. Though their electrical efficiency is lower (40-50%), their operational history is well-documented, making them a predictable and low-risk asset for critical infrastructure operators like military bases and hospitals.

- This dynamic is not about one technology being “better” but about fitness for purpose. For a data center, a 10% efficiency gain translates to millions in savings. For a hospital, a 20-year record of uninterrupted operation is more valuable than any potential opex reduction.

Stationary Fuel Cell SWOT, Market Position and Persistence of Different Technologies

The stationary fuel cell market in 2026 is defined by the strength of its resilient, low-emission power generation, creating immense opportunity in the data center sector. However, weaknesses related to upfront cost and the long-term durability of newer technologies persist, while the threat from alternative power sources remains a factor. This environment allows different fuel cell technologies to thrive by serving distinct market needs.

Fuel Cells Power Diverse Critical Sectors

As an introduction to a SWOT analysis, this diagram visually represents the key ‘Strengths’ and ‘Opportunities’ by showing the diverse, high-value applications for stationary fuel cells.

(Source: IDTechEx)

Table: SWOT Analysis for Stationary Fuel Cells (2026)

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | High reliability, low emissions, and potential for CHP applications were recognized. Adoption was steady but lacked a major catalyst. | Superior electrical efficiency (>60% for SOFC) and proven durability (PAFC) are now matched to specific high-value use cases. | The AI boom validated the need for SOFC’s efficiency at scale, while persistent grid failures reinforced the value of PAFC’s proven reliability for critical services. |

| Weaknesses | High capital expenditure (CAPEX) and questions about the long-term durability of newer technologies were significant barriers to widespread adoption. | CAPEX remains high, but the economic case is now justified for data centers. SOFC durability is still being proven at scale, while PAFC’s lower efficiency is a known trade-off. | The value proposition for high-CAPEX fuel cells was validated by the immense cost of downtime for data centers, shifting the economic calculation. |

| Opportunities | Decarbonization goals and the need for backup power presented growth opportunities, but without the urgency seen today. | The exponential power demand from AI data centers has created a massive, immediate market. Increasing grid instability is driving all critical infrastructure to seek on-site power. | The data center market crystalized from a general opportunity into the primary, multi-billion-dollar driver for new SOFC deployments in North America. |

| Threats | Competition from diesel generators and improving battery energy storage systems (BESS) were the primary threats. | BESS solutions are improving for short-duration backup, but cannot match fuel cells for continuous baseload power. Fuel price volatility (natural gas) remains a concern. | The market recognized that fuel cells and batteries serve different functions. Fuel cells are for continuous power and resilience, a role BESS cannot currently fill at scale. |

2026 Scenario, SOFC Data Trajectory vs. PAFC Incumbency

The most critical factor for the stationary fuel cell market ahead is the accumulation of operational data from the massive SOFC deployments currently underway. If these advanced systems demonstrate a level of reliability over the next three to five years that rivals PAFC’s established track record, SOFC technology will likely begin to penetrate even the most conservative critical infrastructure sectors, unifying the market under a single leading technology.

SOFC Dominates Stationary Power Fuel Cells

This chart, which highlights SOFCs as the largest market segment, visually reinforces the section’s forward-looking scenario about SOFC technology’s trajectory to unify the market.

(Source: Grand View Research)

- If this happens: Large-scale SOFC fleets at data centers and commercial sites consistently achieve “five nines” (99.999%) uptime and meet their projected 10-20 year operational lifespans without significant degradation.

- Watch this: The first public announcements of SOFC deployments at military installations, major hospitals, or other government facilities that have historically relied on PAFC or diesel generators. Also, monitor the renewal terms of the first large SOFC service agreements signed in this period.

- These could be happening: PAFC providers may pivot to focus exclusively on highly specialized niches, such as naval applications or high-utilization Combined Heat and Power (CHP) industrial sites where their thermal output provides a distinct economic advantage.

The questions your competitors are already asking

This report covers one angle of the stationary fuel cell market’s segmentation based on risk and application. The questions that matter most depend on your work.

- How does PAFC compare to SOFC for mission-critical power resilience in hospitals and military bases?

- What is the outlook for SOFC deployment in AI data centers versus PAFC deployment in critical infrastructure?

- Which fuel cell companies, like Bloom Energy and Doosan, are gaining or losing ground in their respective target markets?

- Which hospital networks and military operators are adopting PAFC technology for power resilience?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.