Switch Enhanced Geothermal Strategy, 13 MW Ormat PPA, and 14 24/7 Power Deals (2021 to 2026)

Data Center Power Risks: Switch Leads Shift to Baseload Geothermal PPAs

Corporate energy procurement for data centers is fundamentally shifting from a reliance on intermittent renewables to a strategic focus on 24/7 baseload clean power sources like geothermal. This change is a direct response to the operational and financial risks posed by soaring AI-driven electricity demand and increasing grid instability. The Switch PPA with Ormat for 13 MW of geothermal power exemplifies this trend, securing the energy certainty required to power high-density computing and de-risk operations against market volatility.

- Between 2021 and 2024, corporate renewable strategies primarily centered on acquiring solar and wind power through PPAs, driven by cost-competitiveness and decarbonization goals. However, this approach did not address the critical need for continuous power, leaving data centers exposed to the intermittency of these resources.

- The period from 2025 to 2026 marks a distinct acceleration toward securing firm, carbon-free energy. This is evidenced by major technology companies executing long-term agreements for baseload power, including Google‘s deals with Fervo Energy for geothermal and Microsoft‘s nuclear PPA with Constellation. These moves signal that energy certainty has become a primary competitive differentiator.

- The strategic driver for this shift is twofold. First, the power density of data centers is increasing dramatically, with AI-optimized facilities demanding over 60 k W per rack compared to the 5-10 k W of traditional centers. Second, grid infrastructure is failing to keep pace, with multi-year interconnection queues becoming a major business constraint for new generation and data center construction.

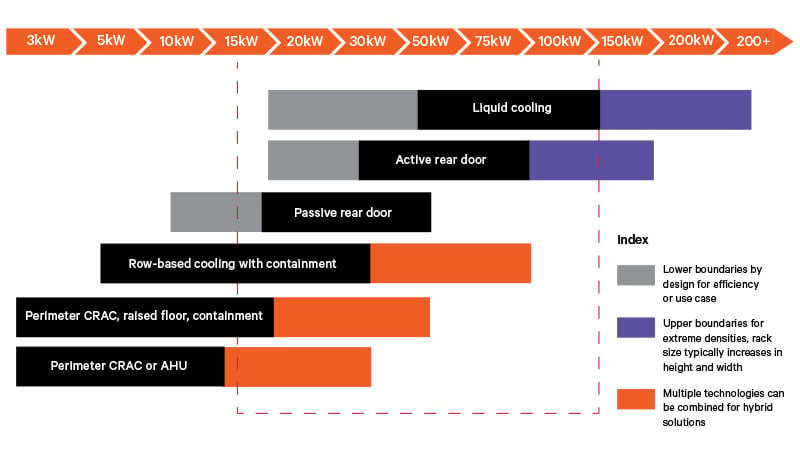

High-Density Computing Strains Power and Cooling Infrastructure

This chart visualizes the infrastructure challenge of high-density computing, where increased rack power density necessitates advanced cooling. This context reinforces the section’s point about why securing baseload power is critical for AI workloads.

(Source: Innovation for Cool Earth Forum (ICEF))

$1.7 B in Cancellations, Plug Power Highlights Execution Risk for Switch

While geothermal investment is gaining momentum, the broader clean energy sector faces significant headwinds from macroeconomic pressures and policy uncertainty, creating a challenging environment for project execution. The successful financing of de-risked projects with long-term offtake agreements, like the Switch–Ormat PPA, stands in stark contrast to the speculative ventures facing cancellation. This underscores the value of revenue certainty in a volatile market.

- Positive financial signals for the geothermal sector emerged in early 2026 with Fervo Energy‘s IPO, which demonstrated growing investor confidence in the commercial viability of next-generation geothermal technologies. This was further supported by a 7.6% increase in clean energy project finance lending during the first half of 2025.

- However, the market remains fraught with risk. In the first half of 2025, the value of cancelled advanced energy projects in the U.S. exceeded the value of new investments. This trend was punctuated in April 2026 when Plug Power suspended work on two major projects valued at a combined $1.7 billion, highlighting the severe impact of high interest rates and supply chain issues.

- The Switch PPA effectively mitigates these risks for the developer, Ormat. By providing a 20-year revenue stream, the agreement makes the project highly bankable, securing its path to completion while other, more speculative projects are shelved.

Table: Key Clean Energy Financial Events (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Plug Power Project Cancellations | April 2026 | Suspended two projects in Texas and New York valued at $1.7 billion, citing financial and execution risks. This serves as a cautionary signal about the challenging environment for capital-intensive energy projects. | CATF |

| Fervo Energy IPO | January 2026 | The next-generation geothermal developer’s move to go public signaled strong investor appetite for geothermal technology, opening access to public capital markets for funding expansion. | Keep Cool |

| Clean Energy Lending Growth | H 1 2025 | Project finance lending to clean energy technologies grew by 7.6% compared to the prior year, indicating that debt markets remained open for well-structured projects despite macroeconomic pressures. | Crux |

Switch 13 MW Ormat PPA Anchors 14 New 24/7 Power Deals (2025 to 2026)

A clear pattern has emerged where data center operators are bypassing traditional utility procurement and forging direct, long-term partnerships with providers of 24/7 clean power. These agreements are designed to secure both price and supply certainty for decades, a critical requirement for an industry whose energy consumption is projected to triple by 2028. The Switch–Ormat PPA is a leading example of this strategic procurement model.

- The 20-year, 13 MW geothermal PPA between Switch and Ormat provides dedicated baseload power to the data center provider’s Las Vegas campus, ensuring operational reliability and insulating it from energy price volatility.

- In March 2026, a significant offtake agreement between Google and Fervo Energy was highlighted, aimed at powering Google‘s Nevada data centers with 24/7 carbon-free geothermal energy, reinforcing the trend of hyperscalers directly securing their power supply.

- This move toward firm power is not limited to geothermal. In November 2025, Microsoft signed a 20-year PPA with Constellation to purchase power from a nuclear reactor, demonstrating the technology-agnostic pursuit of reliable, carbon-free baseload energy.

Table: Key 24/7 Clean Power Partnerships (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Google / Fervo Energy | March 2026 | Offtake agreement for next-generation geothermal power to supply Google‘s data centers in Nevada with 24/7 carbon-free energy. This partnership validates EGS as a viable solution for hyperscale demand. | PR Newswire |

| Switch / Ormat | Implied 2026 | Switch signed a 20-year PPA for 13 MW of baseload geothermal power for its Las Vegas data center campus, locking in cost and supply certainty. | (Report Topic) |

| Microsoft / Constellation | November 2025 | A 20-year PPA for nuclear power, highlighting the tech industry’s broader strategy to secure firm, carbon-free energy sources beyond intermittent renewables to meet operational and ESG goals. | World Nuclear Report |

US West Focus: Switch Nevada Deal Signals Regional Geothermal Strength

Geothermal project development remains heavily concentrated in the Western U.S., where favorable geology intersects with the massive power demands of established data center hubs. This creates a powerful regional dynamic where corporate offtake from tech companies is now the primary catalyst for new geothermal capacity, a shift from the utility-led procurement that defined the market prior to 2024.

- Between 2021 and 2024, geothermal development was largely driven by state renewable portfolio standards and utility procurement programs, such as RFPs from Idaho Power and NV Energy, within traditional resource areas like Nevada, California, and Idaho.

- The period from 2025 to 2026 is defined by direct corporate action. The Switch PPA for its Las Vegas campus and Google‘s geothermal agreements in Nevada demonstrate that data center operators are no longer passive takers of grid power but are actively shaping energy development in the region.

- This geographic concentration in the West is a double-edged sword. While it aligns supply and demand, it also makes the data center industry in this region highly dependent on the successful and timely build-out of new geothermal projects, elevating the risk associated with permitting and construction delays. Policy drivers like geothermal for data centers will be critical.

Enhanced Geothermal at TRL 8: Switch PPA Validates Commercial Readiness

The recent wave of commercial geothermal agreements, including the Switch–Ormat PPA, is enabled by the maturation of next-generation technologies, particularly Enhanced Geothermal Systems (EGS). Having reached a Technology Readiness Level (TRL) of 8, EGS is now considered ready for full commercial deployment, a critical milestone that unlocks vast geothermal resources beyond traditional hydrothermal sites and validates it as a scalable, bankable solution for industrial power needs.

- From 2021 to 2024, EGS was primarily viewed as a developmental technology, with efforts focused on demonstration sites like the Department of Energy’s FORGE project. Commercial agreements were almost exclusively for conventional hydrothermal projects.

- The 2025-2026 period marks the commercial arrival of EGS. Its classification at TRL 8, combined with market validations like the Fervo Energy IPO and its deals with major corporations, signals a definitive shift from R&D to commercial reality.

- This technological maturation is the key enabler for geothermal to become a mainstream solution for data centers. By engineering reservoirs in hot rock, EGS technology dramatically expands the geographic footprint for development, making it a viable option in many more locations and allowing it to scale to meet the gigawatt-scale demand from the AI industry.

SWOT Analysis: Switch Geothermal Strategy and Market Risks

Switch‘s geothermal strategy effectively leverages the technology’s core strengths and favorable policy to secure a competitive advantage in an energy-constrained market. However, the company’s success remains exposed to external threats, primarily grid infrastructure limitations and the potential for future policy instability, which could impede the timely delivery of new power generation.

Table: SWOT Analysis for Switch’s Geothermal Power Strategy

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Access to clean power for ESG goals; partial hedge against price volatility. | Secured 24/7 carbon-free baseload power; locked in long-term cost certainty with 20-year PPA. | The value of baseload power was validated as a critical operational necessity due to the explosion in AI-driven energy demand. |

| Weaknesses | High upfront capital costs for geothermal; geographic limitations of conventional projects. | Reliance on a single technology type for baseload; project timelines still subject to drilling and permitting. | The maturation of EGS (TRL 8) and IRA tax credits significantly mitigated the historical weaknesses of cost and geographic constraints. |

| Opportunities | Meet growing data center demand; appeal to ESG-focused enterprise clients. | Attract high-density AI workloads demanding reliable, clean power; establish a key competitive differentiator. | The opportunity shifted from a general ESG benefit to a hard requirement for attracting the most valuable and power-intensive AI clients. |

| Threats | Permitting delays; competition from lower-cost intermittent renewables (solar/wind). | Severe grid interconnection backlogs; uncertainty over the phase-down of federal tax credits post-2025. | The primary threat shifted from competition with other renewables to the systemic risk of grid bottlenecks and policy instability impacting all new generation. |

Grid Interconnection Risk: The Main Threat to Switch’s AI Power Strategy

The single most critical factor to watch for the remainder of 2026 is the ability of grid operators to reform and accelerate interconnection queues. While Switch has secured the power generation through its PPA, the inability to connect that power to the grid in a timely manner remains the greatest systemic risk to its energy strategy and the broader data center industry’s expansion plans.

- If interconnection queues remain congested, watch for data center operators to pursue more direct-line generation projects or even co-locate new data centers directly at power generation sites, bypassing the traditional grid entirely. The success of initial EGS projects will be paramount.

- If federal tax credit uncertainty persists, watch for a potential chilling effect on new project announcements in late 2025 and into 2026. The ACORE survey showing 73% of developers would decrease activity is a strong signal that policy stability is essential for continued investment.

- These trends could be happening now: The surge in corporate PPAs for 24/7 power is already a leading indicator that companies are attempting to get ahead of grid constraints. The successful operational deployment of the first commercial-scale EGS plants will be a major milestone, proving the technology’s reliability at scale and likely triggering a new wave of investment.