Alkaline Electrolysis Manufacturing in China, 60% Global Capacity, 4-6 x Lower Costs, and Price Parity Projections (2021 to 2026)

China’s industrial-scale manufacturing of alkaline electrolyzers has fundamentally altered the global green hydrogen cost curve, creating a two-tiered market where project viability depends on access to its low-cost supply chain. While this has accelerated progress, it has not universally closed the levelized cost of hydrogen (LCOH) gap with blue hydrogen by 2026. Blue hydrogen maintains a cost advantage in regions with low-cost natural gas, but the rapid, policy-driven expansion in China has solidified a trajectory where green hydrogen is set to achieve broad cost parity before 2030, creating significant stranded asset risk for new fossil-based hydrogen investments.

Green Hydrogen Project Viability, China Electrolyzer Costs Create a Two-Tier Market

The aggressive scaling of Chinese electrolyzer production has bifurcated the global market, creating pockets of cost-competitive green hydrogen while blue hydrogen remains the more economic choice elsewhere. This dynamic reshapes investment calculus, tying project feasibility directly to supply chain origin.

- In the 2021-2024 period, most green hydrogen projects were small-scale pilots struggling with high electrolyzer CAPEX, which positioned blue hydrogen as the more viable near-term option for industrial decarbonization.

- From 2025 to today, a massive expansion in Chinese manufacturing has resulted in control of 60% of global electrolyzer capacity, driving prices for its alkaline systems down to be 4-6 times lower than Western alternatives.

- This cost advantage is creating regional successes, with integrated green hydrogen projects in northwestern China, a region with high renewable penetration, now approaching cost parity with fossil-based grey hydrogen.

- Globally, however, the green hydrogen LCOH remains in a wide range of $5.00-$10.00/kg. Projects with access to the Chinese supply chain can realistically target the lower end of this spectrum, between $3.70-$5.20/kg, giving them a distinct competitive advantage.

- This market fracture places significant pressure on Western electrolyzer manufacturers like Siemens Energy and Cummins, who focus on higher-performance but more expensive PEM technology, creating a risk of competitive displacement similar to what occurred in the solar panel industry.

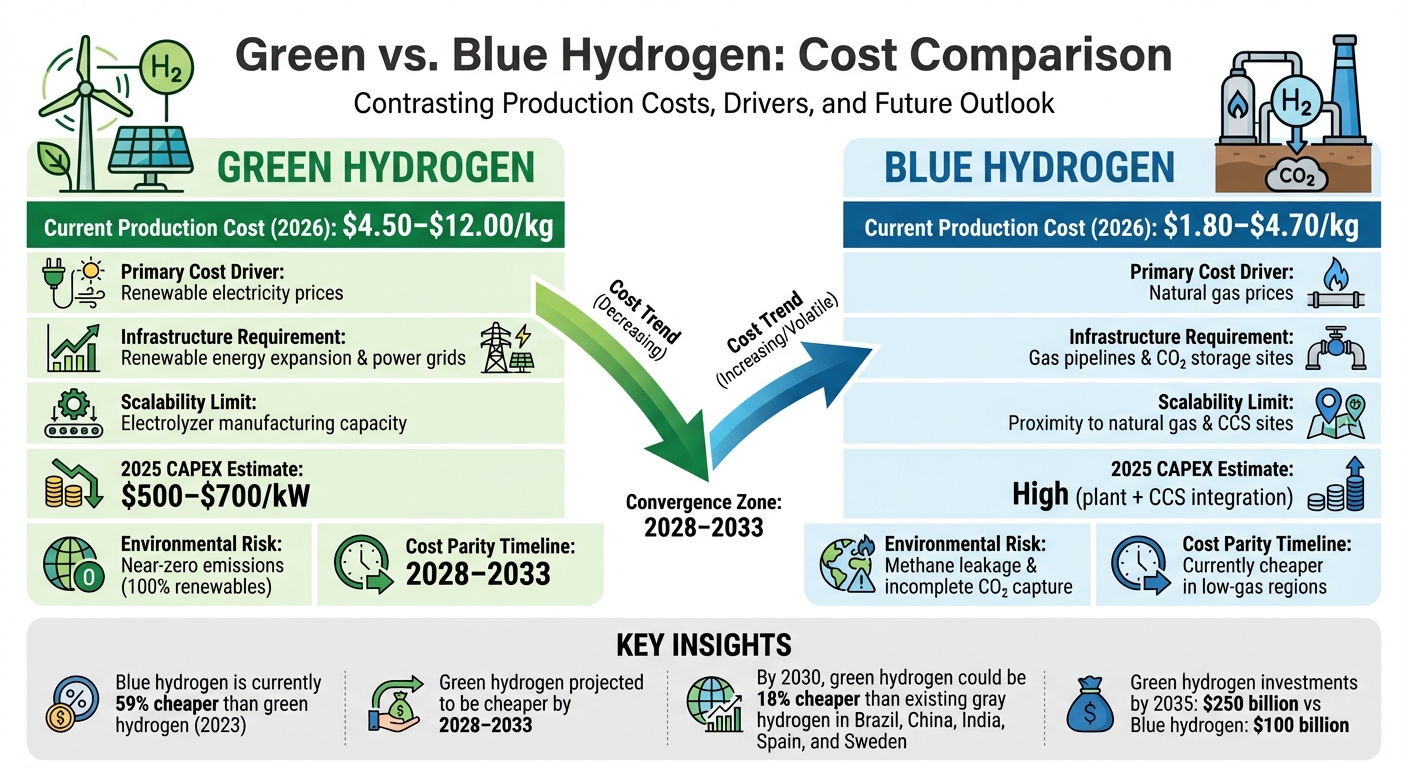

Blue Hydrogen Cheaper Now, Green to Win Soon

This chart illustrates why blue hydrogen was the more viable near-term option, as mentioned in the text, by showing its current cost advantage over green hydrogen.

(Source: Electrical Trader)

China Hydrogen Market, $47 M Forvia Deal & 1.5 GW Project Investment (2025 to 2026)

Capital allocation from both state and corporate entities is cementing China’s role as the central hub for hydrogen technology manufacturing and deployment. This investment is not just in production capacity but also in creating demand through large-scale application projects.

- Globally, government support for the sector is strong, with an estimated $222 billion allocated for the development of both blue and green hydrogen projects, creating a favorable investment climate.

- China has formally elevated hydrogen to a national strategic priority within its 15 th Five-Year Plan (2026-2030), ensuring sustained policy support and financial incentives to build out the entire value chain.

- A landmark project announced in January 2026 is a 1.5 GW offshore wind-to-hydrogen facility, a commercial-scale plant designed to produce 80, 000 tons of green hydrogen annually.

- Corporate confidence in the Chinese market is evident from Forvia’s €40 million ($47 million) capital increase for its Chinese hydrogen subsidiary, a deal that includes strategic investment from the state-owned energy giant Sinopec.

Table: Strategic Hydrogen Investments (2026)

| Investor / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Forvia / Sinopec | Jan 2026 | Forvia secured a €40 million ($47 million) investment from investors including Sinopec for its Chinese hydrogen subsidiary, signaling strong commercial interest in China’s hydrogen mobility and storage market. | Gasworld |

| Offshore Wind-to-Hydrogen Project | Jan 2026 | China unveiled plans for a 1.5 GW offshore wind farm integrated with a green hydrogen production facility capable of producing 80, 000 tons per year, demonstrating a commitment to industrial-scale deployment. | Enerdata |

| Global Governments | Jan 2026 | An estimated $222 billion has been allocated globally by governments for blue and green hydrogen projects, indicating widespread policy support to de-risk investments and stimulate market growth. | ING THINK |

Global Partnerships, China Electrolyzer Dominance Drives International MOUs

The compelling economics of Chinese electrolyzers are catalyzing international cooperation, enabling countries to accelerate their national hydrogen strategies by leveraging China’s established manufacturing prowess and supply chain.

- In April 2026, Egypt’s government signed an Mo U with China’s UEG to develop a large-scale green hydrogen project in the Mediterranean, a clear signal of international willingness to adopt Chinese technology for major energy projects.

- The Namibian government announced in March 2026 that it is actively pursuing Chinese R&D partnerships to build out its domestic capabilities and support its ambitious green hydrogen and ammonia export plans.

- A tripartite partnership formed in Hong Kong in February 2026 between Towngas, Sinopec, and Sinopec Star Company aims to collaborate on hydrogen supply, refueling stations, and green methanol production, creating a vertically integrated ecosystem.

- These agreements highlight a pragmatic global trend: nations are prioritizing cost and speed of deployment, making partnerships with Chinese firms an attractive strategy to achieve their decarbonization goals.

Table: Key Hydrogen Partnerships (2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Egypt & China’s UEG | Apr 2026 | Mo U signed to develop a green hydrogen hub in the Mediterranean, leveraging Chinese technology and investment to build a large-scale production facility for domestic use and export. | Fuel Cells Works |

| Namibia & Chinese Firms | Mar 2026 | Namibian government is actively seeking R&D partnerships with Chinese entities to support its green hydrogen and ammonia ambitions, aiming to import technical expertise and manufacturing capability. | Namibia Economist |

| Towngas, Sinopec, Sinopec Star | Feb 2026 | A tripartite partnership in Hong Kong was established to collaborate on hydrogen production, storage, transportation, and utilization, as well as green methanol projects. | Offshore Energy |

60% Global Capacity, China Hydrogen Market Geographic Concentration

By 2026, China has established itself as the dominant geographic hub for electrolyzer manufacturing, leveraging this concentration to create regional cost advantages that are beginning to influence global energy trade dynamics.

Chinese Electrolyzer Prices Hit 2030 Targets Early

This chart provides a concrete example of China’s market dominance, showing its 2026 prices have already hit 2030 targets, which reflects the geographic manufacturing concentration described.

(Source: LinkedIn)

- Between 2021 and 2024, electrolyzer manufacturing was a more distributed industry, with European and North American firms holding significant capacity and a technological lead in PEM systems.

- The period from 2025 to today has been defined by China’s consolidation of the market. It now controls an estimated 60% of global manufacturing capacity, with a strategic focus on low-cost, mass-produced alkaline electrolyzers.

- This manufacturing might is geographically concentrated within China itself. Regions like Inner Mongolia and Ningxia in the northwest, rich in solar and wind resources, are becoming hotspots for green hydrogen production, with costs that are competitive with local grey hydrogen.

- This concentration poses a significant supply chain dependency risk for the rest of the world. Europe, in particular, now faces a strategic dilemma: either rely on low-cost Chinese imports to meet its hydrogen targets or risk falling behind by supporting a more expensive domestic industry.

Alkaline Electrolysis Commercial Scale, China’s Low-Cost Tech Outpaces PEM

China has successfully industrialized Alkaline Water Electrolysis (AWE), establishing it as the most mature and cost-effective technology for large-scale green hydrogen production in 2026. This focus on a proven technology has allowed it to outpace Western firms that have concentrated on more advanced but less scalable PEM and SOEC systems.

Alkaline Tech Dominates, PEM Electrolysis Grows Fast

This chart directly supports the section’s theme by showing Alkaline electrolysis holding the largest market share, which aligns with China’s successful industrialization of the technology.

(Source: MarketsandMarkets)

- In the 2021-2024 period, Western firms like ITM Power and Sunfire were advancing higher-efficiency PEM and SOEC technologies, which were seen as the future of the industry.

- From 2025 to today, China’s strategic decision to mass-produce mature AWE technology has paid off, allowing it to achieve economies of scale that have driven down CAPEX to levels unattainable by competitors. Chinese alkaline electrolyzers now cost 4-6 times less than European PEM systems.

- While PEM and SOEC electrolysis offer technical advantages like faster response times and higher efficiency, their production costs remain a significant barrier. A 10 MW system using PEM technology can result in an LCOH of $13.07/kg, compared to a projected $7.86/kg for a SOEC system, both significantly higher than targets achieved with low-cost AWE.

- The market in 2026 is defined by this technological divergence. China’s AWE technology is commercially ready for mass deployment today, while more advanced technologies remain on a developmental path, still working to reduce costs and scale up manufacturing.

Post-2026 Projections, China Electrolyzer Costs and Global Market Scenarios

If Chinese manufacturers sustain their current momentum on cost reduction and capacity expansion, the primary strategic risk is a fragmentation of the global hydrogen market. This would result in a dominant low-cost segment supplied by Chinese technology and a smaller, high-performance niche served by Western producers.

China’s Cost Advantage Projected to Widen

This chart’s long-term forecast, showing China’s sustained cost advantage over other regions, provides the visual basis for the section’s projection of a fragmented global market.

(Source: Deep (Tech) Takes – Substack)

- If Western governments respond with tariffs or subsidies to protect domestic industries from low-cost Chinese imports, watch for the emergence of regional hydrogen trading blocs with different technology standards and pricing structures. This could lead to a slowdown in overall global cost reduction by restricting access to the most affordable technology.

- If the performance, efficiency, and durability of Chinese electrolyzers improve to match Western standards while maintaining their significant cost advantage, watch for an accelerated wave of cancellations for blue hydrogen projects, including those in advanced planning stages. The business case for blue hydrogen as a “bridge fuel, ” such as the major project canceled by Air Products involving technology from Topsoe, would be severely undermined.

- If these conditions are met, this could lead to the LCOH gap closing universally before 2030, a much faster timeline than most current industry forecasts predict. This would trigger a rapid and decisive shift in capital away from all fossil-based hydrogen production.

The questions your competitors are already asking

This report covers one angle of the green hydrogen cost curve and its race to parity with blue hydrogen. The questions that matter most depend on your work.

- How does green hydrogen produced with Chinese alkaline electrolyzers compare to blue hydrogen on a levelized cost basis by 2026?

- What is the stranded asset risk for new blue hydrogen projects, given the outlook for green hydrogen cost parity before 2030?

- How does access to China’s low-cost alkaline electrolyzer supply chain create a two-tiered market for project feasibility?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.