Kawasaki Heavy Industries’ Liquid Hydrogen Supply Chain, $20 B Japan Cf D, Iwatani Partnership, and 1 HESC Withdrawal (2024 to 2026)

Kawasaki Heavy Industries’ HESC Withdrawal, 1 Failed Project, and Pivot to Canada (2024 to 2026)

The strategic blueprint for a trans-Pacific liquid hydrogen (LH 2) supply chain is shifting from technical validation to a rigorous test of economic viability, a change defined by Kawasaki Heavy Industries’ (KHI) activities. While the successful 2022 pilot shipment from Australia to Japan proved the cryogenic transport technology, KHI’s withdrawal from the commercial phase of the Hydrogen Energy Supply Chain (HESC) project in December 2024 exposed the primary market risk: an unstable and non-competitive upstream hydrogen supply. This forces a strategic pivot to new geographies like Canada, where the focus is now squarely on securing cost-effective production at scale before committing to transport infrastructure.

- Between 2021 and 2024, the industry focus was on demonstrating the technical feasibility of the LH 2 carrier, the Suiso Frontier. This was achieved with the HESC pilot, which successfully transported a small volume of liquid hydrogen from Australia to Japan, validating KHI’s cryogenic technology.

- Starting in late 2024, the market dynamic changed. Kawasaki Heavy Industries withdrew from the HESC commercial phase, citing delays in securing a cost-competitive hydrogen feedstock. This event signaled that transport technology is ahead of production economics.

- From 2025 onward, the strategy has pivoted toward Canada, a region with a national target to produce 4 million tonnes of low-carbon hydrogen annually by 2030. This move represents an attempt to resolve the feedstock problem that stalled the Australian project.

- The market is now bifurcating. While KHI continues to advance specialized LH 2 technology, parallel projects are gaining traction using more mature carriers. For example, the December 2025 partnership between Tokyo Gas and Teralta to produce e-methane in Canada for export to Japan leverages existing LNG infrastructure, bypassing LH 2’s complexities.

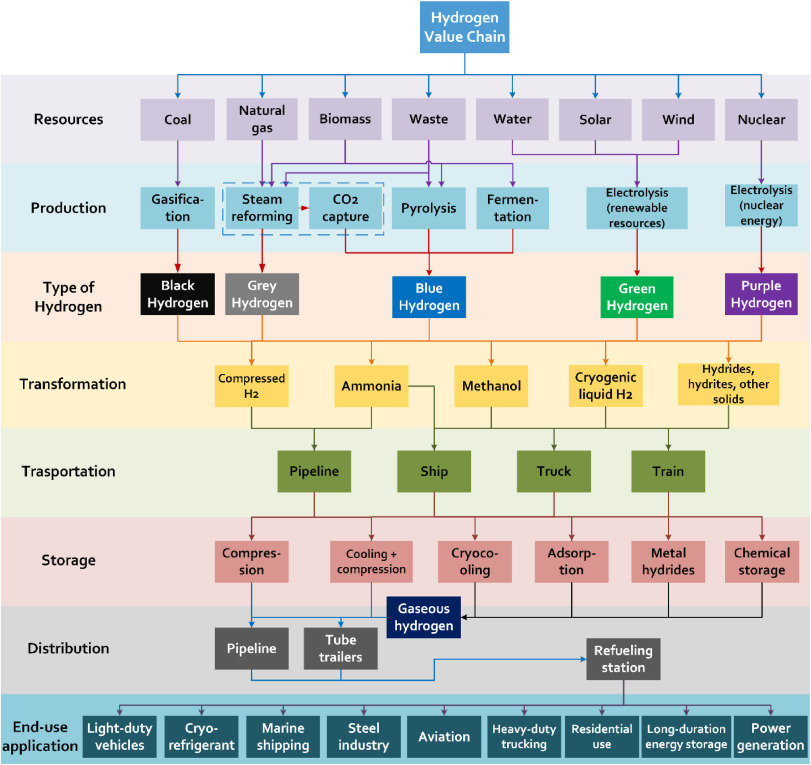

Visualizing the Liquid Hydrogen Value Chain

This flowchart shows the complete hydrogen value chain, including the cryogenic liquid hydrogen shipping technology that Kawasaki Heavy Industries successfully proved in its pilot project.

(Source: ScienceDirect.com)

$20 B in Subsidies, Kawasaki Heavy Industries’ Liquid Hydrogen Cost Hurdles

The commercial viability of a Canada-Japan liquid hydrogen route is entirely dependent on closing a significant cost gap through massive government subsidies and technology-driven cost reductions. The standalone economics are currently unworkable, as the high costs of production, liquefaction, and cryogenic shipping make LH 2 uncompetitive against both incumbent fuels and alternative low-carbon carriers. Japan’s aggressive subsidy programs are a direct response to this reality, designed to de-risk a market that cannot yet stand on its own.

Canada-Japan Hydrogen Export Cost Breakdown

This chart details the significant costs of the proposed Canada-to-Japan liquid hydrogen route, quantifying the contribution of each step from production to delivery.

(Source: ScienceDirect.com)

- The cost of green hydrogen production in Canada stands at $4-6/kg, while grey hydrogen costs only $1-2/kg. This upstream cost is the first major economic hurdle.

- Liquefaction, the process of cooling hydrogen to -253°C, is highly energy-intensive, consuming up to 30% of the hydrogen’s energy content and adding significant operational expense.

- The cost of transport via specialized LH 2 carriers adds an estimated $6-8/kg. This shipping cost alone is more than triple the production cost of grey hydrogen, making the final delivered price prohibitively high without support.

- To address this, Japan launched a $20 billion Contracts for Difference (Cf D) subsidy model in late 2024. The first international auction in January 2026 awarded US$6.8 billion, demonstrating the scale of government intervention required to make projects bankable.

Table: Hydrogen Cost and CAPEX Breakdown (2025-2026)

| Technology / Cost Component | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Green Hydrogen Production | 2026 | The production cost of $4.00 – $6.00/kg via electrolysis is the primary input cost and a major barrier to competitiveness compared to fossil-based production. | Mining and Energy |

| Liquid Hydrogen Shipping | 2026 | Transportation adds another $6.00 – $8.00/kg, making it one of the most significant costs in the entire value chain and a key focus for KHI’s efficiency improvements. | Science Direct |

| Ammonia Shipping (as a carrier) | 2025 | At a cost of $4.77/kg (hydrogen equivalent), ammonia shipping presents a more economically viable near-term alternative to LH 2 transport, leveraging existing infrastructure. | Science Direct |

| Grey Hydrogen Production | 2026 | With production costs of $1.00 – $2.00/kg, grey hydrogen remains the economic benchmark that low-carbon hydrogen must compete against. | Mining and Energy |

Canada vs. Australia, Kawasaki Heavy Industries’ Strategic Alliances and Project Pivots

Kawasaki Heavy Industries’ partnership strategy reveals a pragmatic adaptation to market realities, maintaining its long-term vision for liquid hydrogen while engaging with more immediate, economically viable energy vectors. The core consortium, Hy STRA, remains focused on the end-to-end LH 2 supply chain, but recent collaborations by its partners in alternative carriers like e-methane indicate a diversification of risk and a multi-pathway approach to decarbonizing Japan’s energy supply.

Mapping the Global Hydrogen Alliance Ecosystem

This diagram illustrates the ecosystem of industry bodies in key regions like Australia and Japan, contextualizing Kawasaki Heavy Industries’ strategic partnerships and pivots.

(Source: Hydrogen Portal)

- The Hydrogen Energy Supply-chain Technology Research Association (Hy STRA), a consortium including KHI, Iwatani Corporation, J-POWER, and Shell Japan, was foundational to the Australian pilot. Its purpose was to develop and integrate the technologies for an international LH 2 supply chain.

- Following the withdrawal from the HESC commercial phase in December 2024, the geographic focus for new LH 2 supply has shifted to Canada, where KHI and its partners aim to leverage more favorable green hydrogen production economics.

- A key development showing market diversification is the December 2025 agreement between Tokyo Gas (a major Japanese utility) and Canadian firm Teralta. They are developing an e-methane project, which converts green hydrogen into synthetic natural gas for transport using existing LNG tankers and terminals.

- This parallel activity demonstrates that while KHI provides the specialized technology for a future LH 2 route, key offtakers and partners are not solely reliant on its success. They are actively securing alternative low-carbon energy imports that can use existing infrastructure, presenting both a competitive threat and a complementary pathway.

Table: Kawasaki Heavy Industries Key Partnerships

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Asian Industry Players | Dec 2025 | KHI is collaborating with other industrial firms to advance technologies for commercial-scale LH 2 terminals and e-methane production, building out the regional infrastructure. | IEEJ |

| Iwatani Corporation | Sep 2025 | This partnership focuses on deploying Japan’s domestic liquid hydrogen distribution network, which is critical for last-mile delivery and offtake from KHI’s import terminals. | Iwatani Corporation |

| Hy STRA Consortium | Dec 2024 | A technology research association with Iwatani, J-POWER, Shell Japan, and Marubeni to establish the complete LH 2 supply chain. This group executed the initial Australia-Japan pilot. | Kawasaki Heavy Industries |

Technology Readiness, Kawasaki Heavy Industries’ TRL 9 Challenge, and Carrier Competition

While Kawasaki Heavy Industries has driven its core liquid hydrogen transport technologies to a high level of maturity, the overall supply chain remains less ready for commercial scale than competing hydrogen carriers like ammonia. The primary challenge is not the ship itself but the surrounding infrastructure and the significant energy losses inherent in the cryogenic pathway. Alternative carriers, which can leverage existing global infrastructure for chemicals and LPG, present a more technologically mature and economically attractive solution in the near-to-medium term.

Comparing Liquid Hydrogen and Ammonia Pathways

This diagram visually contrasts the supply chain pathways for liquid hydrogen (LH2) and ammonia (NH3), highlighting the carrier competition central to KHI’s technological challenge.

(Source: ScienceDirect.com)

- From 2021 to 2024, KHI focused on maturing its proprietary technologies, successfully validating the LH 2 carrier and the Kobe receiving terminal (Hy touch Kobe) through the HESC pilot project. This brought key transport components to a high Technology Readiness Level (TRL).

- Post-2025, the market is comparing the full “well-to-wake” readiness of different carriers. While LH 2 provides high-purity hydrogen on delivery, its low TRL for certain components (like large composite cryotanks) and high liquefaction energy penalty are significant disadvantages.

- Ammonia (NH 3) has a TRL of 9 for transport and storage, using existing, mature LPG infrastructure. DNV forecasts that seaborne ammonia trade will dominate intercontinental hydrogen transport, reaching ~65 Mt/yr by 2060.

- Liquid Organic Hydrogen Carriers (LOHCs), such as Dibenzyltoluene (DBT), also have a high TRL of 9. They can be transported at ambient temperatures in conventional oil tankers, eliminating boil-off losses and the need for specialized cryogenic infrastructure.

SWOT Analysis: Kawasaki Heavy Industries’ Liquid Hydrogen Supply Chain Risks and Opportunities

The establishment of a Canada-Japan LH 2 route is defined by a central tension: Kawasaki Heavy Industries’ undeniable technological leadership versus severe market-level economic and logistical headwinds. The evolution from a successful technical pilot to a cancelled commercial project in Australia has clarified the key risks and opportunities that will determine the fate of the Canadian venture.

Table: SWOT Analysis for the Canada-Japan LH 2 Route

| SWOT Category | 2021 – 2024 | 2025 – Today | What Changed / Validated |

|---|---|---|---|

| Strengths | Demonstrated world-first technology with the Suiso Frontier pilot, proving LH 2 marine transport is technically feasible. | Holds validated intellectual property for LH 2 carriers, cryogenic storage, and liquefaction, positioning KHI as a key enabler for any future LH 2 trade. | The technology was validated, shifting KHI’s strength from R&D leadership to being a provider of commercially-ready (though expensive) hardware. |

| Weaknesses | High estimated costs for liquefaction and shipping. Uncertainty around boil-off losses on commercial-scale voyages. | Exorbitant end-to-end cost ($6-8/kg for transport alone) makes LH 2 uncompetitive. High energy intensity of liquefaction (~30% loss). | The HESC project’s cancellation validated that the cost structure is currently unworkable at commercial scale without massive subsidies, confirming the primary weakness. |

| Opportunities | Japan’s strong political will for hydrogen to achieve energy security and decarbonization goals. | Japan’s $20 billion Cf D subsidy program and Canada’s aggressive hydrogen production targets create a powerful, policy-driven market pull and supply push. | The opportunity moved from a conceptual policy goal to a tangible, funded market with Japan’s Cf D auction in Jan 2026 providing a concrete incentive structure. |

| Threats | Competition from other hydrogen carriers like ammonia and LOHCs was theoretical. | Alternative carriers (ammonia, e-methane) are now being pursued in parallel, commercially viable projects (e.g., Tokyo Gas/Teralta). Several global mega-projects collapsed in mid-2025 due to poor economics, highlighting systemic market risk. Several projects were also axed. | The threat from competing carriers became concrete with the announcement of commercial projects leveraging existing infrastructure, proving their near-term advantage over LH 2. |

Future Scenarios: Kawasaki Heavy Industries’ 2027 FID and Canadian Project Viability

The critical event to watch for the Canada-Japan liquid hydrogen supply chain is the Final Investment Decision (FID) on the Canadian production and liquefaction facility, anticipated around 2027. This decision will serve as the ultimate validation of the project’s commercial viability. If the FID proceeds, it indicates that a combination of KHI’s technology cost-downs, Canadian production incentives, and Japanese offtake agreements (backed by subsidies) has successfully de-risked the multi-billion-dollar investment. Conversely, a delay or cancellation would confirm that the economic hurdles of the cryogenic pathway remain too high, likely ceding the near-term trans-Pacific hydrogen trade to more mature carriers like ammonia.

- A successful FID will depend on securing binding, long-term offtake agreements from major Japanese industrial users. Without these guarantees, financing for the massive infrastructure build-out will not materialize.

- The collapse of several large-scale hydrogen projects globally in 2025 serves as a stark warning. These failures were largely attributed to a lack of committed offtakers and unfavorable economics, the very risks the Canada-Japan project now faces.

- Watch for progress on KHI’s development of large-scale LH 2 carriers. The launch of a commercial-sized vessel, significantly larger than the Suiso Frontier, is a necessary precursor for achieving the economies of scale needed to lower shipping costs.

- The trajectory of Japan’s Cf D program is also critical. If the subsidies prove sufficient to bridge the cost gap for LH 2 and not just cheaper alternatives, it will provide the financial certainty needed for investors to commit. One of the largest global projects is the NEOM Green Hydrogen Company in Saudi Arabia.

The questions your competitors are already asking

This report covers one angle of the commercialization of trans-Pacific liquid hydrogen supply chains. The questions that matter most depend on your work.

- What is actually happening with the Canada-Japan liquid hydrogen supply chain since Kawasaki Heavy Industries withdrew from the HESC commercial phase?

- Who are Kawasaki Heavy Industries’ key upstream hydrogen production partners in Canada?

- What is the cost breakdown of a trans-Pacific liquid hydrogen supply chain, from Canadian production to delivery in Japan?

- Kawasaki Heavy Industries’ investments and funding. Is the Canada-Japan project on track to leverage Japan’s $20B Contracts for Difference program?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.