US-Iran War 2026: Why LNG’s Role as a Global Transition Fuel Is Over

Geopolitical Shock: 2026 Conflict Shatters LNG’s Foundational Reliability

The outbreak of the US-Iran conflict in 2026 has shattered the foundational assumption that Liquefied Natural Gas (LNG) is a reliable transition fuel. Before the conflict, from 2021 to 2024, the primary risks associated with LNG were related to methane emissions and market competition from renewables. The war, however, transformed the theoretical threat of supply chain disruption into a catastrophic reality, exposing a fatal flaw in the global LNG market: its over-reliance on the Strait of Hormuz. This event has fundamentally and permanently eroded LNG’s credibility as a secure energy source for nations planning a multi-decade energy transition.

- Prior to 2025, the debate around LNG focused on its climate impact, with a 2024 study noting its lifecycle emissions could be worse than coal. The 2026 war shifted the primary concern from climate credentials to existential supply security, demonstrating how a regional conflict can annihilate a significant portion of global supply overnight.

- The conflict triggered an immediate supply shock when Qatar Energy, the world’s largest LNG producer, suspended all production following direct attacks. This single event removed approximately 20% of the global LNG supply from the market, a scale of disruption previously unseen.

- The market reaction was severe, with European natural gas futures soaring over 40% on the conflict’s first day. Analysts from DBS Bank warned that a prolonged conflict could see LNG prices triple, creating extreme inflationary pressure and destroying the price stability required for long-term energy planning.

- The de facto closure of the Strait of Hormuz due to prohibitive insurance costs created a chokepoint crisis. This severed major importers in Asia and Europe from their key suppliers in Qatar and the UAE, proving that diversifying suppliers is insufficient if they all rely on the same vulnerable transit route. The crisis underscores the permanent shift now underway in LNG supply chains.

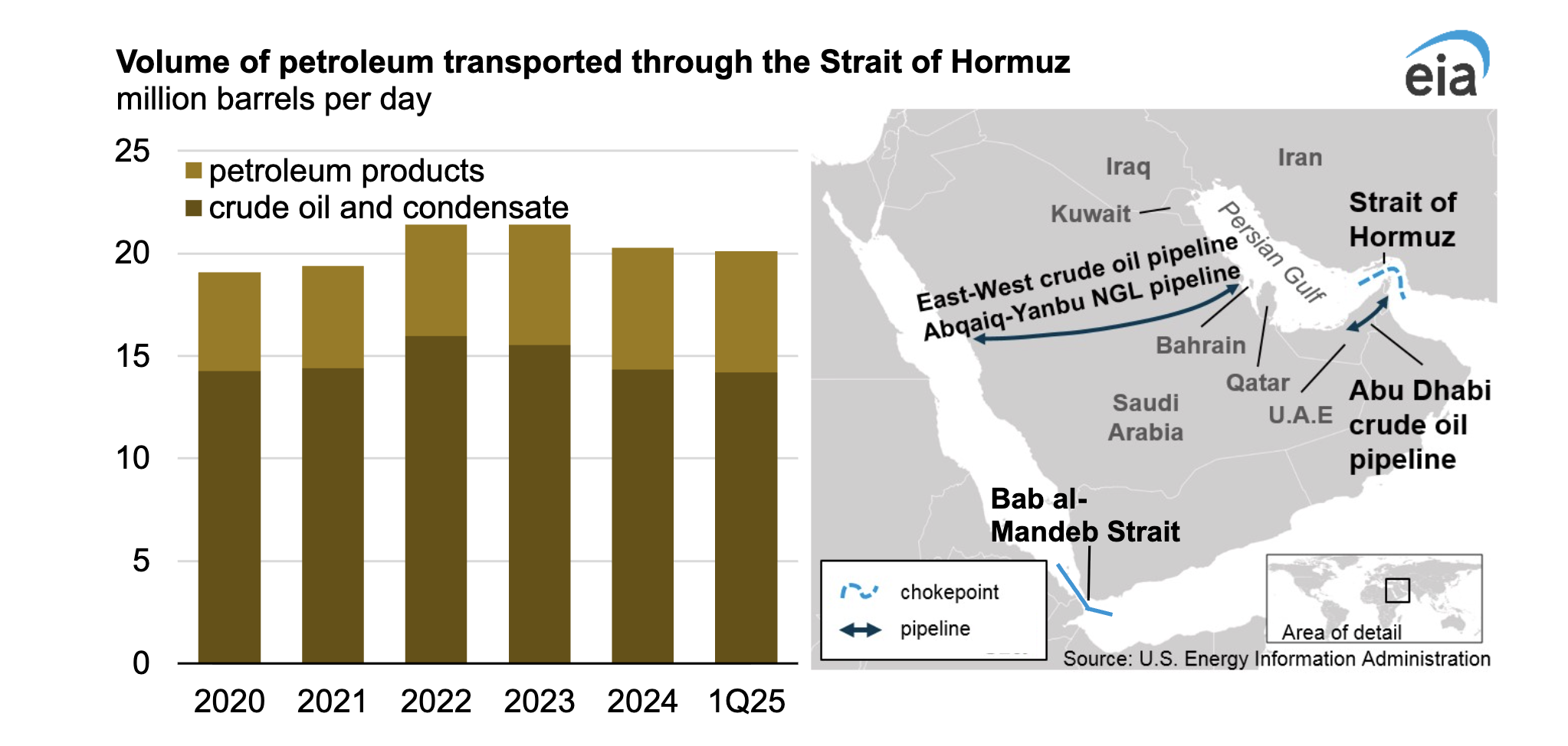

Hormuz Chokepoint Shows LNG Vulnerability

This chart’s focus on the Strait of Hormuz as a critical chokepoint for Qatari and other energy exports directly illustrates the central thesis of this section: the fatal over-reliance on this single maritime route.

(Source: EUobserver)

Market Disruption: Supply Cancellations and Price Explosions in 2026

The US-Iran war did not just disrupt markets; it triggered a series of immediate and large-scale supply cancellations that sent shockwaves through the global economy. The halt in production from key Middle Eastern producers was not a temporary slowdown but a complete cessation of activity, forcing a re-evaluation of all LNG-dependent investments and strategies. This event differs from the 2022 Russia-Ukraine crisis, as it disabled both production facilities and the primary maritime route for a significant portion of global LNG and oil.

Pre-Conflict Forecasts Projected Strong LNG Growth

This chart shows a strong pre-conflict market growth forecast, providing a baseline of financial optimism that was shattered by the supply cancellations and price explosions detailed in this section.

(Source: Fortune Business Insights)

Table: Energy Market Shocks Following the US-Iran Conflict (March 2026)

| Market Segment | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| LNG Price | March 2026 | European natural gas futures soared by over 40% as the conflict began and Qatari production halted, wiping out any pretense of price stability. | intellectia.ai |

| LNG Supply | March 2026 | The halt of Qatar Energy’s production at Ras Laffan removed approximately 20% of total global LNG supply, creating a massive, immediate deficit. | The Independent |

| Crude Oil Price | March 2026 | Brent crude oil prices spiked by over 8%, with analysts projecting prices could surpass $100 per barrel if the conflict persists, affecting the entire energy complex. | Financial Post |

| Refined Products | March 2026 | Saudi Arabia was forced to shut down its largest oil refinery after it was targeted, compounding the supply crisis for both crude and petroleum products. | SCMP |

Geographic Fallout: A Forced Pivot in European and Asian Energy Security

The conflict has forced a radical and immediate recalculation of energy security for the world’s largest LNG-importing regions, particularly Europe and Asia. While the 2021-2024 period saw这些地区深化对全球LNG市场的依赖以实现能源多元化,2026年的战争暴露了这种战略的根本脆弱性。对卡塔尔液化天然气的严重依赖,如今已从一项战略资产转变为一个严重的经济和安全负债。

US LNG Exports Surged Prior to 2026 Crisis

This chart visually confirms the section’s point about Europe’s increasing reliance on U.S. LNG, showing the rapid growth of this specific trade corridor in the years leading up to the conflict.

(Source: Mongabay)

- Between 2021 and 2023, Europe dramatically increased its reliance on U.S. LNG to displace Russian gas, making the transatlantic corridor a dominant trade route. The 2026 crisis revealed this was only a partial solution, as the loss of Qatari volumes created a new, unfillable supply gap, forcing Germany to reactivate its gas emergency task force.

- Asian economies, which accounted for the majority of long-term contracts with Qatar, faced an even more severe crisis. Nations like China, India, and South Korea, which had based their coal-to-gas transition strategies on reliable Qatari supply, were left exposed to extreme price volatility and physical shortages.

- The United States, as the world’s largest LNG exporter, saw a short-term surge in demand and margins for its uncontracted volumes. However, U.S. exporters and new facilities like the Golden Pass LNG terminal cannot fully replace the massive volumes lost from the Middle East, a fact that forces importing nations toward demand reduction and accelerated fuel switching rather than simple supplier substitution. This reality impacts the strategies of major players like Cheniere and Conoco Phillips.

- The crisis has redefined energy security away from diversifying fossil fuel suppliers and toward diversifying energy types. The new imperative is building resilient, localized energy systems based on renewables and storage, which are immune to geopolitical chokepoints like the Strait of Hormuz. This strategic shift is central to understanding the shock to the global energy transition.

Narrative Collapse: LNG’s Bridge Fuel Status Becomes Untenable

The 2026 conflict has proven the “bridge fuel” narrative for LNG to be fundamentally unsound. The concept of a reliable bridge requires structural integrity, yet the war has demonstrated that the LNG supply chain has a critical, unfixable vulnerability. The stability premium offered by renewable energy sources, previously a secondary consideration, has now become the primary driver for future energy investments. Strategic planning at firms like Shell, Chevron, Eni, and ADNOC must now account for this paradigm shift.

Shell’s Forecast Epitomized ‘Bridge Fuel’ Narrative

This pre-conflict demand forecast from Shell, a major player mentioned in the text, perfectly visualizes the strong ‘bridge fuel’ narrative that this section argues has now collapsed.

(Source: Natural Gas Intelligence)

- From 2021-2024, LNG’s maturity as a transition fuel was validated by its growing role in displacing coal and Russian gas. Investments in liquefaction and import terminals were seen as long-term, viable assets for a decades-long transition.

- The 2026 crisis invalidates this long-term view by highlighting the extreme risk of stranded assets. Multi-billion dollar, 30-year investments in LNG infrastructure now appear reckless when the fuel supply can be cut off indefinitely by a regional conflict.

- The conflict starkly contrasts the chaotic, unpredictable pricing of LNG with the stable, predictable costs of renewable energy projects. A 20-year solar or wind Power Purchase Agreement (PPA) offers complete immunity from geopolitical shocks and fuel price volatility, making it a superior tool for economic and national security.

- The argument to accelerate the green transition has moved from an environmental talking point to a core tenet of national security. The crisis provides the ultimate justification for a wartime-level investment in renewable generation, grid-scale storage, and energy efficiency to build resilient, independent energy systems.

SWOT Analysis: LNG’s Role as a Transition Fuel Post-Conflict

The strategic landscape for LNG has been irrevocably altered by the 2026 US-Iran war. A comparison of its strategic positioning before and after the conflict reveals that its fundamental weaknesses were exposed, its threats were realized, and its core strengths were negated. The opportunities for LNG have now largely been transferred to its renewable energy competitors.

Table: SWOT Analysis for LNG’s Role as a Transition Fuel

| SWOT Category | 2021 – 2024 (Pre-Conflict) | 2025 – 2026 (Post-Conflict) | What Changed / Validated |

|---|---|---|---|

| Strengths | Considered cleaner than coal; flexible and fungible global commodity; growing supply from politically stable regions like the U.S. | Fungibility is negated by supply chain collapse; U.S. supply is insufficient to cover the deficit, driving prices to unsustainable levels. | The strength of fungibility was proven to be entirely dependent on the security of chokepoints, which failed. |

| Weaknesses | Lifecycle methane emissions undermine climate benefits; capital-intensive infrastructure with long lead times; known reliance on geopolitical chokepoints (e.g., Hormuz, Panama Canal). | The Strait of Hormuz chokepoint is validated as a catastrophic single point of failure; price volatility becomes extreme, not cyclical. | A known, theoretical weakness (chokepoint reliance) was validated as a fatal, systemic flaw. |

| Opportunities | Displace coal in Asia to reduce air pollution and carbon emissions; replace Russian pipeline gas in Europe for energy security. | Short-term windfall for non-Middle East exporters (e.g., U.S.); primary opportunity shifts to renewable energy, storage, and efficiency as a more secure alternative. | LNG’s primary market opportunities are now overshadowed by its unreliability, accelerating the business case for its competitors. |

| Threats | Increasing cost-competitiveness of renewables and battery storage; geopolitical instability in the Middle East; policy shifts against fossil fuels (e.g., U.S. LNG pause). | The primary geopolitical threat is fully realized, causing a complete market rupture. LNG is now perceived as a high-risk liability. | The “black swan” event of a Hormuz closure occurred, making LNG an unacceptable risk for long-term national energy strategy. |

2027 Outlook: A Rapid, Forced Pivot to Geopolitically Stable Energy

The critical strategic action for 2027 and beyond is a rapid, deliberate pivot away from globally traded fossil fuels toward energy sources insulated from geopolitical risk. The 2026 war was an inflection point that ended the debate over LNG’s long-term role. If a nation’s energy security can be compromised by a conflict thousands of miles away, the energy source is no longer viable for foundational planning. The key signal to watch is whether governments and corporations now prioritize resilience over perceived short-term cost savings.

Data Supported LNG’s ‘Cleaner than Coal’ Strength

This chart quantifies a key pre-conflict ‘Strength’ from the SWOT table—that LNG has lower lifecycle emissions than coal—providing direct visual evidence for one of the core arguments presented.

(Source: Oil Price)

- Watch for accelerated renewable deployment: Expect European and Asian governments to announce aggressive new targets and subsidies for solar, wind, and battery storage, framing these investments as matters of urgent national security. This will directly impact the fleet strategies of companies like Chevron.

- Monitor LNG infrastructure investment decisions: The clearest signal of LNG’s diminished future will be the widespread cancellation or indefinite postponement of new long-term import terminal projects. Conversely, a push to complete projects already under construction will indicate a desperate short-term scramble for supply.

- Track the price of stability: Observe the corporate sector’s willingness to sign long-term, fixed-price PPAs for renewable energy, even if the nominal cost is higher than pre-crisis spot LNG prices. This will indicate a permanent market repricing of geopolitical risk.

- Observe U.S. policy divergence: The U.S. will face a strategic dilemma: capitalize on its position as a major LNG exporter to support allies, or adhere to climate goals by limiting new export infrastructure. The outcome of this debate will signal the future of LNG in the Atlantic basin and impact the growth strategies of firms like ADNOC looking to compete.

Frequently Asked Questions

Why did the 2026 US-Iran conflict supposedly end LNG’s role as a transition fuel?

The conflict ended LNG’s role by shattering its foundational assumption of reliability. The war led to the de facto closure of the Strait of Hormuz, a critical chokepoint, and halted production from Qatar, which removed 20% of global supply overnight. This event proved that the global LNG supply chain has a catastrophic single point of failure, making it too insecure for nations to rely on for long-term energy planning.

How was the 2026 LNG crisis different from the 2022 Russia-Ukraine crisis?

The 2026 US-Iran conflict was different because it simultaneously disabled both major production facilities in the Middle East and the primary maritime route (the Strait of Hormuz) for a significant portion of global LNG and oil. The 2022 crisis primarily concerned the disruption of Russian pipeline gas to Europe, which spurred a switch to seaborne LNG, but it did not physically shut down a major global production hub and its critical export chokepoint at the same time.

What was the immediate market impact of the conflict in March 2026?

The market reaction was immediate and severe. European natural gas futures soared by over 40% on the conflict’s first day. The halt of Qatar Energy’s production at Ras Laffan instantly removed approximately 20% of the total global LNG supply, creating a massive deficit. Additionally, Brent crude oil prices spiked over 8%, with analysts projecting prices could surpass $100 per barrel.

If LNG is no longer a viable bridge fuel, what is the proposed alternative?

The proposed alternative is a rapid and forced pivot toward diversified energy types, specifically resilient and localized energy systems. This means accelerating investment in renewables like solar and wind, along with grid-scale battery storage. These energy sources are considered superior because they are immune to geopolitical chokepoints and fuel price volatility, making them a more secure foundation for national energy strategy.

Why isn’t diversifying LNG suppliers, like buying from both the U.S. and Qatar, enough to ensure energy security?

Diversifying suppliers is insufficient if they all rely on the same vulnerable transit route. The 2026 crisis proved that even if a country has contracts with multiple suppliers in the Middle East (like Qatar and the UAE), the closure of the Strait of Hormuz severs access to all of them simultaneously. While U.S. supply offers some diversification, the article states it cannot fully replace the massive volumes lost from the Middle East, leaving importing nations exposed to shortages and extreme price shocks.