LNG Supply Expansion, $15.1 B Venture Global Financing, 14 Mtpa LNG Canada Project, and 29.5 M Tonnes in US SPAs (2025)

LNG Project Development, Venture Global $15.1 B Deal Signals Start of Supply Wave

The year 2025 marks a fundamental shift in the global Liquefied Natural Gas (LNG) market, initiating a transition from a period of supply scarcity to an era defined by an unprecedented wave of capacity expansion. This has created an intensely competitive environment where project viability is dictated by secured financing and long-term commercial backing, exposing a clear divide between well-positioned developers and those left behind. This market context is crucial for major energy firms like Exxon Mobil and its competitors.

- In the first ten months of 2025, U.S. LNG exports grew by 25% year-over-year as developers successfully secured a near-record 29.5 million metric tonnes per year in long-term Sales and Purchase Agreements (SPAs) to de-risk future projects.

- The scale of this new wave was validated in November 2025 when Venture Global closed a record-breaking $15.1 billion project financing for Phase 1 of its Calcasieu Pass 2 (CP 2) LNG facility, the largest deal of its kind for the industry.

- Canada officially entered the global export market as the LNG Canada project in British Columbia, with a Phase 1 capacity of 14 million tonnes per annum (Mtpa), prepared for its first shipments by mid-2025.

- Conversely, the competitive pressure and market risk became evident in December 2025 when Energy Transfer suspended its proposed 16.5 Mtpa Lake Charles LNG project, citing an inability to secure sufficient long-term offtake agreements.

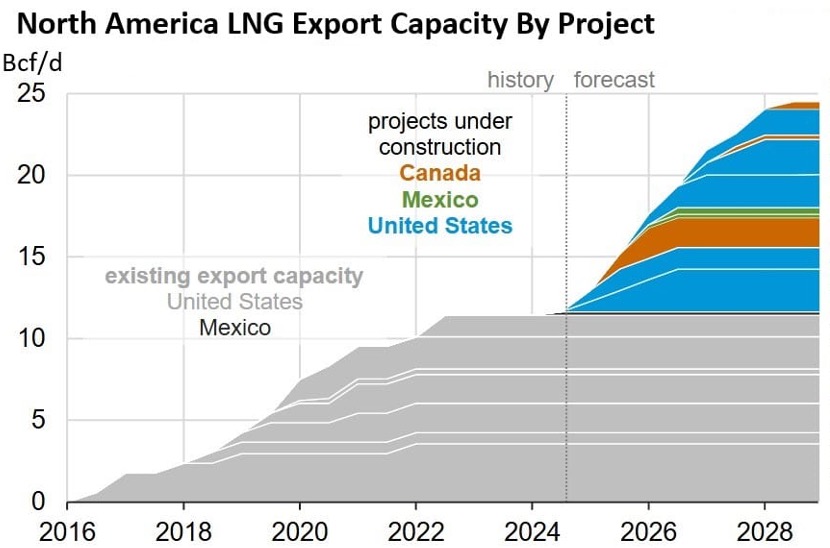

North American LNG Capacity Set to Double

This chart directly visualizes the ‘supply wave’ mentioned in the section heading by showing that North American LNG capacity is set to double, a direct result of the project developments discussed.

(Source: CRES Forum)

$15.1 B Venture Global, LNG Capital Flows to De-Risked US and Qatari Projects

Capital investment in 2025 LNG projects was robust but highly concentrated, flowing to commercially de-risked mega-projects while exposing a stark divide between developers with secured offtake agreements and those without. The high cost of onshore facilities, averaging around $960-$1, 000 per tonne, placed immense pressure on developers to secure financing, a challenge that proved insurmountable for some. This trend is part of a broader re-evaluation of large-scale energy projects, including those in the renewables sector like wind energy.

- Financial markets demonstrated strong appetite for de-risked projects, highlighted by Venture Global’s $15.1 billion financing for CP 2 and Next Decade’s successful $6.7 billion financing closure for Train 4 at its Rio Grande LNG facility.

- The high capital expenditure for new projects was confirmed by Woodside’s Louisiana LNG development, approved with a cost of $960 per tonne, and the Saguaro Energia project in Mexico, estimated at $1, 000 per tonne.

- Floating LNG (FLNG) projects emerged as a lower-cost alternative, with some projects like the Cameroon FLNG demonstrating CAPEX levels as low as $500 per tonne, offering a potential strategic pathway for cost reduction.

- The commercial failure of the 16.5 Mtpa Lake Charles LNG project, which was suspended in December 2025, serves as a clear market signal that capital is unavailable for projects lacking firm, long-term commercial commitments.

LNG Market to Exceed $227B by 2032

This chart quantifies the significant market value growth, which is a direct consequence and indicator of the large-scale capital flows into de-risked projects as described in the section.

(Source: Fortune Business Insights)

Table: Key LNG Project Investments and Cancellations (2025)

| Company / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Energy Transfer / Lake Charles LNG | Dec 2025 | Suspended the 16.5 Mtpa export project due to unfavorable market conditions and a failure to secure sufficient long-term offtake agreements, highlighting market risk. | S&P Global |

| Venture Global / CP 2 LNG | Nov 2025 | Closed a record $15.1 billion project financing for Phase 1, demonstrating strong investor confidence in commercially de-risked U.S. LNG export projects. | Venture Global |

| Next Decade / Rio Grande LNG | Oct 2025 | Closed $6.7 billion in financing for the fourth liquefaction train, confirming the bankability of projects with secured offtake agreements. | Next Decade |

| Woodside / Louisiana LNG | Apr 2025 | Approved development with a project cost of $15.9 billion, establishing a CAPEX benchmark of $960 per tonne for new U.S. Gulf Coast facilities. | Woodside |

LNG Offtake Agreements, Sempra and Total Energies Secure Long-Term Supply Deals

Securing long-term offtake agreements became the critical path to project sanction in 2025, with major players like Sempra, Total Energies, and Chevron locking in multi-decade partnerships to underwrite massive capital investments. These deals, often involving both supply commitments and direct equity stakes, were essential for developers to obtain the billions in financing required to move projects from proposal to construction.

- In August 2025, Sempra and Conoco Phillips extended their partnership on the Port Arthur LNG project, signing a 20-year offtake deal for 5 Mtpa and giving Conoco Phillips a 30% equity stake in Phase 1.

- Total Energies signed a 20-year agreement in May 2025 to offtake 0.5 Mtpa from the Ksi Lisims LNG project in British Columbia and made a strategic investment in the project’s developer, Western LNG.

- Venture Global expanded its partnership with Germany’s SEFE in July 2025, a move that positions the U.S. developer to become Germany’s largest single LNG supplier.

- In June 2025, Japan’s JERA finalized 20-year agreements to procure 5.5 Mtpa of LNG from U.S. projects, underscoring the long-term demand from established Asian buyers.

Europe Becomes Top Destination for U.S. LNG

This chart illustrates the outcome of the offtake agreements mentioned in the heading. Deals with companies like TotalEnergies directly contribute to Europe being a top destination for US LNG.

(Source: American Security Project)

Table: Major LNG Commercial Partnerships and Agreements (2025)

| Partners | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Sempra / Conoco Phillips | Aug 2025 | Extended partnership on Port Arthur LNG, including a 20-year SPA for 5 Mtpa and a 30% equity investment by Conoco Phillips, fully securing the project’s commercial basis. | Sempra |

| Venture Global / SEFE | Jul 2025 | Expanded LNG partnership, positioning Venture Global to become Germany’s largest LNG supplier and strengthening transatlantic energy security ties. | Venture Global |

| Total Energies / Ksi Lisims LNG | May 2025 | Signed a 20-year SPA for 0.5 Mtpa and a strategic investment, providing a key commercial anchor for Canada’s second wave of LNG projects. | Ksi Lisims LNG |

North America vs. Qatar, A Geographic Analysis of New LNG Supply Leadership

The U.S. Gulf Coast and Qatar solidified their positions in 2025 as the dual epicenters of global LNG supply growth, creating a competitive dynamic that will define the market for the next decade. While the U.S. leads in the number of independent projects, Qatar’s state-backed North Field Expansion offers a scale and cost structure that presents a formidable challenge. Concurrently, Canada emerged as a new, strategically significant Pacific basin supplier targeting Asian markets.

- United States: The Gulf Coast was the hub of activity, with massive project financing deals for Venture Global’s CP 2 and Next Decade’s Rio Grande LNG confirming its leadership. However, the U.S. administration’s pause on new LNG export terminal approvals created uncertainty for a second wave of projects.

- Qatar: The state-owned energy company advanced its North Field Expansion, which plans to add 32 million tonnes of capacity by 2026, competing directly with U.S. projects for long-term contracts with Asian and European buyers.

- Canada: The LNG Canada project in Kitimat, British Columbia, began commissioning in 2025, marking Canada’s debut as a major LNG exporter. Projects like Ksi Lisims LNG also gained commercial traction, strengthening Canada’s role.

- Mexico: Projects such as Mexico Pacific’s Saguaro Energia facility advanced, offering an alternative Pacific Coast export route for U.S. gas that avoids the Panama Canal and targets Asian markets directly.

US LNG Competes on Cost with Global Alternatives

This chart provides a key data point for the ‘Geographic Analysis of New LNG Supply Leadership’ by explaining a primary reason for North America’s competitiveness against rivals like Qatar.

(Source: S&P Global)

LNG Technology in 2025, Focus Shifts from Innovation to Efficiency and Decarbonization

With core liquefaction technology fully mature at Technology Readiness Level (TRL) 9, the competitive focus for LNG developers in 2025 shifted from fundamental process innovation to operational excellence, marginal efficiency gains, and the integration of decarbonization technologies. Meeting increasingly stringent emissions standards and managing costs in a more competitive market became the primary drivers of technological strategy. This focus on decarbonization is also being seen in data center energy strategies, with companies like Microsoft exploring nuclear and solar power.

- Leading operators like Cheniere focused on optimizing existing processes, employing the highly efficient Optimized Cascade® process and aeroderivative gas turbines to improve performance and reduce emissions at their facilities.

- The integration of Carbon Capture and Storage (CCS) gained momentum as a critical component for new projects. Some CCS technologies for LNG applications were validated at TRL-7, demonstrating the ability to capture 10 tonnes of CO 2 per day in pilot phases.

- Floating LNG (FLNG) technology demonstrated a significant cost advantage in some applications. Rystad Energy analysis showed certain FLNG projects achieving CAPEX levels below $600 per tonne, compared to nearly $1, 000 per tonne for some onshore facilities.

- The International Maritime Organization’s approval of a “Net-zero Framework” in April 2025 put direct pressure on LNG shipping, driving investment in more efficient vessel designs and lower-emission propulsion systems to manage future GHG pricing.

LNG Market Shifting to Tech and Low-Carbon Solutions

The chart’s headline is a direct match for the section’s theme, which focuses on the shift in LNG technology towards efficiency and decarbonization.

(Source: MarketsandMarkets)

SWOT Analysis, LNG Market Strengths and Competitive Threats in 2025

The 2025 LNG market is defined by the strength of its massive, de-risked project pipeline, which is backed by a surge in long-term contracts from Asia and Europe. However, this strength is counterbalanced by significant threats from a potential structural oversupply post-2026, which could depress prices, and geopolitical policy risks that could strand future investments. The global energy market remains volatile, a point underscored in the IEA’s analysis of potential supply disruptions.

Natural Gas is Top US Electricity Source

This chart illustrates a fundamental ‘Strength’ for a SWOT analysis of the US-led LNG market: a vast and stable domestic natural gas supply, which underpins its ability to export.

(Source: American Security Project)

Table: SWOT Analysis for the Global LNG Market (2025)

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | U.S. established as a major, reliable supplier; strong European demand growth post-Ukraine invasion. | Massive project pipeline de-risked with long-term contracts (29.5 M tonnes in US SPAs); LNG Canada comes online. | The market validated that bankable projects require long-term contracts, solidifying the two-tiered nature of the market. |

| Weaknesses | High spot price volatility; supply chain constraints and rising construction costs for new projects. | High CAPEX (~$1, 000/tonne) remains a barrier; projects without commercial backing are suspended (Lake Charles LNG). | The high-cost environment was confirmed, making projects without exceptional commercial terms or lower-cost models (FLNG) unviable. |

| Opportunities | Coal-to-gas switching in Asia; Europe’s need to replace Russian gas. | Emerging demand from AI data centers; lower prices post-2026 could accelerate demand growth in price-sensitive markets. | New demand drivers like AI emerged as a significant factor, adding a new layer of long-term structural demand for natural gas and power. |

| Threats | Risk of Russian supply disruption; global economic slowdown impacting demand. | A massive wave of new supply (~300 bcm) risks creating a structural surplus; U.S. policy pause on new terminals creates uncertainty. | The threat shifted from acute supply shortages to a potential long-term supply glut, altering the risk calculus for future investments. |

2026 LNG Outlook, Will Demand Absorb the Oncoming Supply Wave?

The primary question for 2026 is whether global demand, particularly from price-sensitive Asian markets, can absorb the massive wave of new LNG supply without a significant and prolonged price collapse that would challenge the economics of the next wave of projects. The interplay between U.S. policy, Qatari competition, and Asian demand growth will determine the market’s trajectory.

- If Asian demand grows faster than anticipated, driven by lower prices and aggressive coal-to-gas switching, then watch for a rapid increase in spot cargo purchases and a new wave of long-term contracts for projects targeting FID in 2027-2028.

- If the U.S. policy pause on new export terminals remains in effect for an extended period, then watch for investment and commercial momentum to shift decisively toward Canadian, Mexican, and Qatari projects, giving them a distinct competitive advantage.

- These developments could happen as the market processes the largest supply expansion in its history. A key signal to monitor is the pace of FIDs for projects that do not yet have full offtake coverage; a slowdown would indicate that financiers are becoming wary of future market oversupply.

LNG Market Growth Projected Through 2034

This chart directly addresses the section’s forward-looking question, ‘Will Demand Absorb the Oncoming Supply Wave?’, by projecting long-term market demand growth.

(Source: Market.us)

The questions your competitors are already asking

This report covers one angle of the competitive landscape for LNG project development. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the North American LNG project development market?

- What is the outlook for US LNG supply expansion by 2030, following the current wave of project financing?

- Venture Global investments and funding. Is the Calcasieu Pass 2 project on track after securing its record $15.1B financing?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.