PEM Fuel Cell Market 2026: How Government Billions & Corporate Pivots Are Forcing Industrial Scale-Up

From Commercial Pilots to Industrial Scale: PEM Fuel Cell Adoption Accelerates

The Proton Exchange Membrane (PEM) fuel cell industry has decisively shifted from proving commercial viability in niche applications between 2021 and 2024 to a state-sponsored race for industrial-scale deployment in heavy-duty transport and green hydrogen production in 2025 and 2026. This transition is defined by massive government investment and strategic consolidation around PEM as the dominant technology for mass-market decarbonization.

- Between 2021 and 2024, market adoption was characterized by proving technology in contained ecosystems, such as Plug Power deploying over 69, 000 fuel cell systems in the materials handling sector and China putting nearly 6, 000 fuel cell electric vehicles on the road, primarily in heavy-duty pilots. These actions established operational reliability and a baseline for manufacturing.

- The turning point in 2025 was Bosch’s strategic decision to cease development of solid oxide fuel cells (SOFC) and redirect all resources to PEM-based technologies. This pivot by a major Tier 1 supplier validated PEM as the most commercially viable pathway for scaling hydrogen solutions in mobility and electrolysis.

- From 2025 onward, application focus has narrowed and deepened. Projects are now aimed at breaking into the largest markets, demonstrated by the Mi Na Mi project, which targets Europe’s first megawatt-scale PEM fuel cell specifically for heavy-duty trucking, shipping, and rail applications.

- The market is also moving toward vertically integrated models, where PEM technology serves both the production and consumption of hydrogen. Plug Power’s successful securing of a $1.66 billion DOE loan in January 2025 to produce both clean hydrogen and the American-made electrolyzers to make it exemplifies this new industrial strategy.

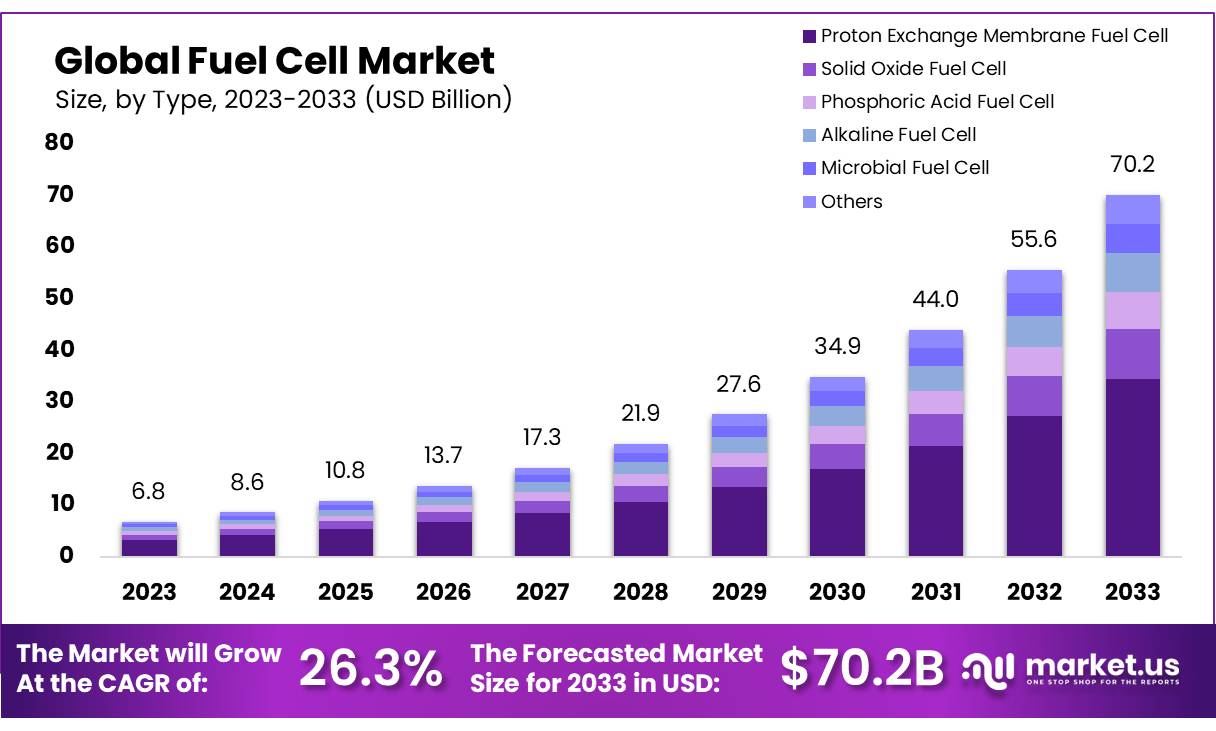

PEM Segment Dominates Fuel Cell Growth

This chart shows Proton Exchange Membrane (PEM) fuel cells as the largest and fastest-growing segment, supporting the article’s focus on PEM as the dominant technology for mass-market decarbonization.

(Source: Market.us)

Investment Analysis: Public Billions De-Risk PEM Fuel Cell Supply Chains

Investment in the PEM fuel cell sector has evolved from private-led, project-specific financing to massive, public-sector-led de-risking designed to catalyze the creation of entire domestic supply chains. This shift from corporate CAPEX to sovereign industrial policy fundamentally changes the scale and speed of market development.

- The $1.66 billion conditional loan guarantee from the U.S. Department of Energy to Plug Power in January 2025 represents a landmark event. Its purpose is not just to fund a single company but to underwrite the build-out of a national clean hydrogen production and PEM electrolyzer manufacturing base.

- In Europe, government funding has become a critical tool for creating stable, long-term demand. Spain’s allocation of €415 million in December 2025 for green hydrogen auctions and the EU’s €7 million funding for the Mi Na Mi project are designed to stimulate demand for PEM electrolyzers and heavy-duty fuel cells.

- This state-led investment model contrasts sharply with the period from 2021 to 2024, which was defined by corporate-led investments like Johnson Matthey‘s £80 million gigafactory in the UK. While significant, such investments carried a higher private-sector risk and were a fraction of the scale of the government programs now in place.

Table: Key PEM-Related Government Funding and Investments (2025)

| Entity / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Spain Green Hydrogen Fund | 2025-12-03 | Allocation of €415 Million in national funds to support projects in the European Hydrogen Bank auctions, creating a strong demand signal for PEM electrolyzers. | Fuel Cell Works |

| Mi Na Mi Project | 2025-07-23 | A €7 Million EU-funded initiative to develop Europe’s first megawatt-scale PEM fuel cell, specifically targeting cost and durability barriers in heavy-duty transport. | Fuel Cell Works |

| Plug Power / U.S. DOE | 2025-01-17 | A $1.66 Billion loan guarantee to support the construction of facilities for producing clean hydrogen and PEM electrolyzers, anchoring a domestic U.S. supply chain. | U.S. Department of Energy |

Partnership Analysis: Alliances Form to Solve PEM Commercialization Barriers

Strategic collaborations in the PEM sector have sharpened from broad technology development into targeted, multi-stakeholder projects aimed at solving the final barriers to mass commercialization, including component cost, manufacturing scale, and material sustainability. These alliances are now focused on engineering solutions for industrial production rather than simply proving concepts.

PEM Fuel Cell Materials Market Expands

This forecast highlights the growing market for key components like Bipolar Plates, which directly relates to the partnerships discussed that aim to solve cost and material barriers.

(Source: Hydrogen Central)

- The Mi Na Mi project, which includes Power Cell Group, exemplifies this new model. It unites fuel cell manufacturers, research institutes, and end-users under a single EU-funded objective: to build a powerful, durable, and cost-effective PEM fuel cell for heavy-duty transport, directly addressing a critical market need.

- The ECOPEM project, funded by the European Commission, is a highly specific R&D collaboration focused on developing non-fluorinated components for PEM fuel cells and electrolyzers. This targets a key long-term risk related to environmental regulations (PFAS) and material costs.

- In Japan, a project sponsored by the New Energy and Industrial Technology Development Organization (NEDO) selected Sumitomo Electric in October 2025 to accelerate the development of anion exchange membranes (AEM). This shows a collaborative push to innovate on core membrane technology to improve performance and reduce reliance on expensive platinum-group metals.

Geographic Focus: North America and Europe Launch State-Backed Industrial Strategy

While China led the world in early deployment volume through 2024, the strategic geography of the PEM fuel cell market has shifted in 2025 and 2026. North America and Europe are now executing coordinated industrial strategies, using massive state funding to build sovereign manufacturing capacity and integrated hydrogen ecosystems.

North American Fuel Cell Market Grows

This chart quantifies the growth of the North American market, directly supporting the section’s focus on the region’s execution of a coordinated, state-backed industrial strategy.

(Source: Market Data Forecast)

- From 2021 to 2024, China was the undisputed deployment leader, adding nearly 6, 000 fuel cell vehicles in 2023 alone. This created essential market pull and drove initial economies of scale for companies like the Reshaping Group, which has deployed over 4, 000 systems.

- In 2025, the United States asserted its industrial ambitions with the $1.66 billion DOE loan to Plug Power. This funding is explicitly aimed at onshoring the supply chain for green hydrogen and PEM electrolyzers, signaling a strategic priority to establish domestic energy security and technology leadership.

- Simultaneously, Europe is constructing a coordinated industrial base through initiatives like the Mi Na Mi and ECOPEM projects. This EU-level R&D is complemented by aggressive national funding, such as Spain’s €415 million commitment, creating a powerful, multi-layered ecosystem to rival Asia and North America.

Technology Maturity: PEM Moves From Validated to Industrialization Phase

Proton Exchange Membrane technology has successfully transitioned beyond the commercial validation phase and is now firmly in an industrialization and optimization stage. The industry’s focus has shifted from proving reliability to engineering for mass production, reducing system costs, and scaling power output for the most demanding applications.

PEM Tech Matures, Boosting Power Density

This chart illustrates the technology’s maturation by tracking the consistent increase in power density over 25 years, visually confirming the shift from validation to industrialization.

(Source: Nature)

- The period between 2021 and 2024 served as the final validation stage. The maturity of PEM technology was confirmed by the operational success of large fleets, including over 1, 800 buses powered by Ballard Power Systems technology and the tens of thousands of forklift systems from Plug Power operating for years in high-uptime environments.

- The definitive signal of PEM’s technological dominance and commercial readiness arrived in February 2025, when industrial giant Bosch abandoned its SOFC development to concentrate entirely on PEM. This move by a key market maker confirmed that PEM has won the race for mass-market applications like mobility.

- Current R&D efforts in 2025 and 2026 are no longer about basic feasibility. They are highly targeted at solving industrial-scale challenges, such as developing non-PFAS components (ECOPEM project) to mitigate future regulatory and cost risks, and engineering megawatt-scale systems (Mi Na Mi project) required for heavy-duty transport.

SWOT Analysis: PEM Fuel Cell Market at a Strategic Inflection Point

The PEM fuel cell market’s primary strength has evolved from technological leadership in niche markets to a powerful, state-backed industrial engine. However, this rapid, capital-intensive scale-up introduces significant execution risks related to infrastructure build-out and securing sufficient offtake to absorb new manufacturing capacity.

PEM Fuel Cell Market to Quadruple

This forecast shows the scale of the opportunity in the PEM fuel cell market, providing crucial context for the SWOT analysis by quantifying the high-growth environment.

(Source: Precedence Research)

Table: SWOT Analysis for the PEM Fuel Cell Market

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Proven technology with high reliability in niche markets (e.g., materials handling with Plug Power). Deep technical expertise held by pioneers like Ballard Power Systems. | Massive government financial backing ($1.66 B DOE loan). Strategic validation from major industrial players (Bosch pivot). Dominant technology for green hydrogen production. | The market’s strength shifted from technical proof points to financial and strategic validation at a national industrial policy level. PEM is now a de-risked technology choice for governments. |

| Weakness | High total cost of ownership. Dependency on expensive platinum-group metals. Lack of scaled manufacturing capacity. | Manufacturing capacity is still catching up to GW-scale ambition. High dependency on the parallel build-out of green hydrogen refueling infrastructure. | While funding is flowing to manufacturing, the core weakness has shifted to a systemic dependency on the pace of the broader hydrogen economy, which is outside any single company’s control. |

| Opportunity | Decarbonize heavy-duty transport (trucks, buses). Provide backup power for critical facilities (e.g., New York data center test). | Build out sovereign, vertically integrated green hydrogen ecosystems. Displace diesel generators at scale. Address hard-to-abate marine and rail sectors with MW-scale systems. | The opportunity grew from replacing specific assets to building entire new energy value chains, supported by government mandates and funding for energy independence. |

| Threat | Strong competition from advancing battery-electric technology. Slow pace of hydrogen infrastructure investment. Volatility of public company valuations. | Execution risk on gigaprojects and infrastructure. Market consolidation and potential for shakeouts (e.g., MAN Energy Solutions job cuts). Dependence on continued, stable policy support. | The primary threat is no longer technological competition but the systemic risk of failing to execute the massive industrial scale-up and infrastructure build-out that is now being funded. |

2026 Scenario: Focus Shifts to Offtake as Production Capacity Ramps Up

If the massive capital injections of 2025 successfully accelerate PEM fuel cell and electrolyzer manufacturing capacity, the most critical signal to watch in 2026 will be the conversion of this potential supply into firm, large-volume, multi-year offtake agreements. The central question is no longer whether the factories can be built, but whether customers will emerge at a commensurate scale.

Transport Sector Drives PEM Market Growth

This chart projects the transport sector will become the dominant application, directly supporting the 2026 scenario where securing large-volume offtake agreements from this sector is critical.

(Source: Global Market Insights)

- If this happens: Manufacturers like Plug Power, Cummins, and Ballard Power Systems announce a series of binding, multi-hundred-unit orders for heavy-duty truck and bus modules.

- Then watch this: The share prices and investment ratings of these companies, as the market rewards tangible revenue visibility over projected capacity. Also, monitor for final investment decisions (FIDs) on new green hydrogen production plants directly linked to the DOE loan and EU funding programs.

- Because this could be happening: A surge in firm orders would validate the entire government-led investment thesis, confirming that demand from logistics, transport, and industrial offtakers is materializing. Conversely, a continued reliance on Mo Us and pilot-scale orders would signal that vehicle and infrastructure demand is lagging manufacturing investment, indicating a potential near-term supply glut and increasing the pressure for market consolidation.

Frequently Asked Questions

What is the biggest change in the PEM fuel cell market described in the report?

The main change is the shift from proving commercial viability in niche applications (2021-2024) to a state-sponsored race for industrial-scale deployment (2025-2026). The focus has moved from pilot projects to mass production for heavy-duty transport and green hydrogen, driven by billions in government investment and strategic corporate pivots.

Why is PEM technology now considered the dominant choice for fuel cells?

PEM’s dominance was validated by two key factors mentioned in the article. First, its operational reliability was proven in large-scale deployments, like the 69,000 systems used by Plug Power. Second, industrial giant Bosch made a strategic decision in 2025 to stop developing other fuel cell types (like SOFC) to focus entirely on PEM, signaling that it is the most commercially viable technology for mass-market mobility.

What is the government’s new role in the PEM fuel cell industry?

Governments have moved from funding individual projects to driving a full-scale industrial strategy. They are using massive public funding, such as the U.S. DOE’s $1.66 billion loan to Plug Power and Spain’s €415 million fund, to de-risk the creation of entire domestic supply chains for PEM fuel cells and green hydrogen. This state-led investment is designed to build sovereign manufacturing capacity and accelerate market growth.

According to the SWOT analysis, what is the biggest threat to the PEM market’s growth?

The primary threat has shifted from technological competition to execution risk. The article states the main danger is the potential failure to execute the massive industrial scale-up and build out the necessary hydrogen refueling infrastructure. This systemic risk depends on factors beyond any single company’s control and is more critical than competition from technologies like batteries.

For 2026, why is the focus shifting to securing “offtake agreements”?

With massive investments pouring into building manufacturing capacity in 2025, the critical question for 2026 will be whether customers exist at a similar scale. Offtake agreements are firm, multi-year contracts for large volumes of products. Securing these agreements would prove that real demand from heavy-duty transport and industrial users is materializing, validating the government-led investment and turning projected capacity into tangible revenue.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.