China Solar Market 2026: Overcapacity Crisis Forces Strategic Shift from Growth to Consolidation

Solar Overcapacity Risk: China’s Pivot from Unchecked Growth to Market Management

In 2025, China’s solar sector transitioned from a phase of aggressive expansion to one of confronting the systemic risks of its own manufacturing dominance. The period between 2021 and 2024 was defined by rapid, state-driven capacity build-out to meet ambitious national targets. However, 2025 data reveals a critical inflection point where manufacturing capacity vastly outstripped global demand, forcing a strategic pivot toward consolidation and managing the consequences of success.

- Between 2021 and 2024, the primary focus was on scaling production and deployment, with projects like the 16 GW Kubiqi Desert Clean Energy Base exemplifying the massive scale of development under the 14 th Five-Year Plan.

- The market shifted dramatically in 2025, when China’s annual solar manufacturing capacity reached an estimated 1, 200 GW, nearly double the total global installation demand of around 650 GW. This created immense price pressure and financial risk across the supply chain.

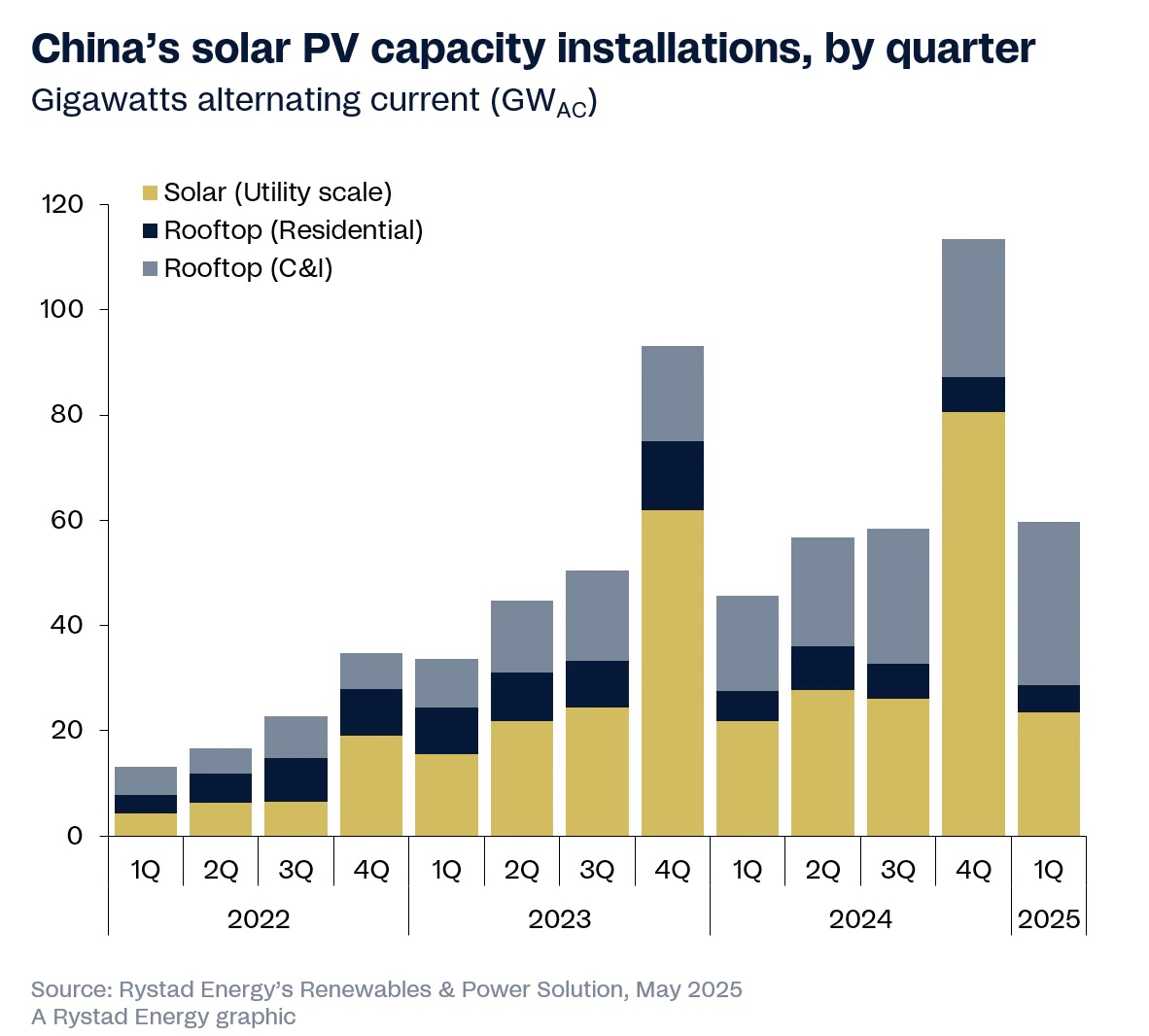

- The unprecedented installation of 60 GW of solar capacity in Q 1 2025 alone, while a milestone, also signaled the immense domestic pressure to absorb the manufacturing surplus, with a significant portion coming from distributed rooftop projects.

- This overcapacity is not an unforeseen consequence but the result of a deliberate industrial strategy to control the global supply chain, which now requires a new phase of state-influenced market management to avoid a catastrophic industry-wide correction.

China’s Solar Installations Drop Sharply

This chart illustrates the “critical inflection point” of 2025, showing the sharp drop in installations after a period of unchecked growth, which directly supports the section’s theme of pivoting to manage overcapacity.

(Source: Rinnovabili)

Investment Pivot: Polysilicon Consolidation Fund Signals Market Correction

Financial activity in China’s solar sector during 2025 shifted from funding pure expansion to financing strategic consolidation. The emergence of a planned multi-billion-dollar fund to manage polysilicon overcapacity is the clearest signal of this new market reality, representing an industry-led, state-influenced effort to stabilize prices and prevent widespread financial distress among producers.

- The most significant financial development in 2025 was the plan by major polysilicon producers, including GCL Technology, to create a $7 billion fund. The objective is to acquire and shut down up to one-third of the industry’s production capacity to address the severe supply glut.

- This action contrasts with the prior period’s investment focus, which saw capital flowing into building new production lines and multi-gigawatt solar farms to meet national deployment goals.

- Despite market pressures, leading vertically integrated companies demonstrated financial resilience. Canadian Solar reported strong Q 2 2025 net revenues of $1.7 billion, driven by diversification into battery energy storage systems, indicating that robust business models can weather the volatility.

Table: Strategic Financial Initiatives in China’s Solar Sector (2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Polysilicon Consolidation Fund | August 2025 | Led by key producers like GCL Technology, this planned $7 billion fund aims to acquire and idle up to a third of polysilicon capacity to stabilize collapsing prices caused by extreme oversupply. | Reuters |

Partnership Data: Global South Expansion Continues Amid Domestic Pressures

While grappling with domestic overcapacity, Chinese solar firms continued to secure strategic international partnerships, particularly in the Global South, reinforcing their roles as the world’s primary EPC contractors and equipment suppliers. These collaborations serve the dual purpose of creating export markets for surplus manufacturing capacity and advancing China’s geopolitical influence through energy diplomacy.

China’s Solar Exports Pivot to Global South

This chart is a perfect match, as its headline and data directly show the strategic shift in export destinations to the Global South, a core topic of this section.

(Source: Carbon Brief)

- In November 2024, Kuwait announced a partnership with Chinese firms for the Shagaya 3 and 4 solar plants. This USD 800 million project highlights the continued reliance of Gulf nations on Chinese technology and project execution expertise for their energy transition goals.

- Throughout 2024-2025, companies like LONGi, Jinko Solar, and Trina Solar were the dominant equipment suppliers for major renewable energy projects across the Gulf Cooperation Council (GCC) countries, embedding themselves in the region’s infrastructure plans.

- China’s strategy in Africa also evolved, with a noted shift from massive infrastructure projects to smaller, more socially impactful clean energy initiatives. This approach, discussed in the lead-up to the 2024 Forum on China-Africa Cooperation (FOCAC), aims to align Chinese capabilities with local development needs.

Table: Key International Solar Partnerships Involving Chinese Firms

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Kuwait Shagaya Solar Project | November 2024 | A joint venture between Kuwait and unspecified Chinese partners to develop the Shagaya 3 and 4 solar plants as an Independent Power Producer (IPP) project valued at approximately USD 800 million. | Energetica India |

| GCC Renewable Projects | 2024 – 2025 | Chinese manufacturers including LONGi and Jinko Solar served as primary equipment suppliers and EPC contractors for multi-billion dollar solar projects across the Gulf, cementing China’s role in the region’s energy transition. | Dentons |

| Africa Clean Energy Cooperation | 2024 | A strategic shift in China-Africa partnerships toward smaller, distributed solar projects designed to address energy access and social development, moving beyond a sole focus on large-scale infrastructure. | World Resources Institute |

Geography: China’s Solar Strategy Spans Domestic Megabases and Global Exports

China’s geographic strategy for solar is two-pronged, combining the development of massive domestic clean energy bases with a robust international export program that positions its companies as indispensable partners in the global energy transition. The immense domestic deployment, motivated by a national strategy to enhance energy security and achieve carbon neutrality goals, serves as the foundation for its global cost leadership and market dominance.

Provinces Exceed Solar Capacity Targets

This chart visually represents the “domestic megabases” strategy by showing how individual provinces are executing the massive, state-driven capacity build-out mentioned in the text.

(Source: Rystad Energy)

- Domestically, activity from 2021-2024 centered on building multi-gigawatt “megabases” in sun-rich western and northern provinces. Key examples include the 16 GW Kubiqi Desert and 10 GW Ulan Buh Desert projects in Inner Mongolia, designed to generate massive amounts of power for transmission to eastern industrial hubs.

- The period from 2025 onward saw a continued focus on these large-scale projects, complemented by a significant surge in distributed rooftop solar, which was a major driver of the 60 GW installed in Q 1 2025.

- Internationally, China solidified its role as the primary technology provider and EPC contractor for the Global South. Its deep involvement in projects across the Persian Gulf and Africa demonstrates a clear strategy to export its industrial capacity and secure long-term strategic influence.

Technology Maturity: From Commercial Scale to Efficiency Leadership

China’s solar technology has moved beyond achieving commercial scale to establishing clear leadership in next-generation efficiency and system integration. While the 2021-2024 period focused on scaling mature crystalline silicon technology, the 2025 landscape is defined by a race for higher efficiency and the deployment of complementary technologies like Concentrated Solar Power (CSP) to address grid stability.

Chinese Firms Dominate 2024 PV Module Shipments

This chart provides direct evidence for the section’s claim that China achieved “commercial scale,” showing how its firms dominate global shipments, which is the foundation for the subsequent pivot to efficiency leadership.

(Source: PV Tech)

- The 2021-2024 period was characterized by the mass production of PERC (Passivated Emitter and Rear Cell) modules, which became the global standard.

- In 2025, the competitive focus shifted decisively to higher-efficiency technologies. LONGi demonstrated this by achieving a 24.8% efficiency rating for its new Hi-MO 9 module, based on advanced HPBC technology, pushing the performance boundaries for commercially available products.

- Alongside PV advancements, China showed a sustained state-backed commitment to Concentrated Solar Power (CSP). The connection of 9 new CSP projects in 2025, bringing the national total to 27, highlights a strategic investment in dispatchable solar power to complement intermittent PV generation and enhance grid reliability.

SWOT Analysis: China’s Solar Industry in 2026

China’s solar sector enters 2026 from a position of unparalleled strength but faces significant internal weaknesses stemming from its own success. The central challenge is transitioning from a strategy of building overwhelming capacity to one of managing it for sustainable, high-quality growth.

China’s Dominance in Solar Manufacturing

This chart is an ideal fit, as it visually quantifies the primary strength mentioned in the SWOT analysis: China’s “complete supply chain dominance” across all key manufacturing stages.

(Source: Coalition For A Prosperous America)

- Strengths: Complete supply chain dominance and massive economies of scale provide an unassailable cost advantage.

- Weaknesses: Systemic manufacturing overcapacity creates intense margin pressure and the risk of financial instability.

- Opportunities: Leading the next wave of high-efficiency technology and integrated energy solutions (PV+storage, CSP) offers a path to higher-value growth.

- Threats: The primary threat is a disorderly market correction within China, potentially leading to widespread bankruptcies and price wars that could disrupt the global market.

Table: SWOT Analysis for China’s Solar Sector (2021-2025)

| SWOT Category | 2021 – 2024 | 2025 | What Changed / Validated |

|---|---|---|---|

| Strengths | Rapidly scaling manufacturing capacity and achieving global cost leadership in polysilicon, wafers, cells, and modules. | Maintained over 80% control of the global supply chain; achieved 1, 200 GW of annual manufacturing capacity. | China’s strategy to use immense domestic scale to achieve global supply chain dominance was fully validated. |

| Weaknesses | Early signs of over-investment and intense domestic competition among dozens of manufacturers. | Manufacturing capacity reached nearly double global demand, leading to collapsing prices and margin pressure. | The risk of overcapacity materialized into a systemic market crisis, forcing a reactive response. |

| Opportunities | Exporting standard-issue modules to global markets; developing large-scale domestic projects. | Leading in high-efficiency tech (LONGi’s 24.8% module); expanding into BESS (Canadian Solar); growing CSP for dispatchable power. | The market focus shifted from selling commodity panels to providing higher-value, integrated technology solutions. |

| Threats | Potential for international trade friction and tariffs aimed at protecting domestic industries in other countries. | The primary threat became internal: a potential disorderly collapse of the polysilicon sector and a cascading price war. The planned $7 billion consolidation fund is a direct response to this threat. | The most immediate and significant threat shifted from external political risk to internal economic instability. |

Scenario Modelling: Consolidation is the Critical Path for 2026

The single most critical action for China’s solar sector in 2026 is the successful execution of its industry consolidation strategy. How it manages the immense overcapacity will determine not only the financial health of its domestic players but also the pricing and stability of the entire global solar market.

China’s Solar Capacity Growth Soared Through 2024

This chart provides the essential context for the scenario, visualizing the “immense overcapacity” created by exponential growth that makes industry consolidation the critical path for 2026.

(Source: CleanTechnica)

China’s Solar Investment Exploded Pre-2025

This chart directly supports a key point in the SWOT table, illustrating the massive “over-investment” that occurred prior to 2025, which is cited as a primary weakness.

- If this happens: If the $7 billion polysilicon fund and other state-guided consolidation efforts succeed in reducing excess capacity, the market will stabilize.

- Watch this: Monitor polysilicon and module spot prices throughout 2026. A stabilization or slight increase in prices would be the first signal of success. Also, watch for official announcements of mergers, acquisitions, or plant closures among second-tier manufacturers.

- These could be happening: A successful consolidation will accelerate the pivot to “high-quality growth.” Companies will compete more on technological superiority (efficiency, reliability) and integrated solutions rather than on price alone, solidifying the market position of leaders like LONGi, Jinko Solar, and Trina Solar.

Frequently Asked Questions

Why is China’s solar market facing a crisis if it’s so dominant?

The crisis stems from massive manufacturing overcapacity. In 2025, China’s manufacturing capacity reached 1,200 GW, which was nearly double the global installation demand of 650 GW. This vast surplus has led to collapsing prices, intense margin pressure, and significant financial risk for producers across the supply chain.

What is the main strategy China is using to solve this overcapacity problem?

The primary strategy is industry-led, state-influenced consolidation. The most significant initiative is a planned $7 billion fund by major polysilicon producers, including GCL Technology, to acquire and shut down up to one-third of the industry’s excess production capacity to stabilize prices.

Are Chinese solar companies still expanding internationally despite the domestic crisis?

Yes. While managing domestic overcapacity, Chinese firms are continuing to secure international partnerships, especially in the Global South. This serves the dual purpose of creating export markets for their surplus products and advancing geopolitical influence, as seen in major projects in Kuwait, the GCC region, and Africa.

How is solar technology in China evolving amidst these market changes?

The technological focus has shifted from scaling up production to leading in efficiency and system integration. Companies are moving beyond standard PERC modules to commercialize higher-efficiency technologies, such as LONGi’s Hi-MO 9 module with 24.8% efficiency. There is also a strategic investment in Concentrated Solar Power (CSP) to provide dispatchable power and improve grid stability.

According to the analysis, what is the single most important factor for the solar market in 2026?

The most critical factor is the successful execution of China’s industry consolidation strategy. Whether or not the industry can successfully manage and reduce its overcapacity will determine the financial health of Chinese producers and dictate the price stability of the entire global solar market.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.