European Solar 2026: Perovskite Tech Redefines Manufacturing and Project Economics

Commercial Adoption: Europe’s Shift from Giga-Projects to High-Efficiency Manufacturing

The European solar market is shifting its strategic focus from solely deploying large-scale PV farms to establishing technological sovereignty through next-generation perovskite-on-silicon cells, fundamentally altering the competitive landscape. This pivot from a scale-driven to a technology-driven model prioritizes power density and domestic manufacturing, creating new risks and opportunities for developers and investors.

- Between 2021 and 2024, market leadership was defined by the ability to develop and finance giga-scale projects, primarily in Iberia. Companies like Iberdrola demonstrated this with its 590 MW Francisco Pizarro plant in Spain, capitalizing on high solar irradiation and land availability to drive down the levelized cost of energy.

- The years 2024-2025 marked a turning point with Oxford PV’s achievement of a certified 25% conversion efficiency on a commercial-sized tandem solar cell. This milestone, coupled with the ramp-up of its Brandenburg, Germany factory, signals a viable path for Europe to compete on technology rather than on the price of conventional silicon panels.

- This technological advance introduces a significant risk for asset owners and developers committed to standard silicon technology, which typically offers 14-22% efficiency. Perovskite’s ability to generate more power per square meter is a decisive advantage in land-constrained European markets and will command premium pricing for high-value applications like rooftop and agrivoltaics.

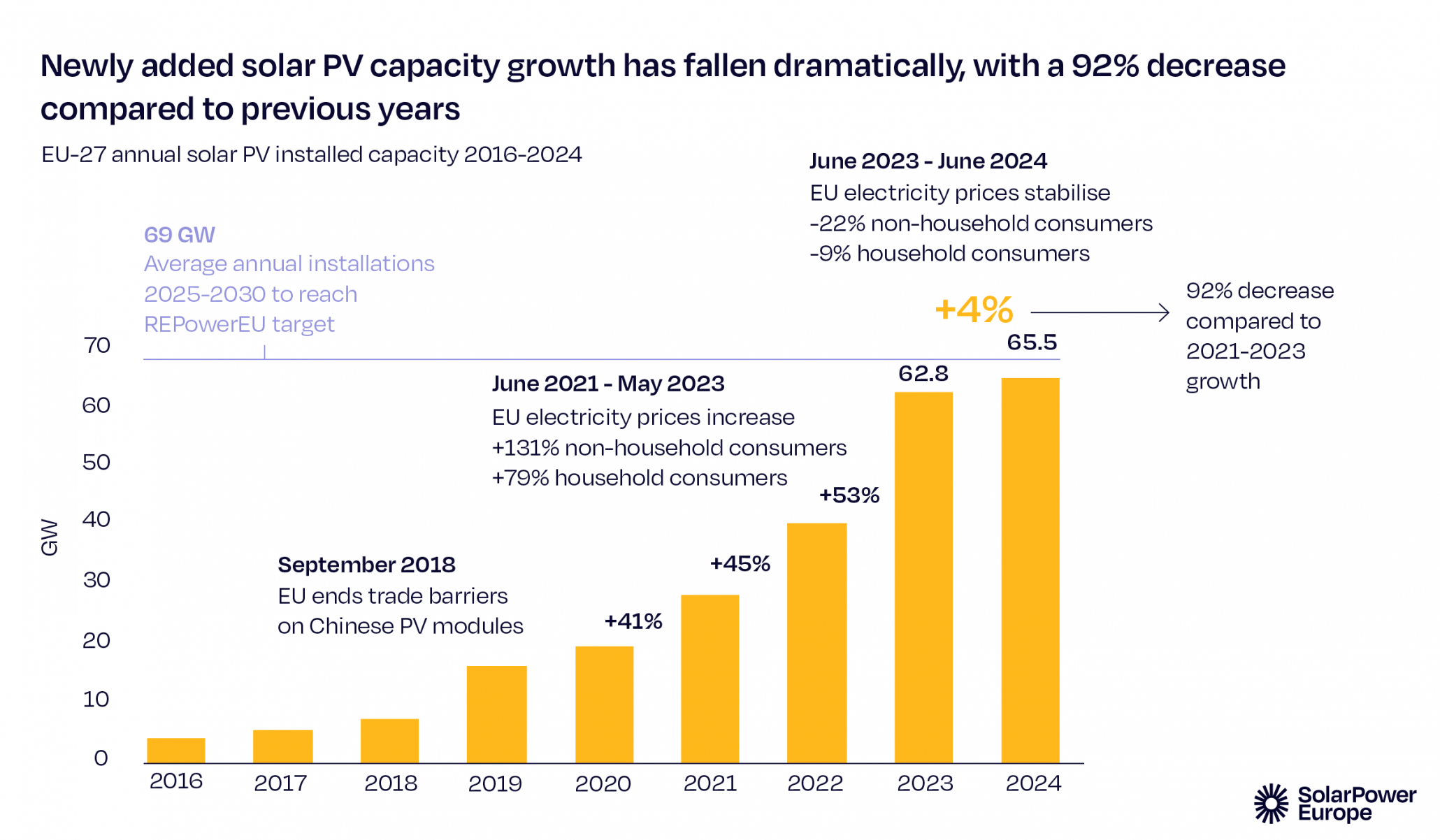

EU Solar Growth Rate Slows Dramatically

This chart perfectly illustrates the market disruption mentioned in the section, showing that the year-over-year growth rate fell sharply in 2024, reflecting the strategic shift from scale to technology.

(Source: PV Tech)

Investment Analysis: Funding Shifts to Technology Pioneers and Integrated Energy Hubs

Investment patterns in 2024-2025 reveal a dual focus: while substantial capital continues to flow into the execution of multi-gigawatt project pipelines, strategic funding is increasingly directed towards the commercialization of high-efficiency technologies and integrated energy systems.

- Financing for large-scale conventional solar projects remains robust, demonstrated by the €300 million European Investment Bank loan secured in 2025 to support the first phase of Aquila Clean Energy’s 1.2 GW Themis portfolio in Portugal.

- Hybrid projects that integrate solar with battery storage and green hydrogen are attracting major capital commitments due to their ability to provide grid stability. The planned €1 billion investment in the 1 GW Horizeo project by Engie and Total Energies in France exemplifies this trend.

- The successful operation of Oxford PV’s Brandenburg factory implies significant prior venture and strategic investment to move its technology from the lab to production. The company’s validated efficiency leadership positions it as a prime target for growth capital aimed at scaling production to rival incumbent silicon-based manufacturers.

Table: Key European Solar Investments and Financing (2024-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Themis Solar Portfolio (Aquila Clean Energy) | 2025 (Construction Start) | Secured a €300 million EIB loan for a 1.2 GW solar portfolio in Portugal, signaling strong institutional backing for giga-scale projects in Iberia. | Aquila Clean Energy |

| Horizeo (Engie/Total Energies) | 2025 (Construction Start) | A nearly €1 billion planned investment for a 1 GW hybrid project with storage and hydrogen, representing a strategic shift towards integrated energy hubs. | renews.biz |

| Joselillo Solar Plant (Prodiel/Everwood) | 2024-2025 (Construction) | Reached financial close with a €232 million package for a 495 MW portfolio, demonstrating continued investor appetite for large Spanish solar assets. | Prodiel |

| Francisco Pizarro (Iberdrola) | 2022 (Operational) | A benchmark €300 million investment for a 590 MW plant, proving the commercial viability of giga-projects financed through corporate PPAs. | Iberdrola |

Strategic Partnerships: Corporate PPAs and Joint Ventures Enable Solar Expansion

Strategic alliances, particularly long-term corporate Power Purchase Agreements (PPAs) and joint ventures between energy majors, are the primary commercial mechanisms for de-risking capital-intensive solar projects and facilitating the adoption of new technologies across Europe.

- Corporate PPAs have become essential for achieving project bankability in a subsidy-free environment. The 292 MWp Vendimia Solar Cluster, developed by Lightsource bp and operational in 2024, was enabled by a PPA with Amazon Web Services (AWS) to power its data centers.

- The successful development of Germany’s 650 MWp Witznitz Energy Park was underpinned by a 15-year PPA signed with Shell Energy Europe for a significant portion of its capacity, proving the model’s effectiveness even for the largest European projects.

- Joint ventures are critical for executing complex, integrated projects. The partnership between Engie and Total Energies to develop the 1 GW Horizeo project combines their respective expertise in renewables, grid services, and large-scale project management.

Table: Key European Solar Partnerships and Alliances (2024-2025)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Lightsource bp & AWS | Feb 2024 | A corporate PPA for the 292 MWp Vendimia Solar Cluster, highlighting the role of tech giants in underwriting new renewable capacity in Spain. | Lightsource bp |

| MOVE ON Energy & Shell | Mar 2024 | A 15-year PPA for 323 MW of capacity from the 650 MWp Witznitz Energy Park, enabling the subsidy-free construction of Europe’s largest solar park. | PV Magazine |

| Engie & Total Energies | 2025 (Target) | A joint venture to develop the 1 GW Horizeo project in France, demonstrating the collaboration required for complex, hybrid solar projects. | renews.biz |

| European Energy & Google | 2023-2024 | A PPA agreement to support the development of new solar projects, underscoring the trend of corporate buyers driving renewable energy growth in Denmark and Italy. | European Energy |

Geographic Focus: Iberia’s Project Dominance and Germany’s Tech-Manufacturing Nexus

While Spain and Portugal continue to dominate Europe’s giga-project pipeline due to superior solar resources and land availability, Germany is solidifying its position as the critical hub for next-generation solar manufacturing and technology commercialization.

Germany and Spain Lead EU Solar Additions

This chart directly validates the section’s geographic focus by showing Germany and Spain as the clear leaders in new solar capacity added in 2024, underpinning the Iberia-Germany nexus theme.

(Source: www.review-energy.com)

- From 2021 to 2024, Spain was the undisputed epicenter of large-scale solar development. It hosts a massive project pipeline from developers like Iberdrola and Solaria, including landmark projects such as the 590 MW Francisco Pizarro plant.

- Portugal has emerged as a key growth market, confirmed by Aquila Clean Energy’s plan to begin construction on its 1.2 GW Themis Solar Project in 2025, one of the largest planned portfolios on the continent.

- Germany represents the strategic pivot toward technology. It is not only home to Europe’s largest operational solar park (Witznitz, 650 MW) but, more importantly, hosts Oxford PV’s pioneering Brandenburg factory and the influential Fraunhofer ISE research institute, making it the center of Europe’s push for technological sovereignty.

Technology Maturity: Perovskite Tandem Cells Enter Commercialization

Perovskite-on-silicon tandem cell technology has officially transitioned from the laboratory to initial commercial production, representing the most significant technological disruption to the solar industry in over a decade and directly challenging the dominance of conventional silicon.

New Solar Panels Approach 25% Efficiency

This table directly supports the section’s narrative on technology maturity by listing new commercial panels with efficiencies approaching the 25% benchmark mentioned in the text.

(Source: Clean Energy Reviews)

- Before 2024, the utility-scale market was exclusively served by mature monocrystalline silicon PV technology, where commercial panel efficiencies plateaued in the 20-22% range and competition was primarily based on manufacturing cost.

- The year 2024 was a critical validation point. Oxford PV achieved a certified 25% conversion efficiency on a commercial-sized cell, proving the technology is ready for mass production and deployment. This is a substantial leap, not an incremental improvement.

- While advanced lab-scale results, such as the 27% efficiency achieved by University of Oxford researchers in August 2024, indicate further potential, the immediate commercial challenge is scaling manufacturing to compete on volume and bankability against deeply entrenched silicon supply chains.

SWOT Analysis: Competitive Dynamics in European Solar 2026

The European solar market’s strengths in policy and innovation are creating a clear opportunity to reclaim manufacturing leadership, though this is counter-balanced by persistent infrastructure weaknesses and the threat of established, low-cost competition from Asia.

China Dominates 2024 Global Solar Market

This chart quantifies the primary competitive ‘Threat’ mentioned in the SWOT analysis, showing China’s 55% share of the global market, which puts the European situation in a global context.

(Source: Lightsource bp)

Table: SWOT Analysis for the European Solar Market

| SWOT Category | 2021 – 2023 | 2024 – 2025 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strengths | Strong policy support (EU Green Deal); high solar irradiation in Southern Europe; mature project development ecosystem. | Aggressive policy targets (REPower EU); validated R&D leadership with commercial-ready perovskite technology. | European R&D leadership was validated as commercially viable with Oxford PV’s 25% efficiency record, moving from theoretical advantage to a tangible product. |

| Weaknesses | Heavy reliance on Asian supply chains for silicon wafers and cells; slow and complex permitting processes. | Grid connection queues emerge as a primary bottleneck; skills shortages for installation workforce (target of 1 M by 2025). | The weakness in domestic manufacturing is now being directly addressed by the commercialization of perovskite, though grid limitations have become a more acute problem. |

| Opportunities | Growth of corporate PPAs; development of large-scale projects in Spain and Portugal; falling LCOE of solar. | Establishment of a high-value, domestic manufacturing base for perovskite; growth of hybrid projects (solar+storage); agrivoltaics. | The opportunity shifted from simply installing more panels to manufacturing higher-value panels, creating a new competitive vector beyond just price-per-watt. |

| Threats | Competition from low-cost Asian PV module imports; potential for social opposition to large land-use projects. | Incumbent Asian manufacturers could accelerate their own tandem cell R&D; grid instability from high intermittent renewable penetration. | The threat of Asian market dominance remains, but now Europe has a distinct technological counter-strategy instead of attempting to compete on the same commoditized product. |

2026 Outlook: The Race to Scale High-Efficiency Solar Manufacturing

The primary strategic imperative for 2026 is whether European innovators can scale perovskite manufacturing fast enough to capture significant market share from incumbent silicon technologies before global competitors replicate the technology and erase Europe’s current lead.

European Solar Market Forecasted to Hit $194B

This forecast quantifies the massive market potential discussed in the 2026 outlook, underscoring the economic stakes of the ‘race to scale’ high-efficiency manufacturing.

(Source: Market Data Forecast)

- If Oxford PV’s Brandenburg factory successfully ramps up production and its high-efficiency panels demonstrate strong field performance and bankability, watch for a wave of new investment into European advanced solar manufacturing and a clear developer preference for these panels in land-constrained or high-value projects.

- A critical signal to monitor in 2025-2026 will be the announcement of the first utility-scale (100 MW+) solar farm built exclusively with European-made perovskite-on-silicon tandem cells. This event would validate the technology’s bankability and operational reliability at scale.

- Conversely, if production scaling proves too costly or slow, or if reliability issues emerge, the market will continue on its current trajectory. This scenario would see growth dominated by giga-projects using imported silicon panels, reinforcing the market leadership of large-scale developers like Iberdrola and Lightsource bp who have mastered the logistics and financing of the incumbent model.

Frequently Asked Questions

What is the main strategic shift happening in the European solar market?

The European solar market is shifting from a scale-driven model, focused on building massive PV farms with conventional technology (like in 2021-2023), to a technology-driven model. This new strategy prioritizes establishing domestic manufacturing of high-efficiency perovskite-on-silicon cells to gain technological sovereignty and compete on power density rather than just the cost of imported panels.

Why is perovskite-on-silicon technology considered a game-changer?

Perovskite-on-silicon technology is a game-changer because it offers a significant leap in conversion efficiency. The article highlights Oxford PV’s achievement of a certified 25% efficiency, far exceeding the 14-22% offered by standard silicon. This ability to generate more power per square meter is a decisive advantage in land-constrained European markets and for high-value applications like rooftops.

Are large-scale ‘giga-projects’ still a major focus for investment?

Yes, large-scale projects continue to attract major investment. The article notes that while strategic funding is moving towards technology, substantial capital is still flowing into giga-projects. This is demonstrated by the €300 million EIB loan for Aquila Clean Energy’s 1.2 GW Themis portfolio in Portugal and the planned €1 billion investment in the 1 GW Horizeo project in France.

How are companies financing these large, capital-intensive solar projects without subsidies?

Companies are primarily using corporate Power Purchase Agreements (PPAs) to finance projects in a subsidy-free environment. A large corporate buyer, like Amazon Web Services (AWS) or Shell Energy Europe, commits to purchasing the electricity for a long term (e.g., 15 years). This guaranteed revenue stream makes the project ‘bankable,’ allowing developers to secure loans and investment for construction.

What is the biggest risk or challenge to Europe’s new perovskite-focused solar strategy?

The biggest challenge is whether European companies can scale up manufacturing of the new perovskite technology fast enough to capture market share. The article identifies a key threat: incumbent Asian manufacturers could accelerate their own R&D, replicate the technology, and erase Europe’s current lead before it can establish a strong, high-volume production base.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.