Corporate Solar Scaling in 2026: Why Portfolio Procurement is the New Standard

The Shift to Portfolio Procurement: Analyzing Corporate Solar Projects in 2026

Hyperscale corporate energy procurement has fundamentally shifted from transactional, single-project power purchase agreements (PPAs) to strategic, multi-gigawatt portfolio-based partnerships. This evolution is driven by the operational necessity to secure massive volumes of reliable, clean power for AI infrastructure, forcing corporations to act as active enablers of new generation rather than passive buyers. The change is evident when contrasting procurement patterns before and after 2025.

- Before 2025, corporate strategies often involved signing individual PPAs with various developers to meet renewable energy targets, such as Meta’s 200 MW wind deal with Trans Alta in 2022. This approach, while effective for incremental additions, lacked the scale and risk mitigation required for exponential demand growth.

- From 2025 onward, the model evolved into programmatic, portfolio-level agreements with select partners. The expanded partnership between Meta and Zelestra, totaling nearly 1.2 GWdc across seven U.S. projects, exemplifies this, providing the developer with revenue certainty to build new assets and giving the offtaker a diversified supply.

- This new strategy directly enables the financing and construction of new assets, moving beyond simple renewable energy credit (REC) purchases. For example, Meta’s offtake commitment was critical for Zelestra to secure a $113 million green financing package for its 81 MW Jasper County Solar Project in Indiana.

- The scope of these portfolios now frequently includes integrated technologies to address intermittency. The Zelestra partnership includes a hybrid facility with a 400 MWh battery energy storage system (BESS), signaling a move from matching annual consumption to ensuring 24/7 reliable power for data centers.

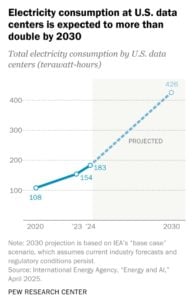

Data Center Demand Drives Procurement Shift

This chart illustrates the massive growth in data center power demand, which is the primary driver for the strategic shift to portfolio procurement discussed in this section.

(Source: CarbonCredits.com)

Investment Analysis: How Offtake Agreements De-Risk New Solar Development

Large-scale corporate offtake commitments have become the primary financial instrument for de-risking and accelerating new utility-scale solar development. These long-term agreements provide the guaranteed revenue stream developers need to secure project financing, transforming corporate buyers into anchor financiers for grid expansion. This mechanism is visible in the series of major project investments backed by Meta’s procurement strategy.

Solar Capacity Grows on De-Risked Investment

This forecast of rising solar capacity visualizes the successful outcome of financial de-risking mechanisms, like corporate offtake agreements, that are enabling new project development.

(Source: CarbonCredits.com)

Table: Key Solar Project Investments Enabled by Corporate Offtake (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Enbridge / Clear Fork Solar | July 2025 | $900 million investment in a 600 MW solar project in Texas. The project is explicitly designed to support Meta’s nearby data center operations, directly matching local load with new renewable generation. | Enbridge Powers Meta Data Centers with $900 M Texas Solar Investment |

| Zelestra / Jasper County Solar | April 2025 | Secured a $113 million green financing package from Banco Santander for an 81 MW solar project. The financing was contingent on the long-term Environmental Attribute Purchase Agreement (EAPA) with Meta. | Zelestra Secures $113 Million Green Financing |

| Engie / Swenson Ranch Solar | October 2025 | Meta contracted 100% of the renewable energy from this new $900 million project in Texas, part of a larger 1.3 GW partnership. This offtake enabled the large-scale project to move forward. | Meta Buys 100% of Renewable Energy from New $900 Million… |

Partnership Dynamics: Building a Diversified Developer Ecosystem for Solar Scaling

To mitigate supply-side risk and ensure access to a continuous pipeline of projects, hyperscalers are building a diversified ecosystem of development partners rather than relying on a single provider. This strategy fosters a competitive environment and provides flexibility to procure capacity across different regions and project timelines. Meta’s approach, which includes a nearly 1.2 GWdc portfolio with Zelestra alongside even larger agreements with other developers, is the archetype for this model.

Table: Comparative Analysis of Meta’s U.S. Clean Energy Partnerships (2025-2026)

| Partner / Project | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Multiple Nuclear Partners | February 2026 | Agreements to secure up to 6.6 GW of nuclear power. This strategic pivot aims to add firm, baseload clean power to its portfolio to support 24/7 AI data center operations. | Meta Secures Up To 6.6 GW Nuclear Power… |

| Next Era Energy Resources | December 2025 | Agreement to develop approximately 2.5 GW of new clean energy capacity across 13 U.S. sites. This represents a large-scale, multi-project buildout to power expanding data infrastructure. | Meta, Next Era Agree 2.5 GW Clean Energy Buildout… |

| Zelestra | February 2026 | Expanded partnership to nearly 1.2 GWdc across seven projects, including the 176 MWdc Skull Creek Solar Plant. This demonstrates a deep, programmatic relationship with a trusted developer. | Zelestra Expands Relationship with Meta… |

| Invenergy | December 2024 | Agreement for over 760 MW in renewable energy from four U.S. projects. This partnership adds another major independent power producer to Meta’s diversified developer ecosystem. | Invenergy to Provide over 760 MW in Renewable Energy… |

Geographic Strategy: Concentrating Solar Procurement in Key Data Center Hubs

Corporate solar procurement is now geographically concentrated in regions that offer a combination of high-quality solar resources and significant data center load, such as Texas. This clustering strategy aims to match energy generation with consumption more effectively, reduce transmission costs, and directly support the local grids where operational demand is highest. The heavy focus on Texas across multiple partnerships validates this approach.

- Between 2021 and 2024, procurement was geographically diverse but often followed resource availability, with projects spread across markets like the Midwest and Southeast. For example, Meta’s partnership with Silicon Ranch involved a $2.3 billion investment across seven new projects in Georgia.

- From 2025 to today, there is a clear strategic consolidation in Texas’s ERCOT market, which is a major hub for both data centers and solar development. Meta’s deals with Zelestra (720 MWdc), Enbridge (600 MW), and Engie (Swenson Ranch) are all located in Texas.

- This regional focus allows companies to hedge against price volatility within a specific electricity market and claim more direct responsibility for decarbonizing the grid that powers their facilities. The 176 MWdc Skull Creek Solar Plant, part of the Zelestra portfolio, is another key asset supporting Meta’s Texas operations.

Technology Maturity: Expanding from Solar to Firm Power for 24/7 Reliability

The corporate procurement model is maturing beyond acquiring intermittent renewables to meet annual targets and is now focused on building a portfolio that can provide reliable, carbon-free energy on a 24/7 basis. While solar remains a cornerstone, its limitations are driving hyperscalers to integrate storage and explore firm power technologies like nuclear to meet the constant energy demand of AI workloads. This technological expansion marks a significant step-change in strategic maturity.

- In the 2021-2024 period, the primary focus was on acquiring large volumes of solar and wind capacity. Deals like the one with D. E. Shaw Renewable Investments for 400 MWac of solar were typical, aiming to maximize renewable megawatt-hours.

- The period from 2025 to today shows a clear pivot toward solving for intermittency. The inclusion of battery storage in solar projects, as seen with Zelestra, became more common.

- The most significant shift in 2026 is the aggressive exploration of firm, clean power. Meta’s pursuit of up to 6.6 GW of nuclear power is a definitive signal that solar and wind alone are considered insufficient to power the next generation of AI infrastructure, requiring a technology-agnostic “all-of-the-above” clean energy strategy.

SWOT Analysis: Corporate Solar Portfolio Strategy

The evolution of corporate solar strategy from single-asset procurement to portfolio-based partnerships presents a new set of strategic considerations. The shift, driven by the intense energy demands of AI, creates new strengths and opportunities but also exposes companies to different risks and threats related to grid capacity and technology integration. A SWOT analysis clarifies the changes between the pre-2024 and post-2025 periods.

Table: SWOT Analysis for Portfolio-Based Corporate Solar Procurement

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Resolved / Validated |

|---|---|---|---|

| Strength | Achieved 100% renewable energy goals on an annual matching basis through large-volume PPAs with partners like Silicon Ranch and Apex Clean Energy. | Ability to de-risk and enable gigawatts of new generation through long-term portfolio commitments with developers like Zelestra and Next Era. | The strategy shifted from being a passive buyer to an active enabler of new infrastructure, giving corporations more control over their energy supply chain. |

| Weakness | High exposure to the intermittency of solar and wind, creating a mismatch between generation profiles and 24/7 data center load. | Increased concentration risk in specific grid regions (e.g., ERCOT in Texas), making the portfolio vulnerable to localized congestion, curtailment, and extreme weather events. | The problem of intermittency was validated, forcing a search for solutions. However, geographic concentration introduced a new form of systemic risk. |

| Opportunity | Leverage massive buying power to secure favorable PPA pricing for individual solar and wind projects. | Use balance sheet and long-term demand to anchor development of firm, clean power technologies like next-generation geothermal and nuclear (e.g., 6.6 GW nuclear pursuit). | The opportunity grew from optimizing cost on mature technologies to catalyzing the commercialization of emerging technologies needed for 24/7 carbon-free power. |

| Threat | Volatility in wholesale electricity markets and potential for rising PPA prices due to supply chain constraints. | The exponential energy demand from AI outpaces the grid’s capacity for interconnection and transmission, creating a structural bottleneck for new projects. | The primary threat shifted from price volatility to the physical limitations of the grid itself, which has become the main constraint on corporate clean energy ambitions. |

Scenario Modelling: The Future of Hyperscale Energy Procurement

If the exponential growth in AI-driven energy demand continues to outpace grid development, watch for hyperscalers to evolve from being anchor offtakers to becoming direct investors or owners of generation assets. This vertical integration would represent the final step in securing their energy supply chain. Current signals strongly suggest this trajectory is not only possible but likely.

- If this happens: Corporate entities will establish energy subsidiaries or joint ventures with utilities and infrastructure funds to directly develop, finance, and operate power plants, including solar, storage, and nuclear facilities.

- Watch this: The outcome of Meta’s exploration of 6.6 GW of nuclear power. A commitment of this magnitude would signal a definitive move from procurement to direct infrastructure enablement and potentially ownership.

- These could be happening: Other hyperscalers will follow suit, issuing RFPs for firm power and exploring direct equity stakes in generation projects. This will fundamentally alter the structure of energy markets, with a handful of large tech companies controlling a significant portion of new clean energy development.

Frequently Asked Questions

Why are large corporations like Meta changing their strategy for buying clean energy?

Corporations are shifting from buying power from single projects to creating large, multi-project portfolio partnerships. This change is driven by the massive, reliable power demands of new AI infrastructure, which forces them to become active enablers of new energy generation to secure the necessary volume and reliability.

What is ‘portfolio procurement’ and how is it different from the old method?

Portfolio procurement is a strategy where a corporation establishes a large-scale, multi-project partnership with a developer for gigawatts of power. It differs from the old method of signing individual, transactional Power Purchase Agreements (PPAs) for single projects. The portfolio approach gives the developer revenue certainty to build multiple new assets and provides the buyer with a large, diversified supply.

How do these corporate energy deals help new solar projects get built?

Large corporate offtake commitments act as a financial guarantee. They provide a long-term, predictable revenue stream for the project developer, which de-risks the investment for lenders. This guarantee is often essential for developers to secure the project financing needed for construction, effectively turning corporate buyers into anchor financiers for new solar farms.

The article says solar alone isn’t enough. What other technologies are companies adding to their portfolios?

To ensure reliable 24/7 power for data centers, companies are moving beyond just solar. They are integrating battery energy storage systems (BESS) to address intermittency, as seen in the Zelestra partnership. More significantly, they are pursuing firm, clean power sources like nuclear energy, with Meta exploring up to 6.6 GW of nuclear to provide constant, carbon-free baseload power.

What is the biggest risk or challenge with this new portfolio-based strategy?

The primary threat has shifted from market price volatility to the physical limitations of the electrical grid. The rapid growth in energy demand from AI is outpacing the grid’s capacity for interconnection and transmission, creating a major bottleneck for bringing new clean energy projects online. Additionally, concentrating projects in a single region like Texas increases vulnerability to localized grid congestion and extreme weather.

Experience In-Depth, Real-Time Analysis

For just $200/year (not $200/hour). Stop wasting time with alternatives:

- Consultancies take weeks and cost thousands.

- ChatGPT and Perplexity lack depth.

- Googling wastes hours with scattered results.

Enki delivers fresh, evidence-based insights covering your market, your customers, and your competitors.

Trusted by Fortune 500 teams. Market-specific intelligence.

Explore Your Market →One-week free trial. Cancel anytime.