Bloom Energy SOFC Deals, $7.65 B in Contracts, 2.8 GW Oracle Agreement, and 11 Partnerships (2021 to 2026)

SOFC Application Shift, Bloom Energy Focus on Data Center Power

The Solid Oxide Fuel Cell (SOFC) market has pivoted from a technology seeking broad applications to one dominated by a single, high-urgency use case: providing on-site power for grid-constrained AI data centers. This shift marks a clear divergence from the prior period (2021-2024), which saw more diversified and tentative commercial exploration across transportation and industrial sectors. Now, the market is defined by players who can deliver multi-megawatt solutions at speed, a requirement that has elevated specialized stationary power providers while sidelining others.

- Between 2021 and 2024, the fuel cell narrative included significant efforts in the transportation sector, with companies like Honda and GM collaborating on automotive solutions. However, by 2026, these major automakers demonstrably retreated from hydrogen truck programs, citing persistent cost and infrastructure challenges.

- In contrast, 2025-2026 has been defined by Bloom Energy’s singular focus on the data center market. The company capitalized on the “speed-to-power” imperative, where the five-plus year timeline for utility grid upgrades is misaligned with the immediate power needs of AI, creating a massive commercial opening.

- The primary market driver is no longer just decarbonization but grid reliability and rapid deployment. Bloom Energy’s ability to install its SOFC Energy Servers in as little as three months provides a critical advantage for hyperscalers needing to bring new AI capacity online quickly.

- While data centers dominate, niche industrial and marine applications continue to develop. Collaborations involving companies like MODEC and Doosan Fuel Cell are advancing SOFCs for maritime power, but these remain at a pilot scale compared to the gigawatt-level commercial deployments in data centers.

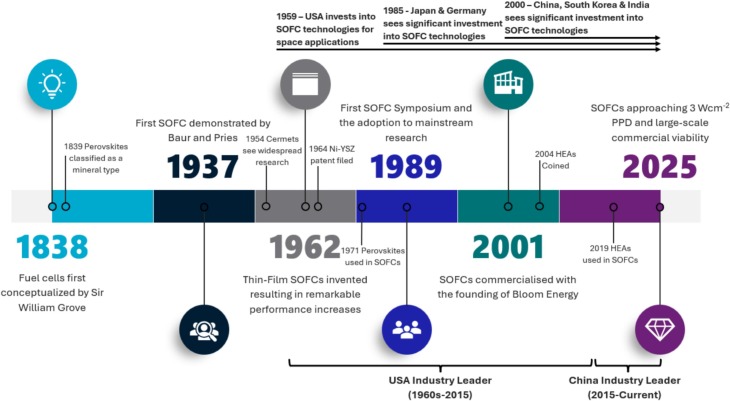

Timeline Tracks SOFC Path to Commercial Viability

This timeline provides historical context for the article’s main point, showing the key milestones that led to the SOFC market’s current pivot to large-scale commercial applications.

(Source: ScienceDirect.com)

$7.65 B in Deals, Bloom Energy Contrasts with Automotive Cancellations

Financial flows in the fuel cell market show a dramatic reallocation of capital away from transportation and toward stationary power infrastructure. While the 2021-2024 period saw continued R&D investment across multiple sectors, 2025-2026 is marked by landmark, multi-billion-dollar procurement contracts for data center power, juxtaposed with the cancellation of high-profile automotive commercialization programs. This bifurcation signals investor confidence in the proven business case for SOFCs in stationary applications over the speculative path for fuel cell electric vehicles (FCEVs).

- Bloom Energy secured an estimated $7.65 billion in data center deals in a 90-day period during early 2026, validating the immense commercial value of its on-site power solutions for the AI industry.

- In contrast, March 2026 reports confirmed the withdrawal of GM, Honda, Stellantis, and Daimler from hydrogen truck initiatives, effectively halting major commercial investment in that segment and ceding momentum to stationary power.

- Even as automotive players pull back, investment in SOFC manufacturing capacity is growing. Competitor Elcogen secured €50 million in February 2026 for a new factory in Estonia, indicating broader European investor interest in scaling the technology for clean energy goals.

Table: Comparative Commercial Events, Stationary vs. Automotive (2026)

| Entity / Sector | Time Frame | Details and Strategic Purpose | Source |

|---|---|---|---|

| Bloom Energy / Stationary Power | Apr 2026 | Signed supply agreement with Oracle for up to 2.8 GW of SOFC systems to power AI data centers, a massive expansion of their existing partnership. | Data Center Dynamics |

| GM, Honda / Automotive | Mar 2026 | Major automakers, including GM and Honda, withdrew from hydrogen truck programs, signaling a strategic retreat from FCEV commercialization due to cost and infrastructure hurdles. | [PDF] J.P. Morgan Asset Management |

| Bloom Energy / Stationary Power | Jan 2026 | Secured a $2.65 billion agreement with American Electric Power (AEP) to deploy up to 1 GW of SOFCs for data center sites across 11 US states. | Fuel Cells Works |

| Elcogen / Manufacturing | Feb 2026 | Received a €50 million investment for a new SOFC factory in Estonia, signaling growing European commitment to scaling SOFC production capacity. | Journal of Solid State Electrochemistry |

Bloom Energy 2 Major Data Center Deals, Oracle and AEP (2026)

Strategic partnerships in 2026 have solidified the SOFC market structure, creating two distinct models: vertically integrated, large-scale deployment and technology licensing for regional or niche applications. Bloom Energy’s alliances with hyperscalers and utilities exemplify the former, built on delivering complete, turnkey power solutions. The latter is represented by technology developers like Ceres Power, which partner with large industrial players to integrate their core SOFC technology into different end markets.

- The partnership between Bloom Energy and Oracle, expanded in April 2026 to include up to 2.8 GW of capacity, is the defining commercial agreement in the sector. It establishes SOFCs as a core infrastructure component for AI build-outs.

- Bloom’s $2.65 billion deal with utility AEP demonstrates a new partnership model where a utility procures SOFCs as a grid asset specifically to serve the power-intensive data center industry in its territory.

- In Europe, the partnership between Centrica and Ceres Power highlights a technology-licensing strategy. Centrica will leverage its market access and energy service expertise to deploy Ceres’ SOFC technology to industrial customers.

- In the marine sector, a letter of intent between Doosan Fuel Cell, Shell, and KSOE aims to develop SOFCs for shipping, bringing together a manufacturer, an energy major, and a shipbuilder to tackle a nascent market.

North America vs Asia, Bloom Energy SOFC Market Penetration

The geographic distribution of SOFC commercial activity has become highly concentrated in North America, driven almost exclusively by the region’s massive data center construction pipeline and corresponding grid limitations. While Asia and Europe remain important markets for SOFC technology development and industrial partnerships, the scale of commercial deployment in the U.S. during 2025-2026 far surpasses activity elsewhere. This reflects a market shaped by regional infrastructure constraints rather than uniform global adoption trends.

- North America is the undisputed center of gravity for large-scale SOFC deployment, confirmed by Bloom Energy’s multi-gigawatt agreements with US-based Oracle and the multi-state utility AEP. This activity is a direct response to power shortages in key data center hubs like Northern Virginia.

- In Asia, the strategy is focused on market entry through partnership and localization. Bloom Energy’s January 2026 Mo U to expand into the South Korean data center market and Elcogen’s Mo U with JNK India target regional growth through local industrial partners.

- Europe’s focus is on building a domestic manufacturing base and fostering industrial decarbonization. The €50 million investment in Elcogen’s Estonian factory and the Centrica-Ceres partnership are geared toward serving the European industrial and commercial power market.

SOFC Commercial Scale, Bloom Energy vs Emerging Marine Applications

The technological maturity of SOFCs in 2026 is best described as commercially proven at scale for one specific application, while remaining in pilot or R&D phases for others. Bloom Energy’s Energy Server platform has achieved a level of operational validation, signified by a 40, 000-hour runtime and deployments at a 20 MW campus scale, that sets it apart. This contrasts with the 2021-2024 period, where SOFCs were often discussed alongside less mature fuel cell variants as part of a broader, future-facing technology bucket.

Diagram Explains Core Solid Oxide Fuel Cell Technology

This diagram illustrates the fundamental science of SOFCs, providing essential background for the section’s discussion on the technology’s proven maturity and scale.

(Source: ScienceDirect.com)

- Bloom Energy’s SOFC platform is a fully commercialized product deployed at the gigawatt scale, backed by a mature manufacturing process. Its success in 2026 is not based on a technological breakthrough but on the mass production and deployment of a proven system.

- In contrast, marine applications of SOFCs remain in the early commercial or pilot stage. The collaboration between MODEC, Eld Energy, and Delta for a 120 k W system on an FPSO vessel is an important validation project, but it highlights the nascent state of the market compared to stationary power.

- Advanced concepts like reversible solid oxide cells (r SOCs), which offer potential for energy storage, continue to be a focus of academic and industry research. However, they are pre-commercial and not a factor in the current market dynamics defined by immediate power generation needs.

Bloom Energy SWOT Analysis, Strengths and Market Threats (2021 to 2026)

The strategic position of the SOFC market has been clarified and strengthened between 2021 and 2026, primarily by finding a high-value, urgent application in data center power. This has amplified the technology’s core strengths in reliability and efficiency while also exposing new risks related to supply chain concentration and high customer dependency.

Table: SWOT Analysis for SOFC Commercial Traction (2021-2026)

| SWOT Category | 2021 – 2024 | 2025 – 2026 | What Changed / Validated |

|---|---|---|---|

| Strengths | High electrical efficiency, fuel flexibility, low emissions profile. Technology was seen as a promising but niche clean energy solution. | Proven reliability (40, 000-hour runtime), rapid deployment timeline (3 months), and modular scalability. Established as critical infrastructure for AI. | The value proposition shifted from environmental benefits to business continuity and speed-to-power, which was validated by multi-billion-dollar data center contracts. |

| Weaknesses | High capital cost compared to conventional power. Lack of manufacturing scale and a clear, large-scale addressable market. | Lower initial margins on large AI data center deals. High valuation multiples (P/E over 127) create investor pressure. Heavy reliance on the data center segment. | The “killer app” in data centers created a viable business model despite high costs, but it also concentrated market risk into a single, albeit massive, vertical. |

| Opportunities | Broad potential applications in transportation, industrial CHP, and distributed generation. Government subsidies for clean energy. | Explosive, grid-constrained power demand from AI. Multi-gigawatt utility-scale deployments (AEP). Expansion into international data center markets (South Korea Mo U). | The AI boom created an urgent, multi-billion-dollar market inflection point that did not exist in the prior period, transforming SOFCs from an option to a necessity for some users. |

| Threats | Competition from batteries and other fuel cell types (PEM). Slow development of hydrogen infrastructure for transportation applications. | Competition from other on-site power like gas engines. Potential for improvements in grid infrastructure to eventually reduce demand. Execution risk on a massive backlog. | The primary competitive threat shifted from other “green” technologies to established, conventional power generation solutions that can also provide on-site power. The exit of auto OEMs like Honda and GM removed FCEVs as a major competitive narrative. |

2027 Revenue Outlook, Bloom Energy Data Center Execution Risks

The critical factor to monitor for the SOFC market moving into 2027 is execution. If a key player like Bloom Energy successfully delivers on its massive backlog and achieves its aggressive revenue guidance of $3.1 billion for 2026, it will cement SOFCs as a permanent, mainstream component of critical power infrastructure. The trajectory is no longer about proving technological viability but about demonstrating the financial and operational capacity to deploy at an unprecedented scale.

- Watch Bloom Energy’s reported revenue and margins. Analysts have set high expectations, with price targets like Clear Street’s $68.00 based on projected revenue of $3.7 billion by 2027. Any failure to meet these targets could signal execution challenges.

- If grid constraints in key markets like North America and Europe persist or worsen, the demand for on-site SOFC power will likely accelerate further, validating the current investment thesis and potentially leading to even larger agreements.

- Monitor the progress of SOFC partnerships in industrial and marine sectors. While currently small-scale, successful pilot projects could open up the next significant growth verticals for the technology beyond data centers in the post-2027 timeframe.

- Observe the strategic moves of automakers like Honda and GM. A potential re-entry into fuel cells, perhaps focused on stationary power or heavy-duty transport, would signal a renewed belief in the technology’s viability beyond the challenging passenger vehicle market.

The questions your competitors are already asking

This report covers one angle of SOFC commercialization, focusing on the divergence between data center and transportation applications. The questions that matter most depend on your work.

- Which companies are gaining or losing ground in the SOFC market as the focus shifts from transportation to data centers?

- What is the outlook for SOFC deployment in grid-constrained AI data centers by 2030?

- Which hyperscale data center operators are adopting SOFCs to bypass long grid upgrade timelines?

- What is the commercial status of Honda-GM’s fuel cell ventures following their retreat from hydrogen trucks?

This report does not answer these. Enki Brief Pro does.

Your question, your angle, your framework. SWOT, PESTL, scenario modelling. The same niche depth, built around the decision your work actually depends on.